Beamr video compression achieves up to 50% improvement for AVs

Introduction & Market Context

Workday, Inc. (NASDAQ:WDAY) released its Q2 FY26 investor presentation on August 21, 2025, highlighting continued revenue growth and significant margin expansion. The enterprise software provider, which specializes in human capital management and financial management applications, reported solid performance metrics while emphasizing its ongoing investments in artificial intelligence capabilities.

The company continues to operate in a large addressable market estimated at $160 billion, serving over 11,000 global customers across more than 175 countries. Workday’s strong position in the enterprise software market is evidenced by its penetration of more than 65% of Fortune 500 companies, including over 70% of the top 50.

Quarterly Performance Highlights

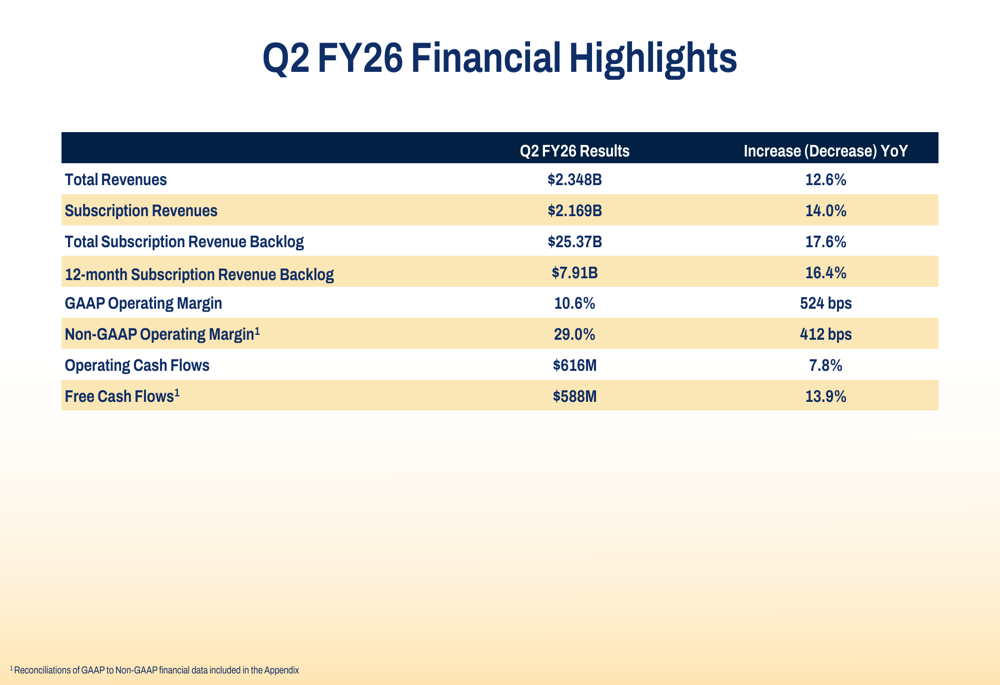

Workday reported total revenues of $2.348 billion for Q2 FY26, representing a 12.6% increase year-over-year. Subscription revenues, which form the core of the company’s business model, grew at a faster pace of 14.0% to reach $2.169 billion.

The company’s backlog metrics showed even stronger growth, with total subscription revenue backlog increasing by 17.6% year-over-year to $25.37 billion, while the 12-month subscription revenue backlog grew by 16.4% to $7.91 billion. These figures suggest continued momentum in Workday’s business and provide visibility into future revenue streams.

As shown in the following financial highlights chart:

Profitability metrics also showed substantial improvement. GAAP operating margin expanded by 524 basis points to 10.6%, while non-GAAP operating margin increased by 412 basis points to 29.0%. Cash flow generation remained strong, with operating cash flows of $616 million (up 7.8% year-over-year) and free cash flows of $588 million (up 13.9% year-over-year).

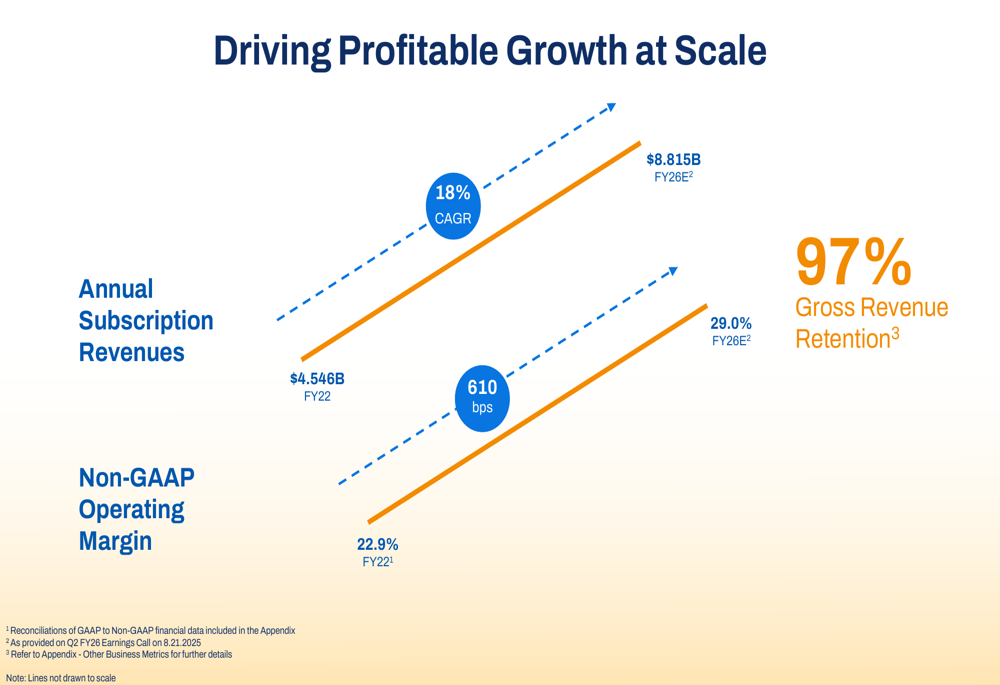

The company’s long-term growth trajectory demonstrates consistent execution on its strategy to drive profitable growth at scale:

Strategic Initiatives and Customer Wins

During the quarter, Workday continued to expand its customer base, welcoming new clients including Banamex, Carrefour (EPA:CARR), Masan Group, Memorial Health, and Red Coats. The company also expanded existing relationships with major enterprises such as Google (NASDAQ:GOOGL), Nationwide Insurance, Qantas Airways, Randstad (AS:RAND), Tokyo Electron, and University of Virginia.

The following image highlights some of the key customer wins and expansions from the quarter:

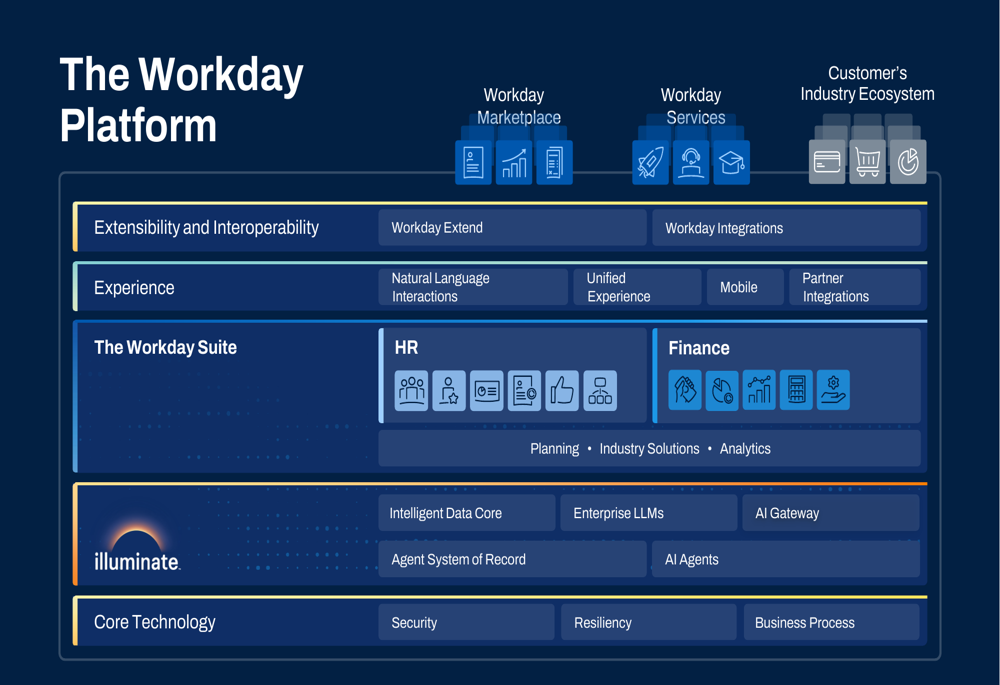

Workday has been actively enhancing its AI capabilities through strategic acquisitions and product development. The company entered into an agreement to acquire Paradox and completed the acquisition of Flowise during the quarter. Additionally, Workday unveiled a new AI developer toolset and introduced the Workday Agent Partner Network, further strengthening its position in the rapidly evolving AI space.

The company’s platform architecture illustrates how Workday is integrating AI capabilities across its product suite:

Other strategic initiatives included the launch of Workday Government to target the public sector market and an expanded presence in India, including the appointment of Sunil Jose as President of India. The company’s user community now represents more than 75 million users and processes over 1 trillion transactions annually.

Guidance and Forward-Looking Statements

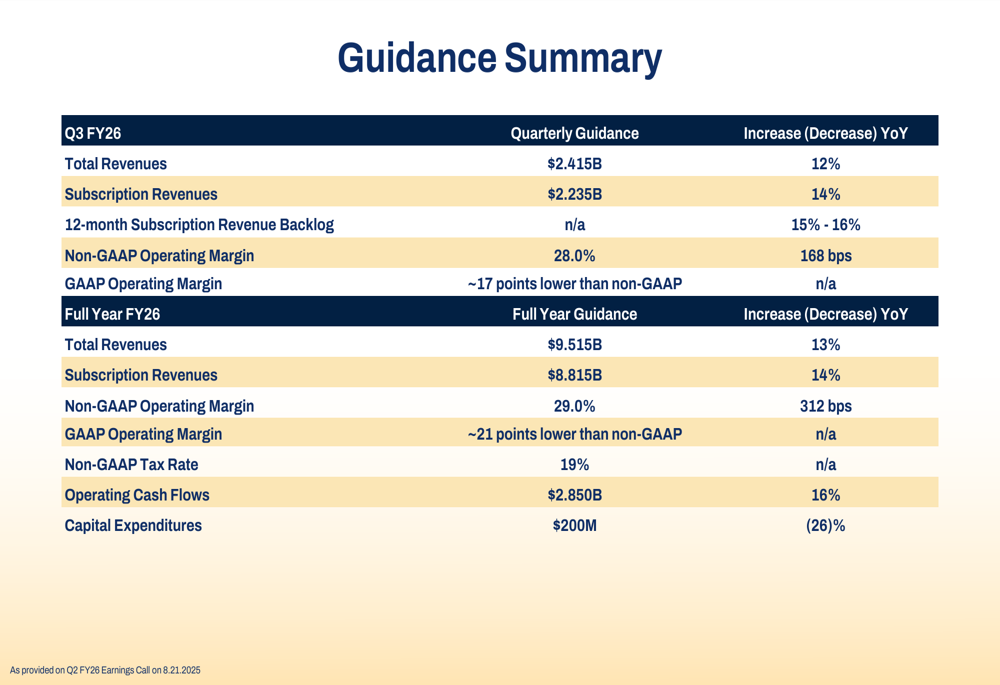

Looking ahead, Workday provided guidance for both Q3 FY26 and the full fiscal year. For Q3, the company expects total revenues of $2.415 billion (12% year-over-year increase) and subscription revenues of $2.235 billion (14% year-over-year increase). The 12-month subscription revenue backlog is projected to grow by 15-16%, while non-GAAP operating margin is expected to be 28.0%, representing a 168 basis point increase.

For the full fiscal year 2026, Workday forecasts total revenues of $9.515 billion (13% year-over-year increase) and subscription revenues of $8.815 billion (14% year-over-year increase). The company expects a non-GAAP operating margin of 29.0%, which would be a 312 basis point improvement. Operating cash flows are projected to reach $2.850 billion, a 16% increase from the previous year.

The detailed guidance summary is presented below:

Market Reaction and Conclusion

Despite the strong quarterly results and positive guidance, Workday’s stock showed a slight decline of 0.69% in after-hours trading, with the price falling to $225.91. This follows a pattern observed in previous quarters, where solid financial performance hasn’t necessarily translated into immediate stock price appreciation. After the Q1 FY26 results, the stock had declined by 6.83% despite beating analyst expectations.

Workday continues to maintain strong financial health with more cash than debt on its balance sheet. The company’s consistent execution on its strategy to drive profitable growth at scale is evident in the expanding operating margins and steady revenue growth. With a gross revenue retention rate of 97%, Workday demonstrates strong customer loyalty and a stable recurring revenue base.

The company’s focus on AI innovation, international expansion, and penetration of the government sector positions it well for continued growth. However, investors appear to be taking a cautious approach, potentially due to broader market conditions or concerns about sustaining growth rates in an increasingly competitive enterprise software landscape.

As Workday continues to execute on its strategic initiatives and maintain its financial discipline, the company remains well-positioned to capitalize on its large addressable market and expand its presence in the enterprise software space.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.