Uxin shares drop 45% as predicted by InvestingPro’s Fair Value model

Introduction & Market Context

YDUQS Participacoes SA (BVMF:YDUQ3) released its third-quarter 2025 results on November 13, highlighting strong performance across its diversified education portfolio despite regulatory changes in Brazil's education sector. The company's stock closed at R$34.05, down 1.76% following the announcement, despite reporting improved financial metrics and operational growth.

The education provider demonstrated resilience through its multi-segment strategy, with particular strength in premium offerings and semi on-campus programs. YDUQS has successfully navigated the post-pandemic education landscape by balancing traditional campus-based education with digital and hybrid learning models.

Quarterly Performance Highlights

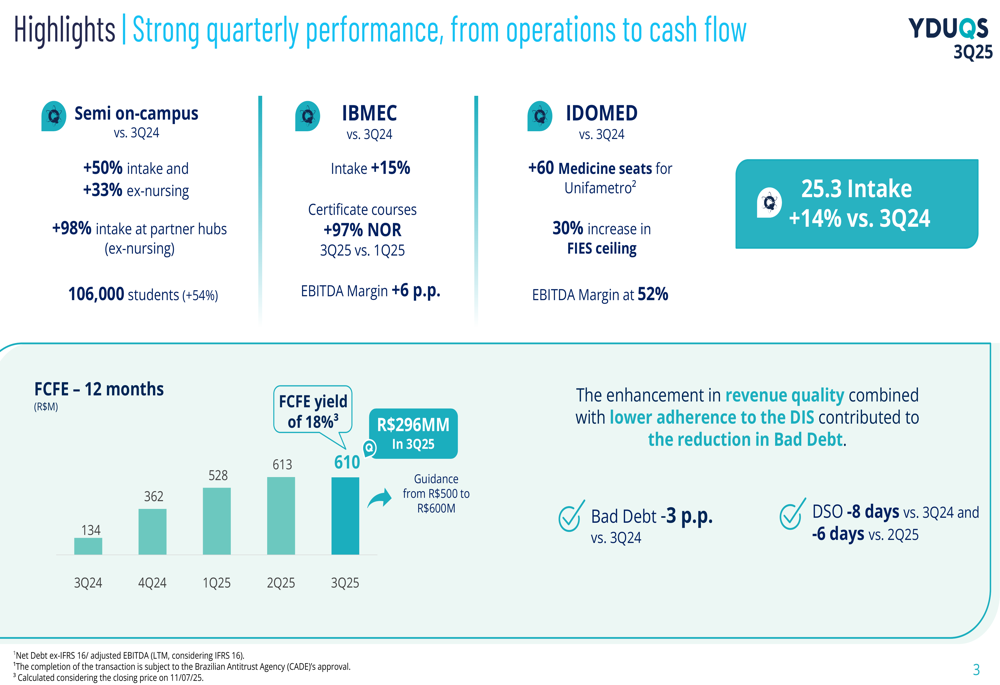

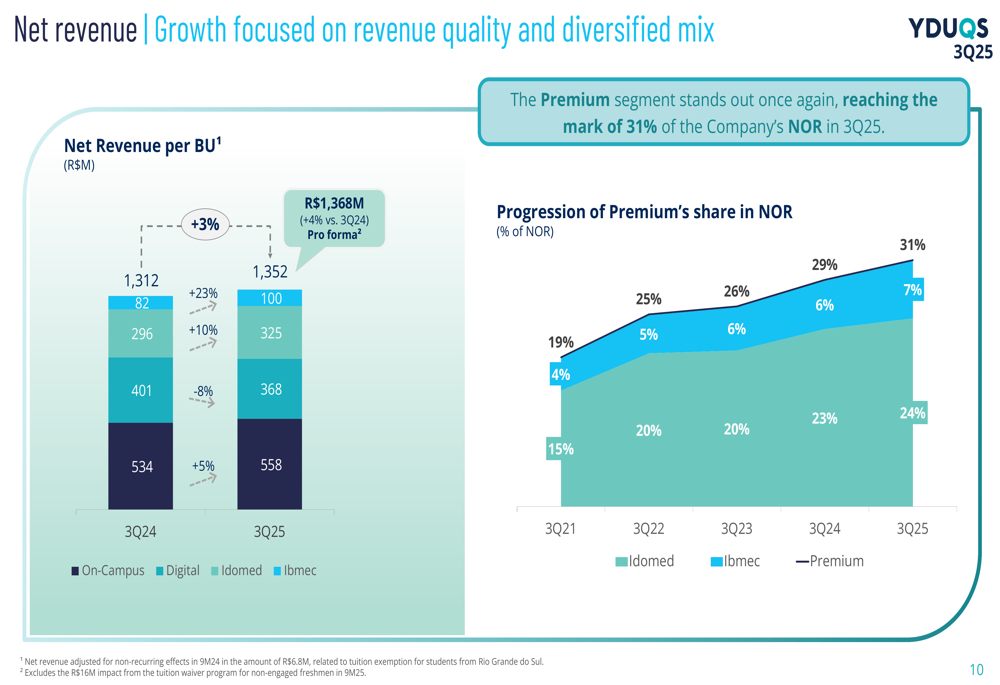

YDUQS reported a 4% year-over-year increase in net revenue to R$1,368 million in Q3 2025, driven primarily by growth in its premium segments and semi on-campus programs. The company's adjusted EBITDA improved by 6% compared to Q3 2024, with margins expanding by 1 percentage point.

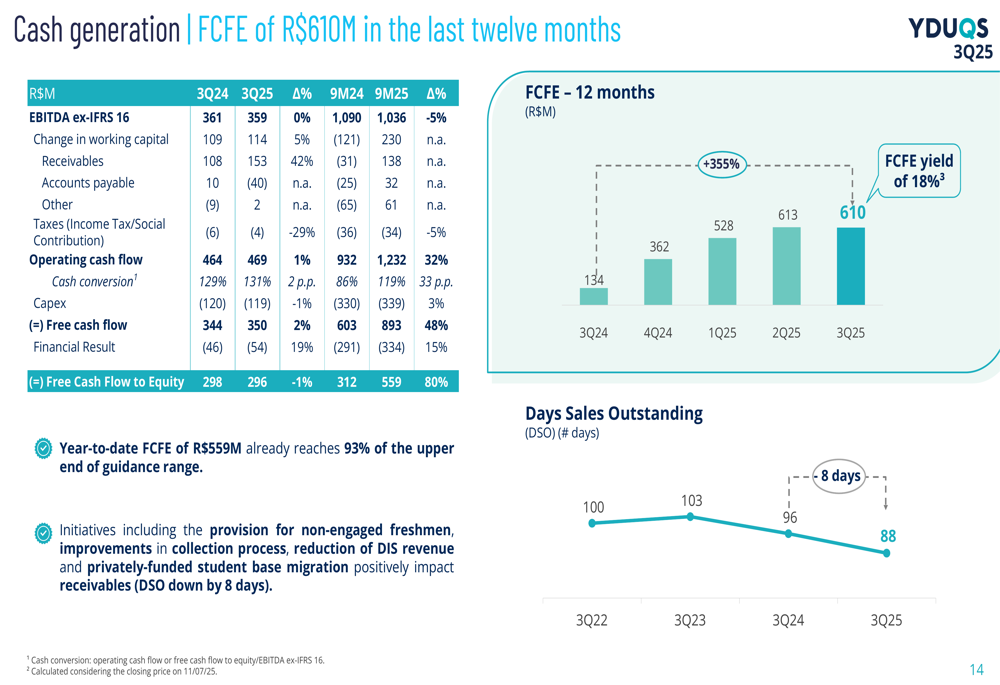

The standout metric was free cash flow to equity (FCFE), which reached R$610 million for the trailing twelve months, representing an impressive FCFE yield of 18%. This cash generation strength exceeded the company's guidance range of R$500-600 million.

As shown in the following chart of key performance highlights, the company saw significant growth across multiple segments:

Student intake increased by 14% compared to Q3 2024, with particularly strong performance in the semi on-campus segment, which grew by 50%. The company also reported a substantial reduction in bad debt, down 3 percentage points year-over-year, and an 8-day improvement in days sales outstanding (DSO) compared to the same period last year.

Segment Performance Analysis

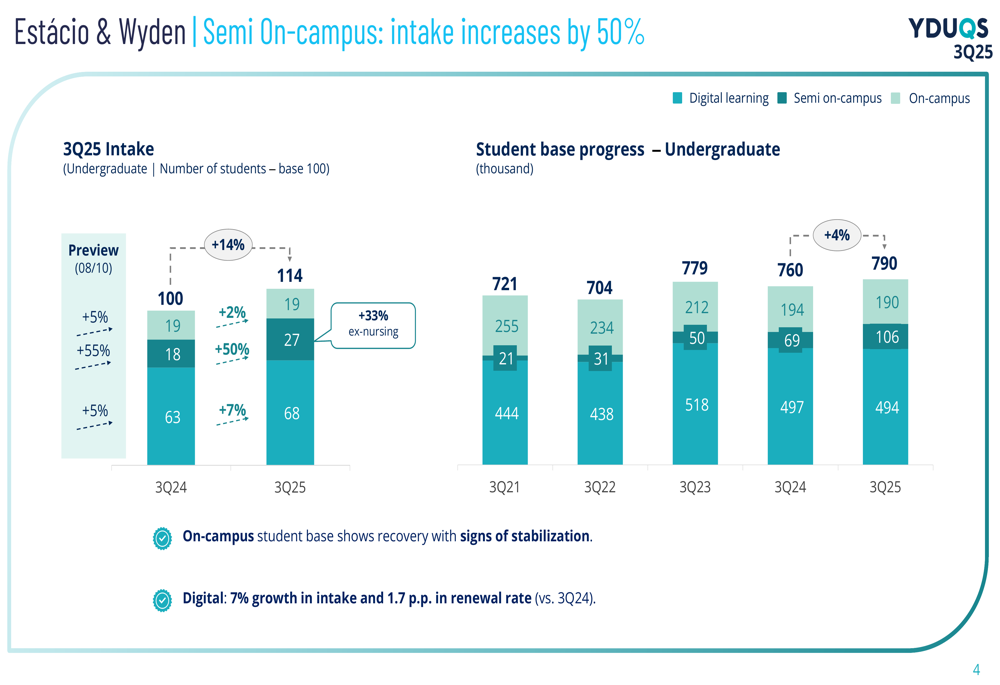

The semi on-campus segment emerged as a key growth driver, with intake increasing by 50% and the student base growing to 106,000 students, a 54% increase year-over-year. This segment's performance is particularly notable given the regulatory changes affecting Brazil's education sector.

The following chart illustrates the growth in the semi on-campus segment:

YDUQS's premium segments continued to demonstrate strong performance. Ibmec, the company's premium business education brand, reported a 23% increase in net revenue for the first nine months of 2025, with a 40% jump in adjusted EBITDA. The segment's EBITDA margin improved by 6 percentage points in the quarter.

Similarly, Idomed, the company's medical education segment, maintained strong growth momentum with an 11% increase in net revenue and a 10% rise in adjusted EBITDA for the first nine months of 2025. Idomed achieved an impressive 52% EBITDA margin, benefiting from 60 additional medicine seats for Unifametro and a 30% increase in the FIES ceiling.

The company's revenue mix continues to shift toward premium offerings, as shown in the following chart:

The premium segment now accounts for 31% of YDUQS's net revenue in Q3 2025, up from 19% in Q3 2021. This strategic shift has positively impacted the company's profitability profile, with premium segments now representing 43% of total EBITDA, a 17 percentage point increase since Q3 2021.

Financial Health and Cash Generation

YDUQS demonstrated significant improvement in its financial health during Q3 2025. The company's cash generation remained robust, with free cash flow to equity reaching R$610 million for the trailing twelve months, as illustrated in the following chart:

The company continued its deleveraging trend, with the net debt to EBITDA ratio improving to 1.52x in Q3 2025, down from 1.7x in Q3 2024. This reduction in leverage, combined with strong cash generation, has enhanced YDUQS's financial flexibility.

Bad debt management was another highlight, with a 3.2 percentage point reduction compared to Q3 2024. Days sales outstanding improved by 8 days year-over-year and 6 days sequentially, reflecting enhanced collection efficiency and revenue quality.

Despite higher interest rates in Brazil, YDUQS maintained stable earnings per share at R$1.5 for the trailing twelve months, with pro forma EPS reaching R$1.9.

Strategic Initiatives and Outlook

YDUQS is actively adapting to the new regulatory framework in Brazil's education sector, which presents both challenges and opportunities. The company is leveraging its diversified portfolio and premium positioning to navigate these changes effectively.

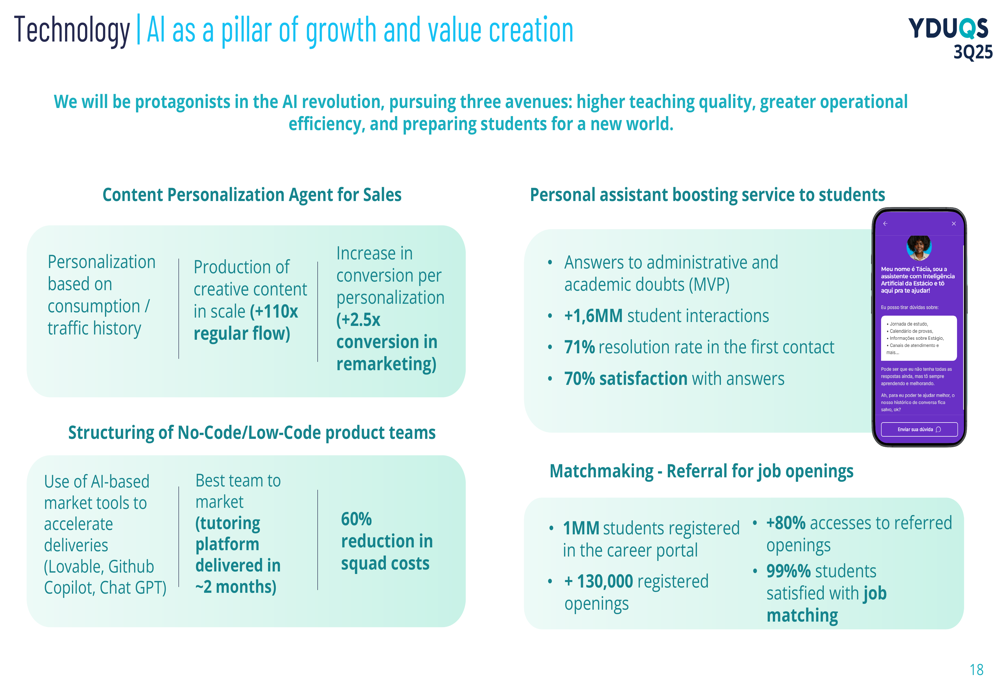

Artificial intelligence has emerged as a key growth pillar for YDUQS, with initiatives focused on content personalization, no-code/low-code product teams, and job matching services for students. These innovations are expected to enhance the student experience and drive operational efficiencies.

The company also emphasized its commitment to ESG principles, highlighting its leadership in sustainability, climate strategy, and talent attraction initiatives. YDUQS has received recognition from various ESG rating agencies, reinforcing its position as a responsible corporate citizen.

Looking ahead, YDUQS appears well-positioned to deliver on its EPS guidance, focusing on intake and retention, bad debt reduction, contingency management, and G&A optimization. The company's strategic emphasis on premium segments and cash generation is expected to continue driving performance in the coming quarters.

During the earnings call, CEO Rossano Marques emphasized the company's focus on cash generation, stating, "Cash generation is our great focus, enabling us to reach our goals." He also highlighted the role of technology in their strategy: "Technology is a very strong base of everything that we did."

As YDUQS navigates the evolving education landscape in Brazil, its diversified portfolio, premium positioning, and financial strength provide a solid foundation for sustainable growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.