Asia tech stocks slide tracking Wall St losses amid AI doubts, govt. uncertainty

Introduction & Market Context

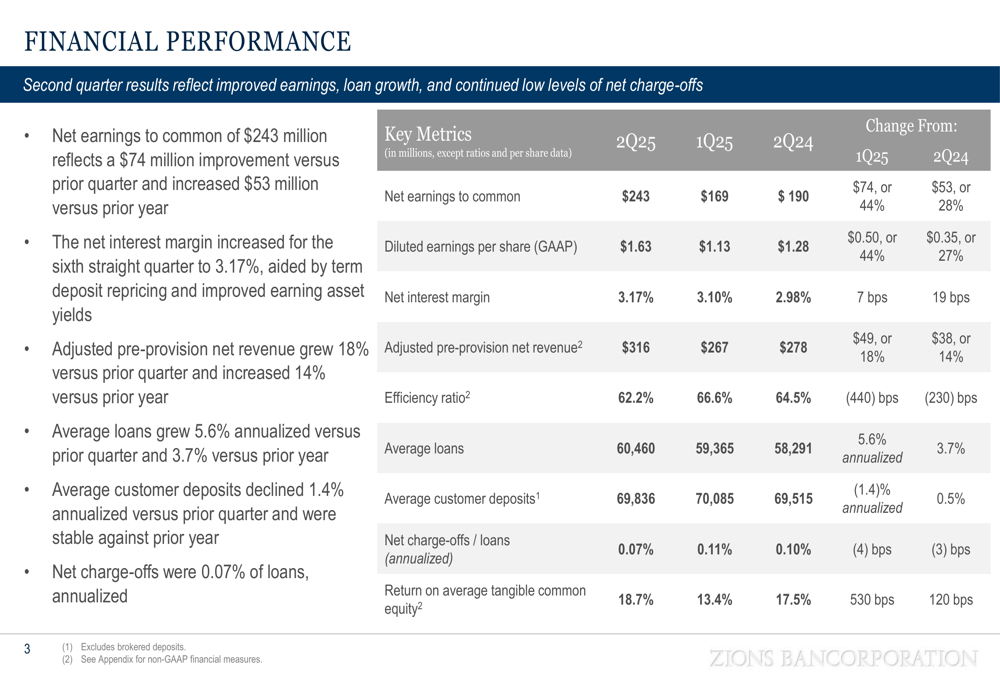

Zions Bancorporation (NASDAQ:ZION) presented its second quarter 2025 financial results on July 21, 2025, revealing substantial earnings growth and improved operational efficiency. The bank reported net earnings to common shareholders of $243 million, representing a 44% increase from the previous quarter and a 28% rise year-over-year. Following the announcement, Zions’ stock saw a modest 0.35% increase in after-hours trading, reaching $57.

The results significantly exceeded market expectations, with earnings per share of $1.63 surpassing the forecasted $1.31 by 24.43%. Revenue also outperformed projections, totaling $838 million against an anticipated $811.06 million. As of the latest trading data, the stock stands at $55.18, within its 52-week range of $39.32 to $63.22.

Quarterly Performance Highlights

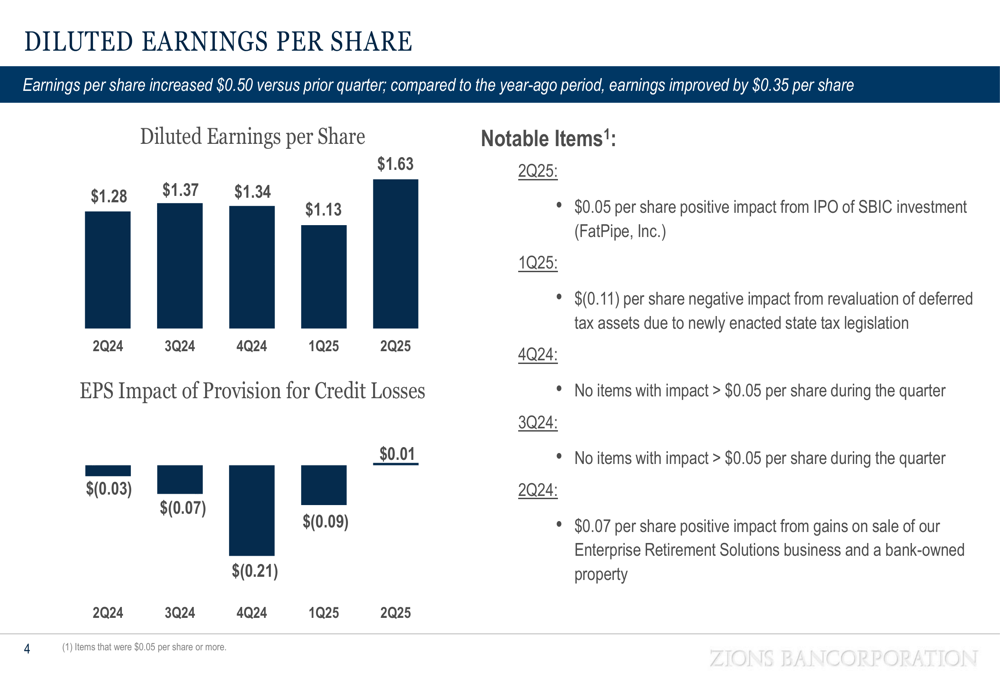

Zions delivered strong financial performance across key metrics in Q2 2025. Net earnings to common shareholders reached $243 million, translating to diluted earnings per share of $1.63, a substantial improvement from $1.13 in the previous quarter and $1.28 in the same period last year.

As shown in the following comprehensive performance summary, the bank demonstrated growth in several critical areas:

The bank’s net interest margin expanded to 3.17%, continuing a six-quarter trend of improvement. This expansion contributed to a 4% increase in net interest income compared to the previous quarter and a 9% rise year-over-year. Adjusted pre-provision net revenue grew by 18% quarter-over-quarter and 14% year-over-year, reflecting the bank’s operational efficiency.

The following chart illustrates the consistent improvement in diluted earnings per share over recent quarters, including the impact of notable items:

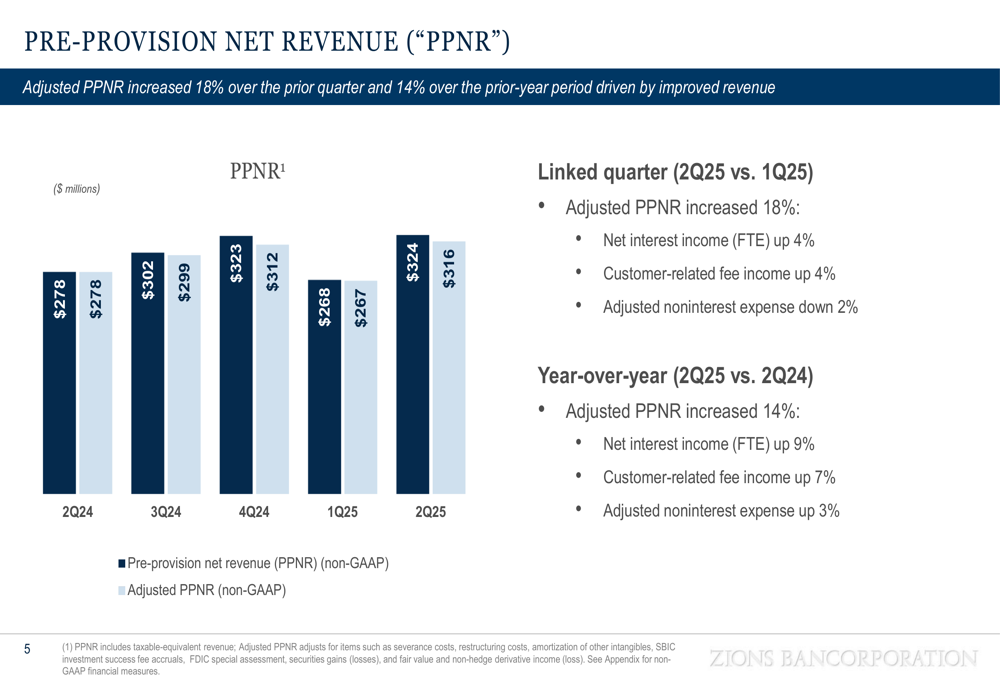

Pre-provision net revenue (PPNR), a key indicator of a bank’s core profitability before accounting for potential loan losses, showed significant improvement. The 18% increase over the prior quarter was driven by higher net interest income, increased customer-related fee income, and reduced noninterest expenses.

The following chart details the components contributing to PPNR growth:

Net Interest Income and Margin

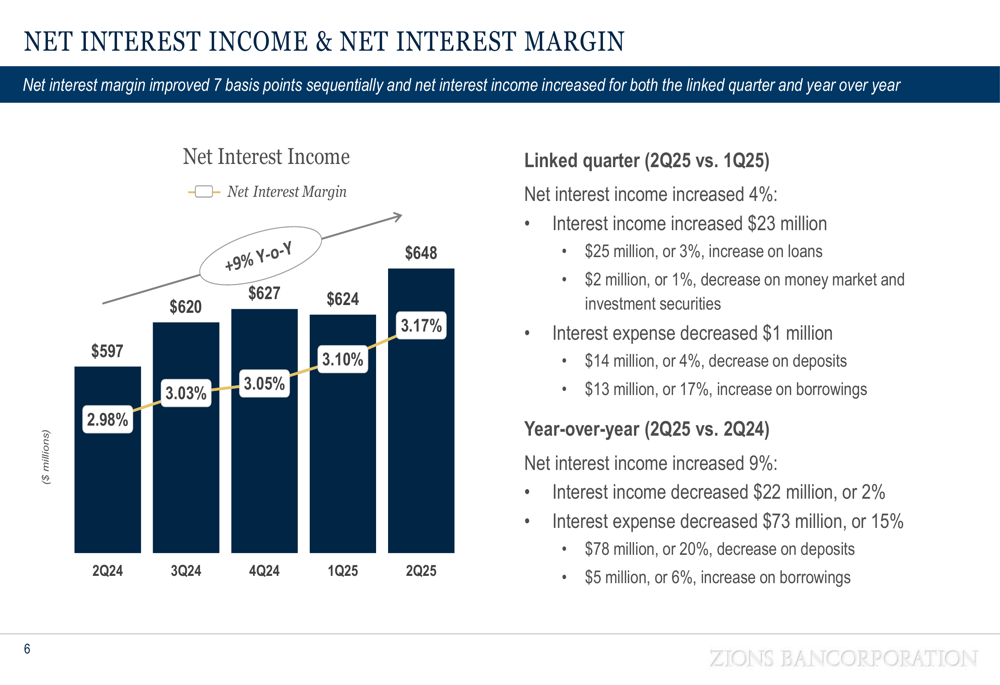

Zions’ net interest income increased by 4% quarter-over-quarter to $648 million, driven primarily by a 3% increase in loan interest income. The net interest margin expanded to 3.17%, reflecting the bank’s effective balance sheet management and asset repricing.

The following chart illustrates the trend in net interest income and margin:

The improvement in net interest margin was supported by higher yields on loans and reduced deposit costs. Interest expense on deposits decreased by 4% quarter-over-quarter, while interest income on loans increased by 3%. This favorable shift in the bank’s interest-earning assets and interest-bearing liabilities contributed to the overall margin expansion.

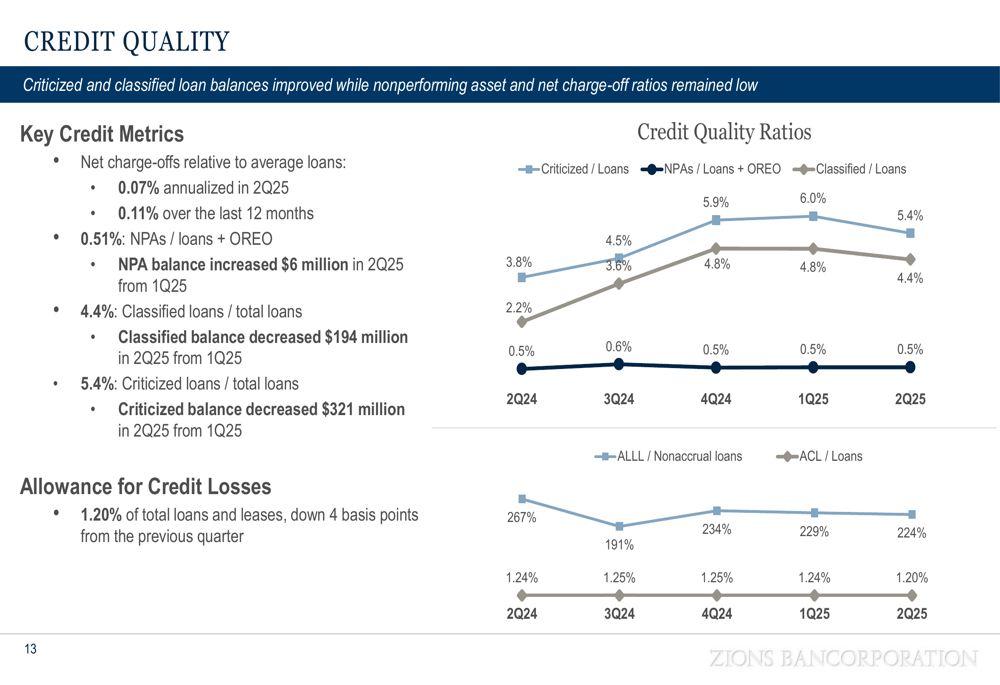

Credit Quality and Loan Portfolio

Zions maintained strong credit quality metrics during the quarter, with net charge-offs at just 0.07% of loans on an annualized basis. Criticized and classified loan balances improved, while nonperforming asset ratios remained low.

The following chart illustrates the bank’s credit quality trends:

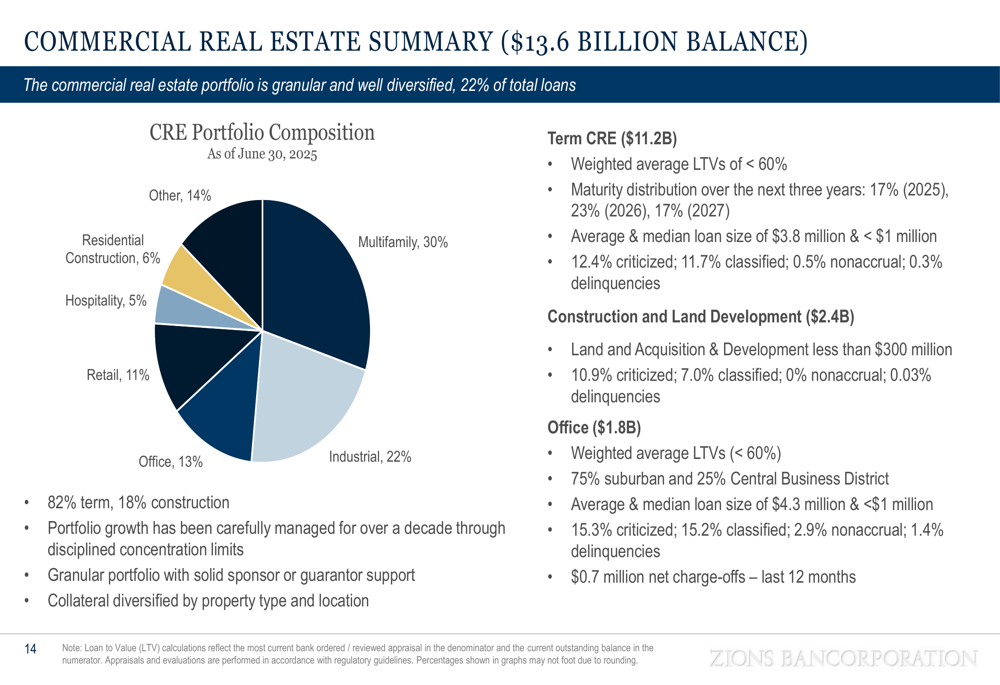

The commercial real estate (CRE) portfolio, which represents 22% of total loans with a balance of $13.6 billion, showed signs of improvement. CRE classifieds decreased by $196 million during the quarter, with reductions primarily in office, industrial, and multifamily properties.

The CRE portfolio remains well-diversified across property types, with multifamily (30%) and industrial (22%) comprising the largest segments, followed by office (13%) and retail (11%):

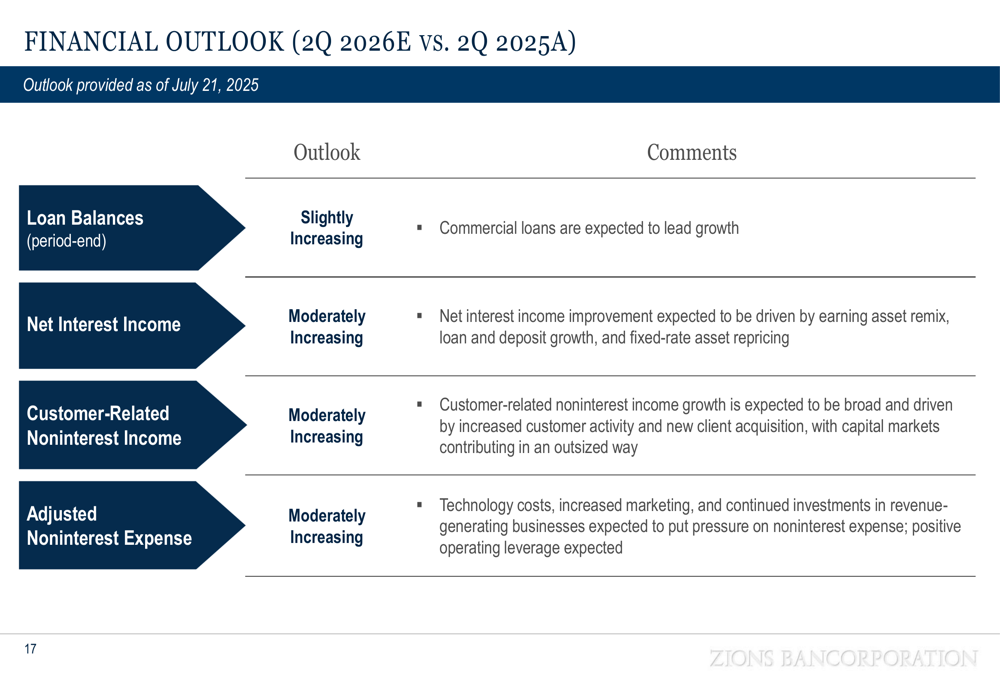

Capital Position and Outlook

Zions maintains a strong capital position relative to its risk profile, with substantial loss-absorbing capacity. The bank’s Common Equity Tier 1 capital and allowance for credit losses provide significant protection against potential credit losses.

Looking ahead to 2026, Zions provided a positive outlook across several key areas. The bank expects moderate increases in net interest income, customer-related noninterest income, and adjusted noninterest expenses, with loan balances projected to increase slightly:

CEO Harris Simmons expressed optimism about the company’s talent acquisition strategy, noting, "We’re finding some really good people who through disruption in other places are looking for a good home." Meanwhile, President and COO Scott McClain emphasized the bank’s focus on efficiency, stating, "We have every year about 2% of our base of expenses that we’re eliminating through just continuous improvement."

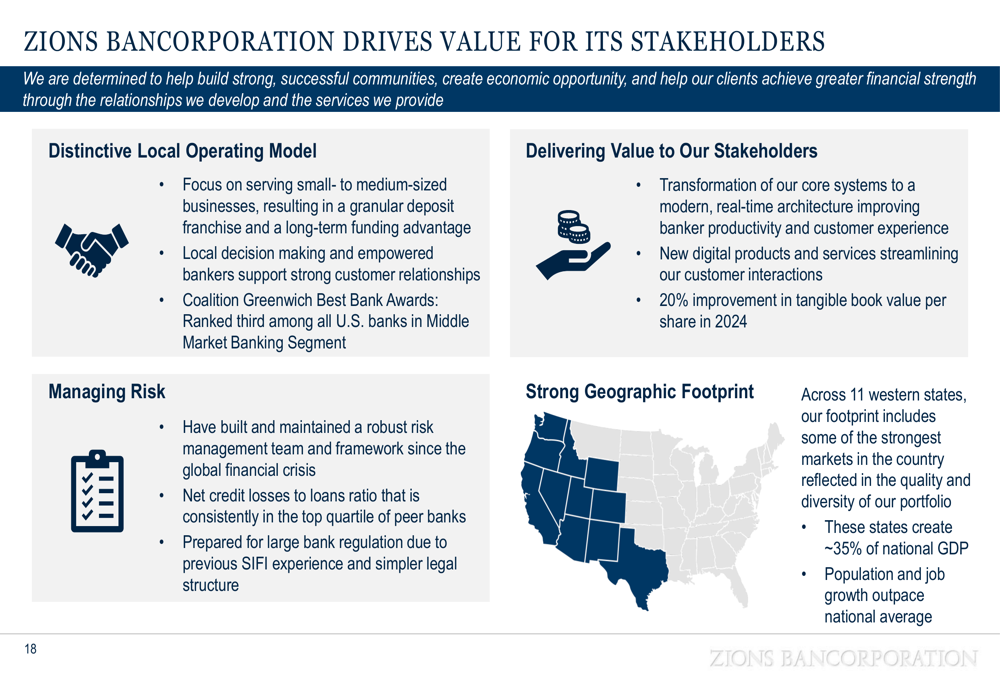

Strategic Positioning

Zions continues to differentiate itself through its distinctive local operating model, focusing on small to medium-sized businesses across its 11-state western U.S. footprint. The bank emphasizes local decision-making and empowered bankers to support strong customer relationships.

The following slide outlines the bank’s approach to creating stakeholder value:

The bank highlighted its transformation of core systems and streamlined customer interactions, which contributed to a 20% improvement in tangible book value per share in 2024. Zions also emphasized its robust risk management framework, which has helped maintain net credit losses consistently in the top quartile of peer banks.

While the bank faces challenges including economic uncertainty from potential tariff impacts, competitive pressures on margins, and regulatory changes, its strong Q2 performance demonstrates resilience and effective management of these risks. With a beta of 0.88, the stock has shown lower volatility compared to the broader market, potentially offering stability in an uncertain economic environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.