China AI: Bernstein sees chipmakers benefiting from Nvidia scrutiny

Executive Summary

Williams Companies (NYSE:WMB) reported solid first quarter 2025 results, with Adjusted EBITDA reaching $1,989 million, a 3% increase year-over-year and a robust 12% sequential growth from the fourth quarter of 2024. The natural gas infrastructure company raised its 2025 Adjusted EBITDA guidance midpoint by $50 million and increased its growth capital expenditure by $925 million to fund the newly commercialized Socrates power generation project.

The company also announced a 5.3% dividend increase to $0.50 per share and received a credit rating upgrade to BBB+ from S&P, with Moody’s assigning a positive outlook. These developments build on Williams’ momentum from the previous quarter, when the company reported record adjusted EBITDA and raised its 2024 guidance midpoint to $7.075 billion.

Quarterly Performance Highlights

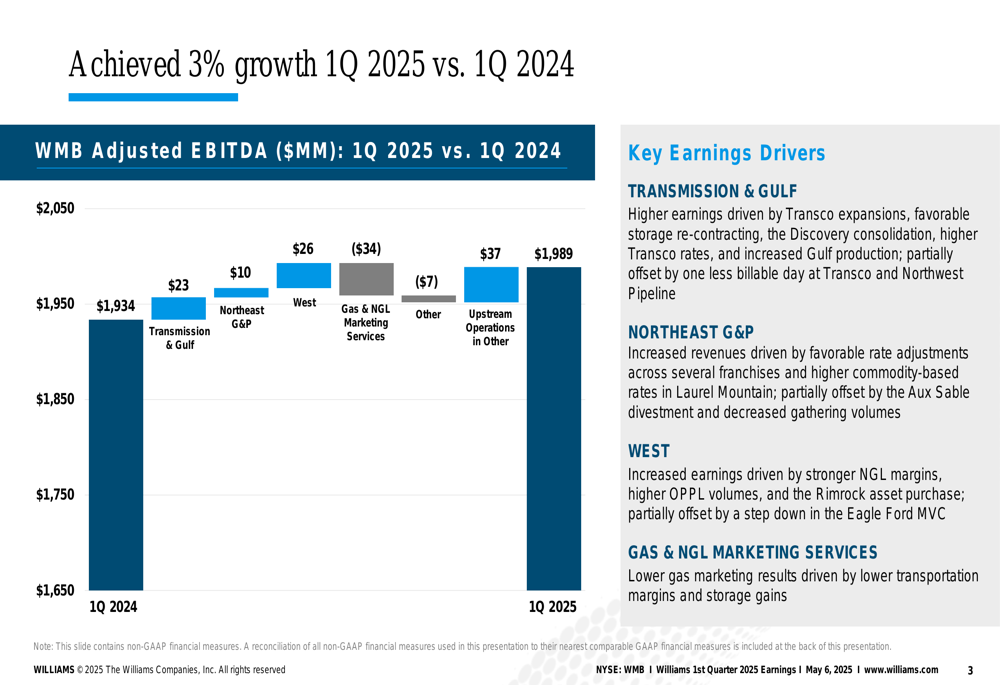

Williams delivered year-over-year growth in its first quarter results, with Adjusted EBITDA increasing by $55 million or 3% compared to Q1 2024. This growth was primarily driven by strong performance in the Transmission & Gulf, Northeast G&P, and West segments, partially offset by lower results in Gas & NGL Marketing Services.

As shown in the following chart detailing the Q1 2025 vs. Q1 2024 Adjusted EBITDA breakdown:

The Transmission & Gulf segment contributed an additional $23 million, primarily from Transco expansions. The Northeast G&P segment added $10 million through favorable rate adjustments, while the West segment provided $26 million in growth driven by stronger NGL margins. The company’s upstream operations contributed $37 million, offsetting a $34 million decline in Gas & NGL Marketing Services due to lower transportation margins and reduced storage gains.

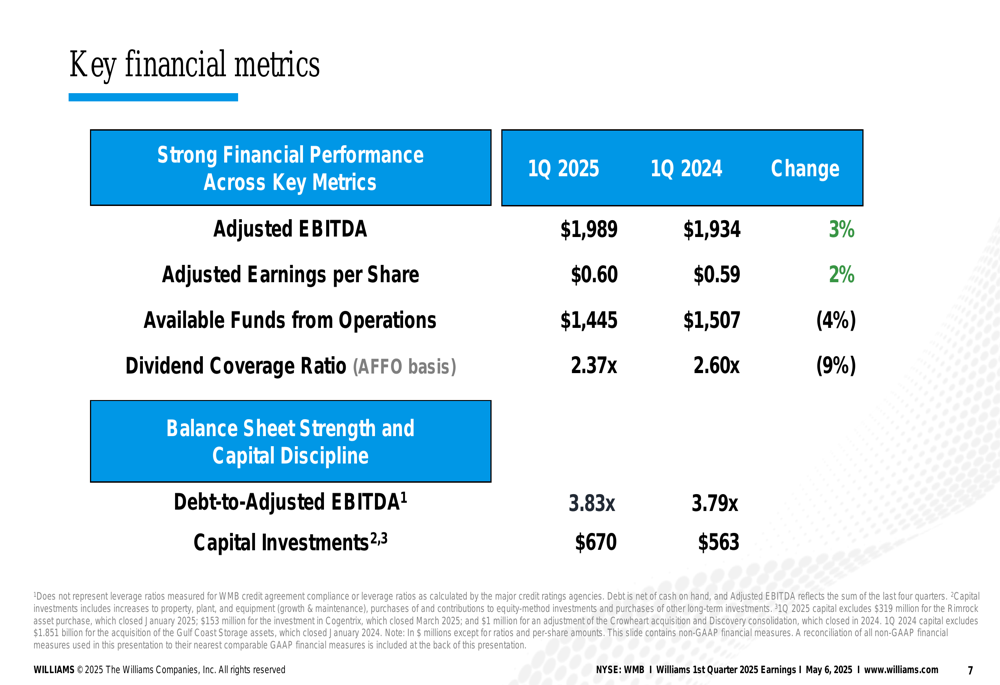

Williams’ key financial metrics for the quarter showed mixed results compared to the prior year:

While Adjusted EBITDA and Adjusted EPS showed modest growth of 3% and 2% respectively, Available Funds from Operations (AFFO) decreased by 4% to $1,445 million. The dividend coverage ratio declined from 2.60x to 2.37x, though it remains at a healthy level. Capital investments increased by 19% to $670 million as the company accelerated its growth initiatives.

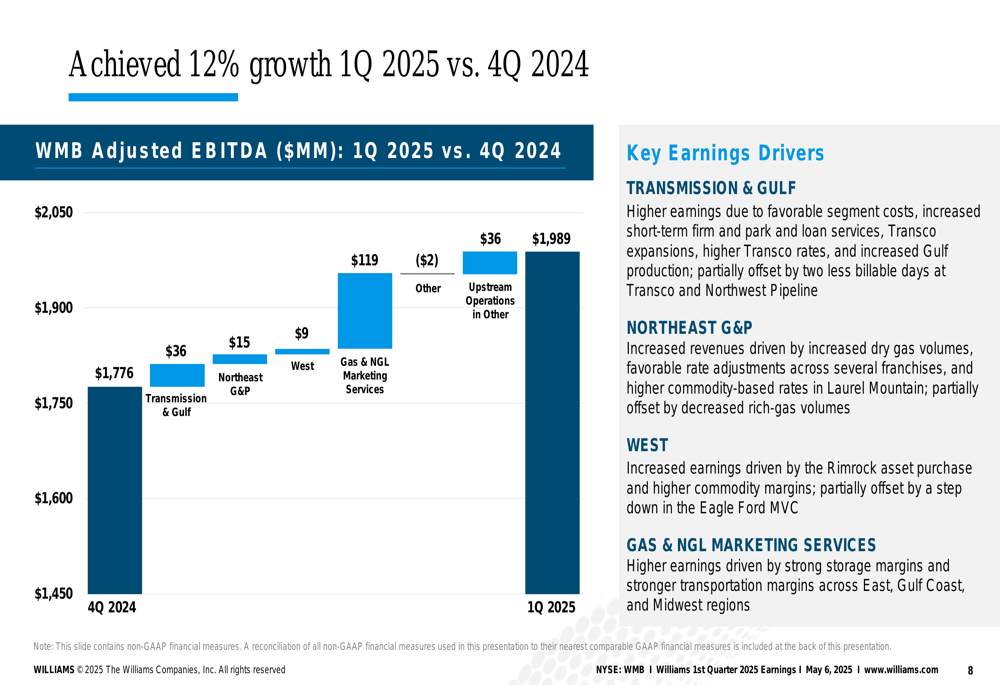

The sequential comparison with Q4 2024 showed even stronger momentum, with Adjusted EBITDA growing by 12%:

This quarter-over-quarter improvement was broad-based across all major business segments, with particularly strong contributions from Gas & NGL Marketing Services ($119 million increase) due to strong storage margins, and Transmission & Gulf ($36 million) from favorable segment costs.

Strategic Initiatives

Williams highlighted several strategic initiatives during the quarter that position the company for continued growth. The most significant announcement was the commercialization of the Socrates power generation project, which increased the company’s 2025 growth capital expenditure by $925 million.

Additionally, Williams acquired approximately 10% interest in Cogentrix Energy, enhancing its power market intelligence and creating opportunities in the rapidly growing electricity sector. The company explained that this strategic investment, which closed on March 3, 2025, will provide valuable insights into developing trends in the power market.

The company also made progress on several transmission expansion projects, including signing a precedent agreement for Transco’s Power Express expansion and placing the Whale and Ballymore projects in-service in the deepwater Gulf of Mexico.

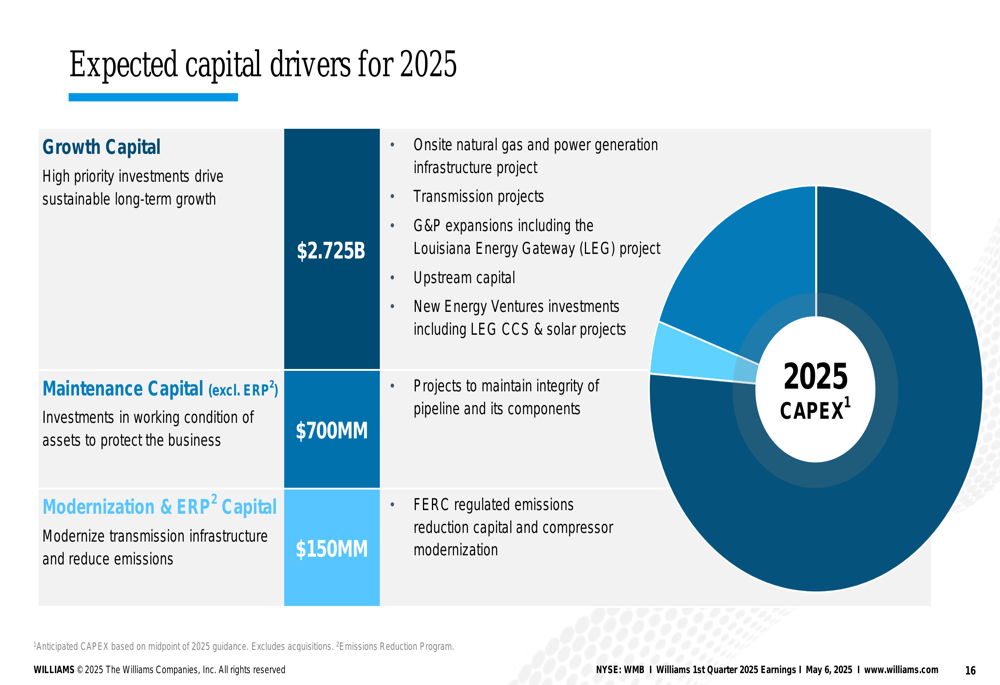

Williams’ expected capital drivers for 2025 reflect these strategic priorities:

Growth capital of $2.725 billion will be directed toward onsite natural gas and power generation infrastructure, transmission projects, gathering and processing expansions, upstream capital, and new energy ventures investments. The company will also invest $700 million in maintenance capital and $150 million in modernization and ERP capital.

Forward-Looking Guidance

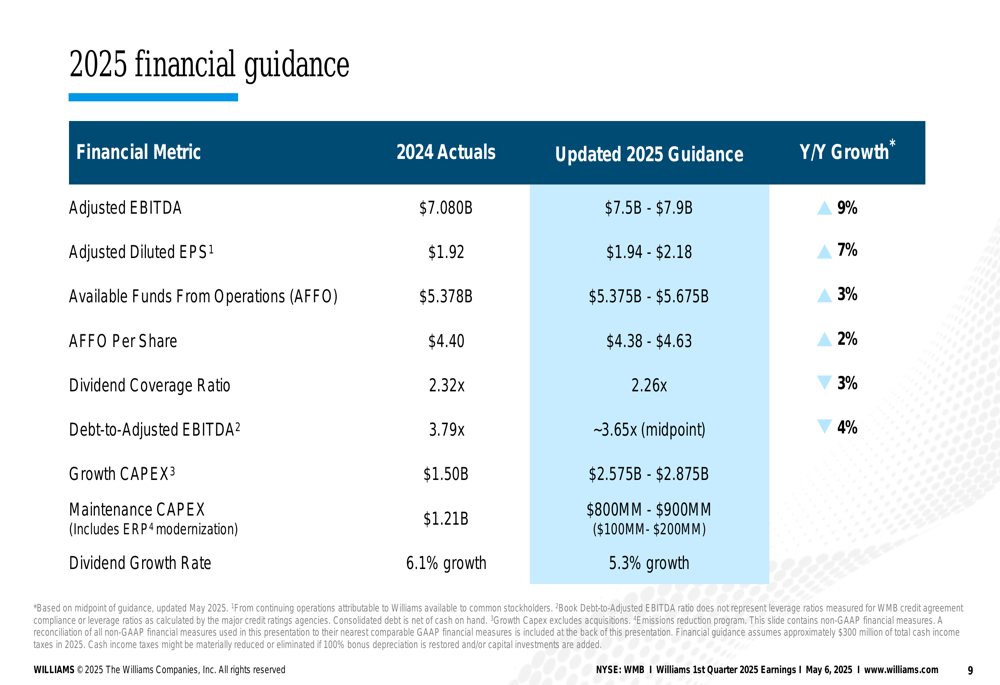

Based on strong first quarter results and the commercialization of the Socrates project, Williams raised its 2025 financial guidance:

The updated guidance projects Adjusted EBITDA of $7.5-$7.9 billion, representing 9% year-over-year growth from 2024 actuals of $7.080 billion. Adjusted EPS is expected to reach $1.94-$2.18, a 7% increase, while AFFO is projected at $5.375-$5.675 billion, up 3%. The company also anticipates improving its debt-to-adjusted EBITDA ratio to approximately 3.65x from 3.79x in 2024.

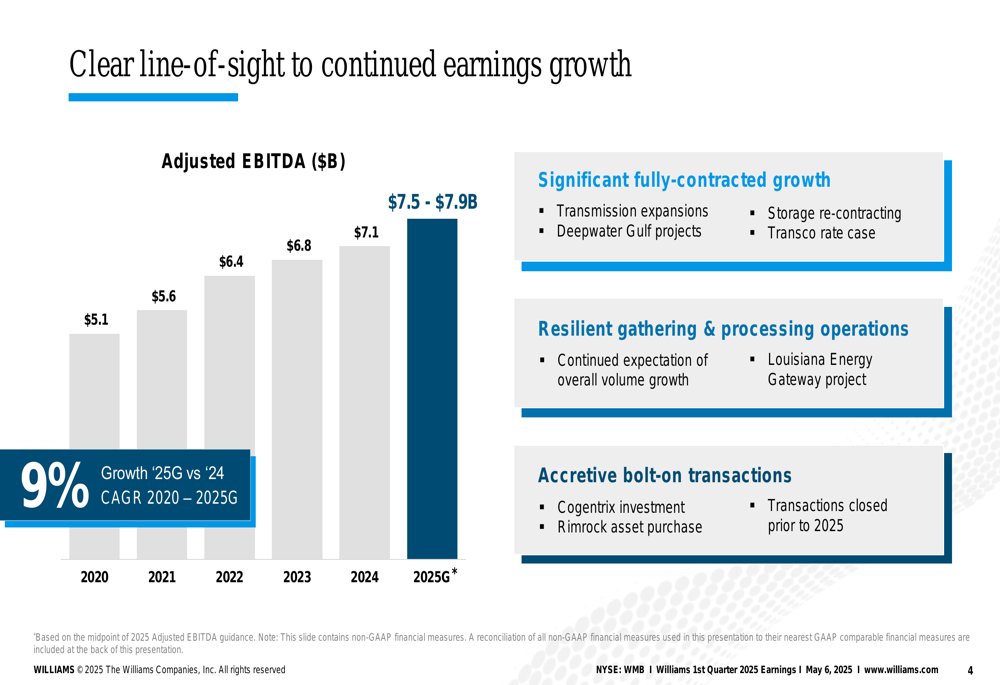

Williams has demonstrated consistent growth in Adjusted EBITDA over the past several years and expects this trend to continue:

The company’s projected 2025 Adjusted EBITDA of $7.5-$7.9 billion represents a 9% increase over 2024 and a compound annual growth rate of approximately 8% since 2020. This growth is supported by transmission expansions, deepwater Gulf projects, storage re-contracting, the Transco rate case, resilient gathering and processing operations, and accretive bolt-on transactions like the Cogentrix investment and Rimrock asset purchase.

Market Position & Opportunities

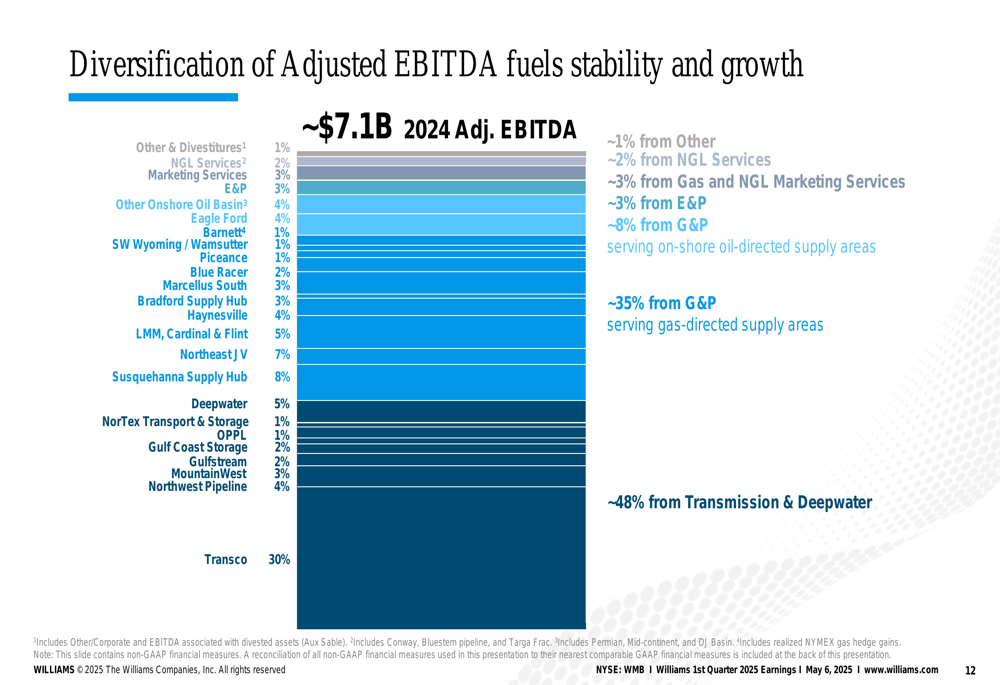

Williams emphasized its strong position in the natural gas infrastructure market, which it described as entering a "golden age of natural gas." The company’s diversified business model provides stability and multiple growth avenues:

Nearly half (48%) of Williams’ 2024 Adjusted EBITDA came from Transmission & Deepwater operations, with another 35% from gathering and processing serving gas-directed supply areas. This diversification helps insulate the company from volatility in any single segment.

The company highlighted several market trends supporting its growth strategy, including increasing natural gas demand across all sectors. Total (EPA:TTEF) demand including exports averaged 129 Bcf/d in Q1 2025, up from 122 Bcf/d in Q1 2024, driven by strong residential/commercial sector demand and export growth.

Williams also pointed to significant growth opportunities in power generation, noting that electricity demand is projected to increase by 32% from 2025 to 2040, driven by data centers and EV growth. This aligns with the company’s investments in power generation infrastructure and its strategic stake in Cogentrix.

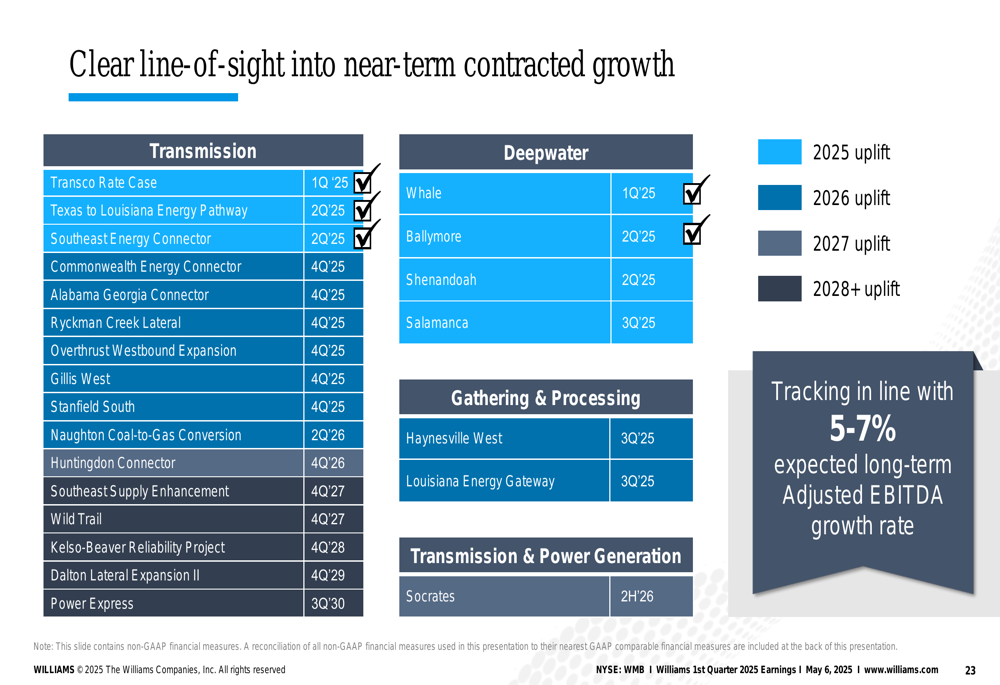

The company’s near-term growth is supported by a clear pipeline of contracted projects:

These projects span transmission, deepwater, gathering and processing, and power generation, providing visibility into growth through 2028 and beyond.

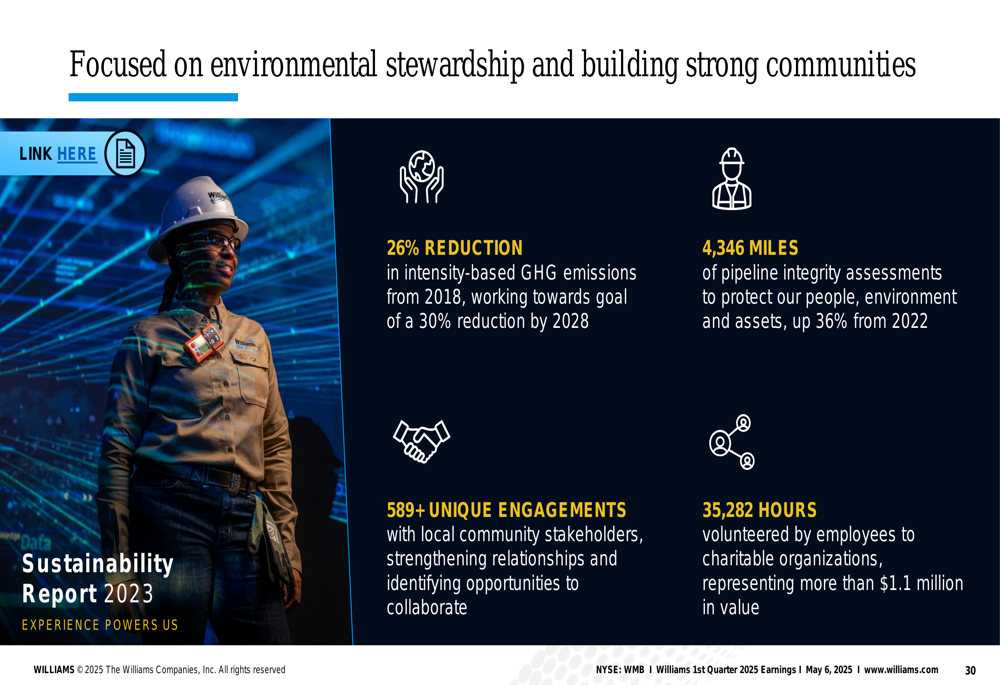

Environmental Commitments

Williams highlighted its progress on environmental stewardship and community building:

The company has achieved a 26% reduction in intensity-based greenhouse gas emissions since 2018, working toward a goal of 30% reduction by 2028. Williams completed 4,346 miles of pipeline integrity assessments in 2024, a 36% increase from 2022, while also engaging with local community stakeholders and contributing over 35,000 employee volunteer hours.

Looking forward, Williams has committed to a 5% reduction in methane intensity from 2024 for its 2025 annual incentive plan, with goals to reach 0.0375% in scope 1 methane intensity by 2028 and achieve a net-zero ambition by 2050.

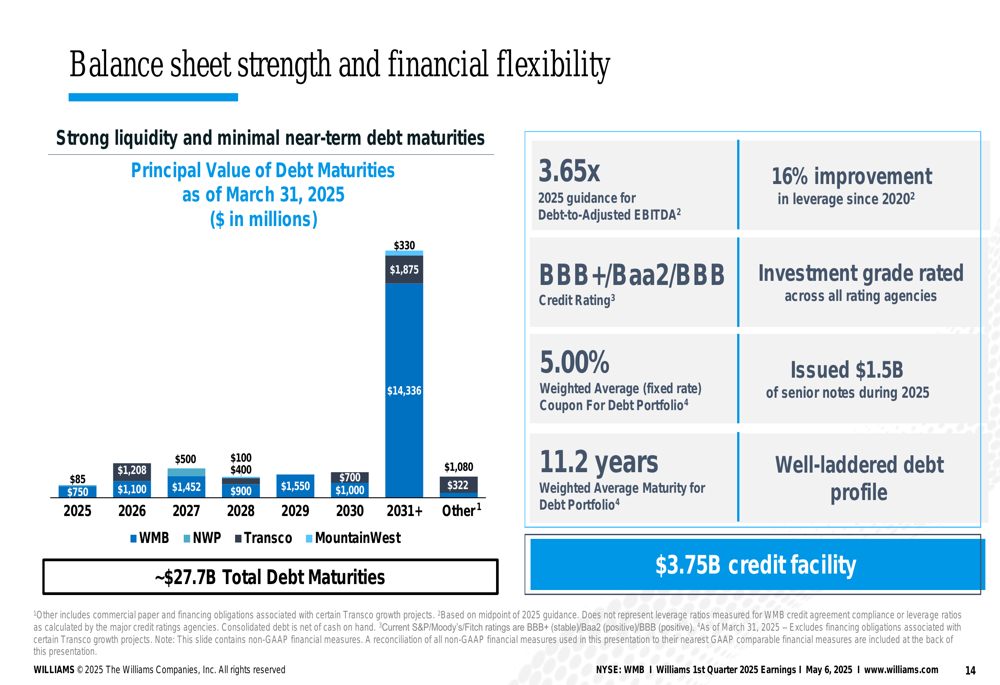

Balance Sheet Strength

Williams emphasized its financial flexibility and strong balance sheet position:

The company’s debt-to-adjusted EBITDA ratio is expected to improve to 3.65x in 2025, representing a 16% improvement since 2020. Williams maintains investment-grade ratings across all agencies, with a recent upgrade to BBB+ from S&P. The company’s debt portfolio has a weighted average fixed-rate coupon of 5.00% and a weighted average maturity of 11.2 years, providing stability and predictability in its capital structure.

During 2025, Williams issued $1.5 billion of senior notes and maintains a $3.75 billion credit facility, giving it ample liquidity to fund its growth initiatives while maintaining financial discipline.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.