AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

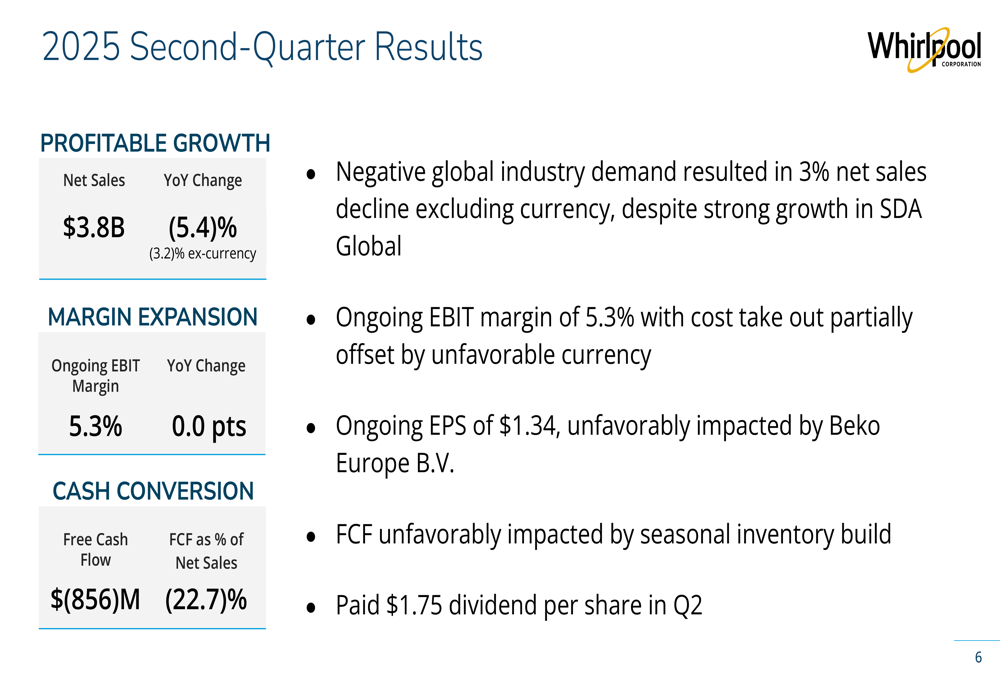

Whirlpool Corporation (NYSE:WHR) released its second-quarter 2025 earnings presentation on July 29, 2025, highlighting how its strong domestic manufacturing footprint positions the company to benefit from recent tariff changes despite ongoing industry challenges. The appliance manufacturer reported net sales of $3.8 billion, down 5.4% year-over-year (or -3.2% excluding currency effects), while maintaining a stable ongoing EBIT margin of 5.3%.

The presentation comes as Whirlpool’s stock closed at $99.74 on July 28, 2025, and rose to $100.40 in after-hours trading, showing modest investor confidence despite the sales decline. This follows a pattern seen in Q1, when the stock rose despite slight misses on both EPS and revenue forecasts.

Quarterly Performance Highlights

Whirlpool’s second-quarter results revealed the impact of challenging global industry demand, with net sales declining 3% excluding currency effects. However, the company maintained its ongoing EBIT margin at 5.3% year-over-year, as cost reduction initiatives helped offset unfavorable currency impacts.

As shown in the following summary of Q2 2025 results, the company reported ongoing EPS of $1.34, which was negatively impacted by Beko Europe B.V. Free cash flow was $(856) million, representing -22.7% of net sales, with the company noting this was affected by seasonal inventory build:

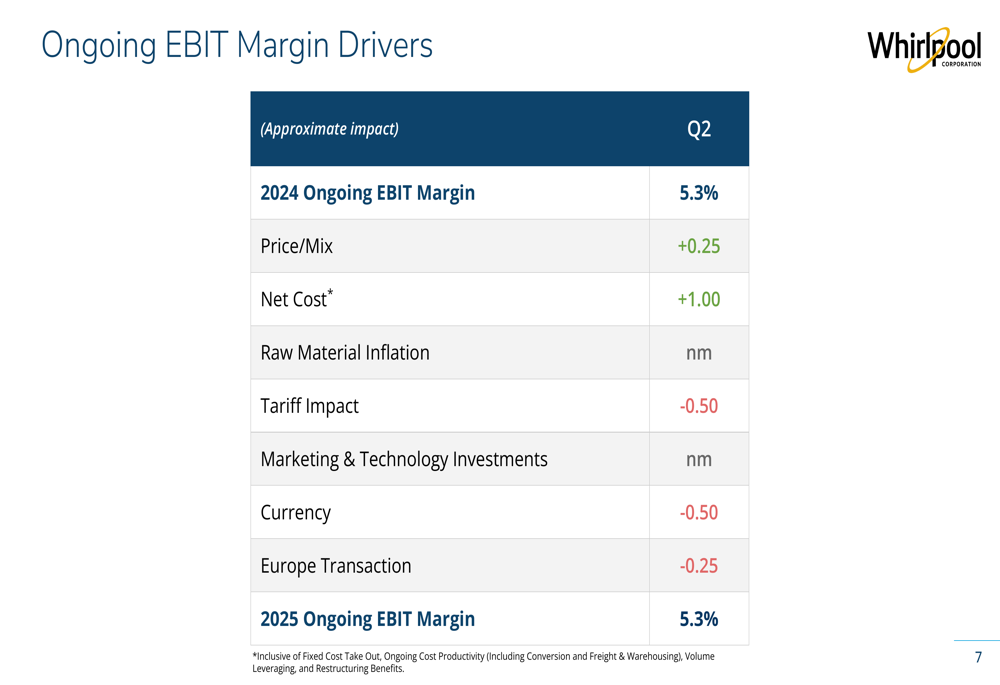

The drivers behind Whirlpool’s EBIT margin performance reveal how the company navigated various headwinds and tailwinds during the quarter. While price/mix contributed positively (+0.25 points) and net cost actions added a full percentage point to margins, these gains were offset by tariff impacts (-0.50 points), currency effects (-0.50 points), and the Europe transaction (-0.25 points):

Strategic Positioning

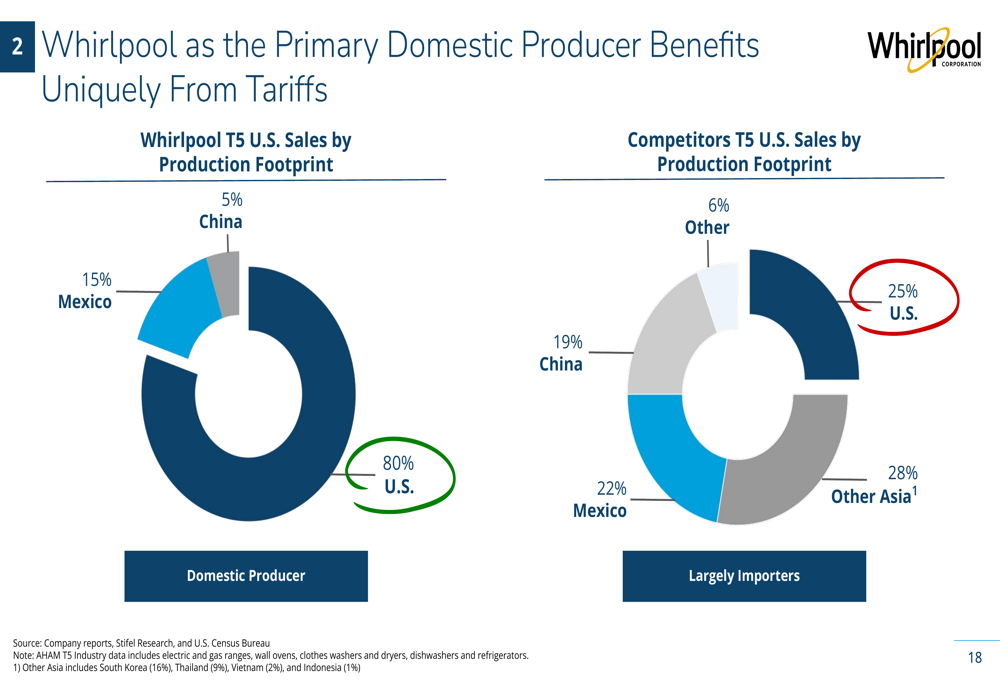

A central theme of Whirlpool’s presentation was its advantageous position as a primarily domestic manufacturer in the face of increasing tariffs. The company emphasized that 80% of its top 5 U.S. sales come from domestic production, compared to competitors who produce only 25% of their products in the U.S.

This chart clearly illustrates Whirlpool’s domestic production advantage compared to competitors:

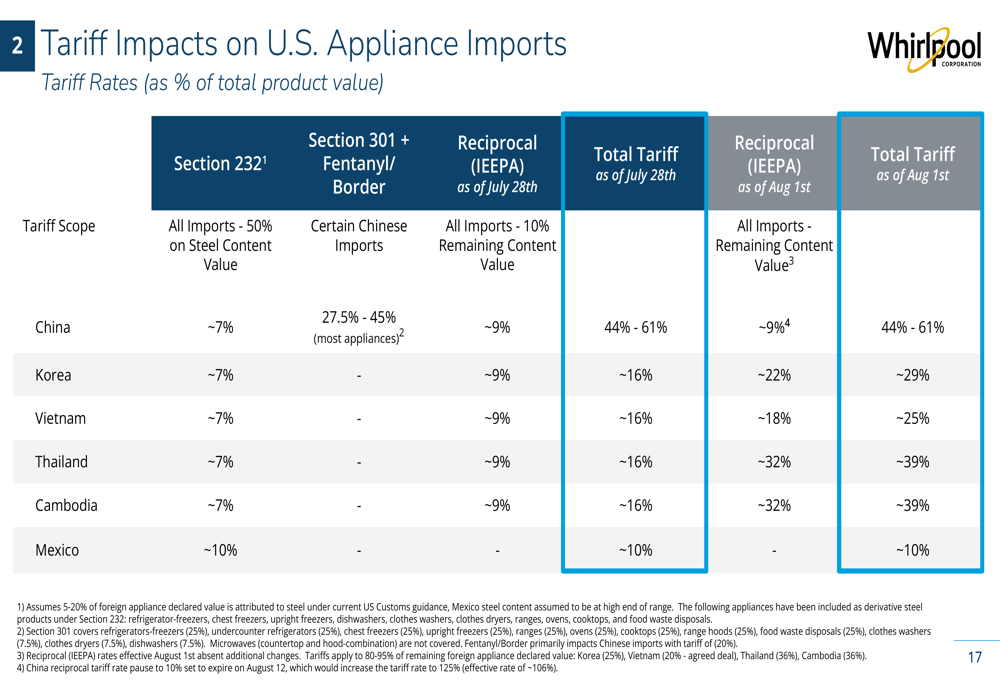

The company provided a detailed breakdown of tariff impacts on U.S. appliance imports, highlighting how various tariff sections affect different countries and product categories. This analysis underscores why Whirlpool believes it will be a "net winner" in the current trade environment:

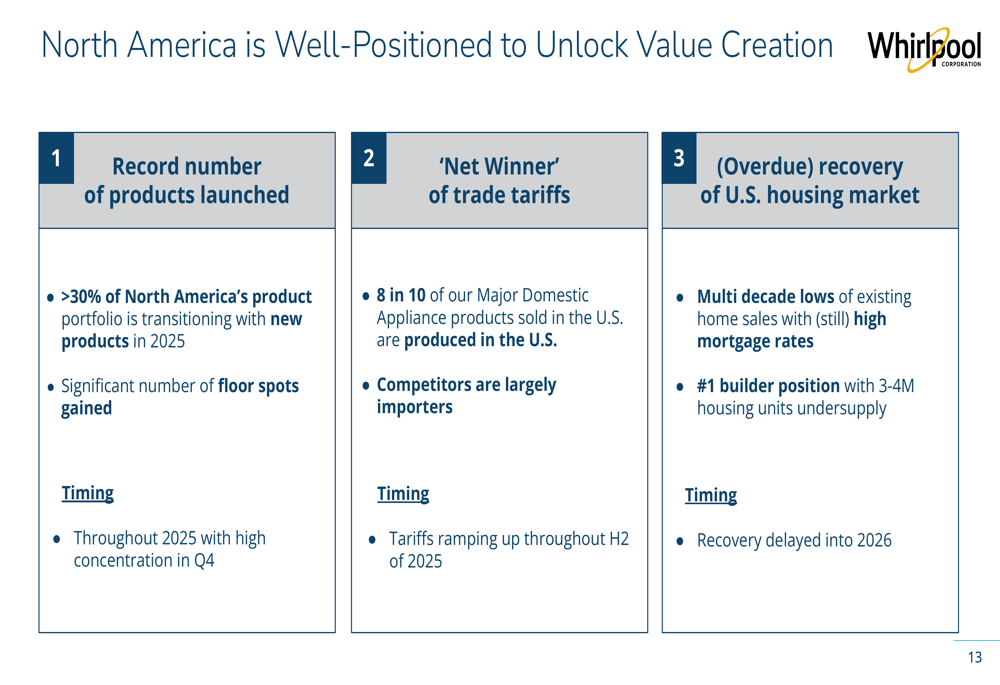

North America Growth Catalysts

Whirlpool outlined three key catalysts expected to drive growth in its North American market: new product launches, tariff advantages, and an eventual housing market recovery. The company is transitioning more than 30% of its North American product portfolio with new products in 2025, with a high concentration expected in Q4.

The following slide details these growth catalysts and their expected timing:

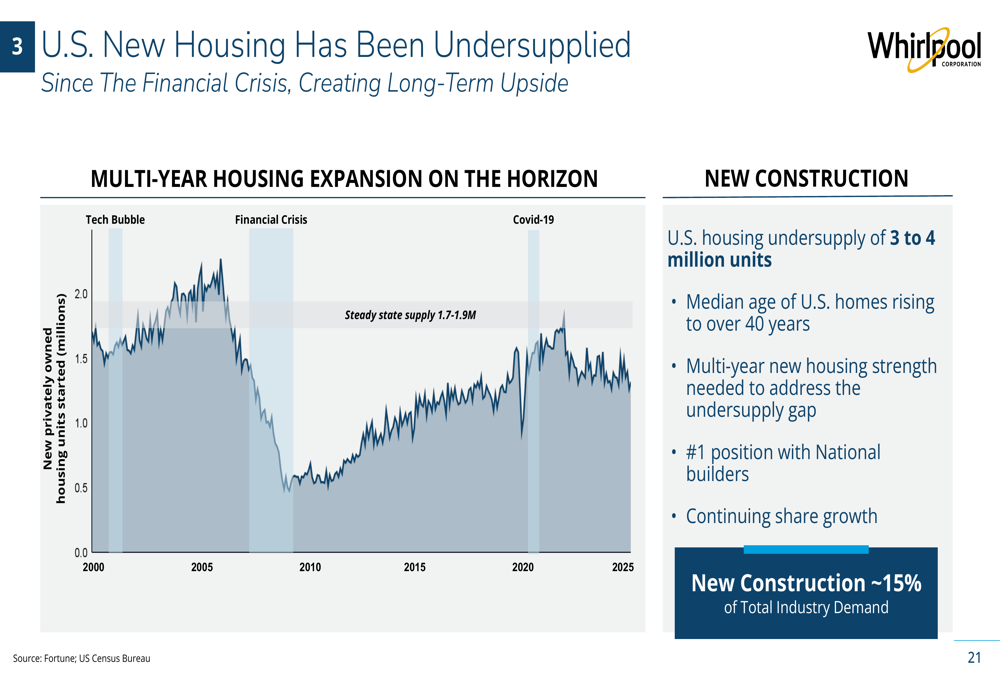

The company’s analysis of U.S. housing market dynamics suggests significant long-term upside potential. Despite current challenges with high mortgage rates keeping existing home sales at multi-decade lows, Whirlpool highlighted the estimated 3-4 million unit undersupply in the U.S. housing market:

Regional Performance Analysis

Whirlpool’s presentation broke down performance by region, revealing varied results across its global operations:

1. North America (NAR): Net sales of $2.4 billion in Q2 2025, down 5% year-over-year, with EBIT margin of 5.9%, down 0.4 percentage points year-over-year. Consumer sentiment weakness negatively impacted both demand and product mix.

2. Latin America (LAR): Net sales of $0.8 billion in Q2 2025, down 10% year-over-year, though excluding currency effects, the decline was only 1%. EBIT margin improved to 6.0%, up 0.2 percentage points year-over-year.

3. Asia: Net sales of $0.3 billion in Q2 2025, down 6% year-over-year (or 4% excluding currency). EBIT margin expanded by 0.9 percentage points to 7.1%.

4. Small Domestic Appliances (SDA) Global: This segment was a bright spot, with net sales of $0.2 billion, up 3% year-over-year. EBIT margin significantly improved to 17.3%, up 3.4 percentage points year-over-year, driven by strong direct-to-consumer sales.

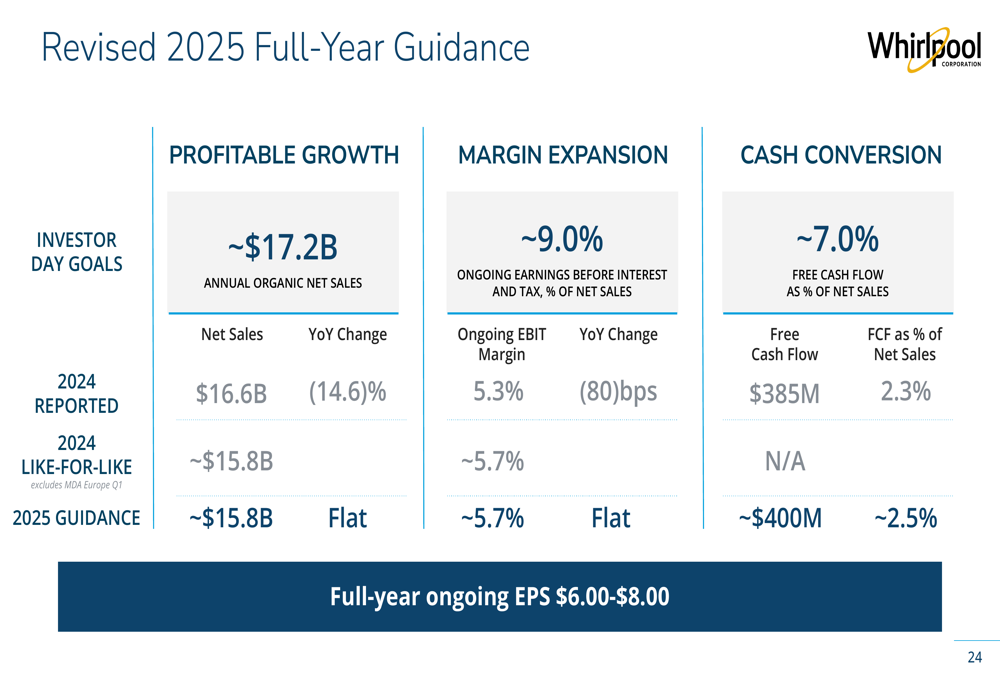

Revised 2025 Guidance

Whirlpool revised its full-year 2025 guidance, projecting annual organic net sales of approximately $17.2 billion and an ongoing EBIT margin of around 5.7%, an improvement from 2024’s 5.3%. The company expects free cash flow of approximately $400 million, representing about 7.0% of net sales.

The following slide details the company’s revised full-year guidance:

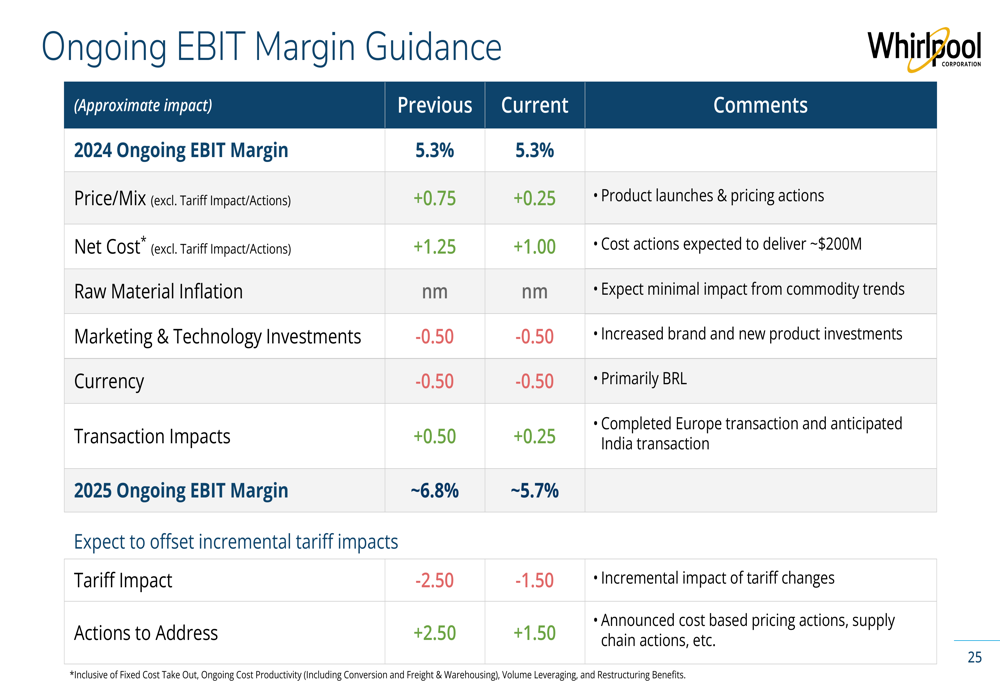

The company provided a more detailed breakdown of its EBIT margin guidance, showing the progression from 2024’s 5.3% to the projected 2025 margin of approximately 5.7%:

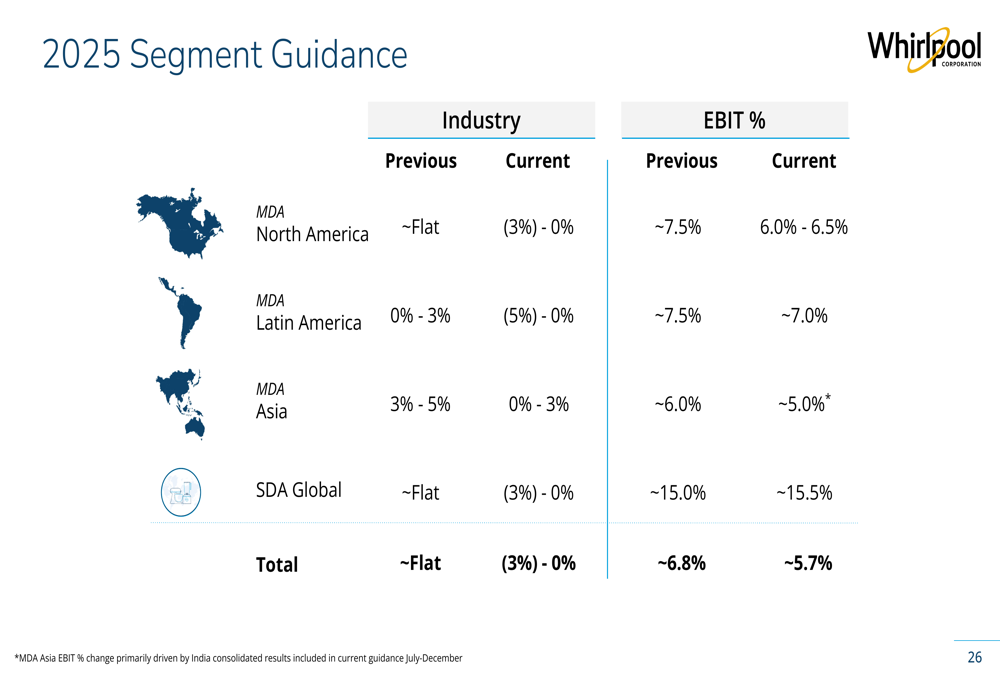

Whirlpool also provided segment-specific guidance across its regional operations, with varying industry outlooks and EBIT margin expectations:

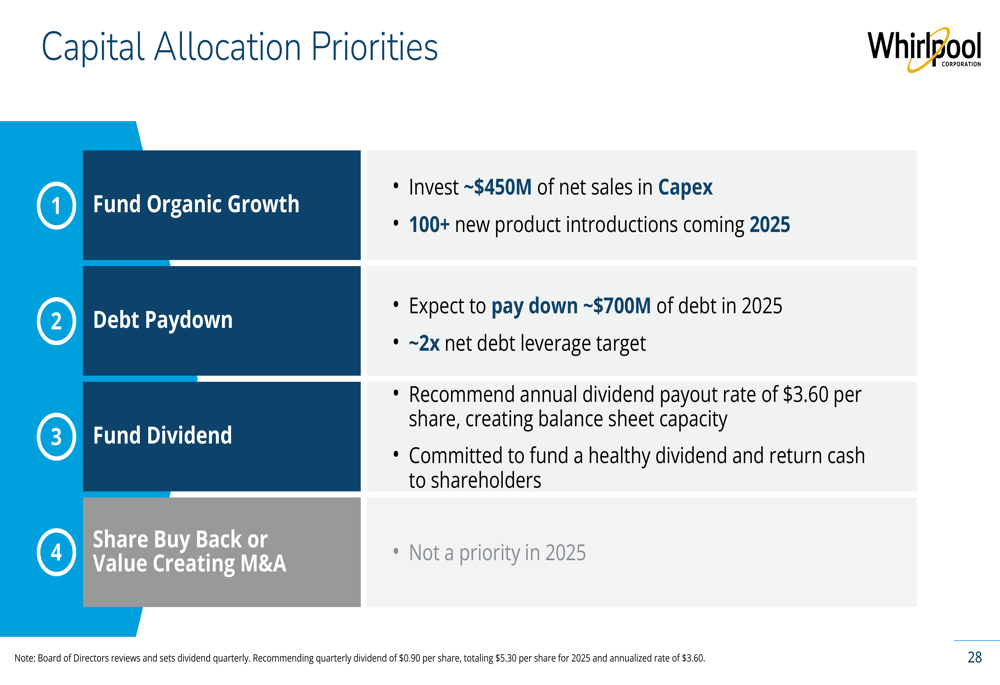

Capital Allocation Priorities

Whirlpool outlined its capital allocation strategy, focusing on three key priorities: funding organic growth, debt reduction, and maintaining its dividend. The company emphasized its commitment to strengthening its balance sheet while ensuring adequate liquidity.

The following slide details the company’s capital allocation framework:

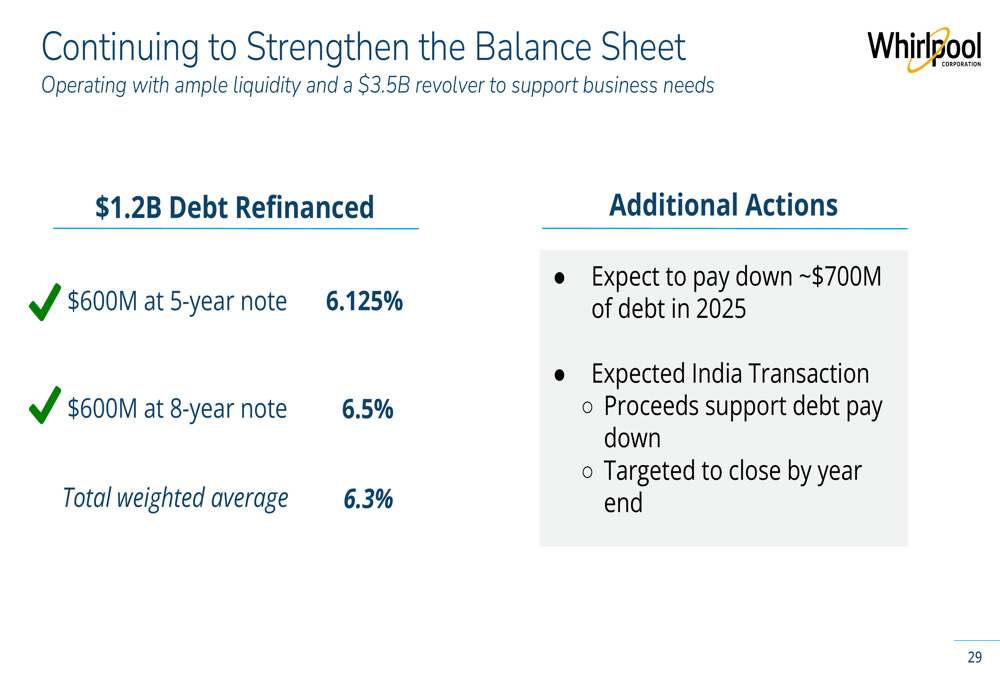

The company also highlighted its efforts to strengthen its balance sheet, noting its debt structure with a 5-year note at 6.125% and an 8-year note at 6.5%:

Forward-Looking Statements

In its closing summary, Whirlpool reiterated its confidence in the North American market’s growth potential, particularly as tariff policies are expected to benefit the company’s predominantly domestic manufacturing footprint. Management expressed optimism about new product launches driving growth, especially in the fourth quarter of 2025.

However, the company acknowledged ongoing challenges, including negative global industry demand, currency headwinds, and a delayed housing market recovery now pushed into 2026. Despite these challenges, Whirlpool maintains that its strategic positioning as a domestic manufacturer, combined with cost reduction initiatives and pricing actions, will enable it to navigate the current environment and deliver on its revised 2025 guidance.

The presentation reinforces CEO Marc Bitzer’s statement from the Q1 earnings call that "No matter how you look at the new tariff landscape, Whirlpool, with its strong U.S. Production base, is a net winner" – a strategic advantage the company continues to emphasize as central to its competitive positioning.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.