Can anything shut down the Gold rally?

Introduction & Market Context

Zoom Video Communications (NASDAQ:ZM) presented its second-quarter fiscal year 2026 results on August 21, 2025, showing accelerating revenue growth and continued expansion of its enterprise business. Despite the company’s improved performance, Zoom’s stock fell 1.05% in after-hours trading to $71.40, following a 1.48% gain during the regular session.

The company continues to transform beyond its core video conferencing roots, with significant investments in artificial intelligence and expansion into contact center and employee experience solutions. Zoom’s presentation highlighted its recognition as a leader in the unified communications-as-a-service (UCaaS) space by Forrester Research (NASDAQ:FORR).

Quarterly Performance Highlights

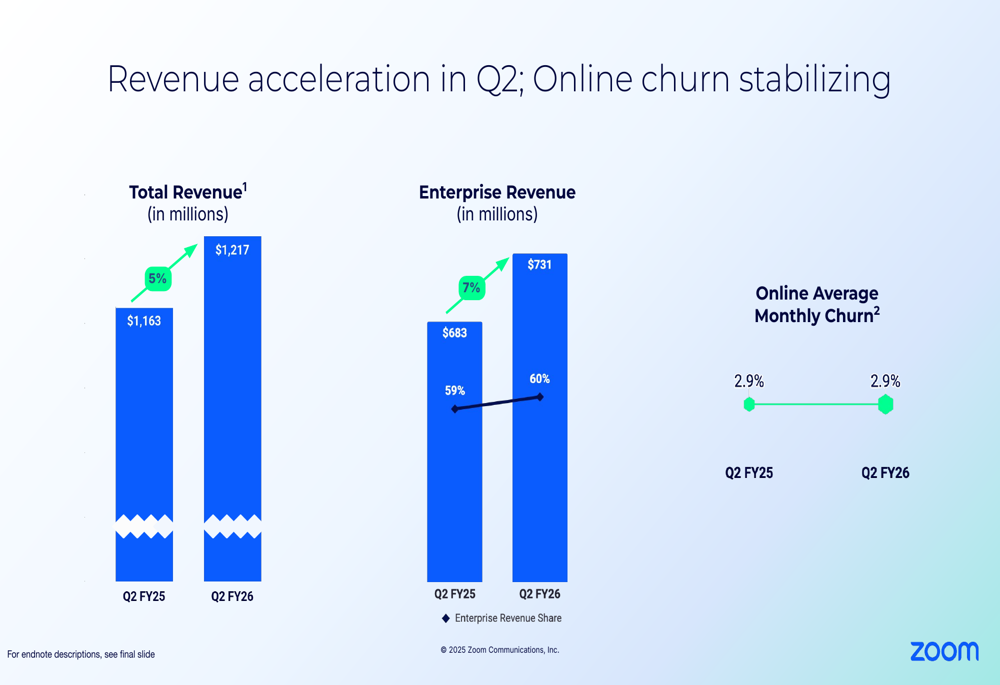

Zoom reported total revenue of $1,217 million for Q2 FY26, representing a 5% year-over-year increase, an acceleration from the 3% growth reported in Q1. Enterprise revenue grew at an even faster pace of 7%, reaching $731 million and now accounting for 60% of total revenue.

As shown in the following revenue breakdown:

The company’s online business appears to be stabilizing, with average monthly churn remaining flat at 2.9% year-over-year. This stability in the online segment, combined with the stronger enterprise growth, suggests Zoom’s business model is finding equilibrium after the post-pandemic normalization period.

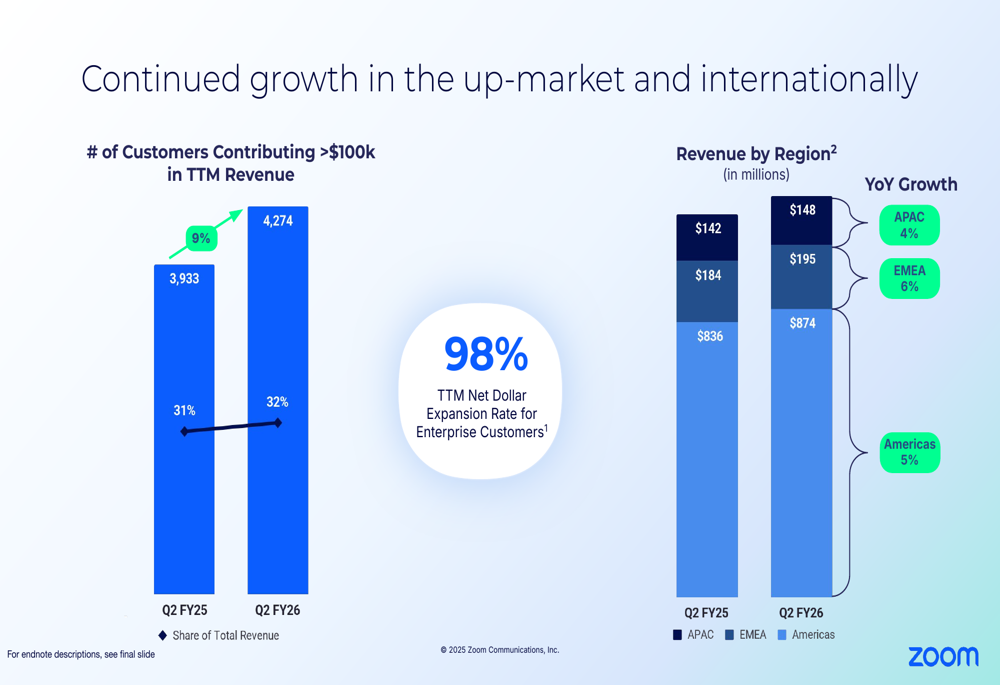

Zoom continued to make progress in expanding its high-value customer base, with 4,274 customers contributing more than $100,000 in trailing twelve-month revenue, a 9% increase from the previous year. The company also demonstrated growth across all geographic regions, with EMEA leading at 6% year-over-year growth, followed by Americas at 5% and APAC at 4%.

The following chart illustrates this international expansion:

AI and Product Innovation

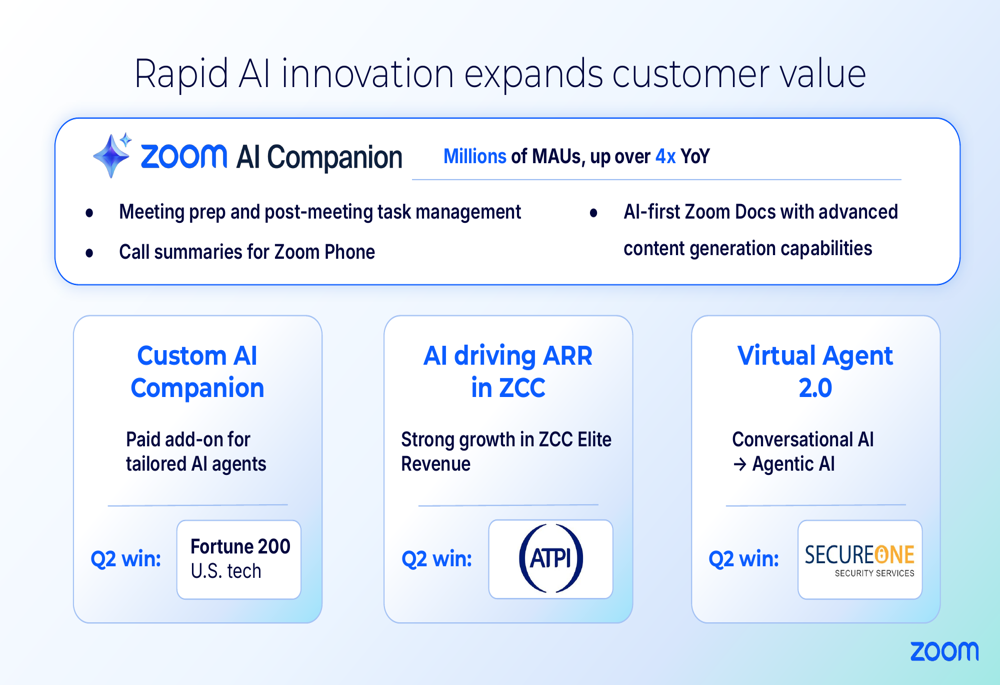

Artificial intelligence emerged as a central theme in Zoom’s presentation, with the company reporting significant adoption of its AI Companion feature. According to the slides, AI Companion users have increased more than fourfold year-over-year, with millions of monthly active users now utilizing features like meeting preparation, post-meeting task management, and call summaries.

The company also introduced Custom AI Companion, a paid add-on for tailored AI agents, which secured a win with a Fortune 200 U.S. technology company during the quarter. Additionally, Zoom highlighted its AI-first document solution and the evolution of its Virtual Agent from conversational AI to agentic AI.

These AI innovations are illustrated in the following slide:

Zoom’s product portfolio expansion beyond meetings continues to gain recognition, with the company being named a Leader in The Forrester Wave™ for UCaaS in 2025. The presentation highlighted several awards, including Best UC Platform, Best UCaaS Provider for the Americas, Best Contact Center Solution, and Most Innovative Product for AI Companion.

Enterprise Growth and Competitive Position

Zoom’s enterprise strategy appears to be gaining traction, particularly in high-growth departmental solutions. The company reported 229 Zoom Contact Center (ZCC) customers with annual recurring revenue exceeding $100,000, representing a 94% year-over-year increase. Notably, Zoom claimed that nine out of its top ten ZCC deals were displacements of leading Contact Center as a Service (CCaaS) competitors.

Similarly, Workvivo, Zoom’s employee experience platform, showed strong momentum with 168 customers contributing more than $100,000 in ARR, a 142% year-over-year increase. The company also announced a new collaboration with PwC to further expand its enterprise reach.

The following slide details these departmental solution metrics:

Financial Analysis and Cash Flow

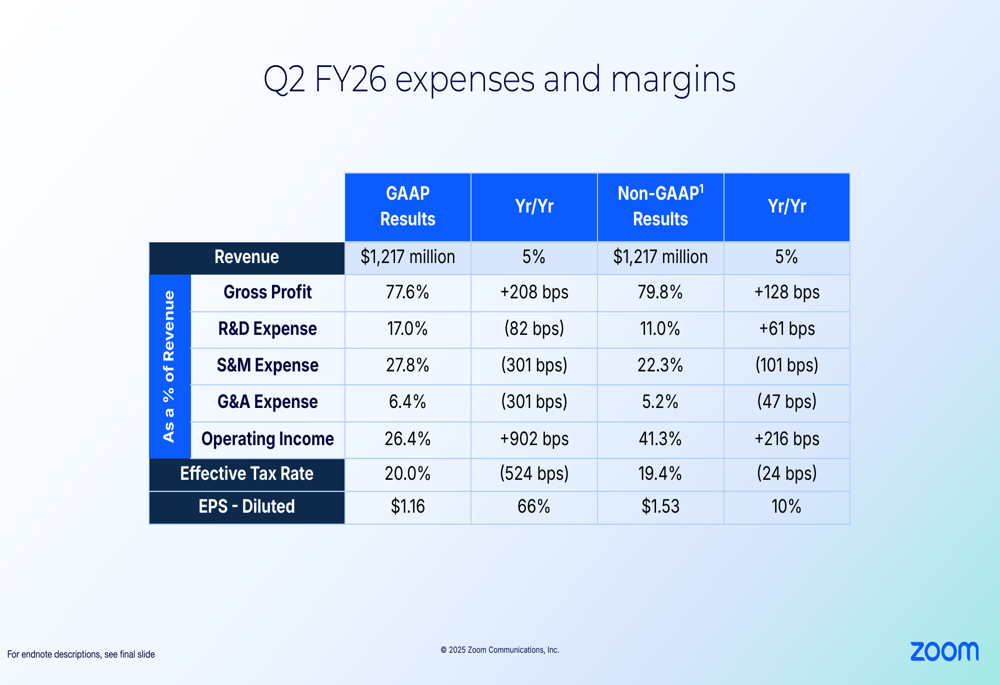

Zoom’s financial performance showed significant improvement in profitability metrics. Non-GAAP operating margin expanded by 216 basis points year-over-year to reach 41.3%, while GAAP operating margin improved by an even more substantial 902 basis points to 26.4%. Diluted non-GAAP earnings per share increased 10% to $1.53.

The detailed financial breakdown is presented in this comprehensive slide:

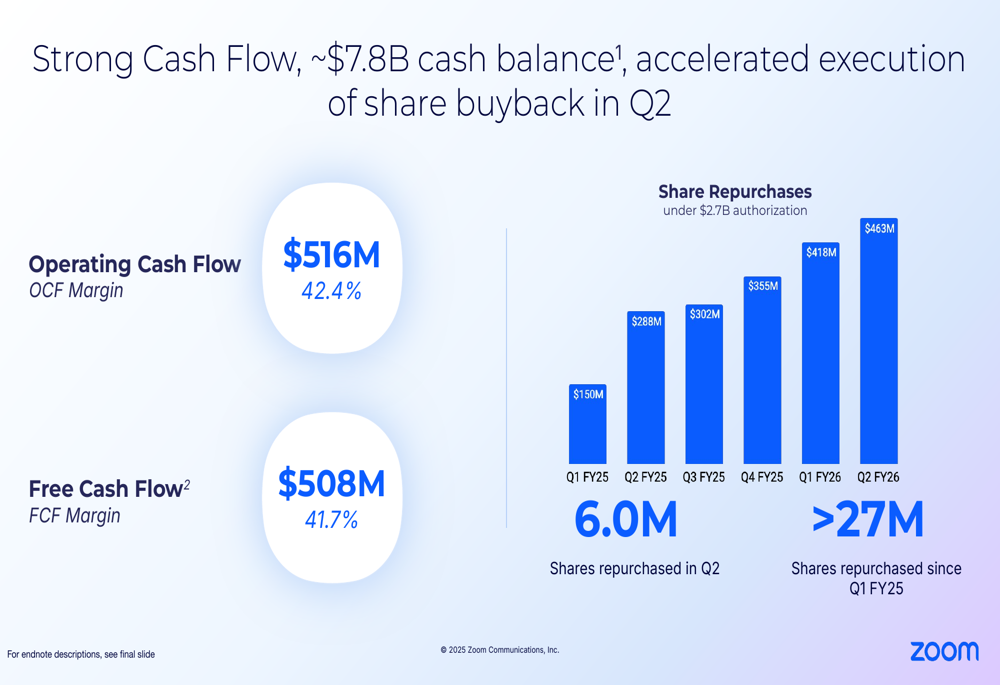

Cash flow generation remained robust, with operating cash flow of $516 million (42.4% margin) and free cash flow of $508 million (41.7% margin). The company continued its aggressive share repurchase program, buying back $463 million worth of shares in Q2 FY26, bringing the total repurchases to over 27 million shares since Q1 FY25. Zoom maintains a strong cash position of approximately $7.8 billion.

The following chart illustrates the accelerating share buyback program:

Forward Guidance and Outlook

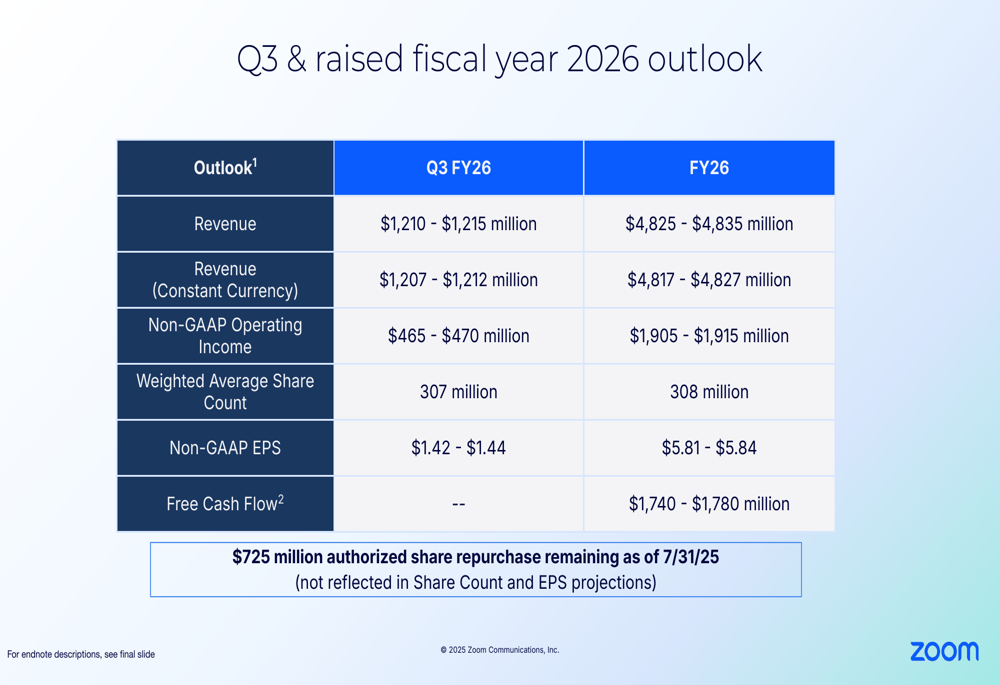

Zoom raised its full-year fiscal 2026 outlook, projecting revenue between $4,825 million and $4,835 million, representing approximately 3-4% year-over-year growth. For the third quarter, the company expects revenue between $1,210 million and $1,215 million.

Non-GAAP operating income for the full year is projected to be between $1,905 million and $1,915 million, with non-GAAP EPS expected to range from $5.81 to $5.84. The company also forecasts strong free cash flow of $1,740 million to $1,780 million for fiscal year 2026.

The detailed outlook is presented in the following slide:

Zoom’s remaining performance obligations (RPO) grew 5% year-over-year to $3,976 million, with current RPO increasing 6% to $1,565 million. This growth in RPO, combined with the 5% increase in deferred revenue, provides visibility into future revenue streams and suggests continued business momentum.

Despite the positive operational results and raised guidance, Zoom’s stock price has declined significantly since its Q1 earnings report, when it traded at $83.10. The current price of $72.16 reflects ongoing investor concerns about Zoom’s long-term growth prospects in an increasingly competitive market for communication and collaboration tools, even as the company demonstrates improved financial performance and business diversification.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.