Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

Zoetis Inc . (NYSE:ZTS), the global animal health leader, presented its first quarter 2025 financial results on May 6, 2025, reporting strong performance across its portfolio and geographic segments. The company demonstrated resilience and growth momentum, leading management to raise its full-year guidance despite some macroeconomic challenges.

The animal health company’s stock traded up 3.25% in pre-market trading at $163.19, reflecting positive investor sentiment following the results announcement. This comes after a period of volatility for the stock, which has traded between $139.70 and $200.33 over the past 52 weeks.

Quarterly Performance Highlights

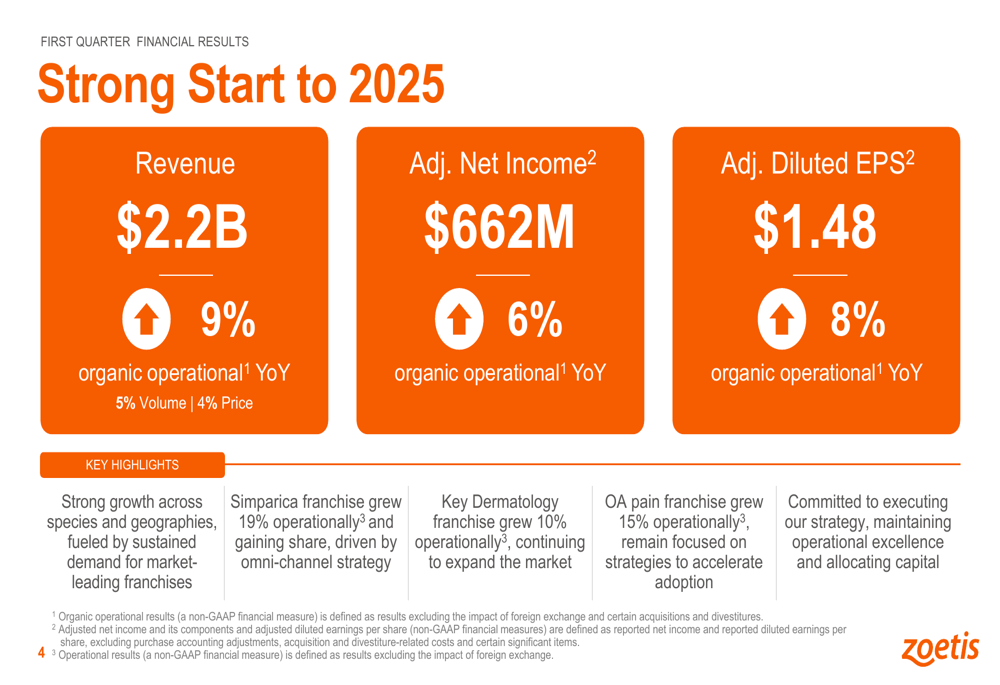

Zoetis reported solid financial results for Q1 2025, with revenue reaching $2.2 billion, representing 9% organic growth year-over-year. This growth was driven by a combination of 5% volume increase and 4% price improvement. The company’s adjusted net income reached $662 million, up 6% organically, while adjusted diluted earnings per share grew to $1.48, an 8% organic increase year-over-year.

As shown in the following summary of Q1 2025 performance:

The company’s performance was driven by strong growth across both companion animal and livestock segments, with particularly robust results in the international markets. U.S. segment revenue reached $1.2 billion, reflecting 6% organic operational growth, while international segment revenue totaled $1.0 billion, representing an impressive 11% organic operational growth.

In the U.S. market, companion animal revenue grew 8% to $1.0 billion, while livestock revenue declined 2% organically to $0.2 billion. Internationally, companion animal revenue increased 10% operationally to $0.6 billion, and livestock revenue grew 12% organically to $0.4 billion.

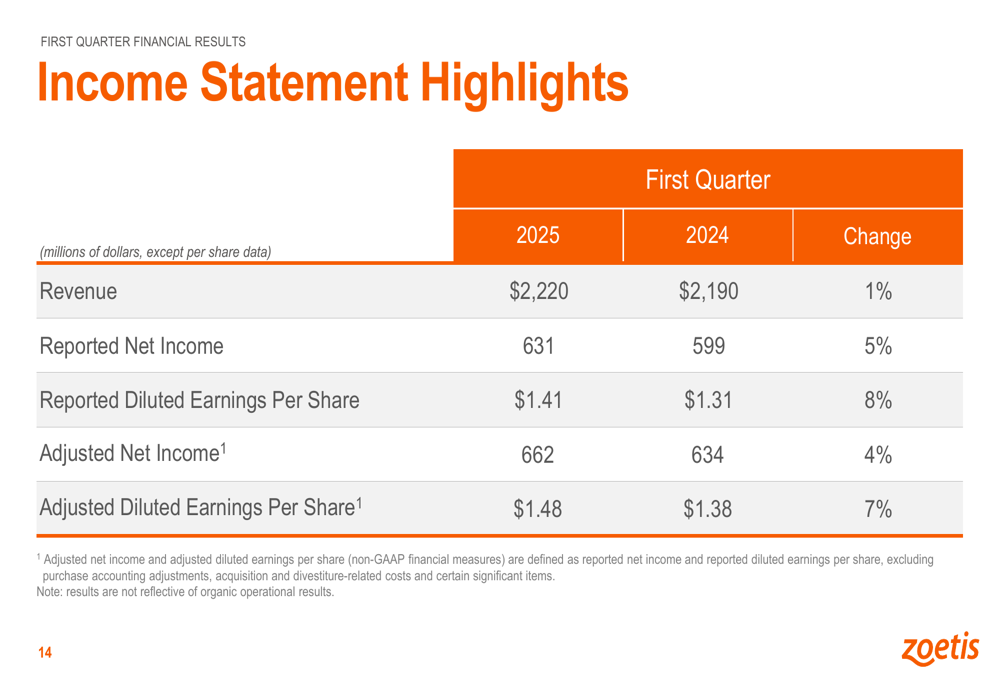

The company’s income statement highlights demonstrate consistent growth in both reported and adjusted metrics:

Gross margins improved in both segments, with the U.S. segment reaching 83.2% (up from 81.3% in the prior year) and the international segment achieving 70.0% (up from 68.9%). These margin improvements reflect the company’s focus on higher-margin products and operational efficiencies.

Key Product Franchise Performance

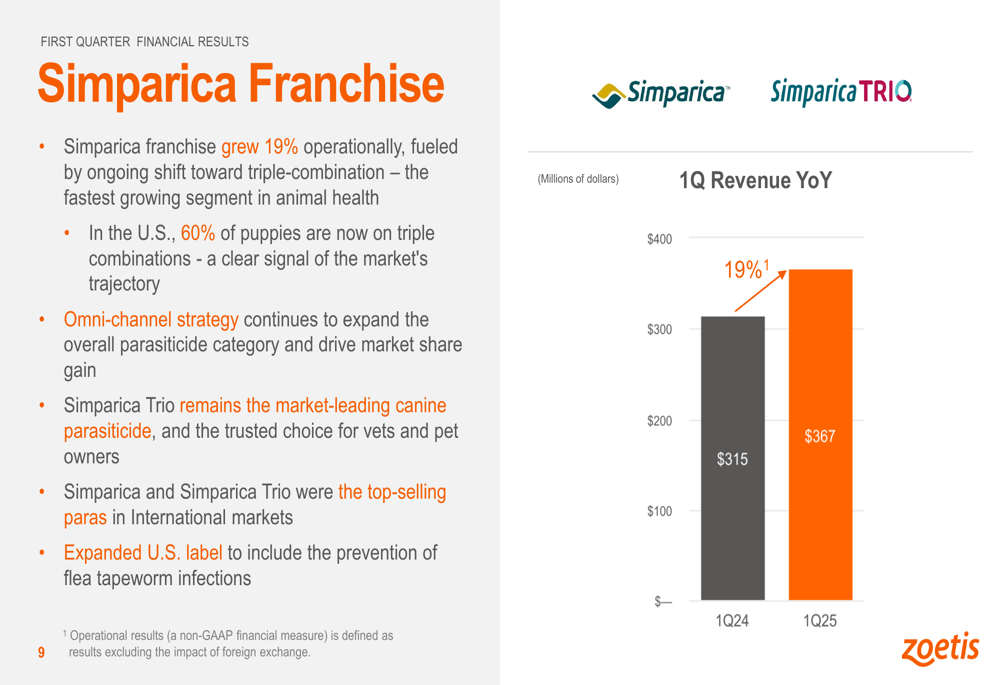

Zoetis’s growth was primarily driven by three key product franchises: Simparica, Dermatology, and Osteoarthritis (OA) Pain. The Simparica franchise, which includes the triple-combination parasiticide Simparica Trio, grew 19% operationally year-over-year, reaching $367 million in Q1 revenue.

As illustrated in the Simparica franchise performance data:

Management highlighted that 60% of puppies in the U.S. are now on triple-combination parasiticides, signaling strong market adoption. Simparica Trio remains the market-leading canine parasiticide, and the company recently expanded its U.S. label to include prevention of flea tapeworm infections.

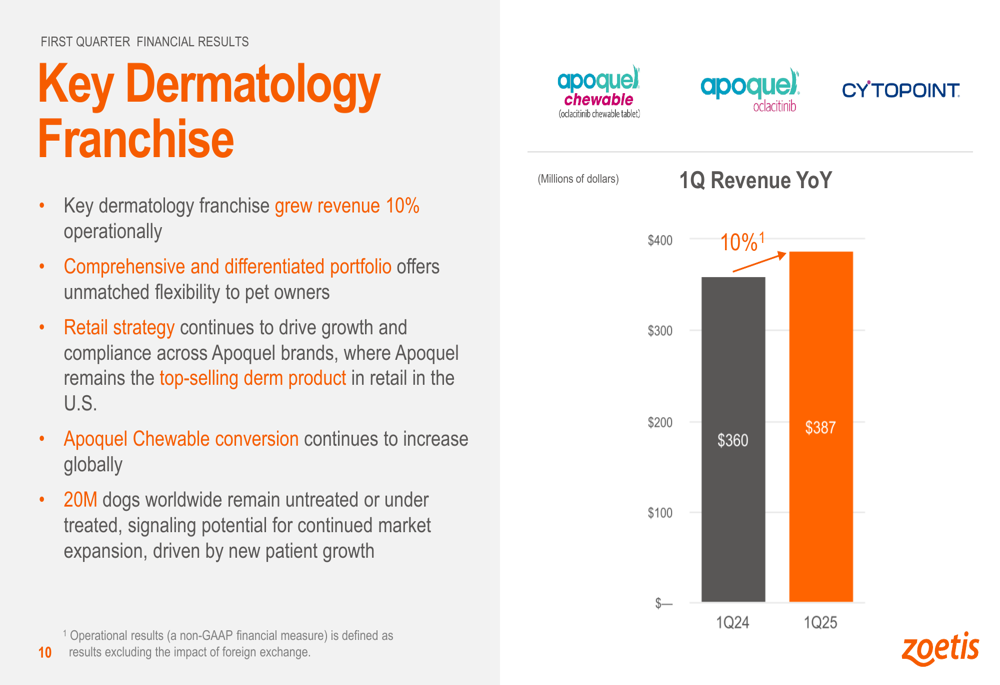

The Key Dermatology franchise, which includes Apoquel and related products, grew 10% operationally to $387 million in Q1. The company’s retail strategy continues to drive growth and compliance across Apoquel brands, with Apoquel remaining the top-selling dermatology product in U.S. retail channels.

The following chart illustrates the dermatology franchise performance:

Management noted significant untapped market potential, with an estimated 20 million dogs worldwide remaining untreated or undertreated for dermatological conditions, providing runway for continued growth.

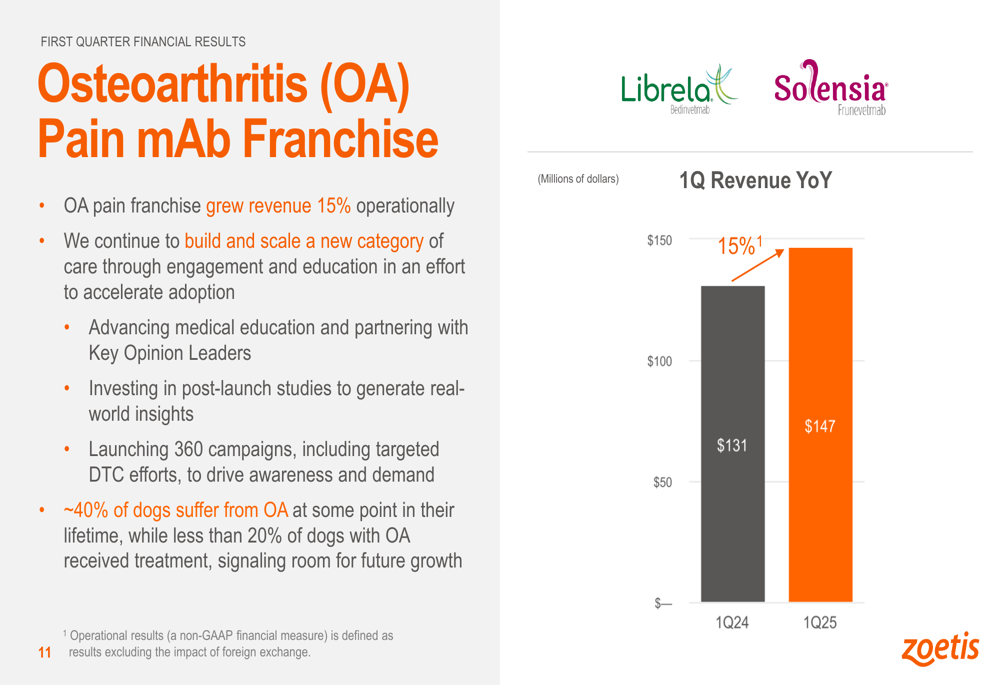

The Osteoarthritis Pain monoclonal antibody franchise grew 15% operationally to $147 million in Q1, as the company continues to build and scale this relatively new category of care:

With approximately 40% of dogs suffering from osteoarthritis at some point in their lifetime, but less than 20% receiving treatment, Zoetis sees substantial opportunity for future growth in this segment. The company is investing in medical education, post-launch studies, and targeted direct-to-consumer campaigns to drive awareness and demand.

Updated Financial Guidance

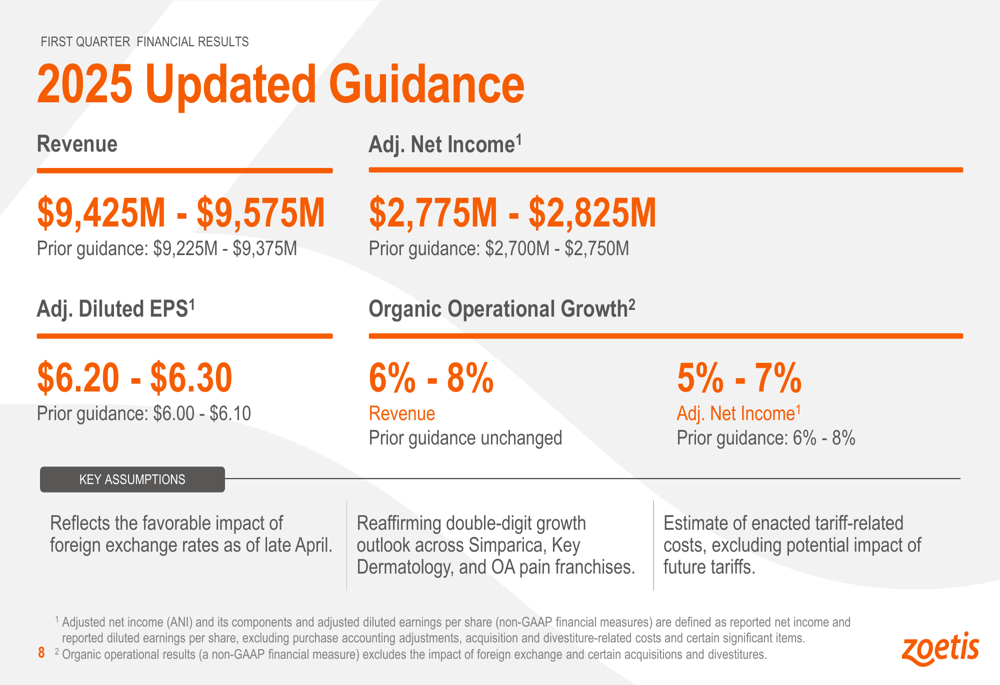

Based on the strong Q1 performance and favorable foreign exchange rates, Zoetis raised its full-year 2025 guidance. The updated outlook includes:

The company now expects revenue between $9,425 million and $9,575 million, up from the previous guidance of $9,225 million to $9,375 million. Adjusted net income is projected to reach $2,775 million to $2,825 million, an increase from the prior guidance of $2,700 million to $2,750 million.

Adjusted diluted EPS is now expected to be between $6.20 and $6.30, compared to the previous guidance of $6.00 to $6.10. The company maintained its organic operational revenue growth projection of 6% to 8% but slightly reduced its organic operational adjusted net income growth expectation to 5% to 7% from the previous 6% to 8%.

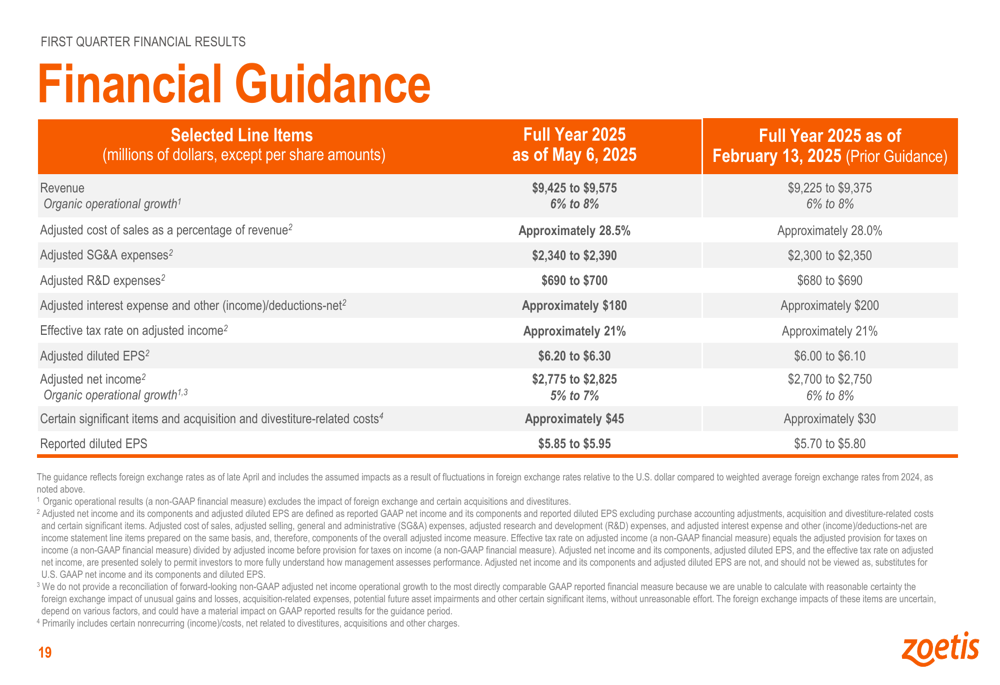

The detailed financial guidance comparison shows the specific changes from the February outlook:

Management reaffirmed its expectation for double-digit growth across the Simparica, Key Dermatology, and OA pain franchises for the full year. The guidance also reflects the favorable impact of foreign exchange rates as of late April and includes estimates of enacted tariff-related costs.

Strategic Initiatives

Zoetis continues to invest in innovation and growth opportunities across its portfolio. In Q1, the company achieved several important regulatory milestones, including a new label indication for Simparica Trio in the U.S. to prevent flea tapeworm infections, conditional licenses for an Avian Influenza Vaccine in the U.S. and Canada, and various approvals for poultry vaccines across multiple markets.

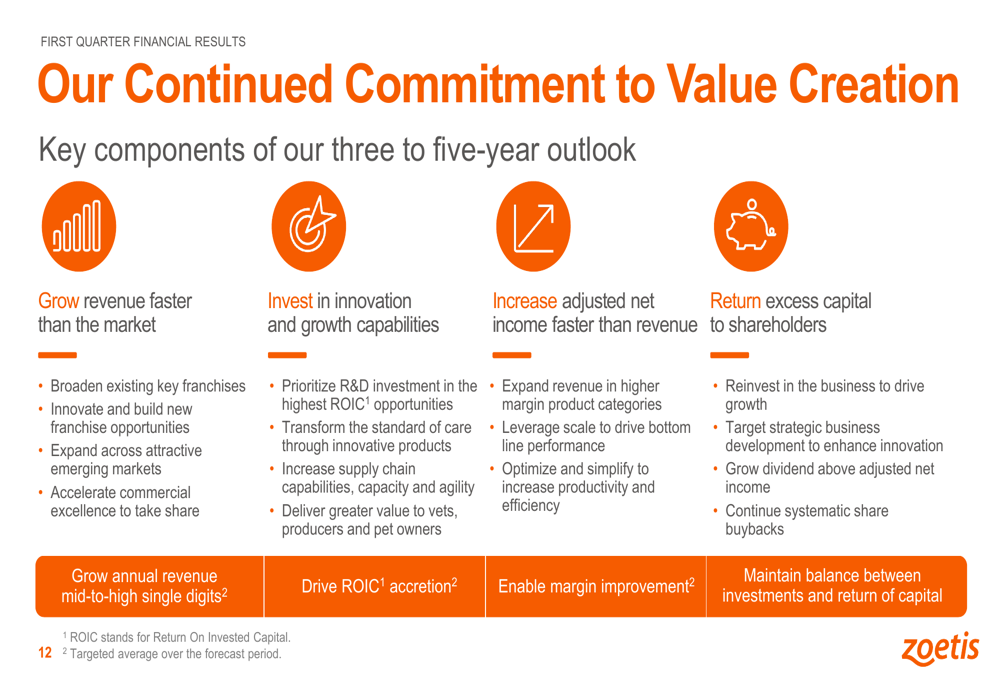

The company’s long-term strategy focuses on four key areas: growing revenue faster than the market, investing in innovation and growth capabilities, increasing adjusted net income faster than revenue, and returning excess capital to shareholders.

Management emphasized its commitment to broadening existing key franchises, innovating to build new franchise opportunities, expanding in emerging markets, and accelerating commercial excellence to gain market share. The company aims to grow annual revenue at mid-to-high single digits while enabling margin improvement.

Zoetis’s strong Q1 2025 performance and raised guidance reflect the company’s robust position in the animal health market and its effective execution of strategic priorities. With continued innovation and expansion across its key franchises, Zoetis appears well-positioned to maintain its growth trajectory throughout 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.