Five things to watch in markets in the week ahead

John Wiley & Sons (NYSE:WLY) reported its first quarter fiscal 2026 results on September 4, 2025, highlighting the company's growing AI licensing business while posting mixed overall performance. Despite the company's optimistic outlook, Wiley's stock fell 7.79% to $39.77 during the trading session.

Quarterly Performance Highlights

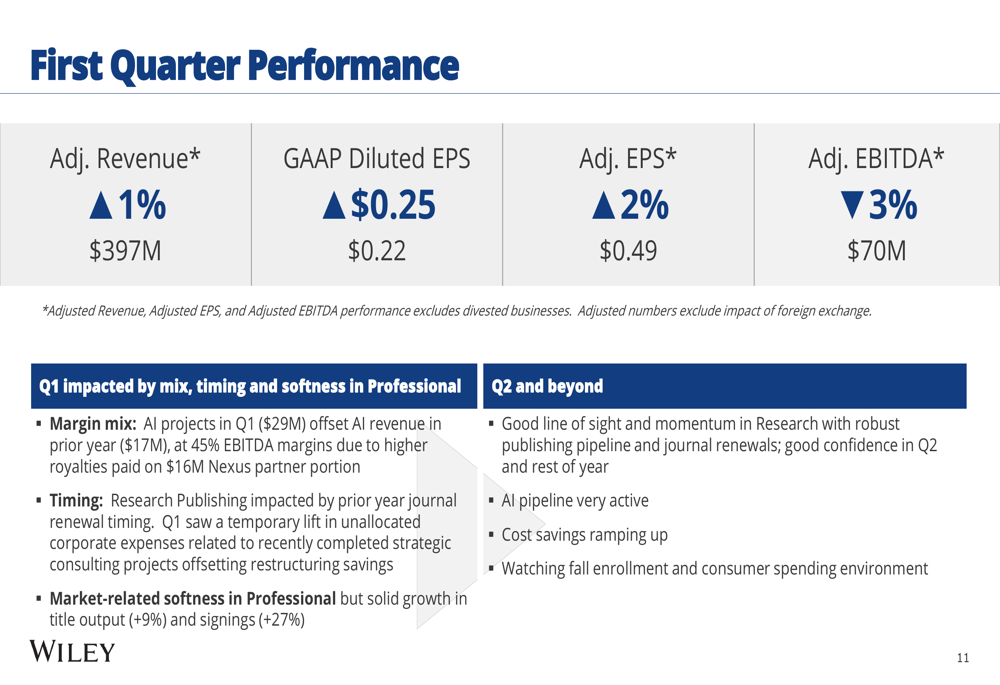

Wiley reported first quarter adjusted revenue growth of 1% to $397 million, with adjusted earnings per share increasing 2% to $0.49. However, adjusted EBITDA declined 3% to $70 million, and GAAP diluted EPS came in at $0.25. The company characterized these results as "in line with expectations."

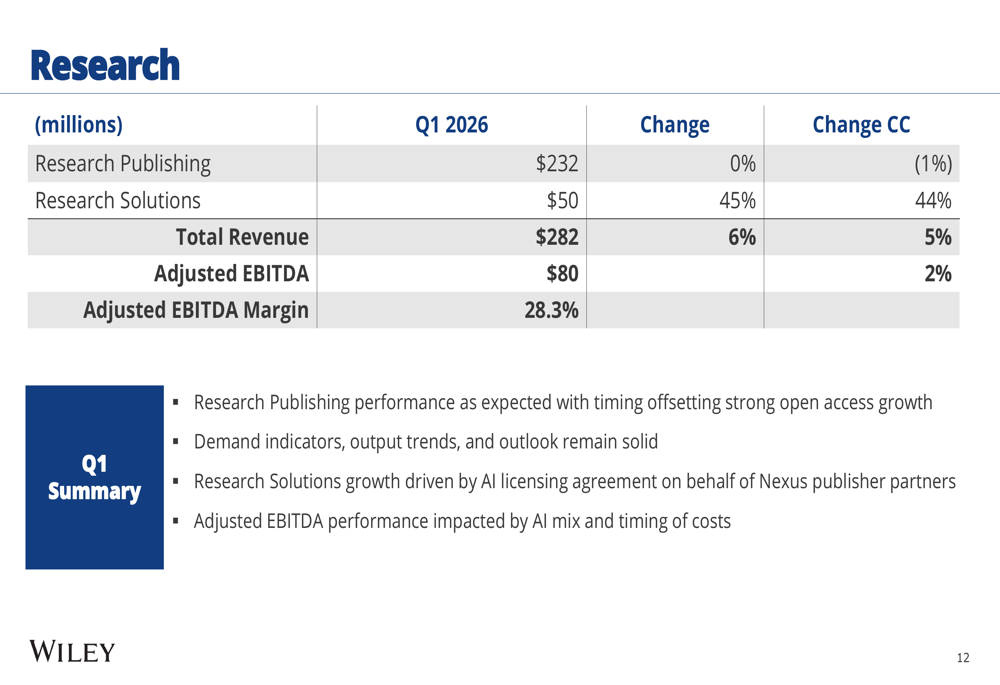

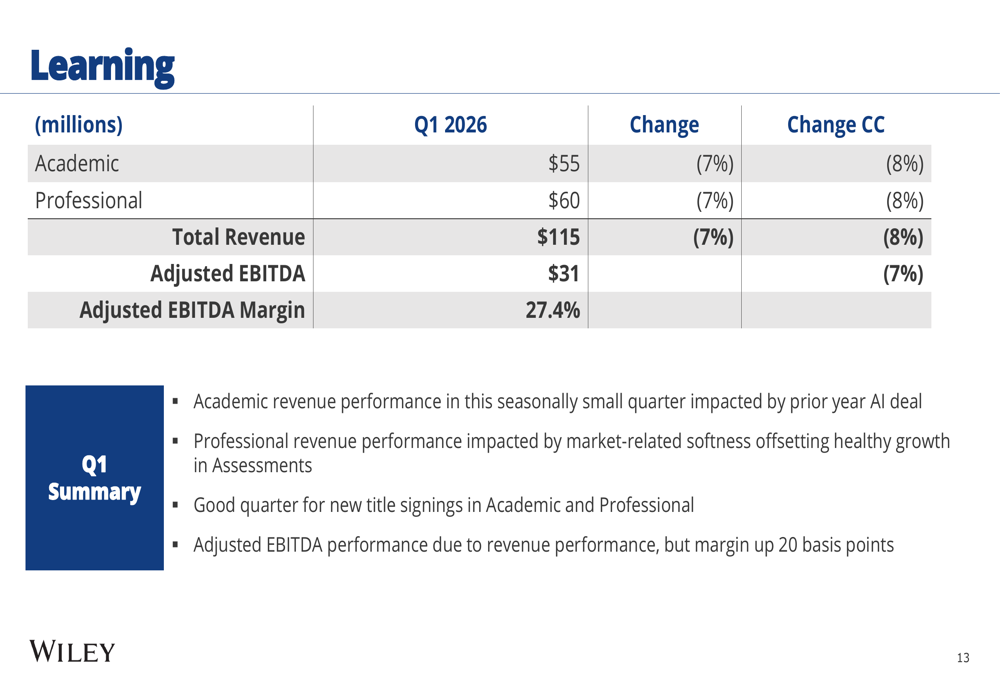

The company's performance showed a stark contrast between its business segments. The Research segment delivered 6% revenue growth to $282 million, driven by strong AI licensing demand and open access growth. Meanwhile, the Learning segment experienced a 7% revenue decline to $115 million, with both Academic and Professional divisions showing weakness.

As shown in the following quarterly performance summary:

The Research segment's growth was primarily fueled by Research Solutions, which surged 45% to $50 million, while Research Publishing remained flat at $232 million. The segment's adjusted EBITDA margin stood at 28.3%.

In contrast, both components of the Learning segment declined by 7%, with Academic at $55 million and Professional at $60 million. The Learning segment maintained an adjusted EBITDA margin of 27.4%.

Strategic AI Initiatives

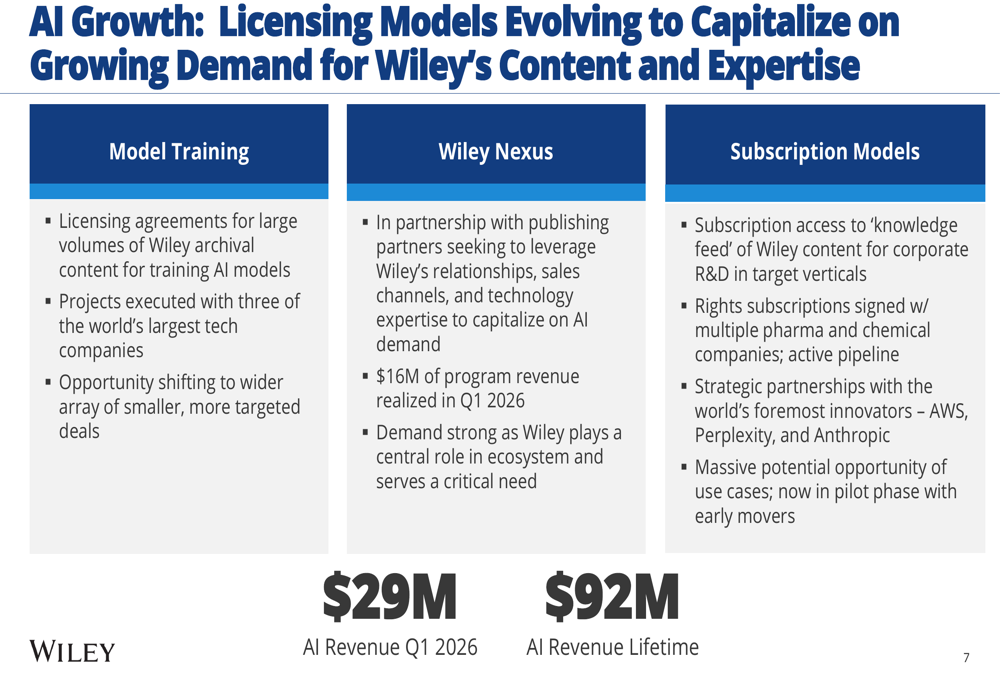

Wiley has positioned itself as a leader in AI content licensing, reporting $29 million in AI revenue for Q1 2026 and lifetime AI revenue of $92 million. The company has developed multiple licensing models, including model training agreements with major tech companies and subscription models for corporate R&D customers.

The company's AI strategy is illustrated in this breakdown of licensing models:

Wiley has expanded its AI partnerships, announcing a strategic relationship with Anthropic, one of the leading AI innovators. The company has also executed licensing projects with three of the world's largest tech companies and developed recurring inference pilots with major pharmaceutical, chemical, and space exploration organizations.

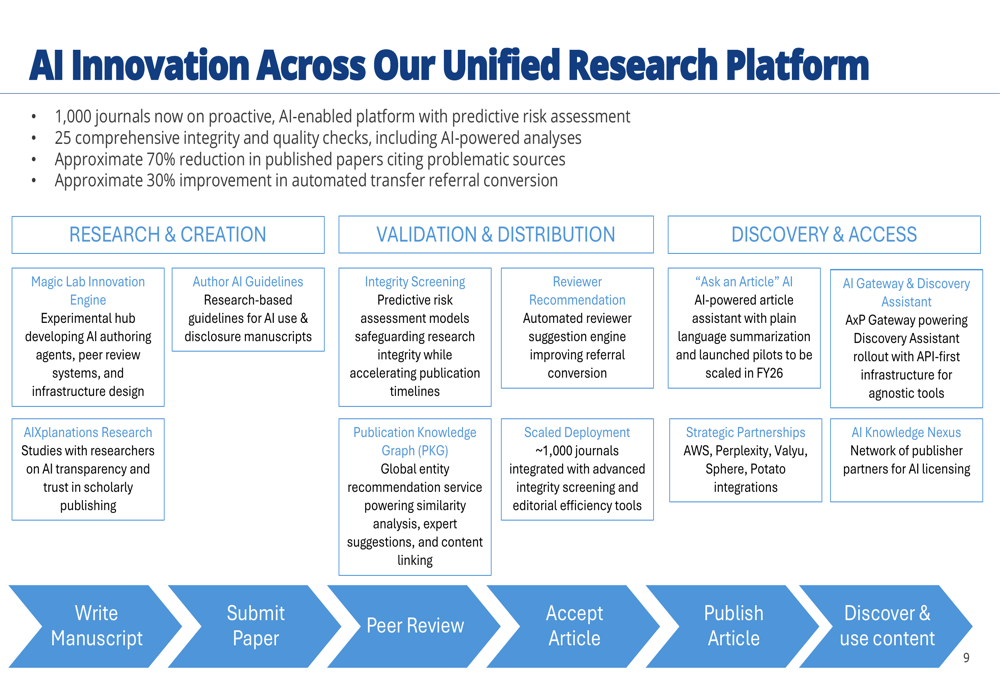

The company is implementing AI innovations across its unified research platform, which now hosts 1,000 journals. These innovations span research creation, validation, distribution, and discovery processes.

Fiscal 2026 Outlook and Commitments

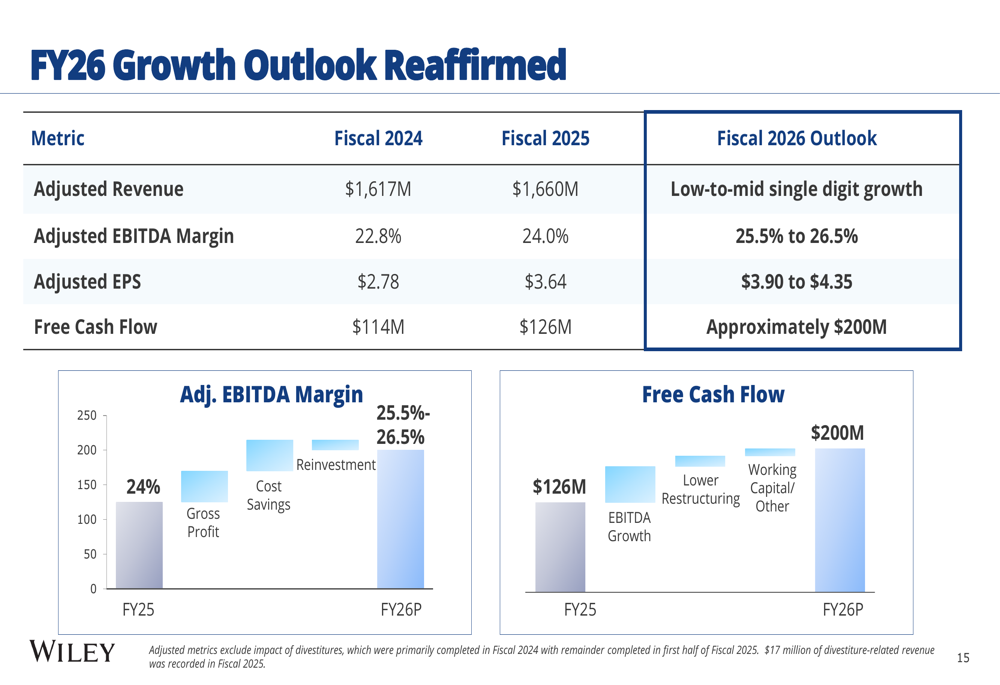

Wiley reaffirmed its fiscal 2026 guidance, projecting low-to-mid single digit revenue growth, adjusted EBITDA margin of 25.5% to 26.5%, adjusted EPS of $3.90 to $4.35, and free cash flow of approximately $200 million.

The company's fiscal 2026 outlook is summarized in the following chart:

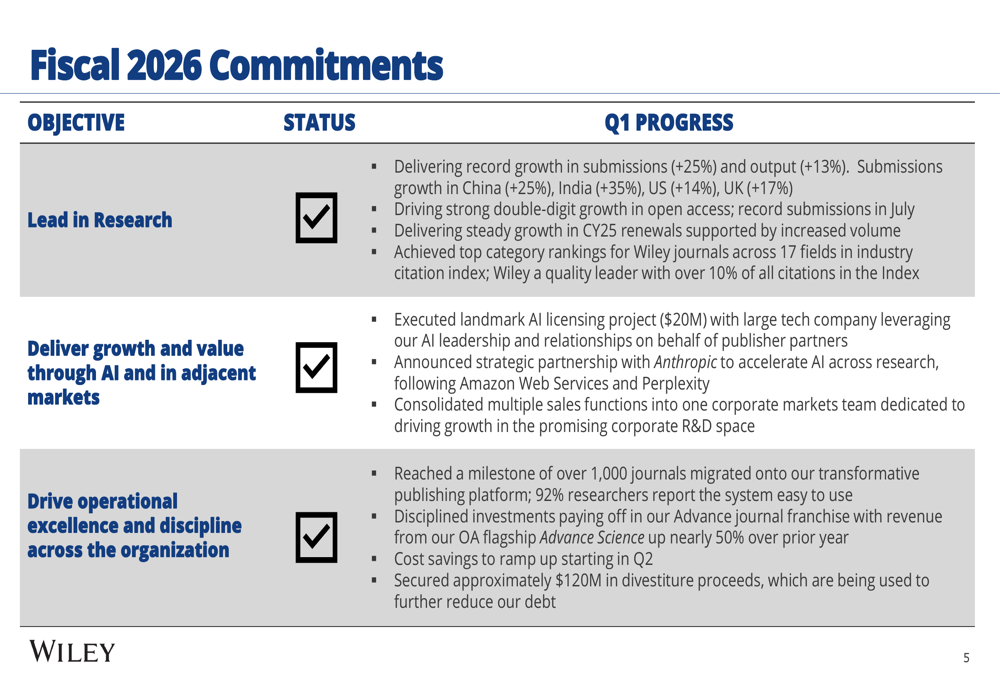

Wiley reported progress on its key strategic commitments, including leading in research, delivering growth through AI, and driving operational excellence. Research submissions increased 25% and output grew 13%, with significant growth in key markets including China (+25%), India (+35%), US (+14%), and UK (+17%).

Financial Position and Shareholder Returns

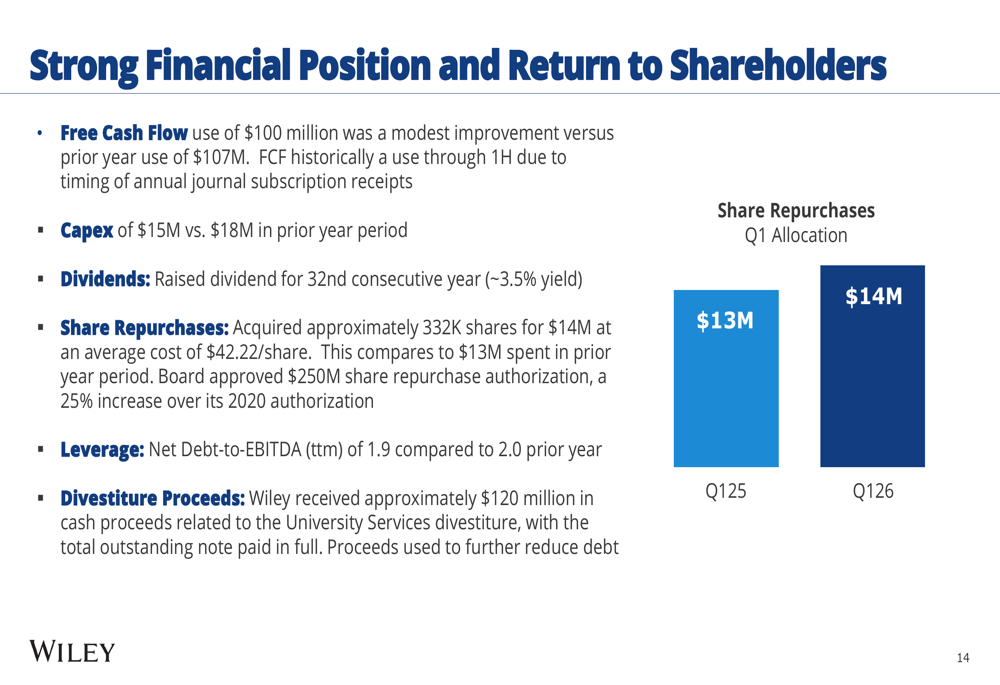

Wiley highlighted its strong financial position and commitment to shareholder returns. The company raised its dividend for the 32nd consecutive year, offering approximately 3.5% yield. The board approved a $250 million share repurchase authorization, representing a 25% increase over the 2020 authorization.

During Q1, Wiley acquired approximately 332,000 shares for $14 million at an average cost of $42.22 per share. The company's net debt-to-EBITDA ratio improved to 1.9 from 2.0 in the prior year, and Wiley received approximately $120 million in cash proceeds from its University Services divestiture.

The following chart illustrates Wiley's financial position and shareholder returns:

Market Reaction and Forward Outlook

Despite Wiley's positive framing of its results and reaffirmed guidance, investors appeared skeptical, sending the stock down 7.79% during the trading session. This reaction contrasts with the company's previous quarter, when it exceeded expectations and saw a 9.37% pre-market stock increase.

The company expressed confidence in its Q2 and full-year performance, citing strong open access growth, continued AI content licensing opportunities, and anticipated cost savings. Management highlighted a six-month publishing backlog and noted that Q1 timing impacts were transitory.

Wiley's executives emphasized the company's AI leadership position and operational discipline as key factors for future growth, while acknowledging softness in the Professional segment. With its focus on recurring revenue models and strategic AI partnerships, Wiley aims to capitalize on what it sees as underpenetrated corporate markets for its content and data services.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.