September looms as a risk month for stocks, Yardeni says

Introduction & Market Context

Wolfspeed Inc. (NYSE:WOLF) presented its second quarter fiscal year 2025 earnings on January 29, 2025, revealing a company in transition as it navigates challenging market conditions. The silicon carbide specialist reported declining revenue and margins while emphasizing its strategic shift to 200mm manufacturing and aggressive cost-cutting measures to improve its financial position.

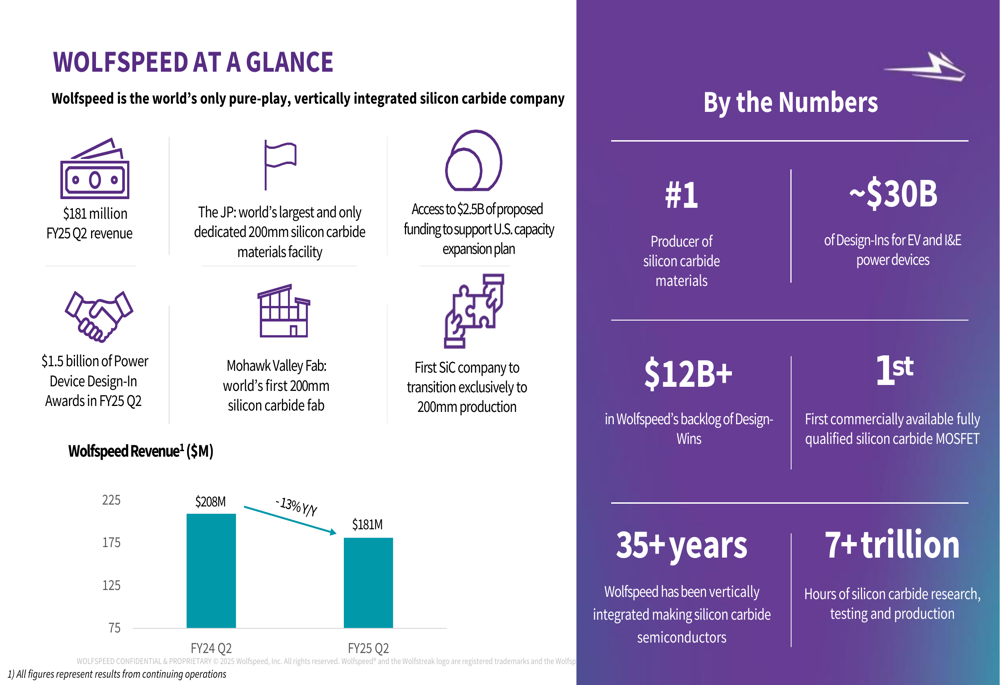

The presentation comes at a critical time for Wolfspeed, as the company positions itself as "the world’s only pure-play, vertically integrated silicon carbide company" amid growing demand for silicon carbide in electric vehicles and industrial applications, despite current market softness.

As shown in the following overview of Wolfspeed’s business and key metrics:

Quarterly Performance Highlights

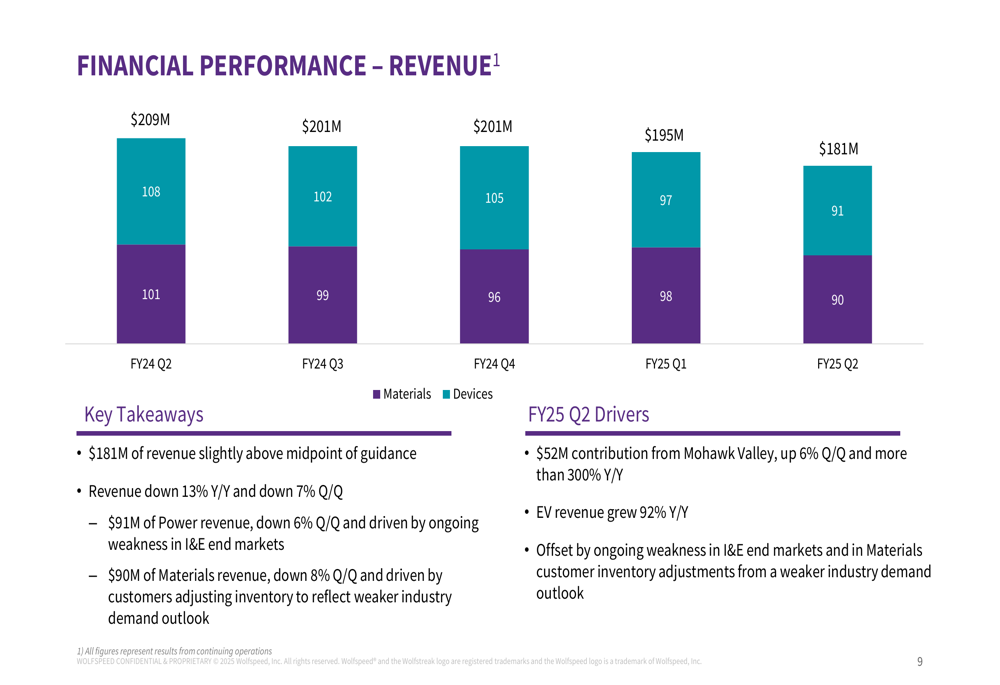

Wolfspeed reported Q2 FY25 revenue of $181 million, down 13% year-over-year and 7% sequentially. The company’s revenue was slightly above the midpoint of its guidance, but reflected ongoing weakness in both its materials and devices segments.

The revenue breakdown shows balanced contributions from both segments, with materials revenue at $90 million (down 8% quarter-over-quarter) and power device revenue at $91 million (down 6% quarter-over-quarter). The materials segment decline was attributed to customers adjusting inventory levels in response to weaker industry demand, while the power segment continued to face headwinds in industrial and energy end markets.

The following chart illustrates Wolfspeed’s revenue trend over recent quarters:

Non-GAAP gross margin deteriorated significantly to 2% in Q2 FY25, compared to 16% in the same quarter last year. This decline reflects the impact of lower revenue, restructuring costs, and ongoing investments in new facilities while operating at lower utilization rates.

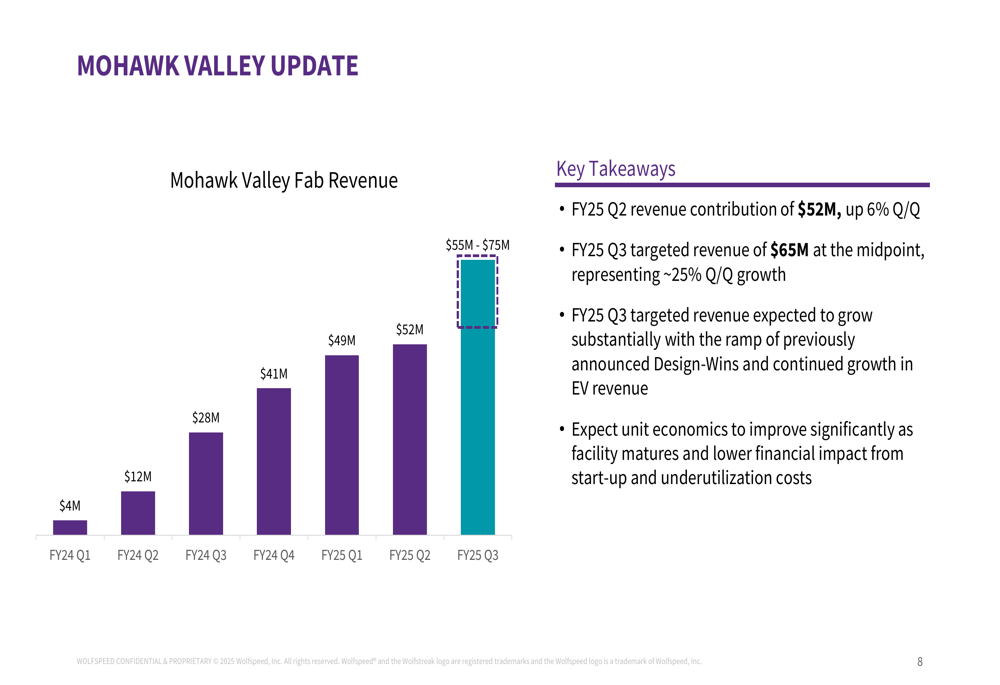

One bright spot in the results was the Mohawk Valley Fab, which contributed $52 million in revenue during Q2, up 6% sequentially. The company expects this facility to drive future growth as it ramps production of 200mm silicon carbide devices.

As shown in the following chart of Mohawk Valley Fab’s revenue progression:

Strategic Initiatives

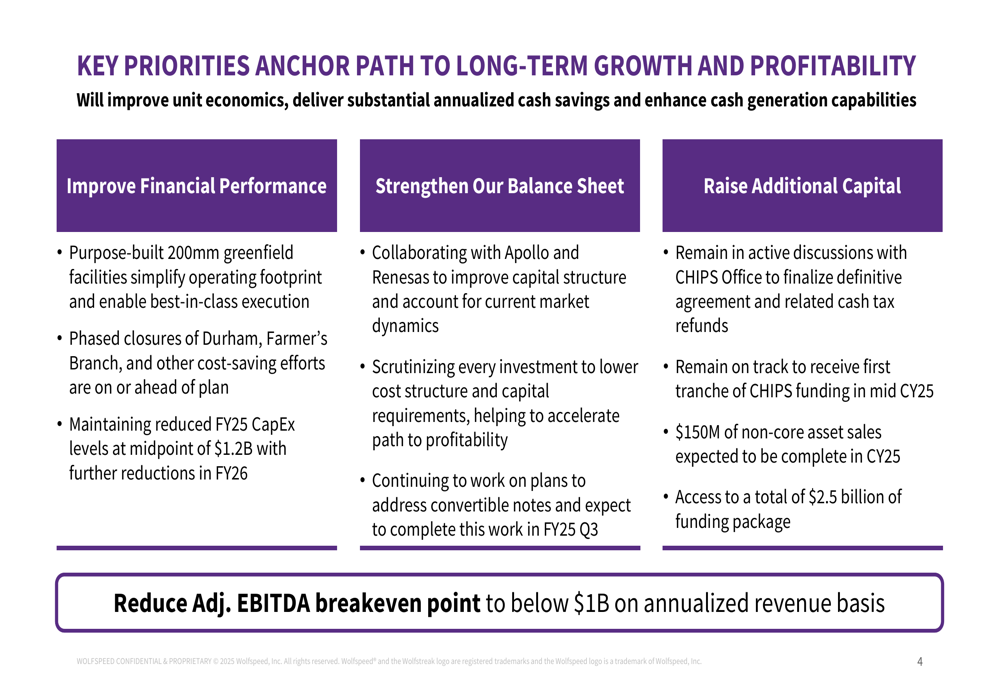

Wolfspeed outlined three key strategic priorities aimed at improving its financial performance, strengthening its balance sheet, and raising additional capital. The company is implementing significant cost-saving measures, including phased closures of facilities in Durham, North Carolina and Farmer’s Branch, Texas, as it transitions to purpose-built 200mm greenfield facilities.

The following slide details these strategic priorities:

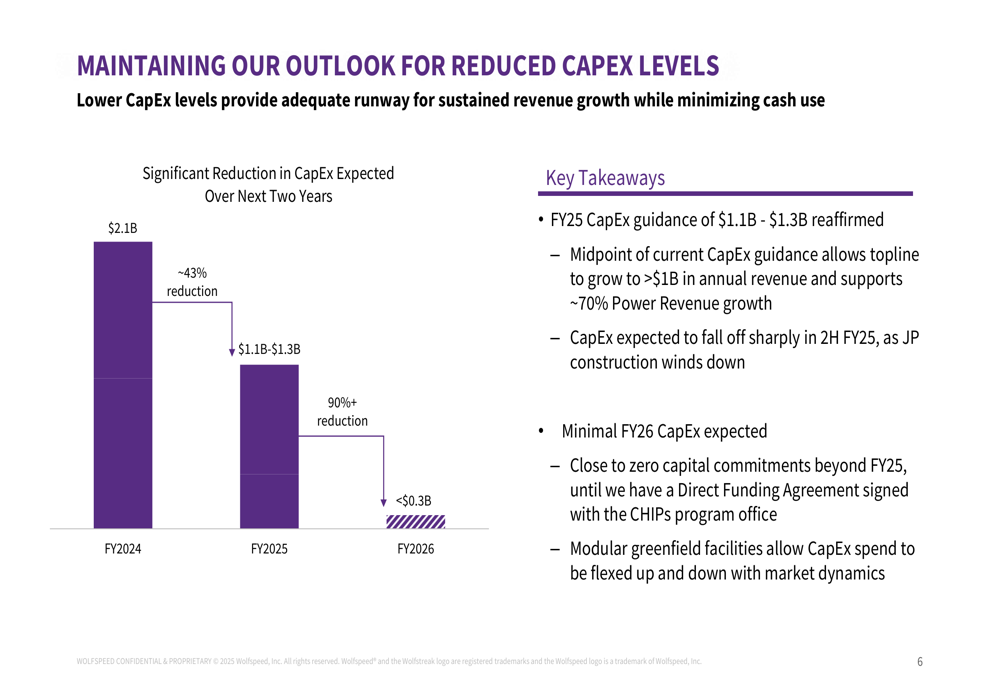

A central element of Wolfspeed’s strategy is the dramatic reduction in capital expenditures. The company reaffirmed its FY25 CapEx guidance of $1.1-$1.3 billion, representing a 43% reduction from FY24 levels. More significantly, it expects FY26 CapEx to fall below $300 million, a 90% reduction from FY24 levels, as construction of its JP materials facility in Siler City, North Carolina winds down.

This CapEx reduction strategy is illustrated in the following chart:

The company is also simplifying its manufacturing footprint by focusing on three key facilities: its headquarters in Durham for crystal growth and substrate processing, the JP facility in Siler City for 200mm materials production, and the Mohawk Valley Fab in Marcy, New York for device manufacturing. Wolfspeed reported that 200mm yields at the JP facility are exceeding expectations, and the company remains on track to receive a Certificate of Occupancy in the first half of calendar year 2025.

Financial Outlook

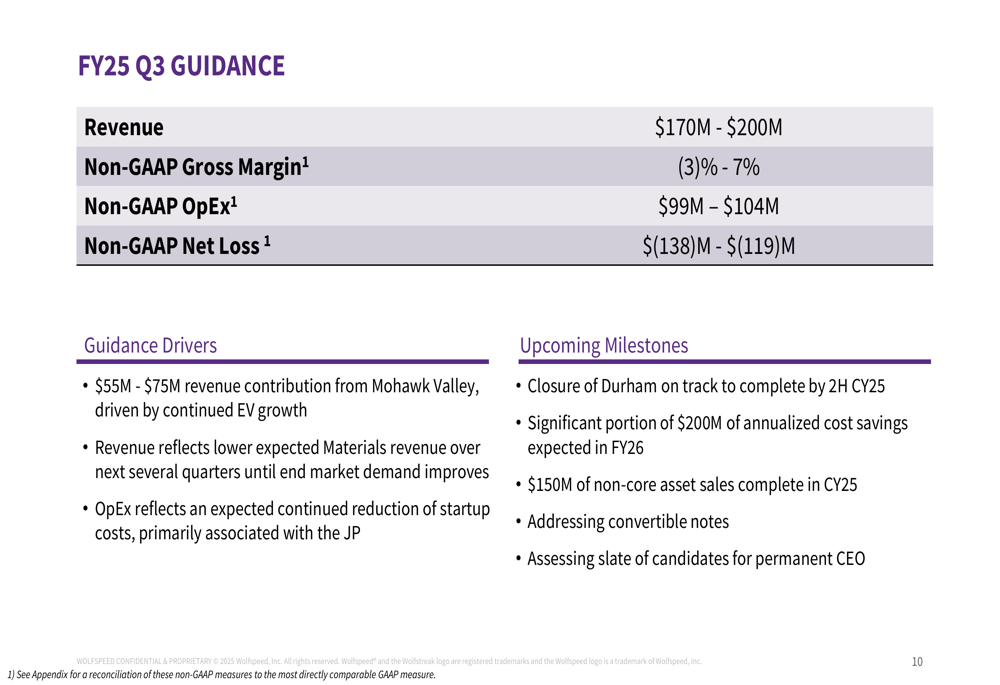

For the third quarter of FY25, Wolfspeed guided for revenue of $170-$200 million and non-GAAP gross margin of -3% to 7%. The company expects Mohawk Valley Fab to contribute $55-$75 million to Q3 revenue, representing approximately 25% sequential growth at the midpoint.

The following slide details the company’s Q3 FY25 guidance:

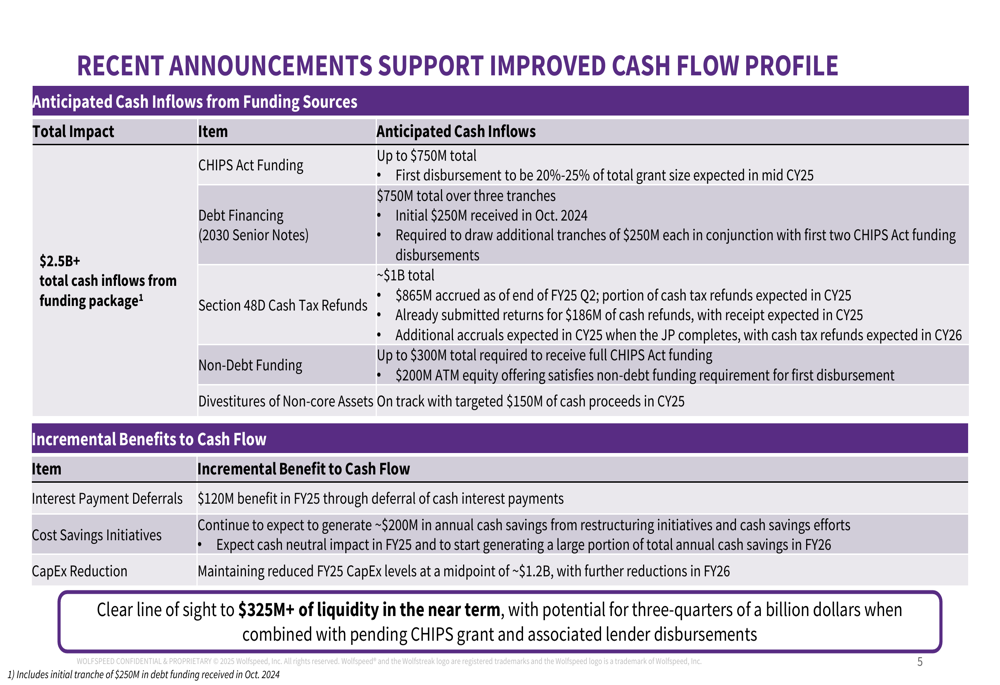

Wolfspeed is also focused on improving its cash flow profile through multiple initiatives. The company anticipates significant cash inflows from various funding sources, including up to $750 million in CHIPS Act funding, with the first disbursement expected in mid-calendar year 2025. Additionally, Wolfspeed expects to receive approximately $1 billion in Section 48D cash tax refunds, with $865 million already accrued as of the end of Q2 FY25.

The company’s cash flow improvement strategy is detailed in the following slide:

Forward-Looking Statements

Despite current financial challenges, Wolfspeed maintains a positive long-term outlook based on its technology leadership and market position. The company highlighted its $1.5 billion of Power Device Design-In Awards in Q2 FY25 and a total of approximately $30 billion of Design-Ins for electric vehicle and industrial & energy power devices. Additionally, Wolfspeed reported over $12 billion in its backlog of Design-Wins.

However, subsequent events suggest the company’s challenges may be more severe than indicated in the Q2 presentation. According to recent earnings reports, Wolfspeed announced a 25% reduction in workforce in Q3 FY25, and its stock fell 18.74% following the Q3 earnings release despite beating EPS expectations. The company’s stock has declined dramatically over the past year, with current trading around $1.29, far below its 52-week high of $17.45.

Wolfspeed is targeting an EBITDA breakeven point at $800 million of annualized revenue and aims to generate $200 million in positive unlevered operating cash flow by FY2026. The company expects $600 million in tax credit refunds in FY2026, which could significantly improve its financial position.

As Wolfspeed navigates this challenging transition period, its success will depend on effectively executing its cost-reduction initiatives, successfully ramping 200mm production, and capitalizing on long-term growth opportunities in electric vehicles and industrial applications.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.