TSX jumps amid Fed rate cut hopes, ongoing U.S. government shutdown

XPLR Infrastructure LP Unit (NYSE:XIFR) reported its second quarter 2025 results on August 7, showing modest financial performance improvement amid ongoing efforts to restructure its capital framework and optimize its renewable energy portfolio. The company, which has faced significant challenges since its disappointing Q4 2024 earnings, continues to execute on its strategic initiatives while working to regain investor confidence.

Introduction & Market Context

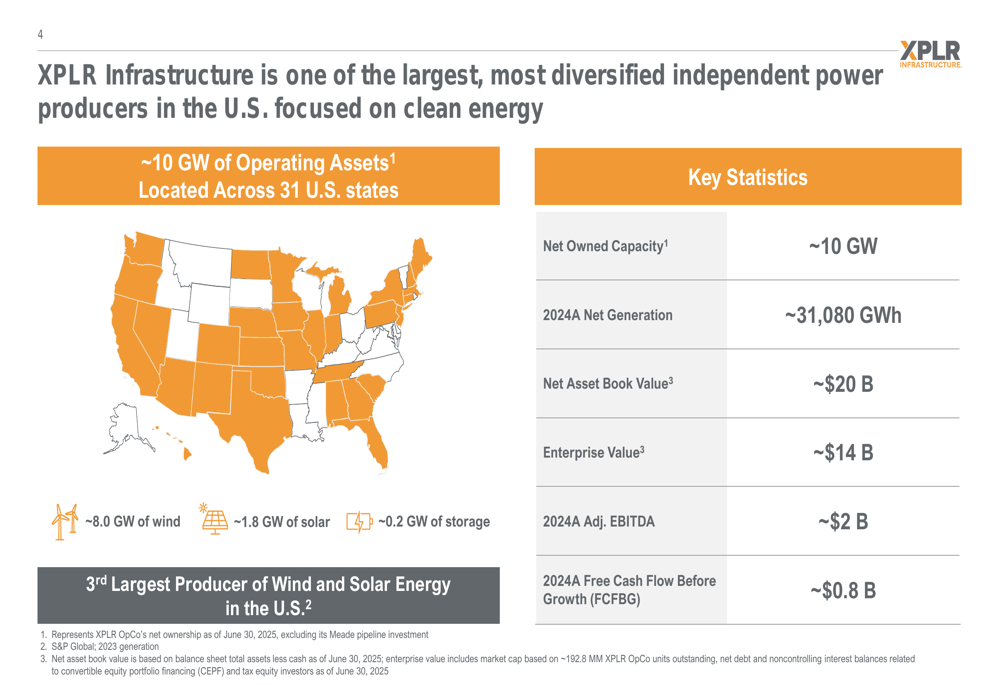

XPLR Infrastructure, the third-largest producer of wind and solar energy in the United States, operates approximately 10 GW of clean energy assets across 31 states. Despite the company’s significant renewable energy footprint, XIFR shares have struggled, trading at $8.90 as of the presentation date, near its 52-week low of $7.53 and far below its 52-week high of $28.25.

As shown in the following overview of XPLR’s operations and financial scale:

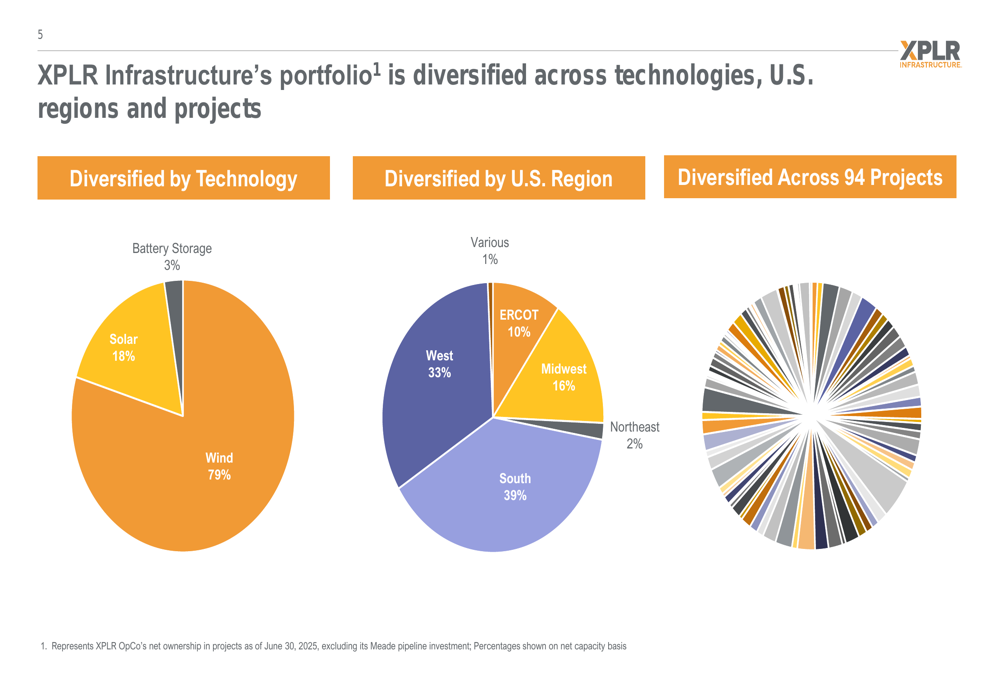

The company maintains a substantial portfolio of renewable energy assets, with wind representing 79% of capacity, solar 18%, and battery storage 3%. This diversification extends across U.S. regions, with the South (39%) and West (33%) comprising the largest portions of XPLR’s geographic footprint.

The following chart illustrates XPLR’s portfolio diversification across technologies, regions, and projects:

Quarterly Performance Highlights

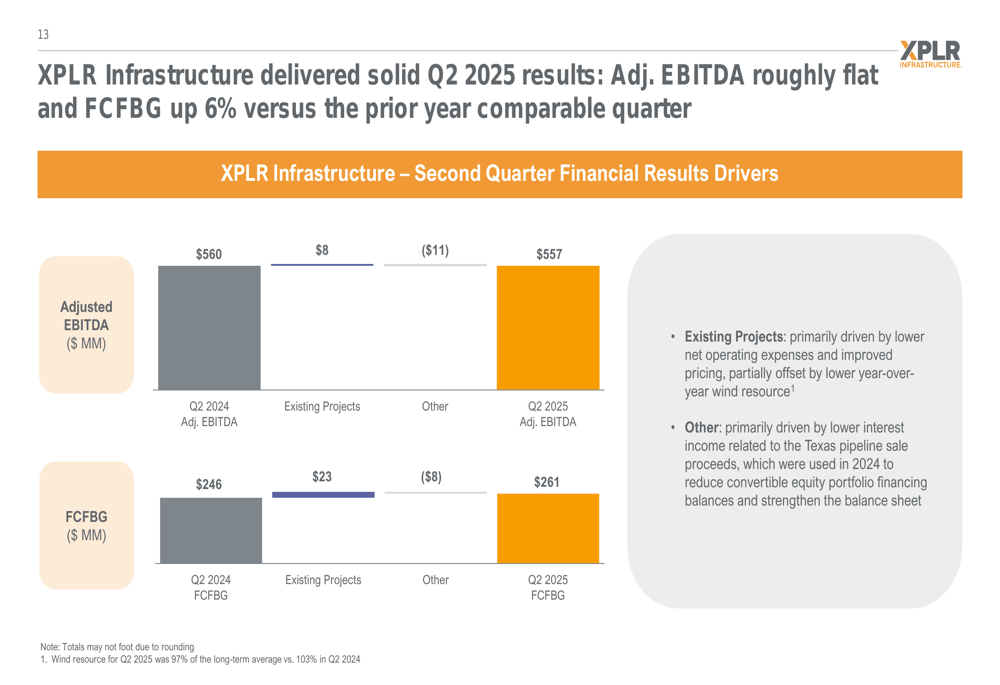

For Q2 2025, XPLR reported Adjusted EBITDA of $557 million, slightly below the $560 million recorded in Q2 2024. However, Free Cash Flow Before Growth (FCFBG) increased by 6% year-over-year to $261 million from $246 million. The company attributed the FCFBG improvement primarily to lower net operating expenses and improved pricing, partially offset by lower year-over-year wind resource.

The following waterfall charts detail the changes in Adjusted EBITDA and FCFBG from Q2 2024 to Q2 2025:

The "Other" category, which negatively impacted both metrics, was driven by lower interest income related to Texas pipeline sale proceeds used in 2024 to reduce convertible equity portfolio financing balances and strengthen the balance sheet.

Strategic Initiatives

XPLR continues to execute on its capital structure simplification strategy, which focuses on addressing legacy Convertible Equity Portfolio Financings (CEPFs). In April 2025, the company completed the buyout of CEPF 1 for approximately $931 million.

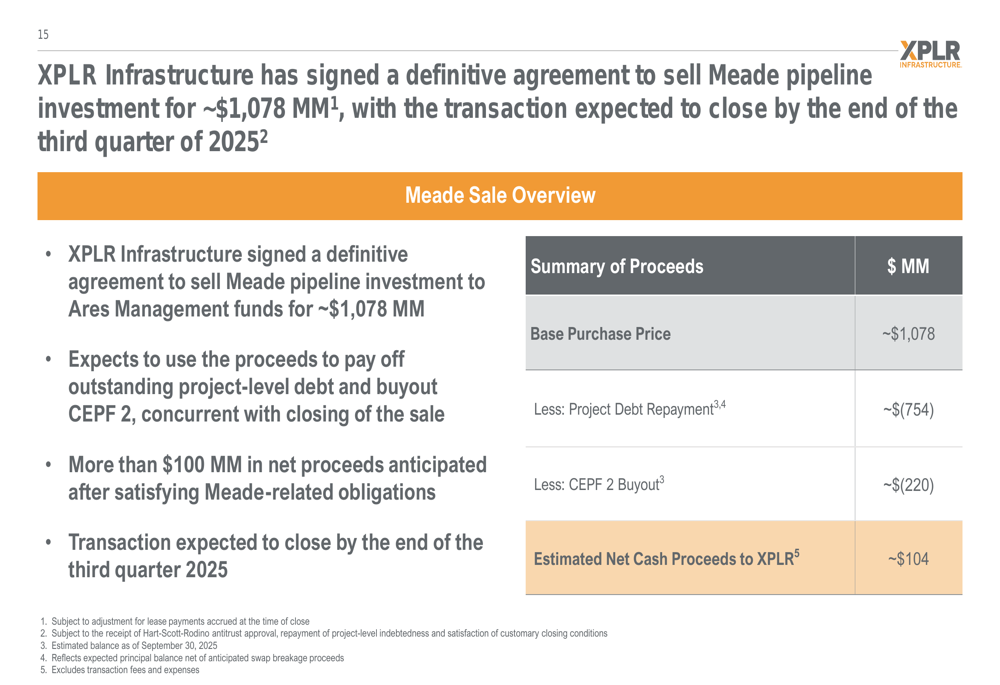

A significant development is the agreement to sell XPLR’s Meade pipeline investment to Ares Management (NYSE:ARES) funds for approximately $1.078 billion. The transaction, expected to close by the end of Q3 2025, will generate net proceeds of approximately $104 million after repaying project debt and buying out CEPF 2.

The following chart details the Meade sale transaction and use of proceeds:

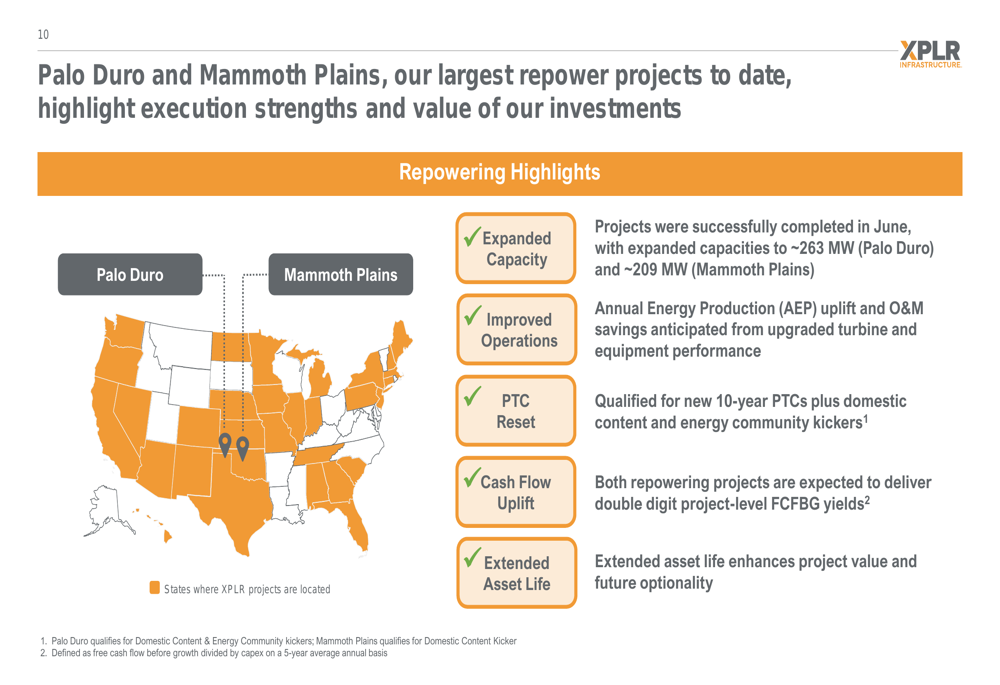

The company is also advancing its wind repowering initiatives, having completed approximately 740 MW of projects through Q2 2025, with a total of approximately 1.6 GW expected to reach commercial operation by 2026. Recent successful completions include the Palo Duro (~263 MW) and Mammoth Plains (~209 MW) projects, which were finished in June 2025.

As shown in this overview of the recently completed repowering projects:

Financial Outlook

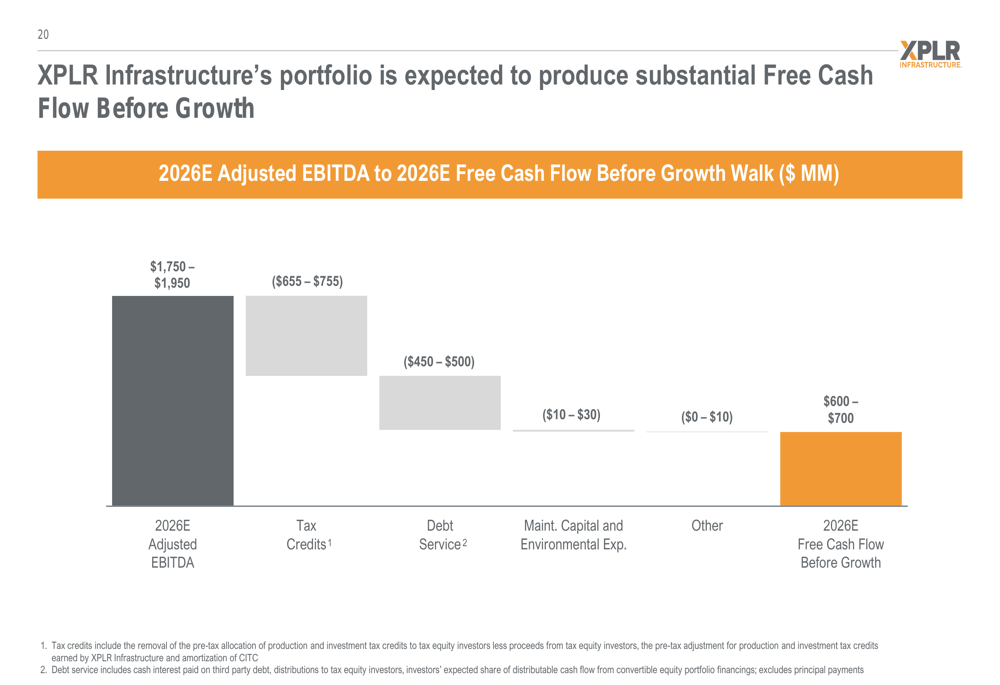

For calendar year 2025, XPLR expects Adjusted EBITDA of $1,850-$2,050 million. For 2026, the company projects Adjusted EBITDA of $1,750-$1,950 million and FCFBG of $600-$700 million. The decline in 2026 Adjusted EBITDA expectations is primarily attributed to the exclusion of contributions from the Meade pipeline investment following its sale.

The following chart illustrates the bridge from 2026 expected Adjusted EBITDA to Free Cash Flow Before Growth:

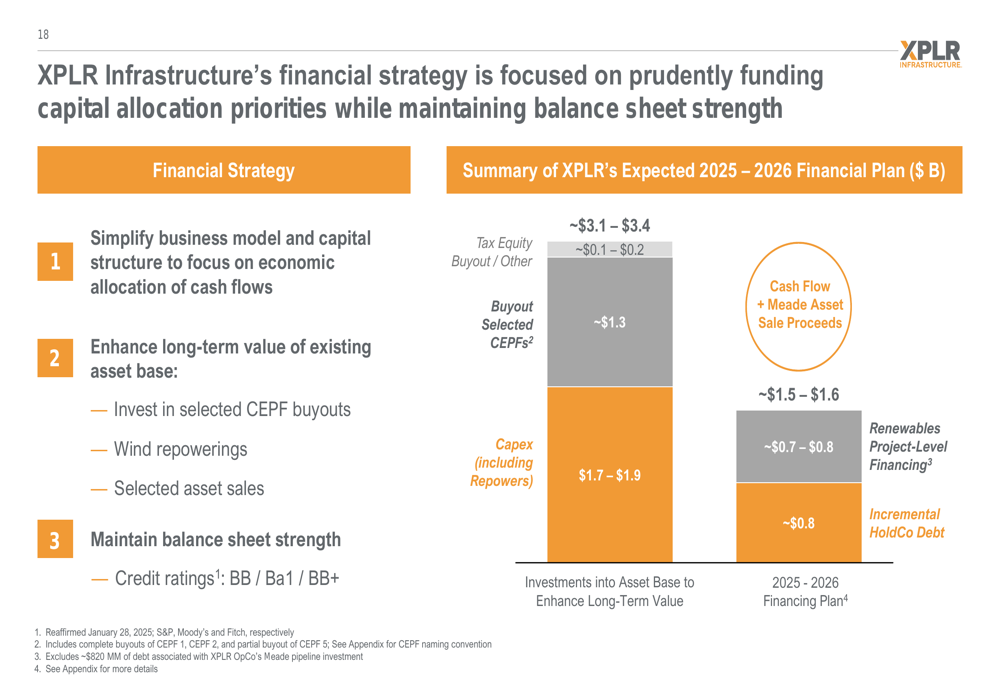

XPLR’s financial plan for 2025-2026 includes significant investments in asset repowering and capital structure simplification. The company has secured approximately $426 million in project financing, with approximately $338 million borrowed in June. Additionally, XPLR has secured commitments for an incremental approximately $600 million, bringing the total to approximately $1 billion.

The following chart outlines XPLR’s 2025-2026 financial plan:

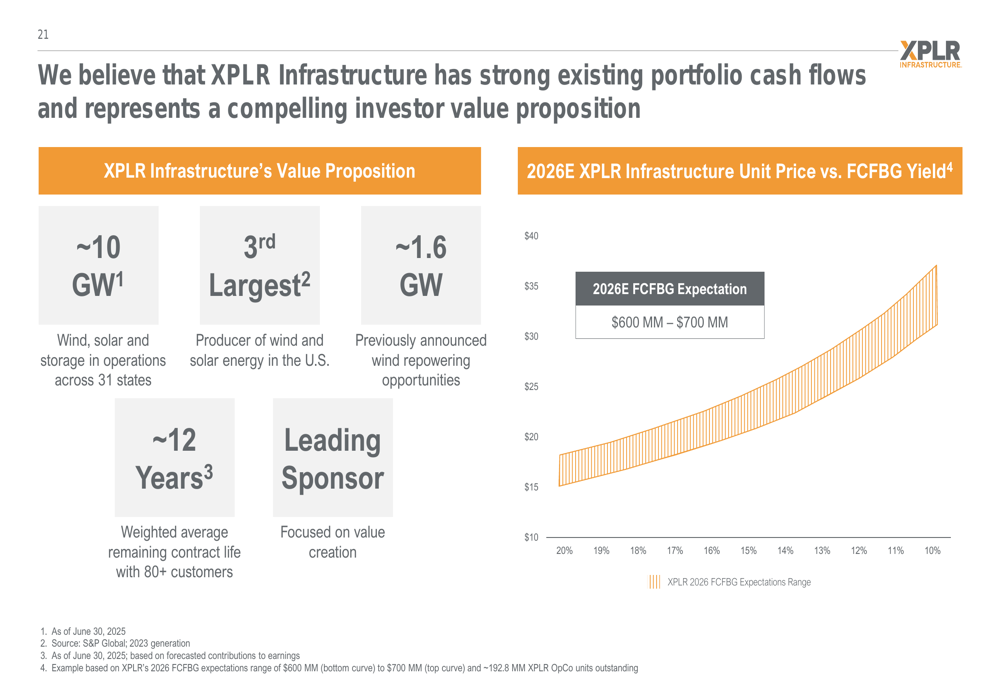

Long-Term Value Proposition

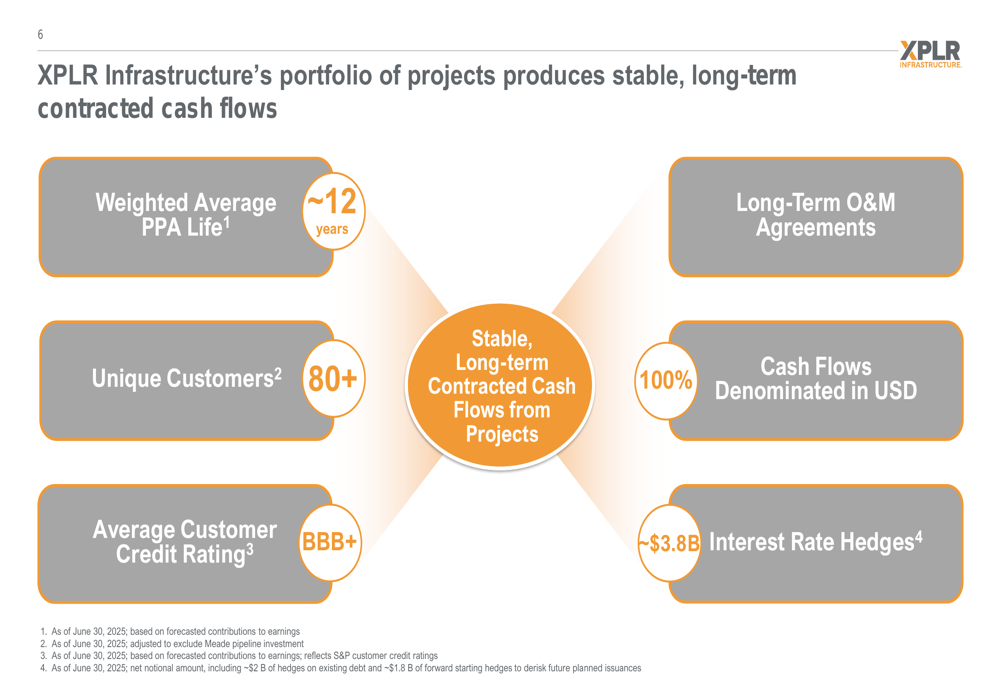

Despite near-term challenges, XPLR emphasizes its long-term value proposition based on its substantial renewable energy portfolio and contracted cash flows. The company highlights its weighted average PPA (Power Purchase Agreement) life of approximately 12 years with over 80 customers maintaining an average credit rating of BBB+.

As shown in the following overview of XPLR’s contracted cash flow profile:

The company’s relationship with NextEra Energy (NYSE:NEE), which owns approximately 98.8 million units in XPLR Infrastructure, provides operational benefits through long-term agreements for management services, asset-level O&M, and administrative services.

XPLR’s investor value proposition centers on its position as a major renewable energy producer with stable, contracted cash flows and growth opportunities through repowering and portfolio optimization:

While the presentation highlights XPLR’s strategic initiatives and long-term value drivers, investors should note the significant disconnect between the company’s messaging and its recent stock performance. Following a major earnings miss in Q4 2024 (reported EPS of -$1.08 versus expected $0.71), XPLR shares have remained under pressure, trading at less than a third of their 52-week high. The company’s efforts to simplify its capital structure and optimize its portfolio represent steps toward addressing these challenges, but significant work remains to restore investor confidence.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.