Elastic launches GPU-accelerated inference service for AI workflows

Introduction & Market Context

Whirlpool Corporation (NYSE:WHR) presented its first-quarter 2025 earnings results on April 24, 2025, highlighting margin expansion and organic growth despite headline revenue declines. The appliance manufacturer, which has been navigating a challenging macroeconomic environment, emphasized its strategic positioning to benefit from changing tariff policies and continued focus on product innovation.

The company’s stock has experienced significant volatility in recent months, with shares trading at $77.74 as of April 23, 2025, well below its 52-week high of $135.49. In premarket trading following the earnings presentation, the stock showed signs of recovery, up 2.02% to $79.31.

Quarterly Performance Highlights

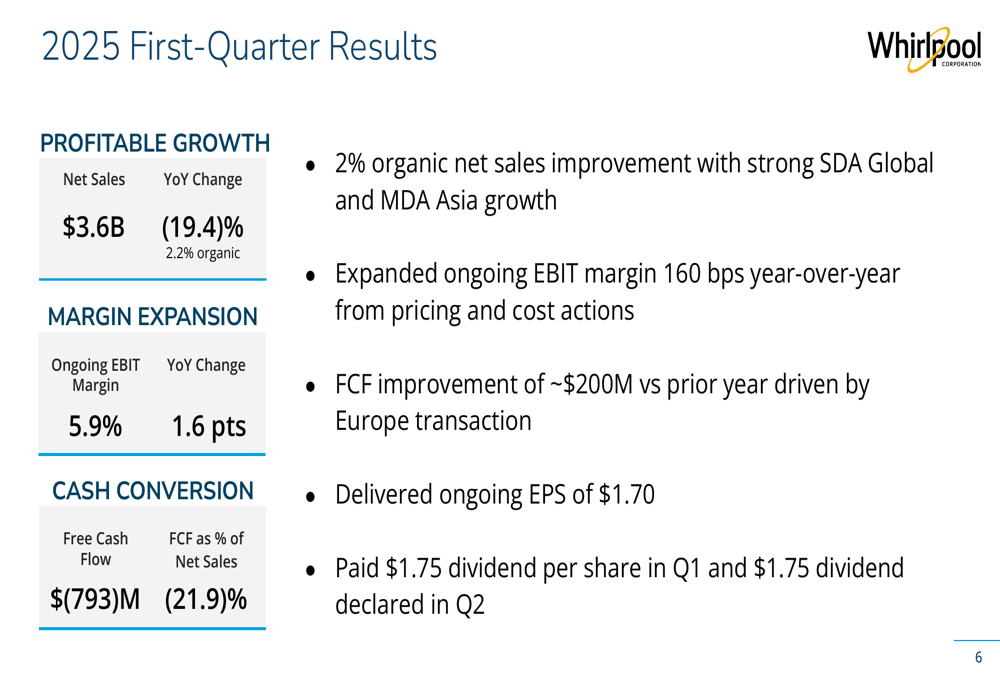

Whirlpool reported first-quarter 2025 net sales of $3.6 billion, representing a 19.4% year-over-year decline. However, the company emphasized that organic net sales increased by 2.2%, with strong performance in Small Domestic Appliances (SDA) Global and Major Domestic Appliances (MDA) Asia segments.

The company’s ongoing EBIT margin expanded to 5.9%, a 1.6 percentage point increase compared to the same period last year. This improvement was primarily driven by pricing actions and cost reduction initiatives. Free cash flow was negative at $(793) million, representing (21.9)% of net sales, though the company noted an improvement of approximately $200 million versus the prior year, attributed to the Europe transaction.

As shown in the following quarterly results summary:

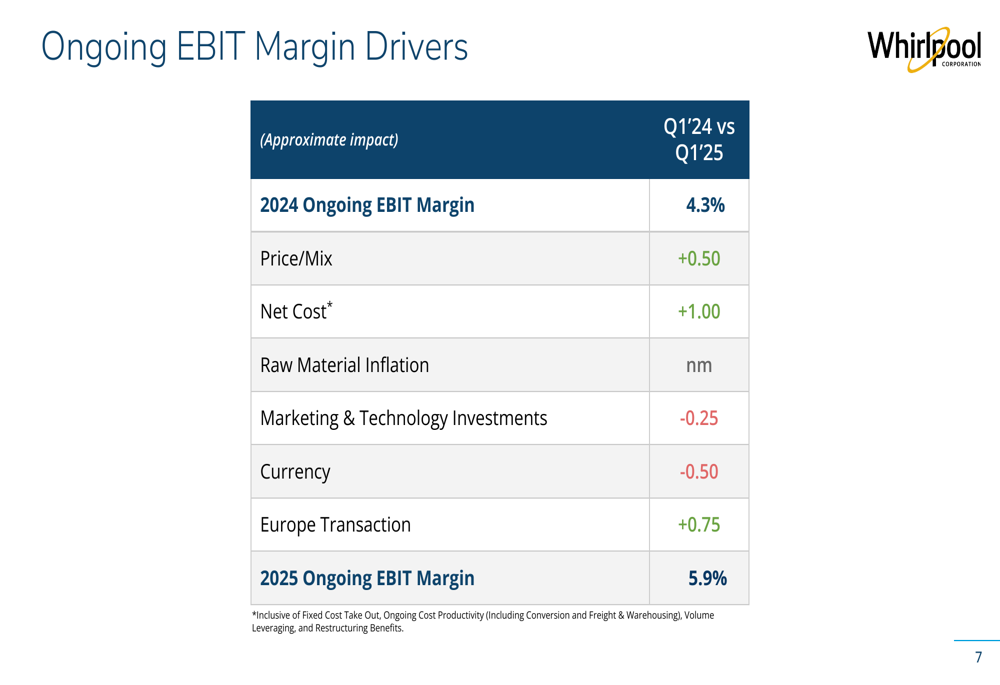

Breaking down the drivers of EBIT margin improvement, Whirlpool identified several key factors contributing to the 1.6 percentage point increase from Q1 2024 to Q1 2025:

Regional performance varied across segments. North America (NAR) delivered stable net sales despite declining consumer confidence and reported a 60 basis point margin improvement year-over-year. Latin America (LAR) saw net sales excluding currency increase by 2% year-over-year, while Asia achieved impressive 16% growth excluding currency effects, driven by strong volume from share gains and industry growth.

Tariff Impact and Competitive Positioning

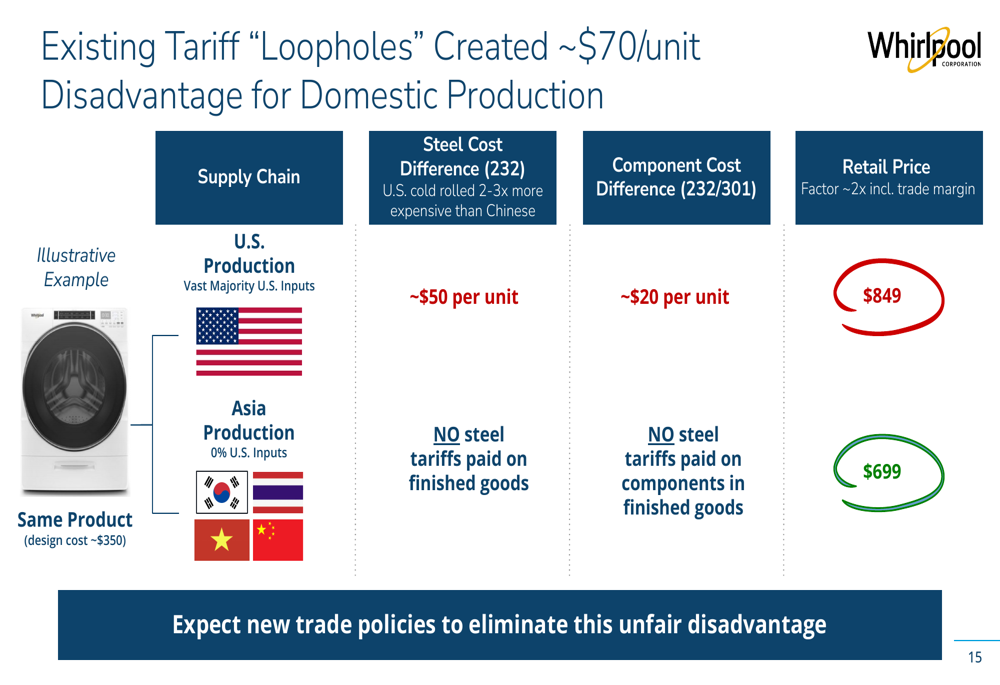

A significant portion of Whirlpool’s presentation focused on the changing tariff landscape and its potential impact on the company’s competitive position. Management highlighted that since 2020, Asian producers have exploited "loopholes" in existing tariffs, creating approximately a $70 per unit disadvantage for U.S.-made products.

The presentation detailed how these loopholes have created an uneven playing field, with U.S. production facing higher costs due to tariffs on raw materials that don’t apply to finished goods imported from Asia:

Whirlpool emphasized that with 80% domestic production, it stands to be a "NET winner" from new tariff policies that would eliminate these disadvantages. The company outlined several mitigating actions already underway, including pricing actions announced in April, supply sourcing evaluation, and implementation of tariff monitoring systems.

Strategic Initiatives and Product Innovation

Product innovation remains a key focus for Whirlpool, with plans for over 100 new product introductions in 2025. The company expects more than 30% portfolio turnover for MDA North America this year, showcasing examples of new launches across its brand portfolio:

These innovation efforts have already garnered industry recognition, with multiple products receiving awards at the Kitchen & Bath Industry Show (KBIS):

In addition to product innovation, Whirlpool outlined its capital allocation priorities for 2025, which include investing approximately $450 million in capital expenditures to fund organic growth, paying down approximately $700 million of debt, and maintaining its dividend commitment. The company noted that share buybacks or value-creating M&A are not priorities for 2025.

Forward-Looking Guidance

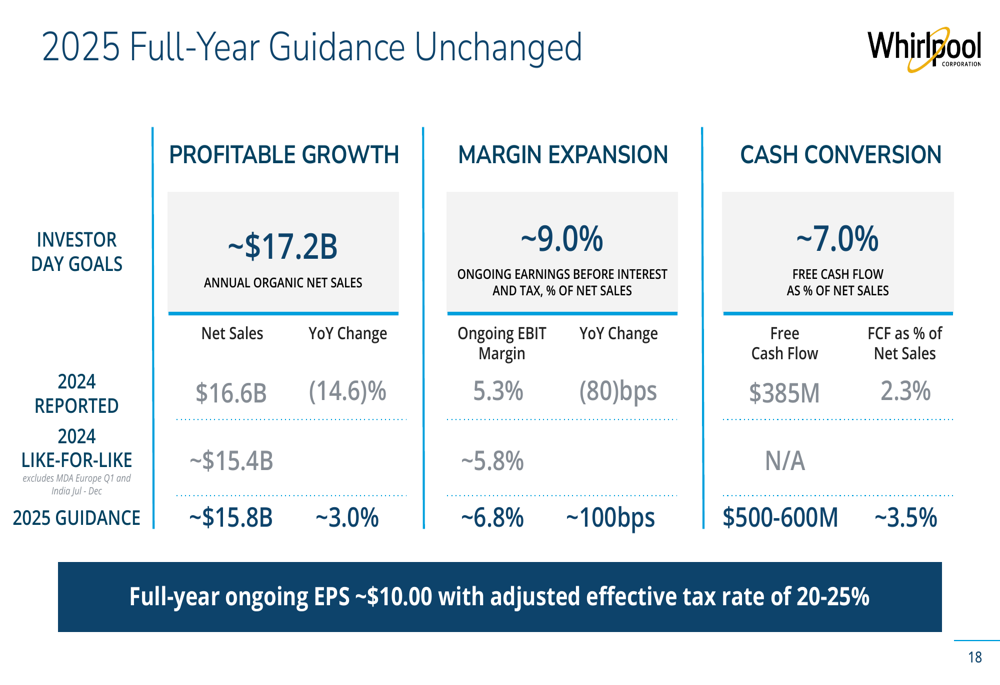

Despite the challenging environment, Whirlpool maintained its full-year 2025 guidance, projecting approximately $17.2 billion in annual organic net sales, ongoing EBIT margin of around 9.0%, and free cash flow of approximately 7.0% of net sales:

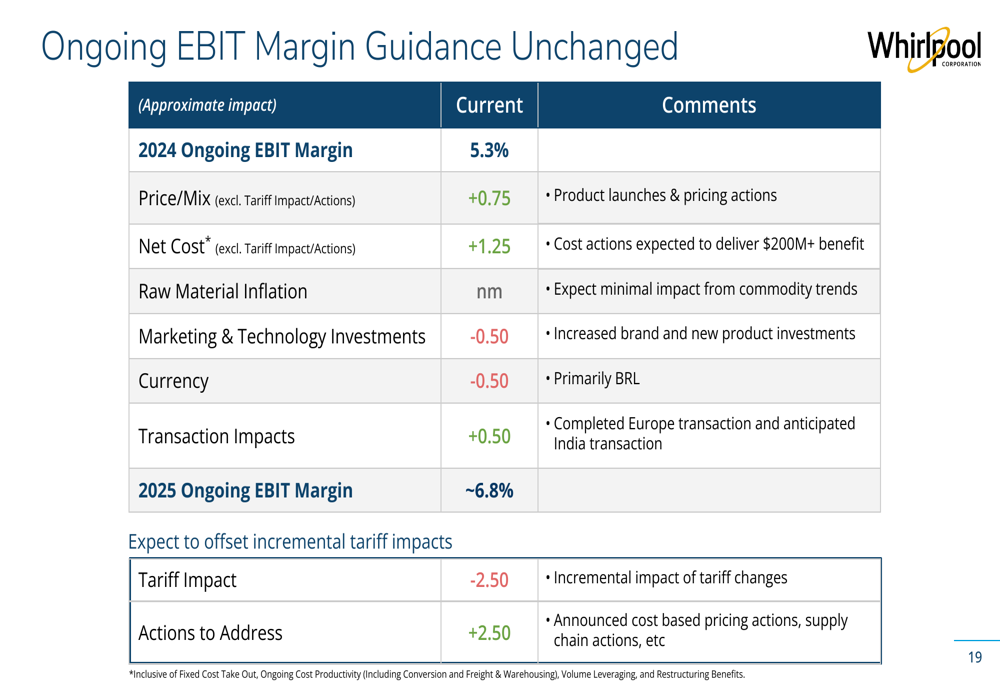

The company provided a detailed breakdown of factors expected to influence its ongoing EBIT margin for the full year, including the anticipated impact of tariffs and actions to address them:

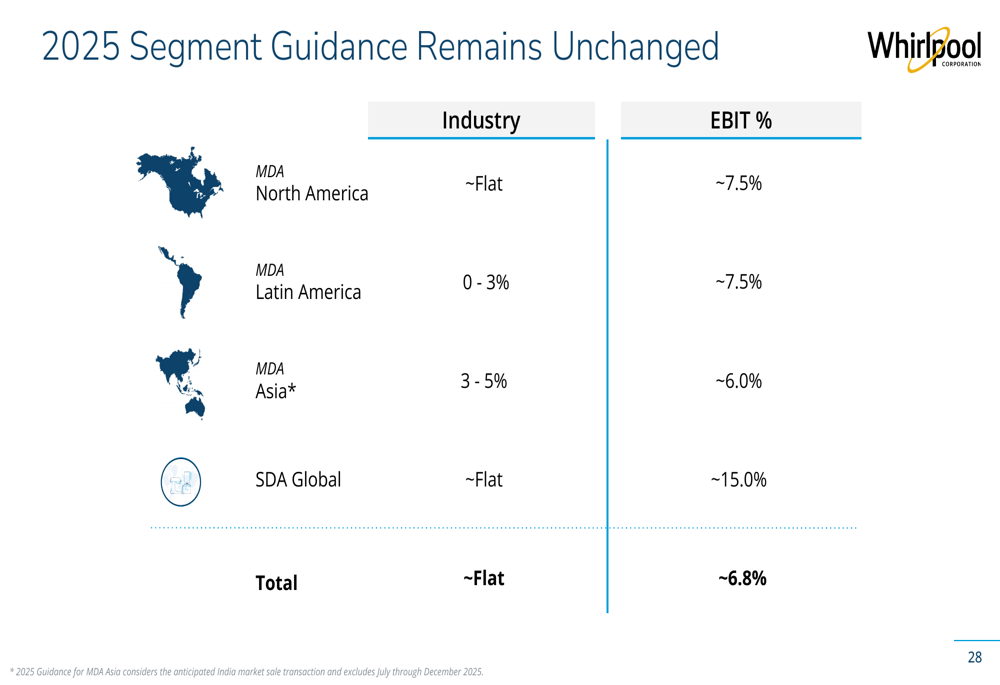

Segment-specific guidance indicates varied expectations across regions, with flat industry growth projected for North America and SDA Global, modest growth of 0-3% for Latin America, and stronger growth of 3-5% for Asia:

Whirlpool’s management expressed confidence in the company’s ability to navigate the current environment, highlighting structural cost reduction targets of over $200 million for 2025 and emphasizing that North America is well-positioned for growth from new products. The company also reiterated its expectation that tariff policies will level the playing field for domestic producers, while continued strength is expected from SDA Global and international businesses.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.