Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Zoetis Inc . (NYSE:ZTS) reported solid second-quarter results on August 5, 2025, with broad-based growth across its portfolio driving an 8% increase in organic operational revenue. The animal health company raised its full-year guidance following the strong performance, which saw its stock surge 6.05% in pre-market trading to $161.

Quarterly Performance Highlights

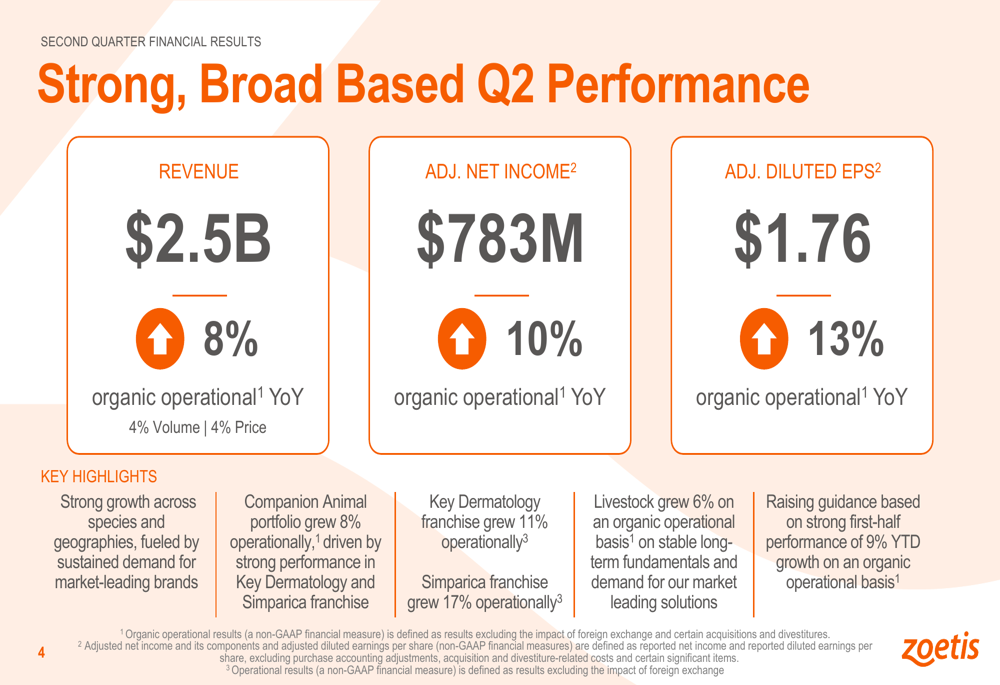

Zoetis delivered robust financial results for the second quarter of 2025, with revenue reaching $2.5 billion, representing an 8% organic operational increase year-over-year. This growth was evenly split between volume (4%) and price (4%). The company’s adjusted net income rose to $783 million, up 10% organically from the previous year, while adjusted diluted earnings per share increased 13% to $1.76.

As shown in the following quarterly performance summary:

The results exceeded analysts’ expectations, with the $1.76 EPS surpassing the forecasted $1.62 by 8.64%. This strong performance was driven by growth across species and geographies, with particular strength in the company’s market-leading brands.

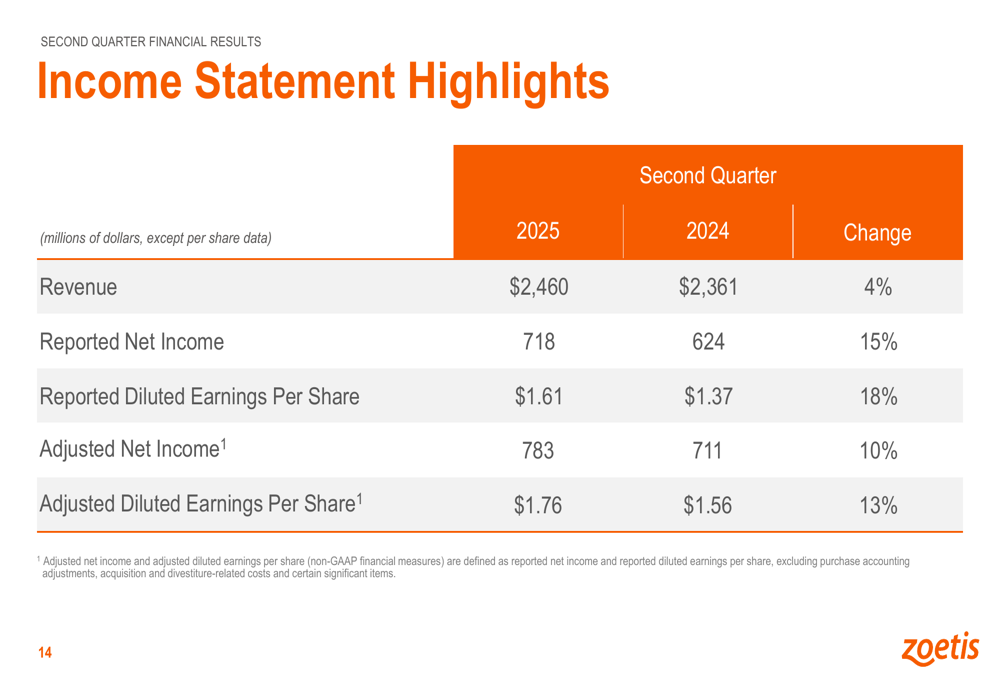

The detailed income statement highlights show significant improvements across key metrics:

Product Portfolio Performance

Zoetis’s companion animal portfolio continued to drive growth, with particularly strong performance from its parasiticide and dermatology franchises.

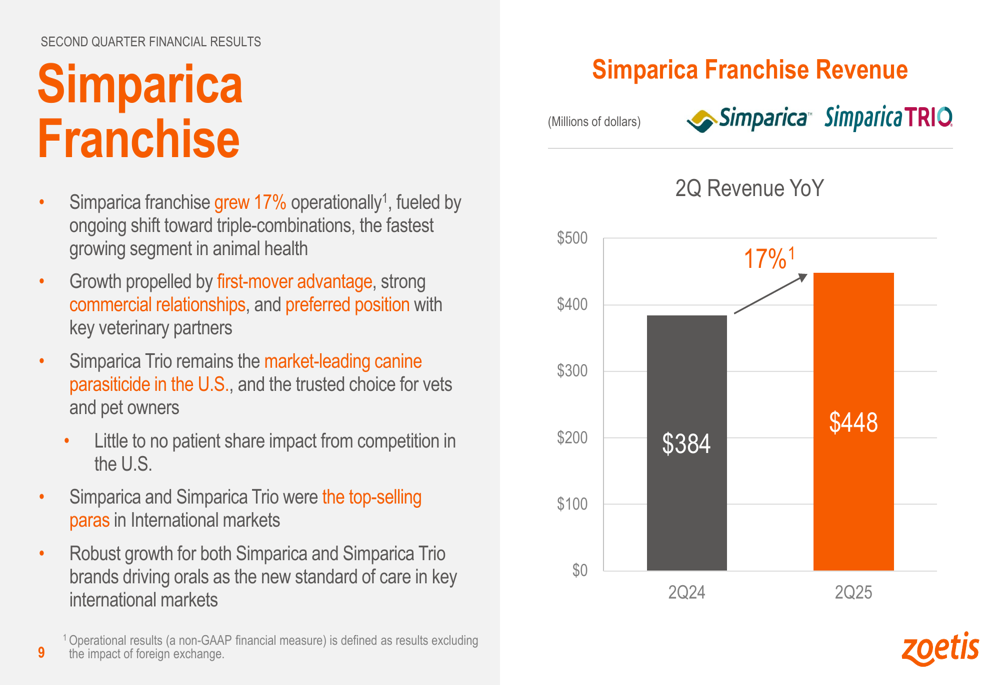

The Simparica franchise, which includes the company’s flagship parasiticide products, grew 17% operationally year-over-year, reaching $448 million in quarterly revenue. This growth was attributed to Simparica Trio’s market-leading position and first-mover advantage in the canine parasiticide market.

As illustrated in the following chart of the Simparica franchise performance:

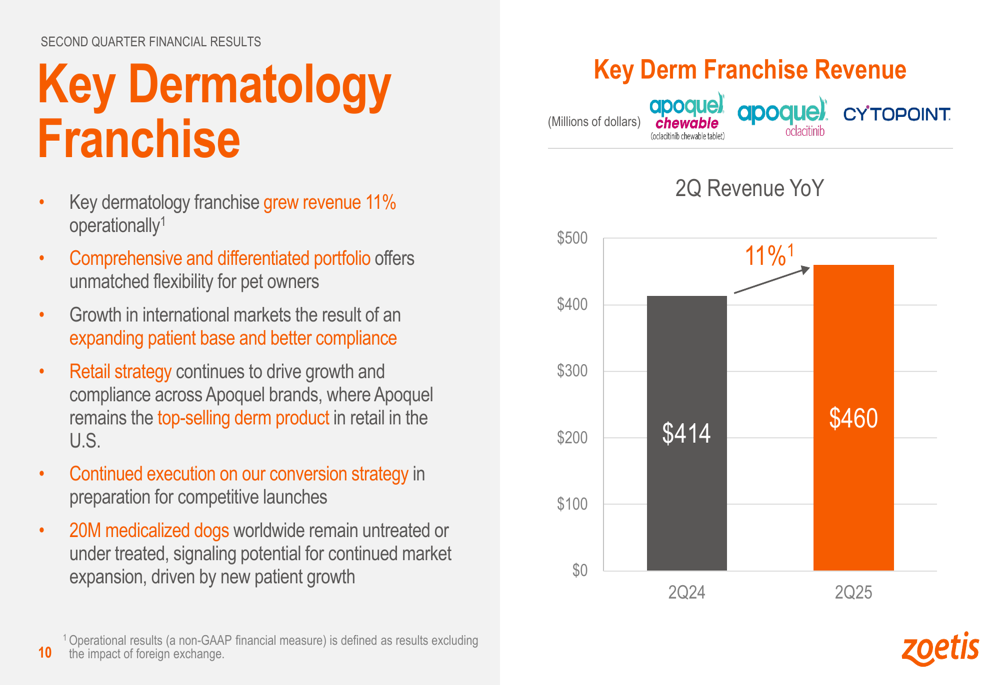

Similarly, the key dermatology franchise showed robust growth of 11% operationally, generating $460 million in Q2 revenue. The company highlighted its comprehensive and differentiated portfolio offering "unmatched flexibility" as a key driver of this growth, along with expansion in international markets and successful retail and conversion strategies.

However, not all product lines performed equally well. The Osteoarthritis (OA) Pain monoclonal antibody franchise, which includes products like Librela, experienced a 4% operational decline, with revenue falling from $149 million in Q2 2024 to $145 million in Q2 2025. During the earnings call, management addressed challenges in Librela adoption, emphasizing their focus on education and third-party studies to drive future growth.

Segment Analysis

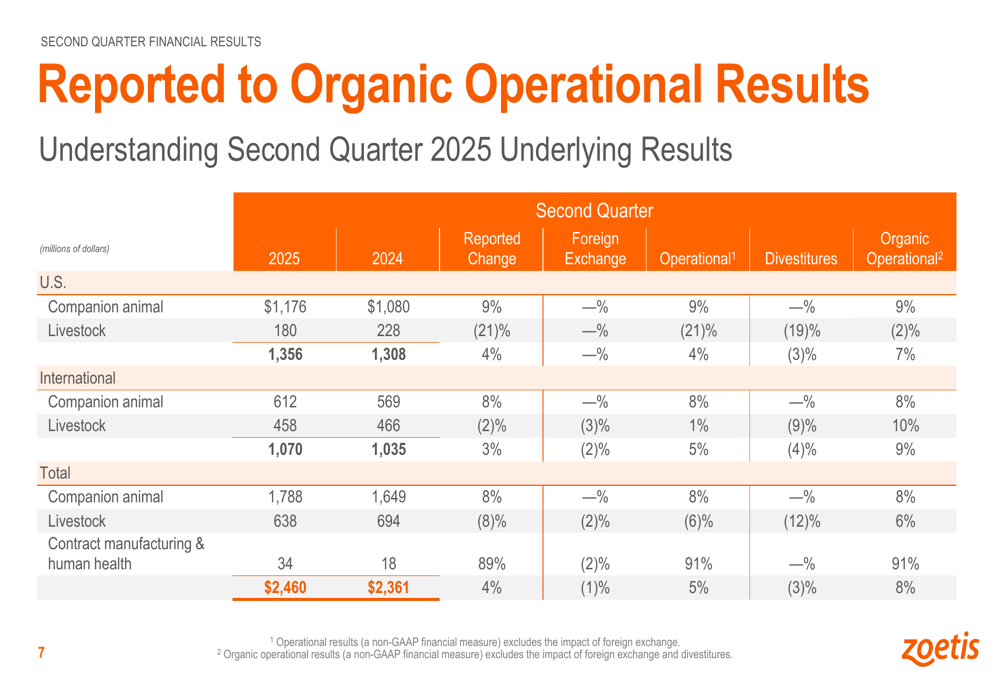

Zoetis reported strong performance across both its U.S. and International segments. The U.S. segment generated revenue of $1.4 billion, representing 7% organic operational growth year-over-year. This was primarily driven by the companion animal business, which grew 9% to $1.2 billion, while livestock revenue in the U.S. declined 2% to $0.2 billion.

The International segment delivered even stronger results, with revenue of $1.1 billion reflecting 9% organic operational growth. Both companion animal and livestock businesses contributed to this growth, with companion animal revenue up 8% to $0.6 billion and livestock revenue increasing 10% to $0.5 billion.

The following table provides a detailed breakdown of reported to organic operational results:

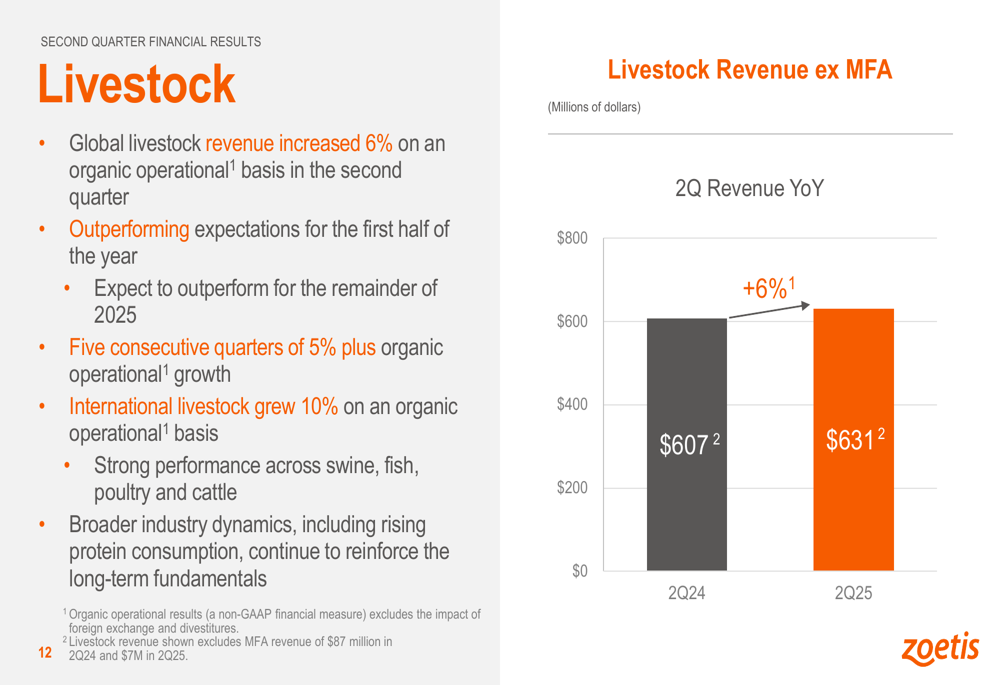

The livestock segment, which had faced challenges in previous quarters, showed significant improvement with global livestock revenue increasing 6% on an organic operational basis. Management noted this represented the fifth consecutive quarter of 5%+ organic operational growth in this segment, indicating a sustained recovery.

Raised Financial Guidance

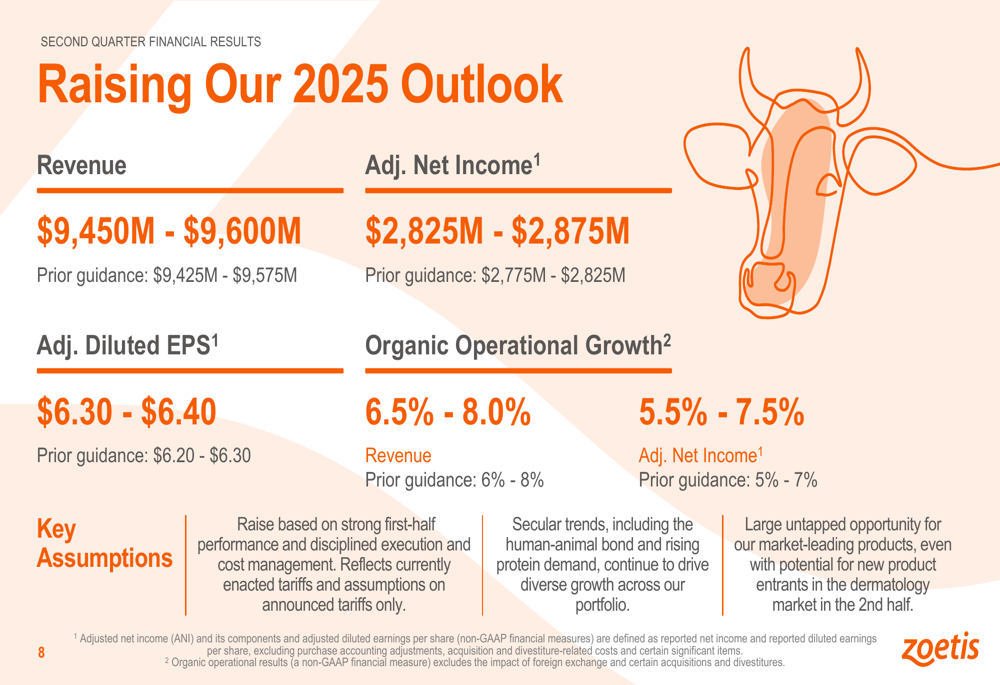

Based on the strong first-half performance, Zoetis raised its full-year 2025 guidance. The company now expects revenue to be between $9,450 million and $9,600 million, up from the previous guidance of $9,425 million to $9,575 million. Organic operational growth is projected at 6.5% to 8.0%, reflecting confidence in continued strong performance.

Similarly, adjusted net income guidance was increased to $2,825 million to $2,875 million, up from $2,775 million to $2,825 million previously. Adjusted diluted EPS is now expected to be in the range of $6.30 to $6.40, compared to the prior guidance of $6.20 to $6.30.

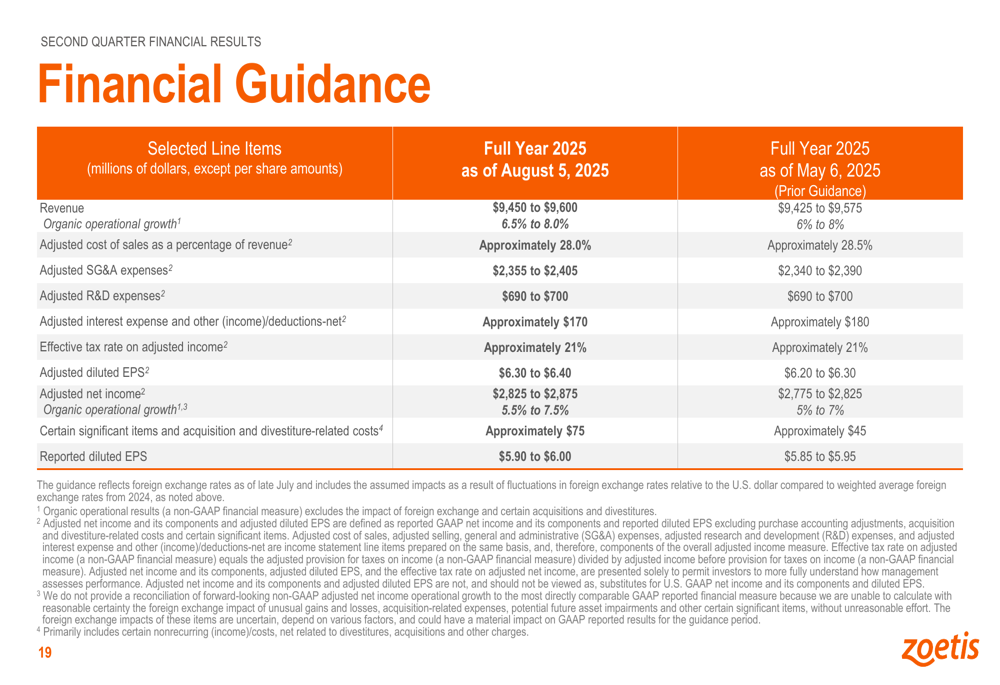

The updated guidance is detailed in the following slide:

The comprehensive financial guidance provides additional details on various expense categories and growth projections:

Forward-Looking Statements

Zoetis highlighted several recent product approvals and advancements that are expected to contribute to future growth. These include new label indications for Simparica Trio in Japan, additional claims for Revolution Plus in Australia, and new approvals for livestock vaccines in Brazil, the EU, and the U.S.

CEO Kristin Peck emphasized the company’s resilience during the earnings call, stating, "We are a strong resilient industry," highlighting Zoetis’s ability to navigate challenges and capitalize on growth opportunities. CFO Wetteny Joseph expressed optimism about future growth, noting, "We expect triple combinations to double by 2028," underscoring the company’s strategic market positioning.

Despite the overall positive outlook, the company faces potential challenges including supply chain issues, market saturation, macroeconomic pressures, tariff impacts, and regulatory changes. During the Q&A session, management addressed concerns about tariff impacts, indicating they are managing these through a diversified supply chain strategy.

With the stock trading near its 52-week low of $139.70 prior to the earnings announcement, the positive results and raised guidance suggest potential for recovery, with analysts setting targets as high as $230. The 6.05% jump in pre-market trading following the earnings release reflects renewed investor confidence in Zoetis’s growth trajectory and market leadership in the animal health sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.