Street Calls of the Week

Introduction & Market Context

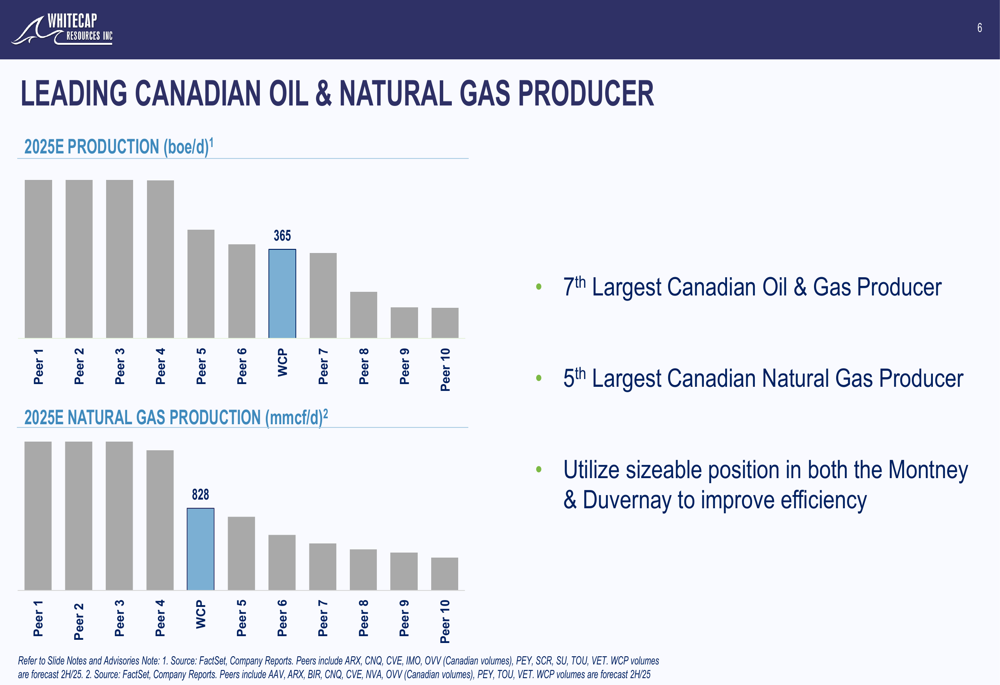

Whitecap Resources Inc . (TSX:WCP) presented its Q2 2025 corporate update on July 24, 2025, highlighting significant production growth and strategic capital allocation. The company has positioned itself as the 7th largest Canadian oil and gas producer and 5th largest Canadian natural gas producer, with a market capitalization of approximately $12 billion and an enterprise value of around $15 billion.

The presentation comes amid a period of strategic growth for Whitecap, which has been expanding its presence in both conventional and unconventional resource plays across Alberta and Saskatchewan. The company’s focus on maintaining a strong balance sheet while delivering shareholder returns has been a consistent theme throughout its development.

Q2 Performance Highlights

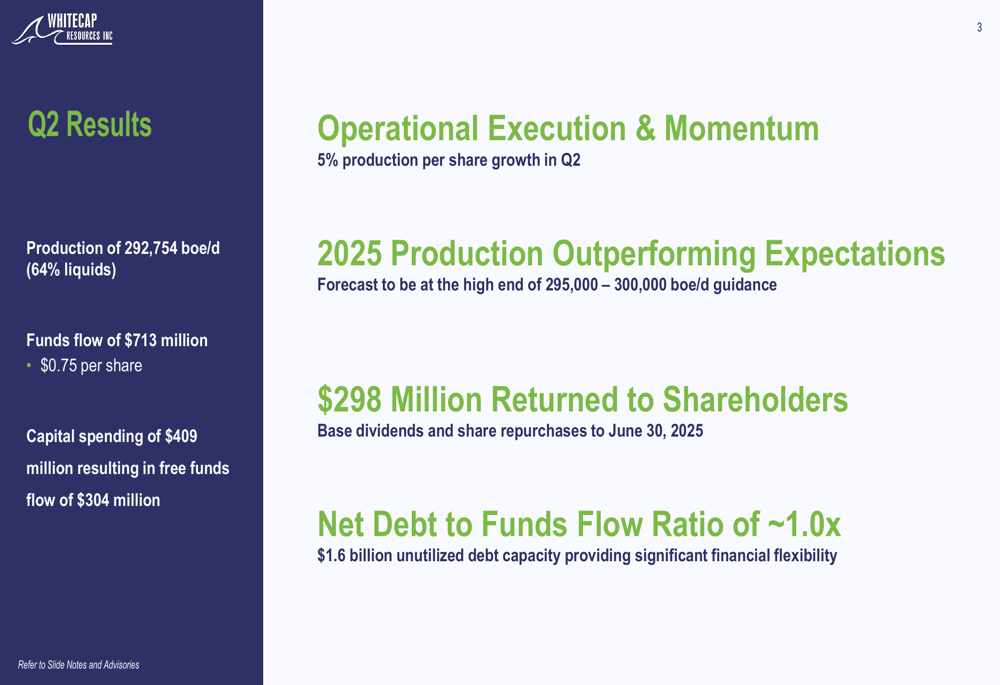

Whitecap reported strong operational and financial results for Q2 2025, with production averaging 292,754 boe/d (64% liquids), representing a 5% production per share growth compared to the previous quarter. The company generated funds flow of $713 million ($0.75 per share) and spent $409 million in capital expenditures, resulting in free funds flow of $304 million.

The company noted that its 2025 production is outperforming expectations and is forecasted to be at the high end of its 295,000 – 300,000 boe/d guidance. Current production has reached 365,000 boe/d, reflecting successful execution of the company’s growth strategy.

As shown in the following summary of Q2 results:

Capital Allocation Strategy

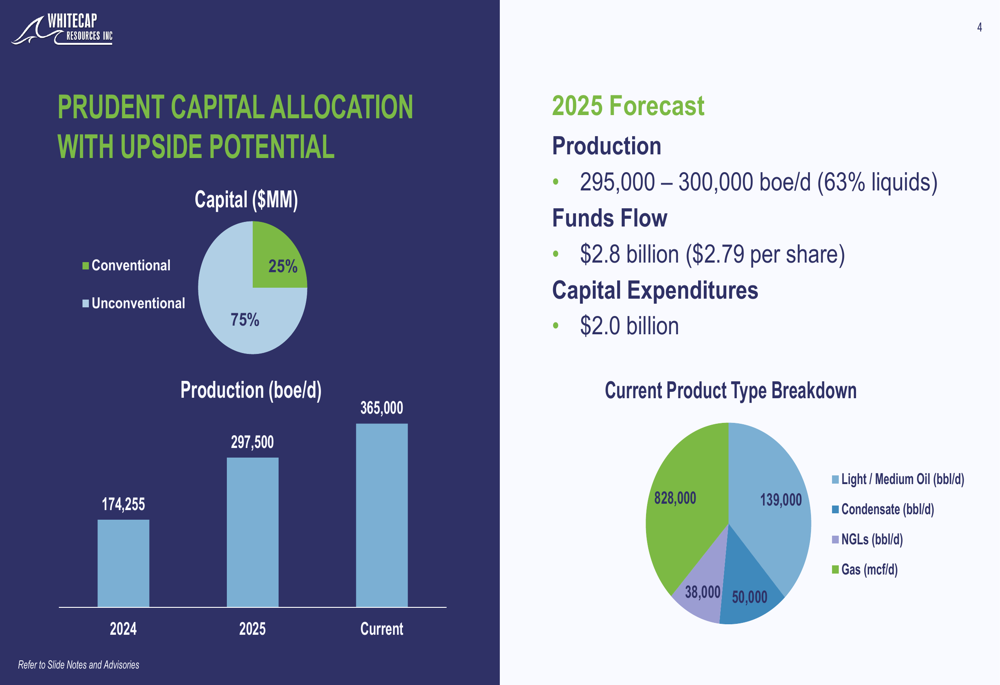

Whitecap’s capital allocation strategy balances investment between conventional and unconventional assets. For 2025, the company has allocated 75% of its capital to unconventional plays (Montney and Duvernay) and 25% to conventional assets. This strategic allocation reflects the company’s focus on high-return projects while maintaining a diversified portfolio.

The company’s production has grown substantially, from 174,255 boe/d in 2024 to a forecasted 297,500 boe/d in 2025, with current production at 365,000 boe/d. This growth trajectory is illustrated in the following capital allocation and production forecast:

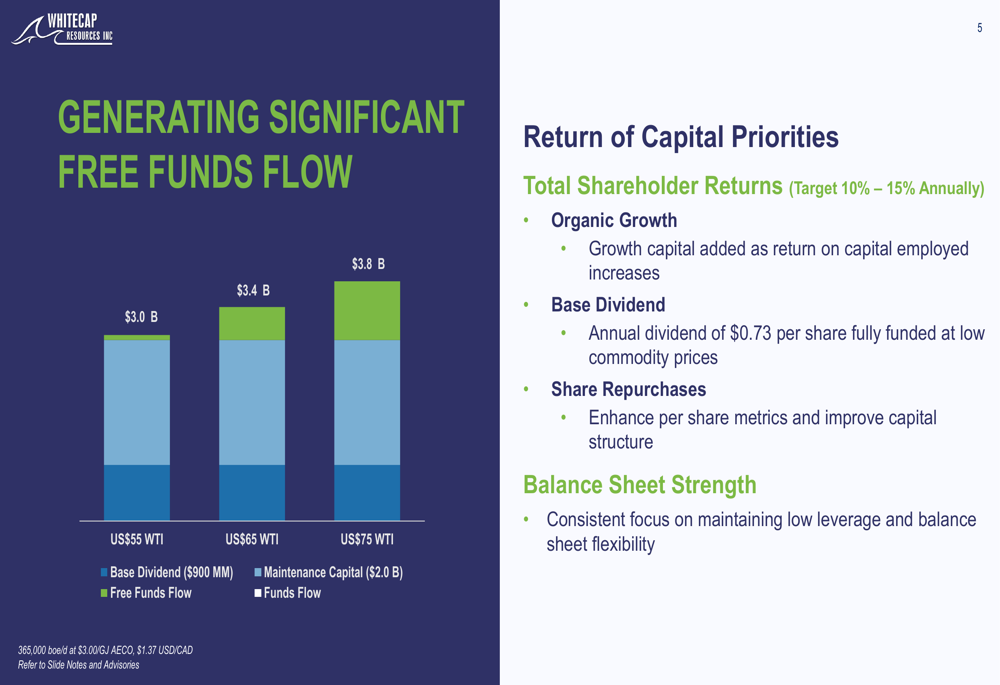

Whitecap’s free funds flow generation remains robust across various commodity price scenarios. At US$65 WTI, the company expects to generate $3.4 billion in free funds flow, well above its base dividend of $900 million and maintenance capital of $2.0 billion. This provides significant financial flexibility for additional shareholder returns and potential growth initiatives.

The company’s capital priorities and free funds flow generation at different price points are shown below:

Financial Strength and Balance Sheet

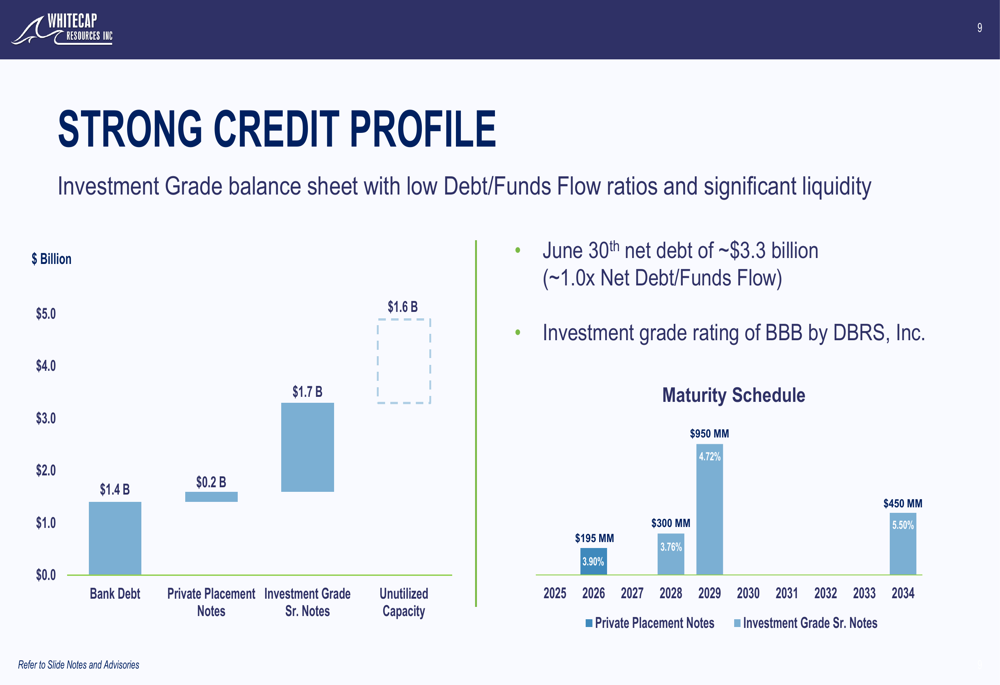

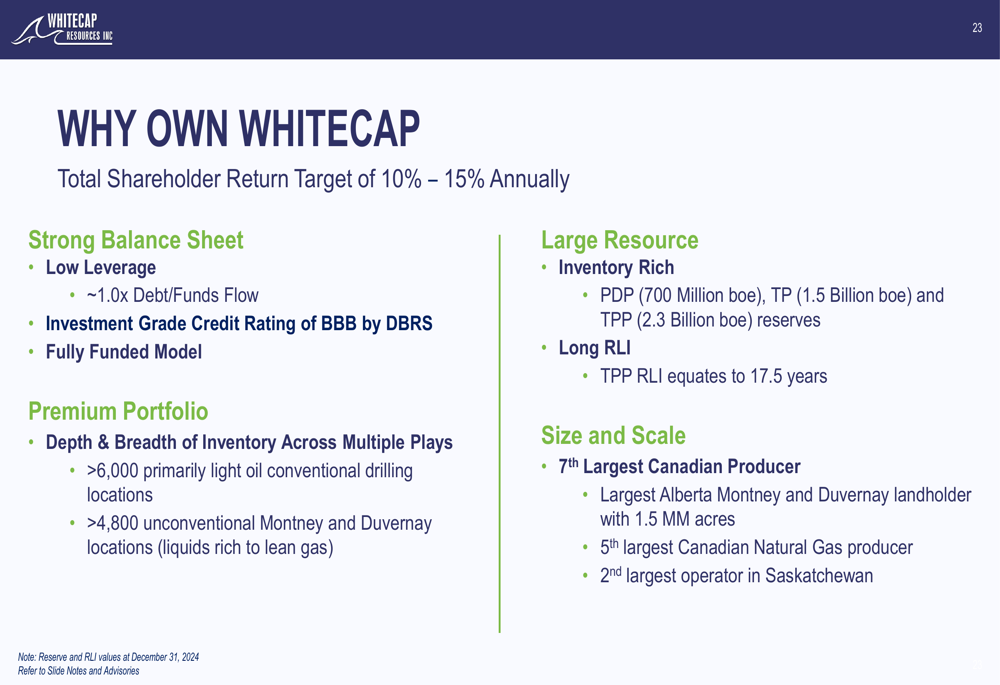

Whitecap maintains a strong financial position with an investment grade balance sheet. As of June 30, 2025, the company reported net debt of approximately $3.3 billion, representing a Net Debt/Funds Flow ratio of approximately 1.0x. The company holds an investment grade rating of BBB from DBRS, Inc., and has $1.6 billion of unutilized debt capacity, providing significant financial flexibility.

The company’s debt maturity schedule is well-structured, as illustrated in the following chart:

Whitecap has demonstrated prudent balance sheet management through commodity price cycles, maintaining an average Net Debt/Funds Flow ratio of 1.5x since 2013. This disciplined approach to financial management has enabled the company to navigate volatile commodity markets while continuing to invest in growth and return capital to shareholders.

Production Growth and Inventory

Whitecap’s growth strategy is anchored by its extensive inventory of drilling locations across both conventional and unconventional assets. The company has over 4,800 locations in its Montney and Duvernay inventory, with 2,600 classified as premium inventory with an average payout of 1.1 years. Additionally, Whitecap has over 6,000 conventional locations, with 2,600 premium locations having an average payout of 1.2 years.

The company’s competitive positioning in the Canadian energy landscape is significant, as shown in the following producer ranking:

Whitecap’s unconventional assets in the Montney and Duvernay plays are expected to be key drivers of future growth. The company has 975,000 acres in the Alberta Montney with over 4,100 potential drilling locations, and 535,000 acres in the Kaybob Duvernay with over 700 locations. These assets provide a deep inventory of high-return opportunities to support long-term production growth.

The economics of Whitecap’s premium inventory in the Montney and Duvernay are compelling, with payout periods ranging from 0.5 to 1.4 years depending on commodity prices, and rates of return from 70% to over 200%. This strong economic profile supports the company’s capital allocation strategy and long-term growth outlook.

Shareholder Returns and Future Outlook

Whitecap has established a target of 10-15% annual total shareholder returns, supported by organic growth, a base dividend of $0.73 per share annually (paid monthly at $0.0608 per share), and share repurchases. The company returned $298 million to shareholders through base dividends and share repurchases in the first half of 2025.

The company’s investment case is summarized in the following slide, highlighting its strong balance sheet, premium portfolio, large resource base, and significant scale:

For 2025, Whitecap has provided guidance of 295,000 – 300,000 boe/d (63% liquids) with capital expenditures of $2.0 billion. The company expects to generate funds flow of $2.8 billion ($2.79 per share) based on current commodity price assumptions.

Whitecap has identified over $200 million in annual savings through corporate consolidation, capital efficiency improvements, and operating cost reductions. These efficiency gains are expected to enhance margins and improve returns on capital employed.

The company’s management team has demonstrated a strong track record of execution, delivering 12% CAGR per share in funds flow, 11% CAGR per share in production, and 13% CAGR per share in TPP reserves over the past 15 years. This consistent performance underscores management’s ability to create value through both organic growth and strategic acquisitions.

Whitecap’s disciplined approach to capital allocation and focus on shareholder returns positions the company well to continue generating value through commodity price cycles. With its extensive inventory of high-quality drilling locations, strong balance sheet, and operational efficiency initiatives, Whitecap remains well-positioned in the Canadian energy sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.