Trump announces 100% chip tariff as Apple ups U.S. investment

Introduction & Market Context

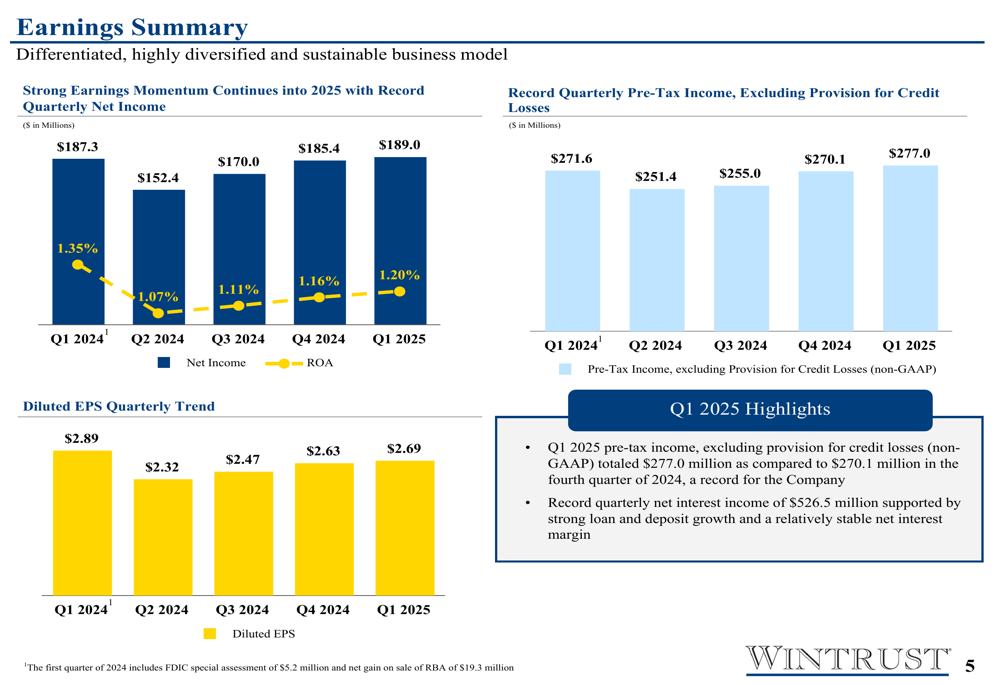

Wintrust Financial Corporation (NASDAQ:WTFC) released its Q1 2025 earnings presentation on April 22, showcasing record quarterly net income and continued balance sheet expansion. The regional bank reported net income of $189.0 million, up $3.7 million from the previous quarter, while maintaining a stable net interest margin despite competitive pressures in the lending market.

The company’s stock has faced some pressure in recent months, trading at $101.43 as of April 21, 2025, down from around $133 at the end of 2024, despite the continued strong operational performance. This disconnect may reflect broader concerns about regional banks amid changing interest rate expectations and increased competition for loans.

Quarterly Performance Highlights

Wintrust delivered record quarterly net income of $189.0 million, translating to diluted earnings per share of $2.69, a $0.06 increase from Q4 2024. The company’s profitability metrics showed improvement across the board, with Return on Assets (ROA) increasing to 1.20% (+4 basis points), Return on Equity (ROE) rising to 12.21% (+39 basis points), and Return on Tangible Common Equity (ROTCE) climbing to 14.72% (+43 basis points).

As shown in the following chart, Wintrust has maintained strong earnings momentum through the first quarter of 2025, with five consecutive quarters of solid performance:

The company’s efficiency ratio improved to 57.21% (GAAP), down 25 basis points from the previous quarter, indicating better expense management relative to revenue generation. Pre-tax, pre-provision income reached $277.0 million, a $7.0 million increase from Q4 2024, highlighting the underlying strength of the core business.

Detailed Financial Analysis

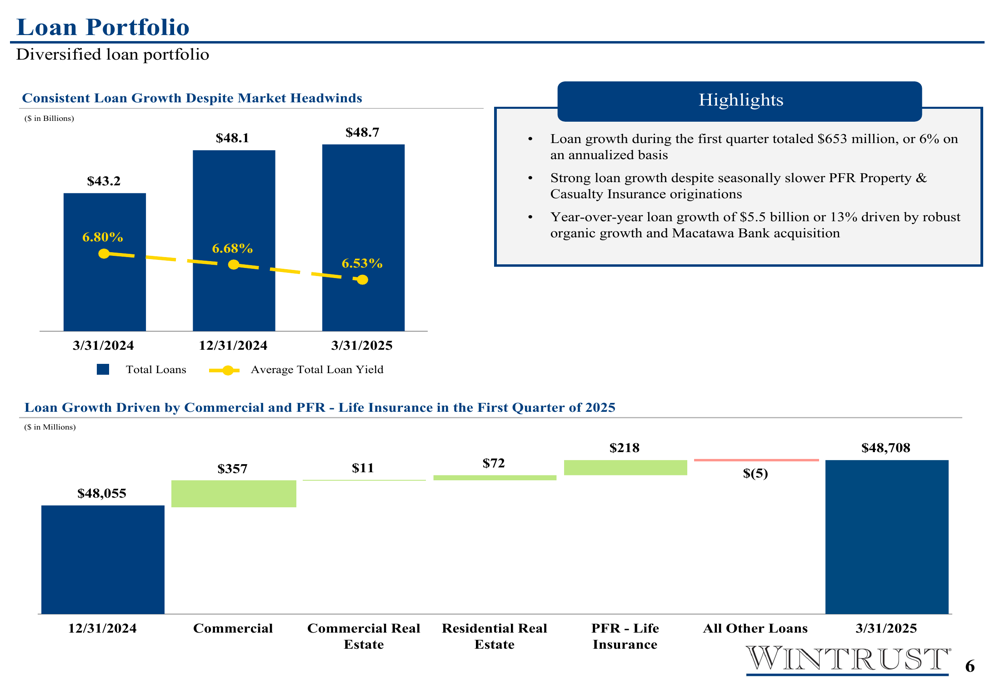

Wintrust’s balance sheet continued to expand in Q1 2025, with total assets reaching $65.9 billion, up $1.0 billion from the previous quarter. The growth was driven by increases in both loans and deposits, maintaining a balanced approach to expansion.

Total (EPA:TTEF) loans grew to $48.7 billion, representing a $0.7 billion or 6% annualized increase from Q4 2024. As illustrated in the following chart, loan growth was primarily driven by commercial and premium finance - life insurance portfolios:

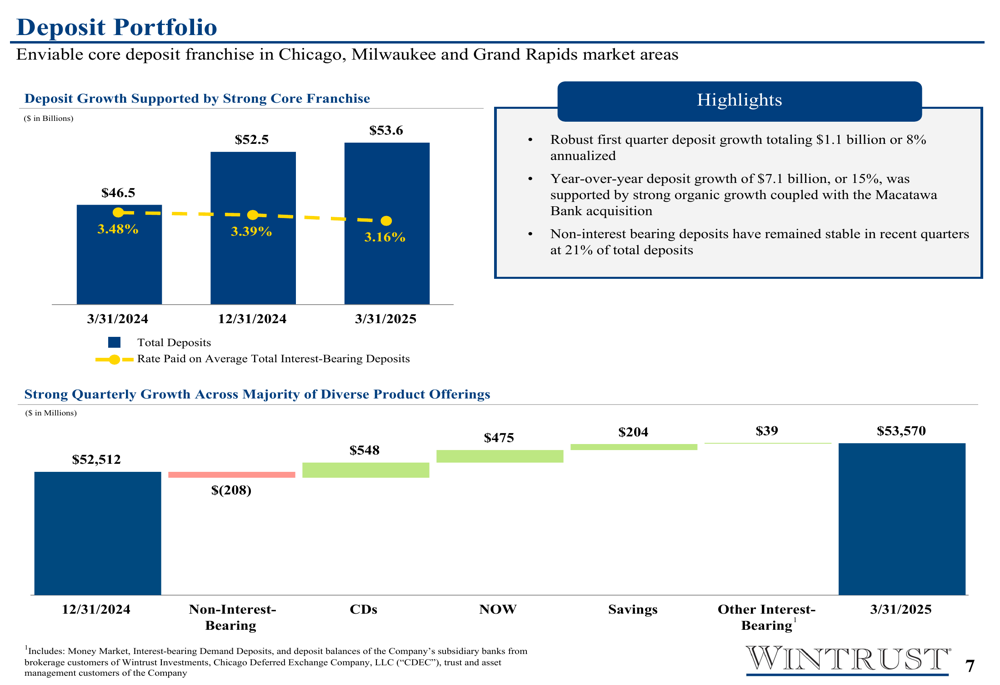

On the funding side, deposits increased to $53.6 billion, up $1.1 billion or 8% annualized from the previous quarter. Year-over-year deposit growth was even more impressive at 15% or $7.1 billion, supported by both organic growth and the Macatawa Bank acquisition completed in 2024. The following chart shows the composition of deposit growth across various product categories:

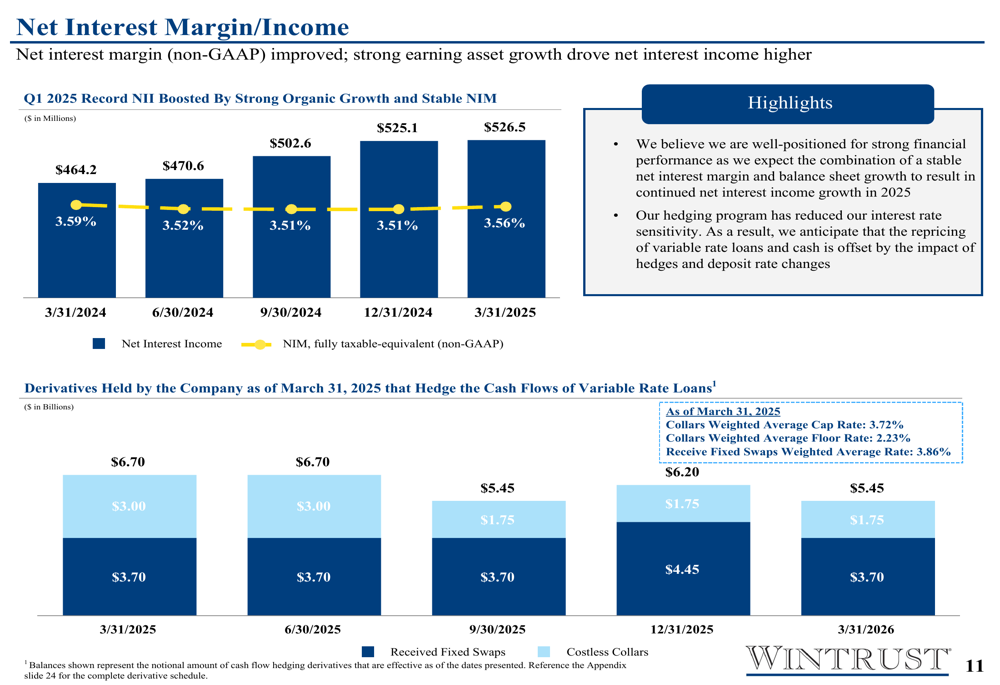

The net interest margin remained stable at 3.56%, supporting record quarterly net interest income of $526.5 million. This stability is particularly notable given the changing interest rate environment and increased competition for loans mentioned during the company’s Q4 2024 earnings call.

As shown in the following chart, Wintrust has effectively managed its net interest margin through various interest rate cycles:

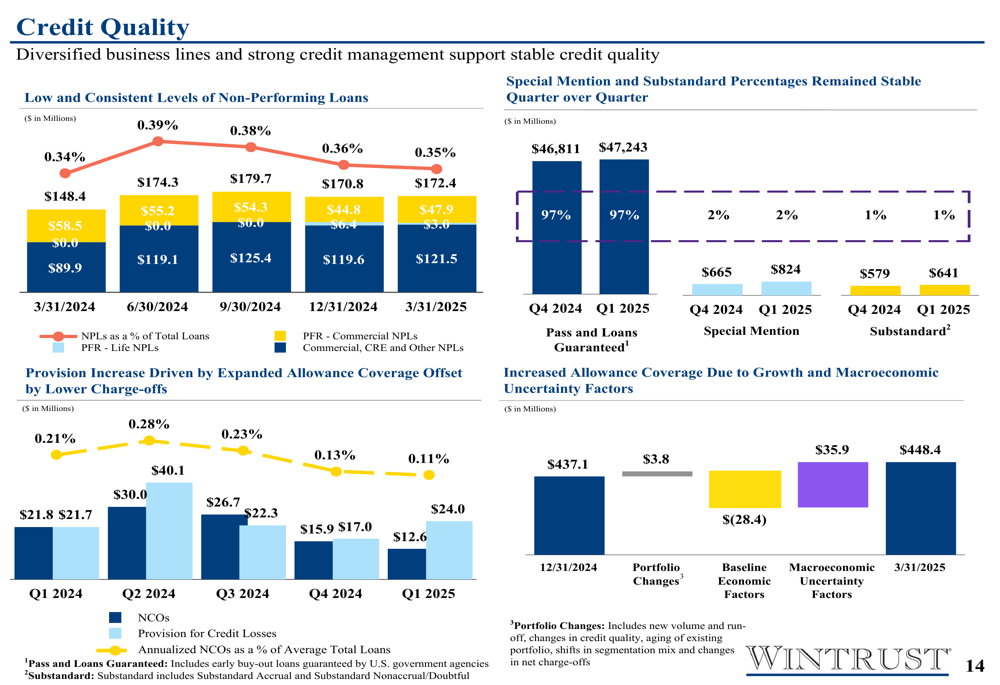

Credit quality remained strong, with non-performing loans decreasing during the quarter. The allowance for credit losses stood at 1.37% of total loans as of March 31, 2025, reflecting the company’s conservative approach to risk management. The following chart illustrates the company’s credit quality metrics:

Strategic Initiatives

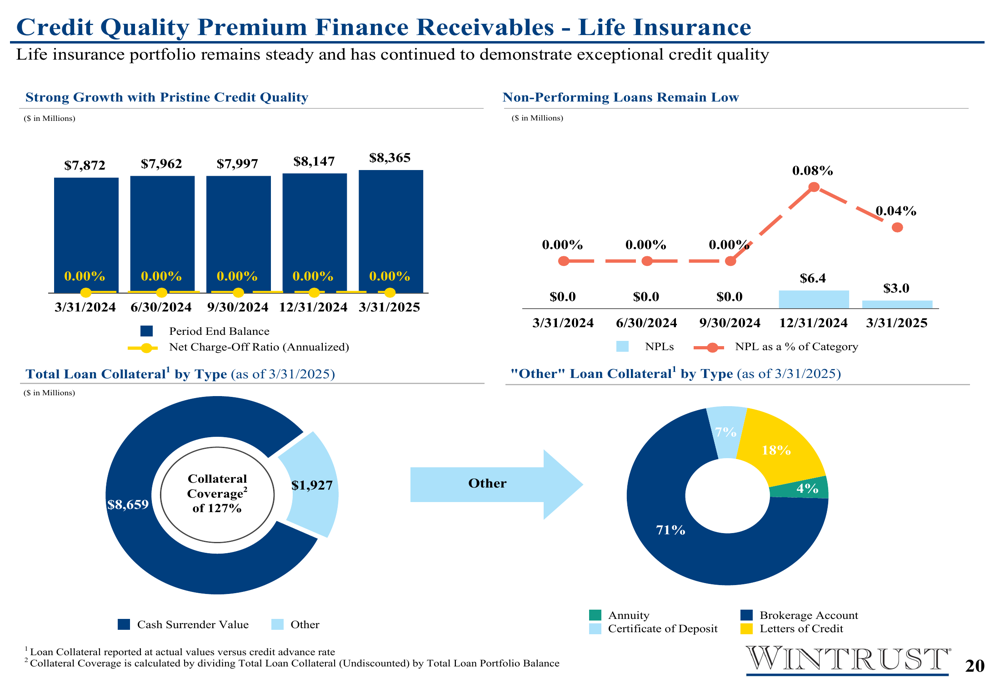

Wintrust continues to leverage its diversified business model, with specialty niches providing competitive advantages in a challenging market environment. The Premium Finance Receivables - Life Insurance (NSE:LIFI) portfolio has been a particular bright spot, demonstrating exceptional credit quality while contributing to growth.

The following chart highlights the strong performance of the life insurance premium finance business:

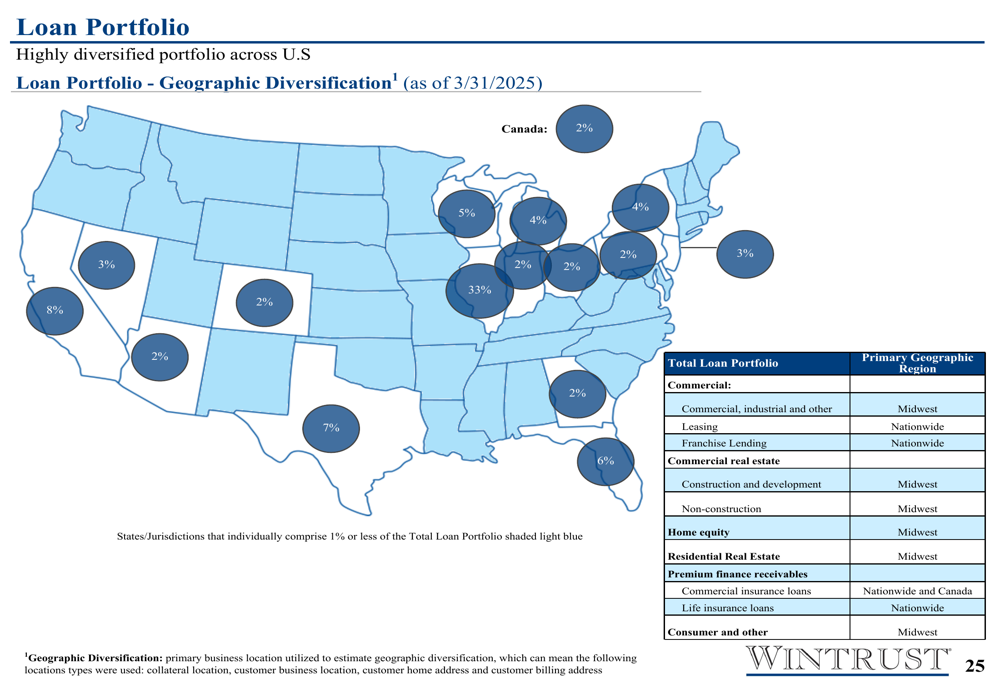

The company’s geographic diversification strategy is evident in its loan portfolio distribution, with a strong presence in the Midwest but also meaningful exposure to other regions:

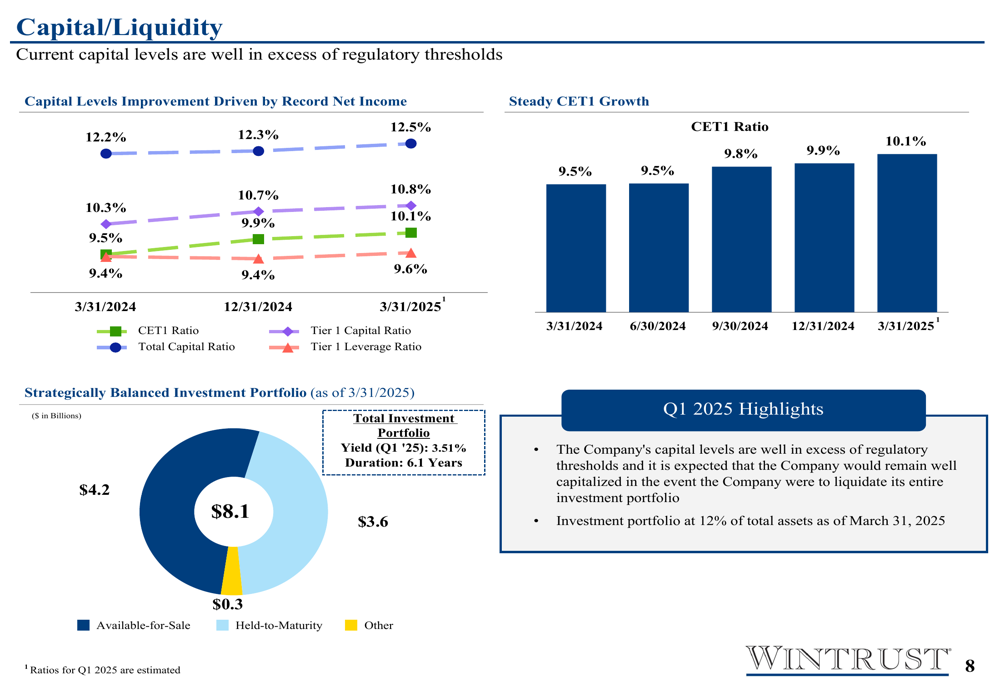

Capital levels remained well above regulatory requirements, with the CET1 ratio improving to 9.6%, up from 9.4% in the previous quarter. This strong capital position provides flexibility for continued organic growth and potential acquisitions.

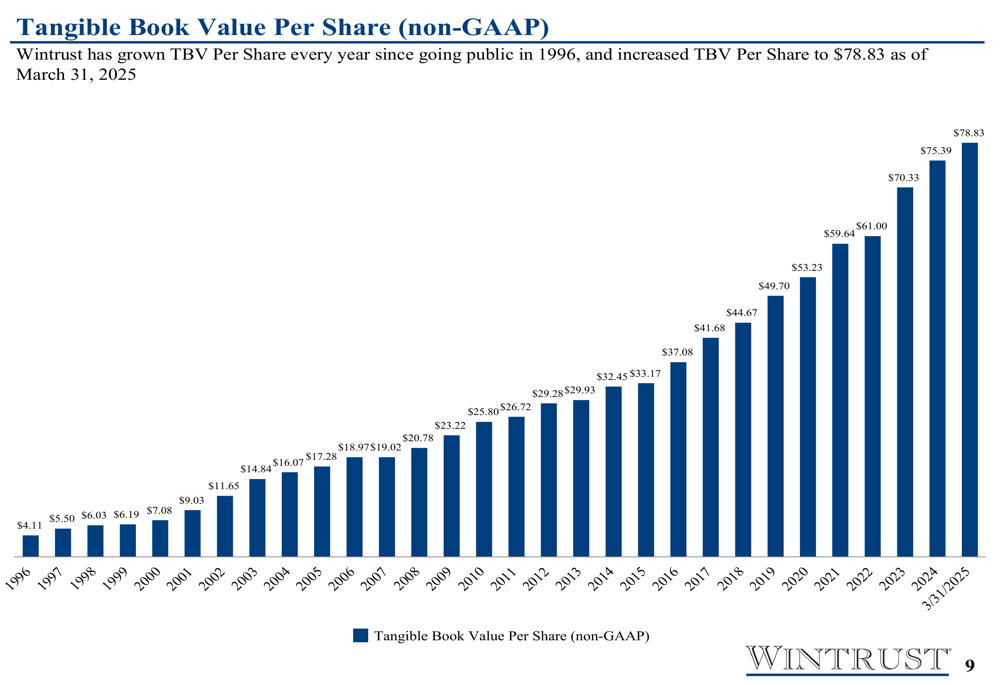

Tangible book value per share reached $78.83 as of March 31, 2025, continuing the company’s unbroken streak of annual growth since going public. This consistent value creation has been a hallmark of Wintrust’s long-term performance:

Forward-Looking Statements

Looking ahead to the remainder of 2025, Wintrust appears well-positioned to maintain its growth trajectory despite competitive pressures in the loan market. During the Q4 2024 earnings call, management anticipated mid to high single-digit loan growth for 2025 with a stable net interest margin around 3.50%, expectations that align with the Q1 2025 results.

The company’s hedging strategy, including $8.45 billion in receive-fixed swaps and collars, provides protection against potential interest rate volatility. This balanced approach to interest rate risk management should help maintain margin stability regardless of the timing and magnitude of Federal Reserve rate cuts.

Management previously highlighted increased competition in loan pricing, particularly in commercial real estate, as banks look to deploy capital. This competitive pressure was acknowledged in the Q1 presentation, but Wintrust’s diversified business model and niche specialties appear to be providing sufficient growth opportunities despite these challenges.

Wintrust’s continued investment in geographic expansion, including its recent growth in Rockford, Illinois, and the integration of Macatawa Bank in Western Michigan, provides additional avenues for growth beyond its core Chicago market. These initiatives, combined with the company’s strong credit quality and capital position, suggest Wintrust is well-equipped to navigate the competitive landscape while continuing to deliver strong financial results throughout 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.