Street Calls of the Week

Introduction & Market Context

WideOpenWest Inc . (NYSE:WOW) presented its first quarter 2025 financial results on May 6, 2025, revealing a company successfully navigating revenue challenges through operational efficiencies. The broadband provider continues its transition to a high-speed data-focused business model while managing the decline in traditional video services.

Following the earnings release, WOW shares traded up 1.38% in aftermarket trading, reaching $4.40. This modest gain comes after the stock has faced pressure in recent months, with shares trading near their 52-week low of $4.03, well below their 52-week high of $5.80.

Quarterly Performance Highlights

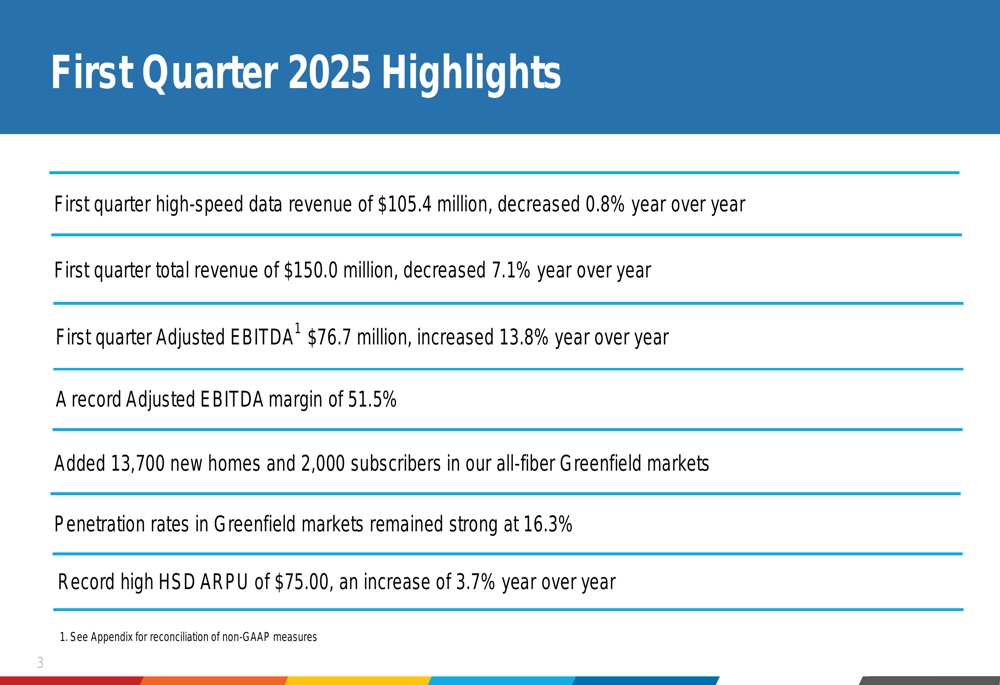

WideOpenWest reported mixed financial results for Q1 2025, with declining revenue offset by significant margin improvements. The company achieved a record adjusted EBITDA margin of 51.5%, demonstrating its ability to enhance profitability despite top-line challenges.

Key performance metrics for the quarter included:

- High-speed data revenue of $105.4 million, down 0.8% year-over-year

- Total (EPA:TTEF) revenue of $150.0 million, down 7.1% year-over-year

- Adjusted EBITDA of $76.7 million, up 13.8% year-over-year

- Record HSD ARPU of $75.00, up 3.7% year-over-year

As shown in the following summary of first quarter highlights:

Detailed Financial Analysis

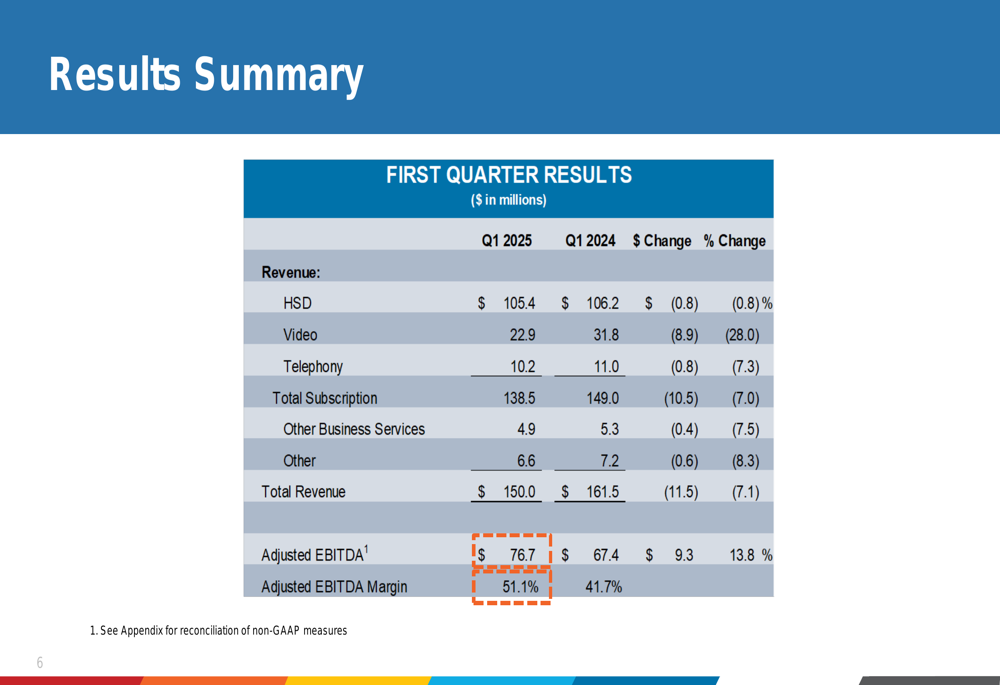

The company’s revenue decline was primarily driven by continued erosion in video and telephony services, consistent with industry-wide cord-cutting trends. Video revenue fell 28.0% year-over-year to $22.9 million, while telephony revenue decreased 7.3% to $10.2 million. These declines outpaced the relatively stable high-speed data revenue, which saw only a modest 0.8% decrease.

Despite the revenue challenges, WOW significantly improved its profitability metrics. The adjusted EBITDA of $76.7 million represented a 13.8% increase from the prior year, resulting in the company’s highest-ever EBITDA margin of 51.5%.

The comprehensive financial results are illustrated in the following slide:

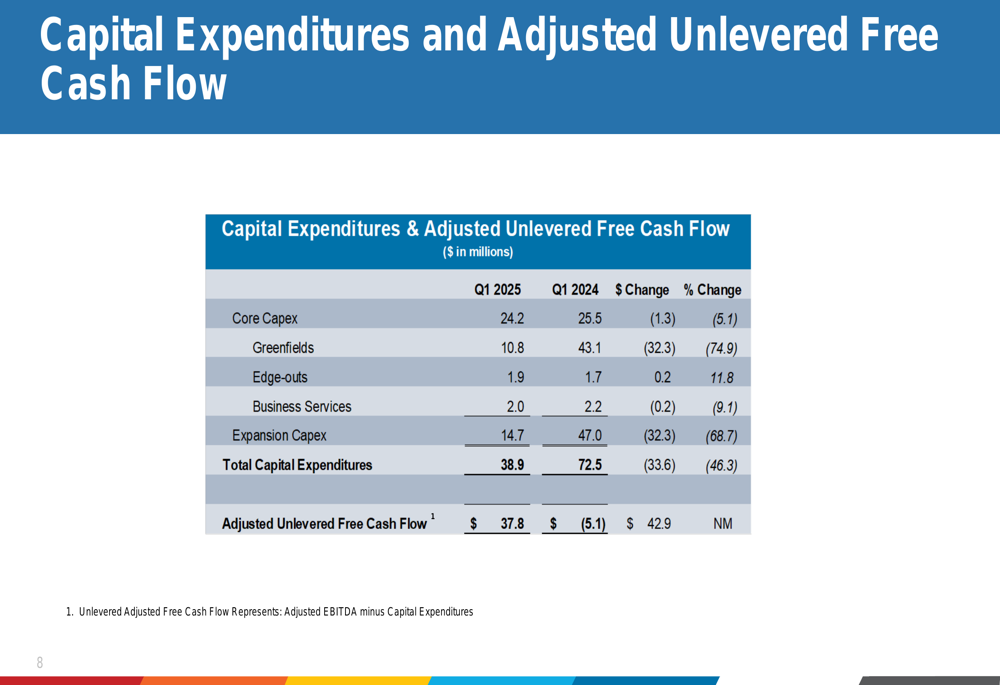

The company also made substantial progress in cash flow generation. Capital expenditures decreased 46.3% year-over-year to $38.9 million, with particularly significant reductions in Greenfield investments (-74.9%). This disciplined capital allocation, combined with improved operational efficiency, helped WOW achieve an adjusted unlevered free cash flow of $37.8 million, compared to -$5.1 million in the same period last year.

The breakdown of capital expenditures and cash flow metrics is detailed below:

Strategic Initiatives

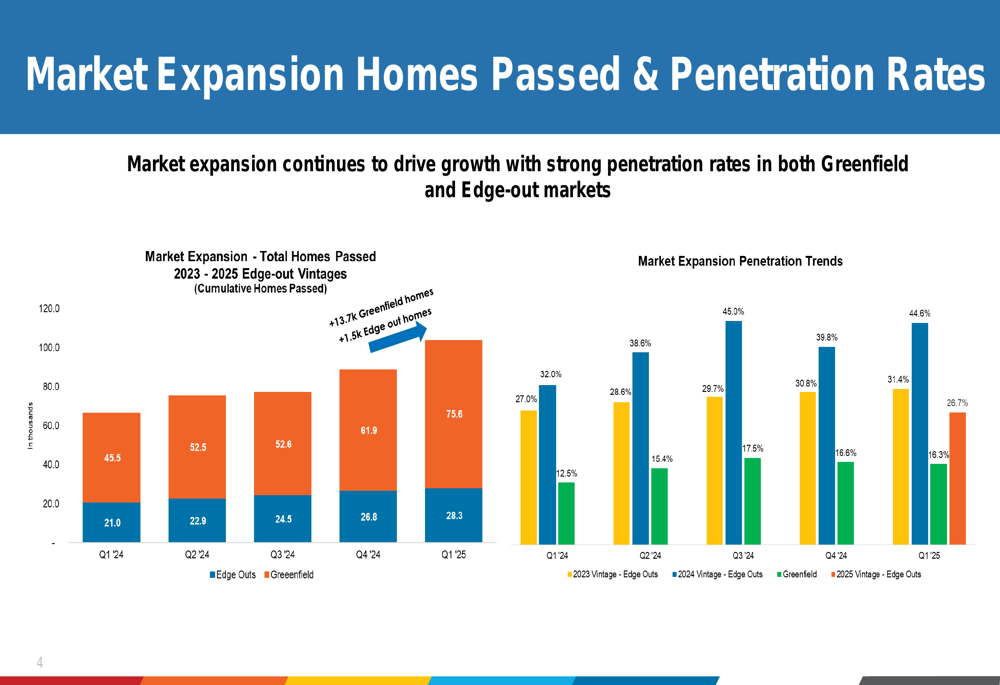

WideOpenWest continues to execute its broadband-first strategy, focusing on expanding its fiber footprint while managing the transition away from traditional video services. The company added 13,700 new homes in Greenfield markets and 1,500 in Edge-out areas during the quarter, demonstrating its commitment to network expansion despite reduced capital intensity.

The company’s market expansion efforts have yielded strong penetration rates, particularly in Greenfield markets at 16.3%. The 2023 vintage Edge-out markets showed impressive penetration of 44.6%, indicating successful customer acquisition in expansion areas.

The following chart illustrates WOW’s market expansion progress:

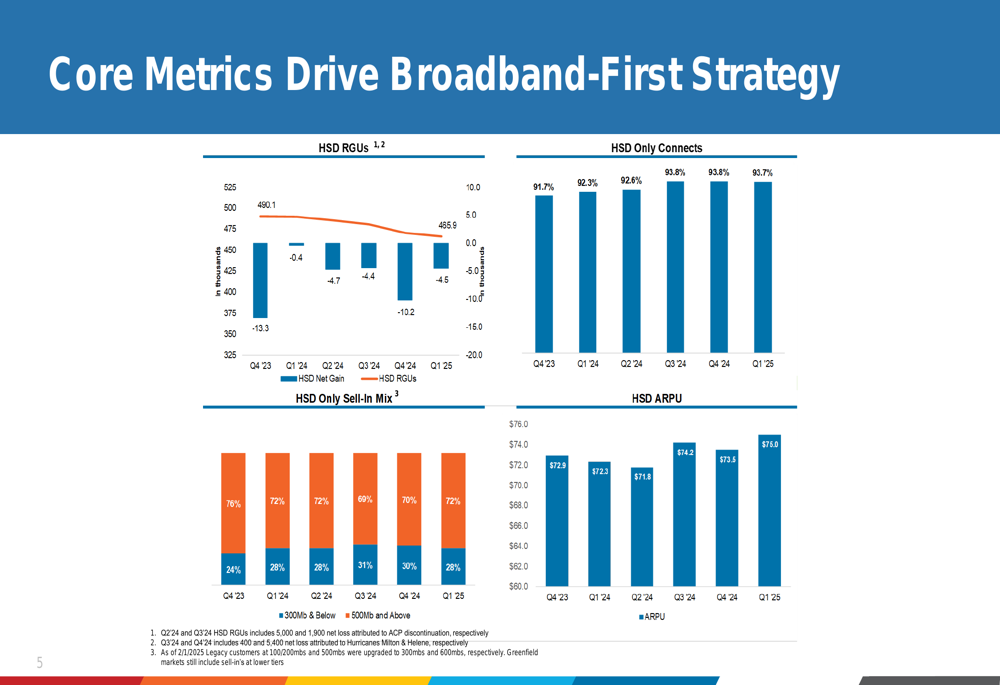

WOW’s broadband-first strategy is further evidenced by its high-speed data metrics. The company reported that over 93% of new connects were HSD-only customers in Q1 2025, and HSD ARPU reached a record $75.00, reflecting the company’s ability to monetize its broadband services effectively despite competitive pressures.

The core metrics supporting this strategy are shown below:

Forward-Looking Statements

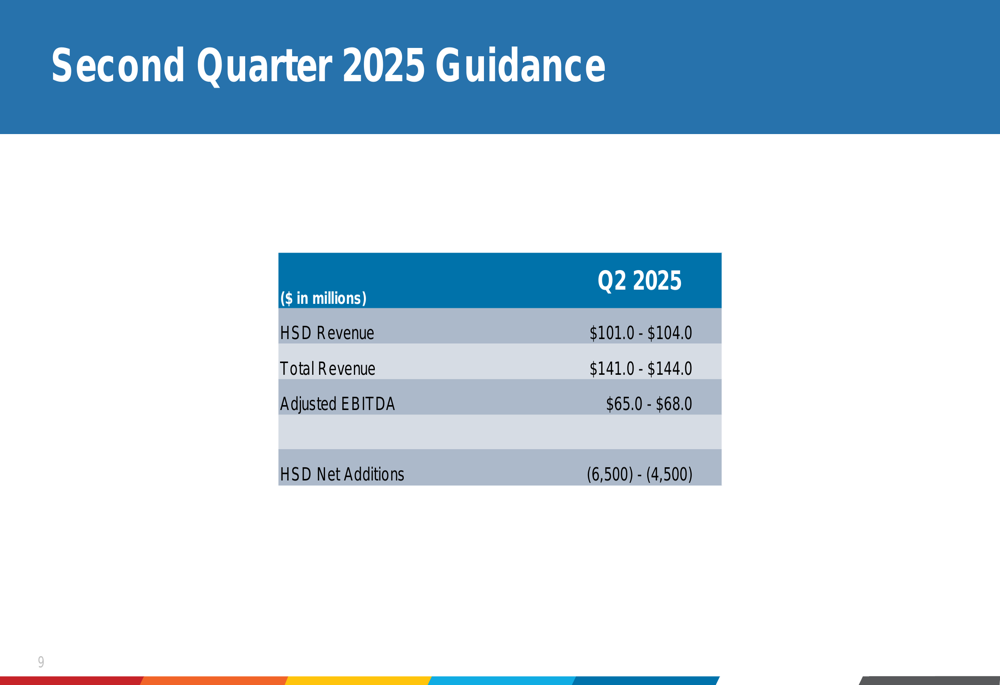

Looking ahead to the second quarter of 2025, WideOpenWest provided guidance that suggests continued revenue challenges but stable profitability. The company expects:

- HSD revenue between $101.0-$104.0 million

- Total revenue of $141.0-$144.0 million

- Adjusted EBITDA between $65.0-$68.0 million

- HSD net subscriber losses between 4,500-6,500

This guidance indicates sequential declines in both revenue and adjusted EBITDA compared to Q1 2025, suggesting ongoing competitive pressures in the broadband market. The projected subscriber losses highlight the challenges WOW faces in customer retention and acquisition despite its network expansion efforts.

The company’s Q2 2025 guidance is summarized in the following slide:

WideOpenWest’s Q1 2025 presentation reveals a company effectively managing its transition to a broadband-centric business model. While revenue continues to decline, primarily due to legacy video services, the company has successfully improved operational efficiency, resulting in record EBITDA margins and positive cash flow generation. The reduced capital expenditure profile suggests a more disciplined approach to growth, though projected subscriber losses in Q2 indicate ongoing competitive challenges in the broadband market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.