Bank CEOs meet with Trump to discuss Fannie Mae and Freddie Mac - Bloomberg

Introduction & Market Context

Xylem Inc. (NYSE:XYL) released its first quarter 2025 financial results on April 29, showcasing organic revenue growth and margin expansion despite facing macroeconomic uncertainties and tariff challenges. The water technology company’s shares were up 2.14% in premarket trading following the announcement, suggesting a positive market reception to the results.

The company’s performance comes amid a complex global trade environment with significant tariff impacts from China, Mexico, and the European Union, which Xylem is actively managing through pricing strategies and supply chain adjustments.

Quarterly Performance Highlights

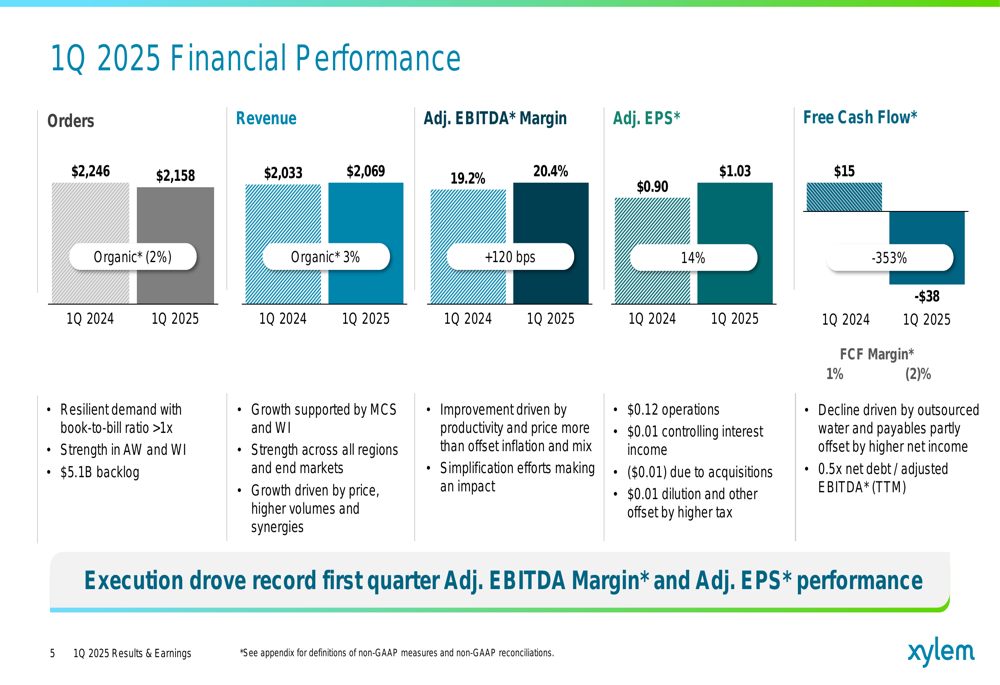

Xylem reported Q1 2025 revenue of $2.069 billion, representing a 3% organic growth compared to the same period last year. The company achieved an adjusted EBITDA margin of 20.4%, expanding 120 basis points year-over-year, while adjusted earnings per share grew 14% to $1.03 from $0.90 in Q1 2024.

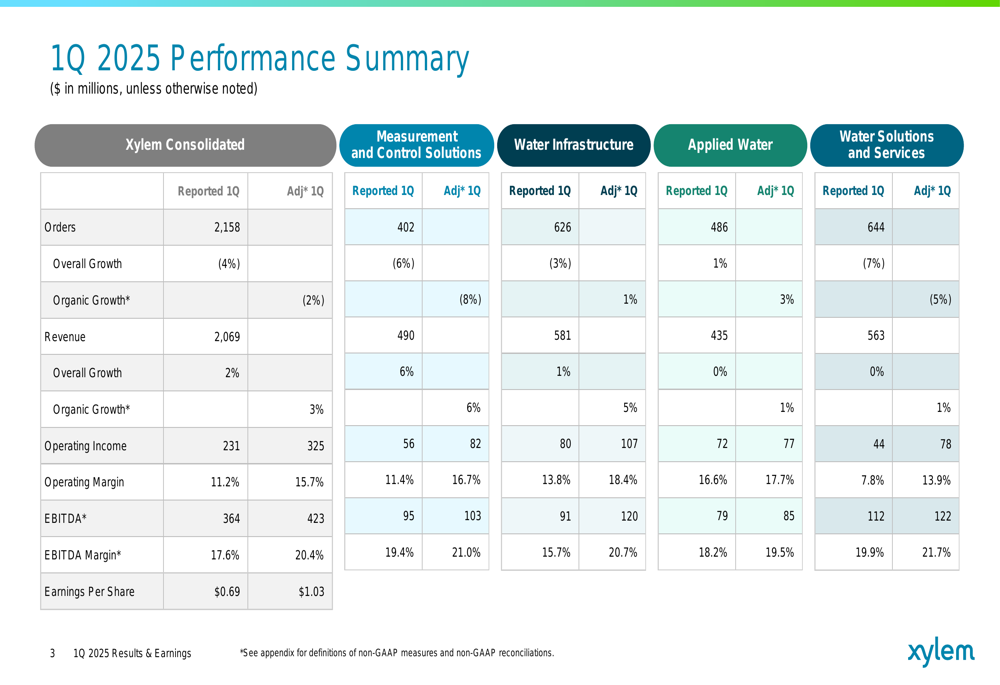

As shown in the following financial performance summary, the company maintained a strong book-to-bill ratio above 1, indicating healthy demand despite a 2% organic decline in orders to $2.158 billion:

"We had a strong start to 2025 with first quarter results exceeding expectations," the company noted in its presentation, highlighting resilient demand, revenue growth across all segments, and double-digit adjusted EPS growth.

However, free cash flow turned negative at -$38 million compared to $15 million in the prior year, a 353% decline primarily driven by outsourced water projects and payables timing. The company maintains a strong balance sheet with a net debt to adjusted EBITDA ratio of 0.5x on a trailing twelve-month basis.

Segment Performance Analysis

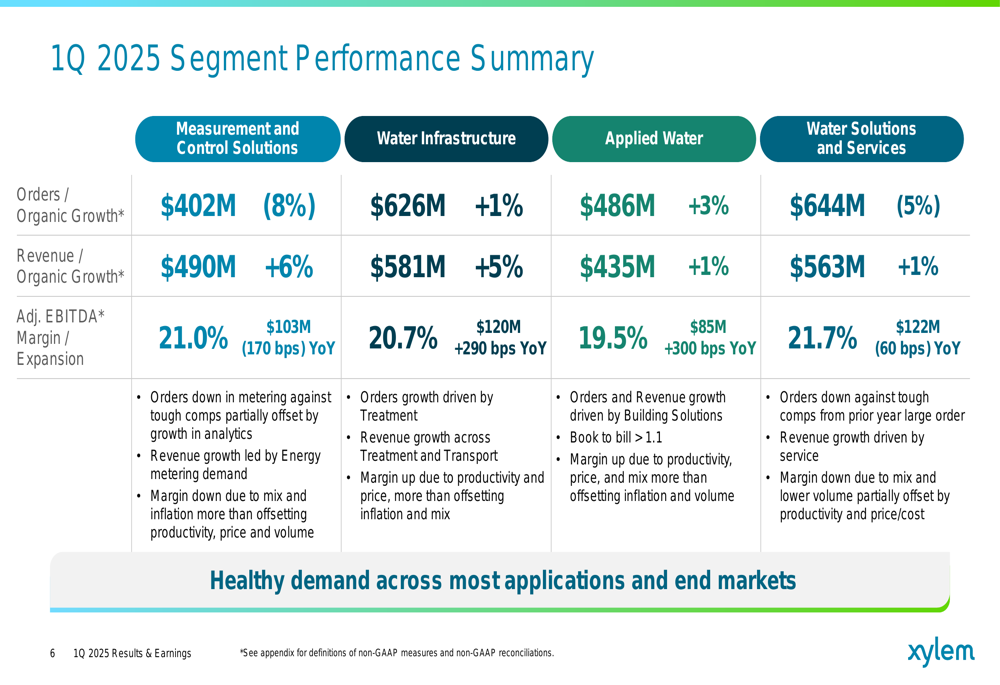

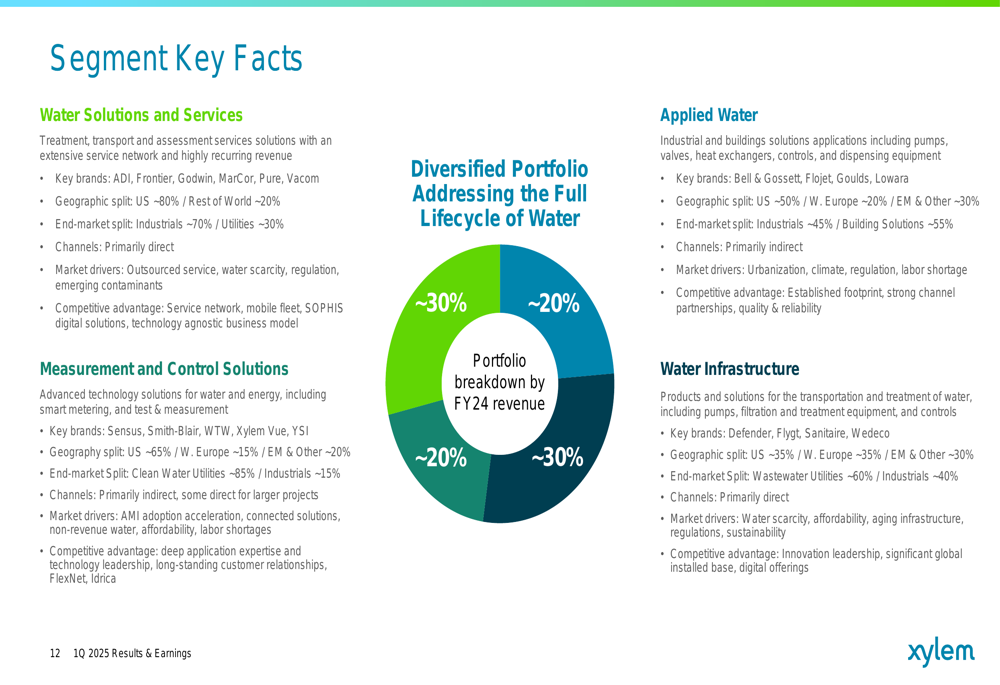

Xylem’s performance varied across its business segments, with Water Infrastructure and Applied Water showing particular strength, while Measurement and Control Solutions (MCS) and Water Solutions and Services (WSS) faced some challenges.

The detailed segment breakdown reveals these performance differences:

Water Infrastructure delivered 5% organic revenue growth and an impressive 290 basis point expansion in adjusted EBITDA margin to 20.7%. Similarly, Applied Water achieved 1% organic revenue growth with a 300 basis point margin improvement to 19.5%.

Meanwhile, Measurement and Control Solutions saw 6% organic revenue growth but experienced a 170 basis point contraction in adjusted EBITDA margin to 21.0%. Water Solutions and Services delivered modest 1% organic revenue growth with a 60 basis point decline in margin to 21.7%.

The company’s overall performance benefited from its diversified portfolio across different water applications, as illustrated in this segment overview:

Tariff Impact Management

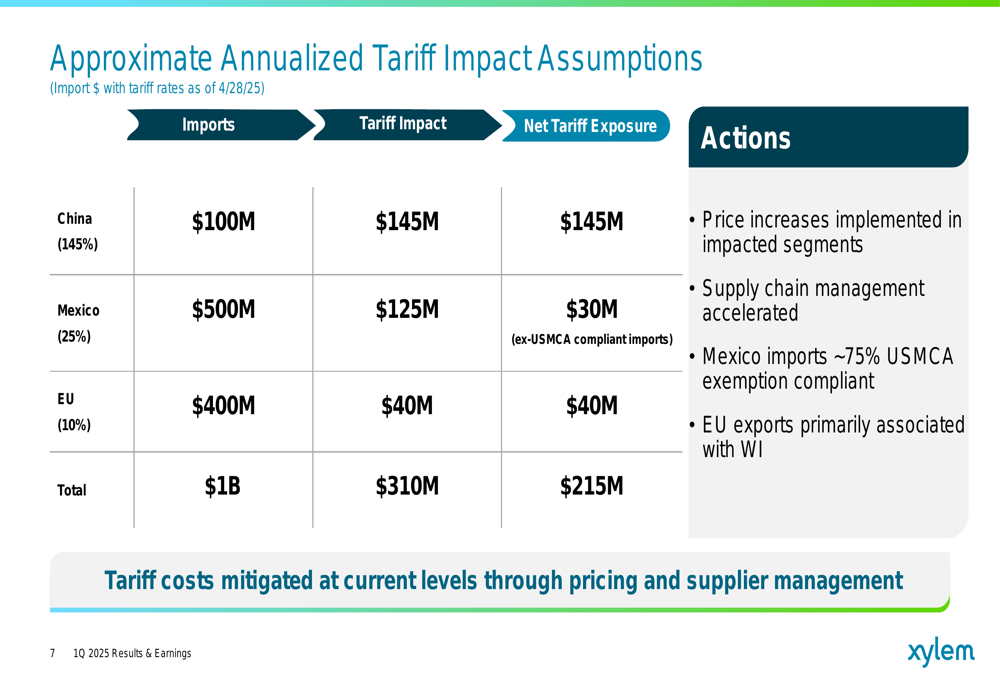

A significant challenge facing Xylem is the impact of global tariffs, which the company addressed in detail during its presentation. The company faces approximately $215 million in net tariff exposure annually, with the largest impacts coming from China (145% tariff rate) and Mexico (25% tariff rate).

The following chart illustrates the tariff impact assumptions and mitigation strategies:

Xylem is implementing several measures to offset these tariff impacts, including price increases in affected segments, accelerated supply chain management, and leveraging USMCA exemptions for approximately 75% of its Mexico imports. The company stated that "tariff costs are mitigated at current levels through pricing and supplier management."

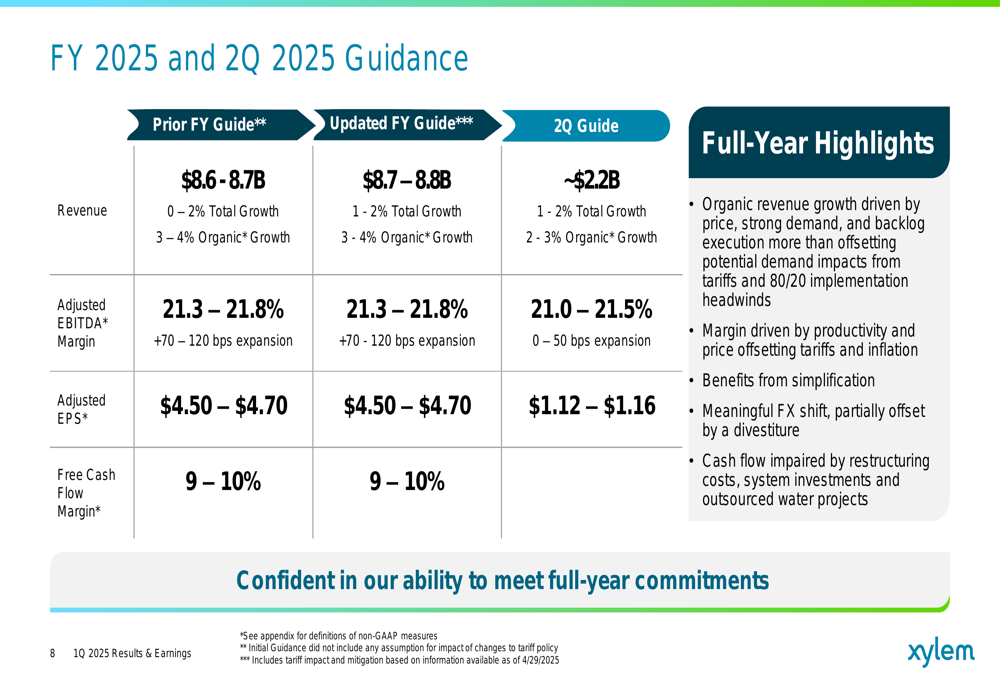

Forward Guidance and Outlook

Despite the challenging environment, Xylem has maintained its full-year 2025 adjusted EPS guidance of $4.50-$4.70 while slightly raising its revenue outlook from $8.6-8.7 billion to $8.7-8.8 billion, representing 1-2% total growth and 3-4% organic growth.

For the second quarter of 2025, the company expects revenue of approximately $2.2 billion with 2-3% organic growth and adjusted EBITDA margin of 21.0-21.5%, representing 0-50 basis points of expansion.

The detailed guidance is presented in the following chart:

"We are confident in meeting our full-year commitments," the company stated, highlighting that organic revenue growth will be driven by pricing, strong demand, and backlog execution, which will more than offset potential impacts from tariffs and implementation headwinds from the company’s "80/20" business optimization initiative.

Margin improvement is expected to come from productivity gains and pricing actions offsetting tariffs and inflation, with additional benefits from the company’s ongoing simplification efforts.

Strategic Initiatives

Xylem emphasized several strategic priorities that are driving its performance and future outlook. The company is focusing on simplifying its business operations, optimizing its portfolio, maintaining sustainability leadership, and creating shareholder value.

The company will release its 2024 Sustainability Report on April 30, highlighting progress toward its 2025 sustainability goals. This focus on environmental leadership aligns with growing market demand for sustainable water solutions.

The comprehensive Q1 2025 performance summary across all segments illustrates the company’s overall solid execution:

In its key takeaways, Xylem emphasized that its momentum is being driven by business simplification initiatives, with capital deployment and portfolio optimization underway. The company remains focused on maintaining its sustainability leadership position while driving profitable growth and shareholder value creation.

With a strong balance sheet, diversified global presence, and continued focus on operational efficiency, Xylem appears well-positioned to navigate the current macroeconomic challenges while delivering on its full-year commitments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.