Gold prices jump to near 3-week high amid US shutdown progress

Zymeworks Inc. (NASDAQ:ZYME) presented its third quarter 2025 results on November 6, highlighting significant revenue growth, clinical progress across its antibody-drug conjugate (ADC) pipeline, and strategic partnership developments. The company’s stock rose 1.5% to $18.32 in aftermarket trading following the presentation.

Quarterly Performance Highlights

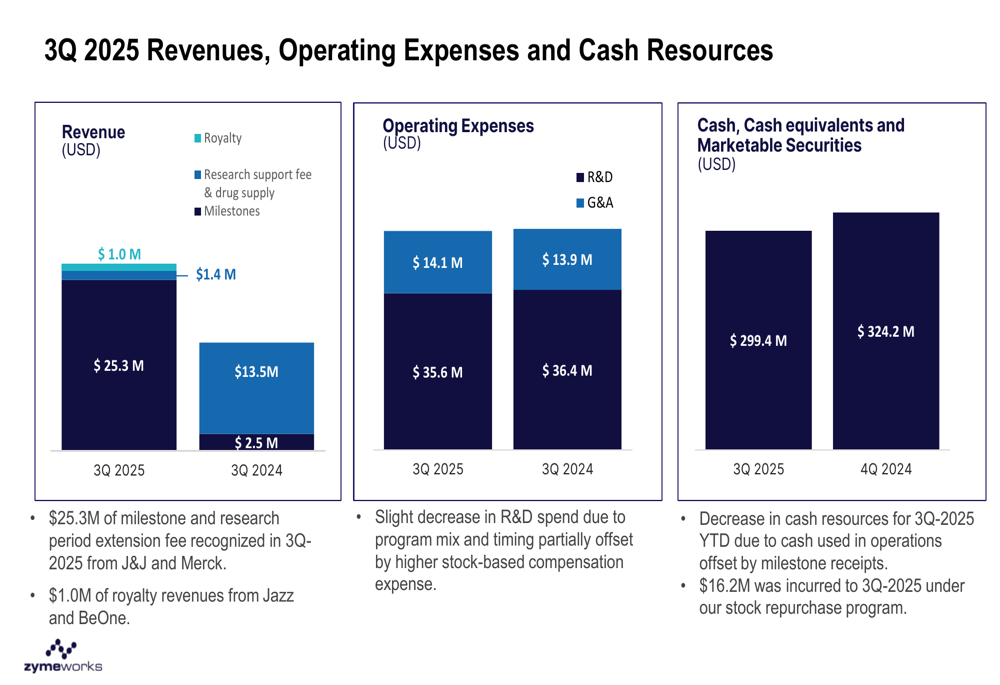

Zymeworks reported total revenue of $26.3 million for Q3 2025, representing a 51% increase from $17.4 million in the same period last year. This growth was primarily driven by milestone payments and research extension fees of $25.3 million from Johnson & Johnson and Merck, complemented by $1.0 million in royalty revenues from Jazz Pharmaceuticals and BeOne.

Operating expenses remained relatively stable at $49.7 million for the quarter, slightly down from $50.3 million in Q3 2024. Research and development expenses decreased marginally to $35.6 million (from $36.4 million), while general and administrative expenses increased slightly to $14.1 million (from $13.9 million).

As shown in the following chart of quarterly financial performance:

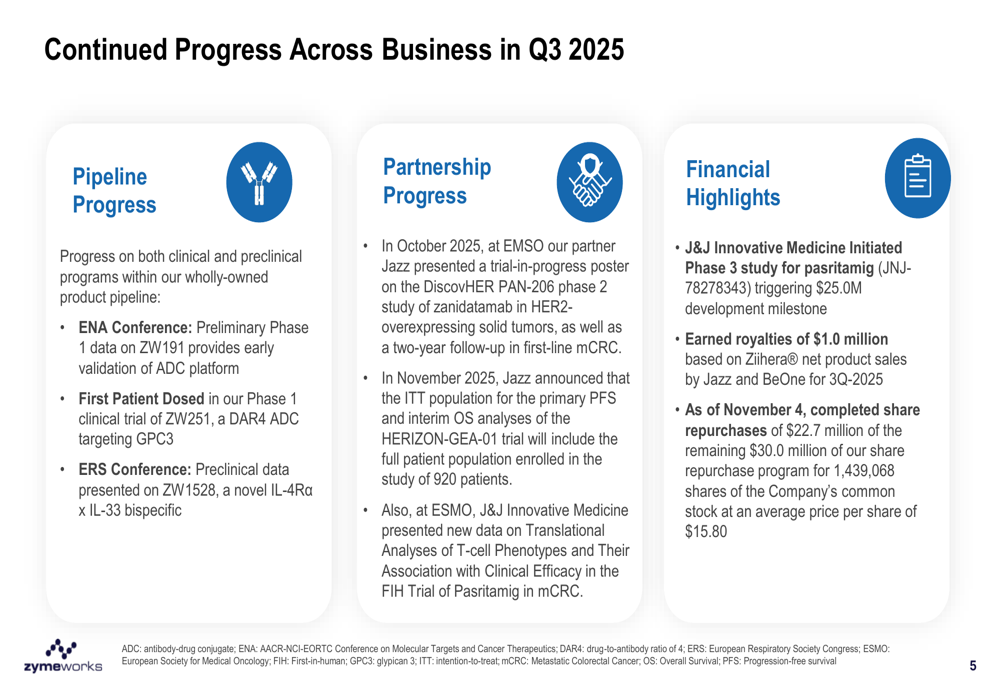

The company’s cash position stood at $299.4 million as of Q3 2025, compared to $324.2 million at the end of 2024. This decrease reflects cash used in operations, partially offset by milestone receipts. Zymeworks also continued its share repurchase program, completing $22.7 million of the remaining $30.0 million authorization for 1,439,068 shares at an average price of $15.80 per share as of November 4.

Clinical Pipeline Progress

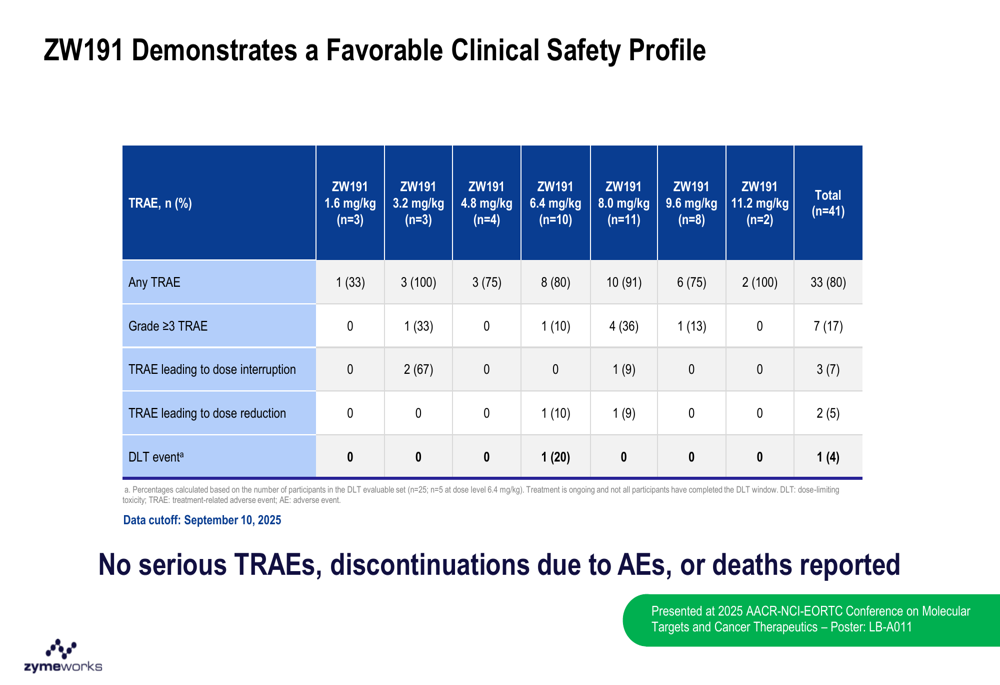

Zymeworks presented promising preliminary Phase 1 data for ZW191, its folate receptor alpha (FRα)-targeted antibody-drug conjugate, at the European Network of Antibody and Cancer Therapeutics (ENA) Conference. The data demonstrated a favorable safety profile across multiple dose levels, with no serious treatment-related adverse events, discontinuations, or deaths reported.

The safety profile of ZW191 is illustrated in the following chart:

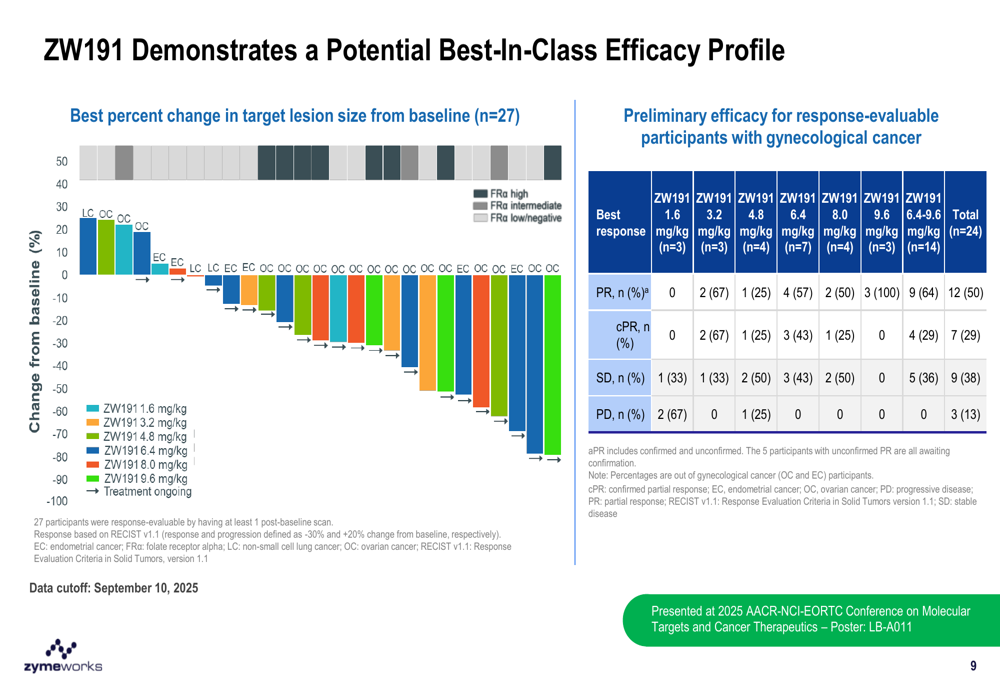

More importantly, ZW191 showed encouraging efficacy results in gynecological cancers, with 50% of response-evaluable participants (12 of 24) achieving partial responses and 29% (7 of 24) achieving confirmed partial responses. The waterfall plot below demonstrates the reduction in target lesion size across patients:

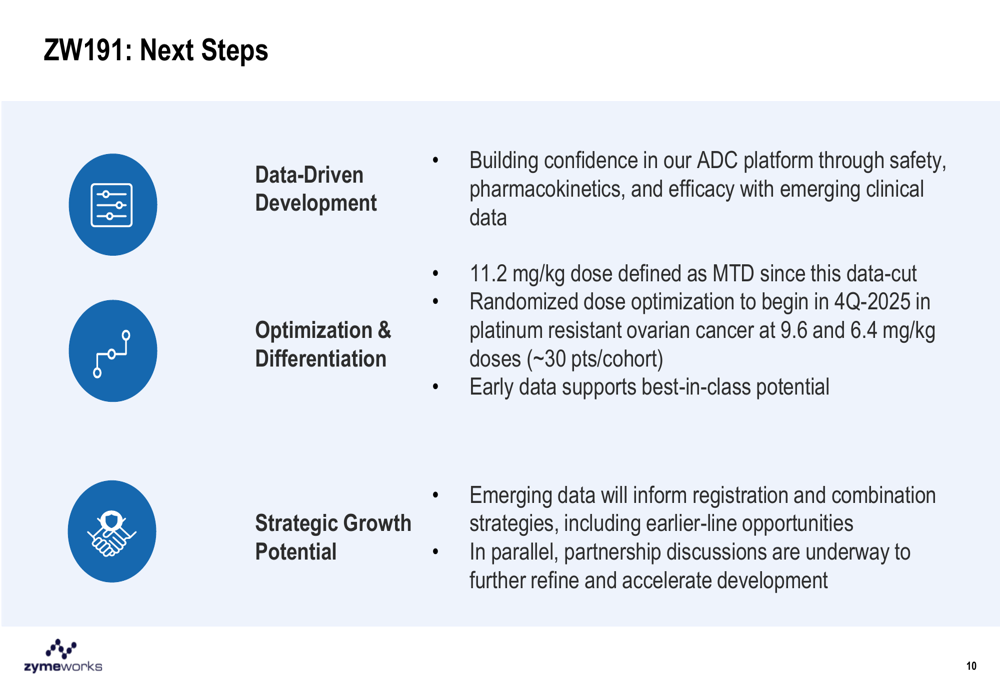

Based on these promising results, Zymeworks plans to initiate a randomized dose optimization study in Q4 2025 for platinum-resistant ovarian cancer, evaluating 9.6 mg/kg and 6.4 mg/kg doses with approximately 30 patients per cohort. The company believes the data supports ZW191’s potential as a best-in-class ADC candidate.

The company’s strategic roadmap for ZW191 includes:

Additionally, Zymeworks announced that the first patient has been dosed in the Phase 1 clinical trial of ZW251, a DAR4 ADC targeting Glypican 3 (GPC3) for hepatocellular carcinoma.

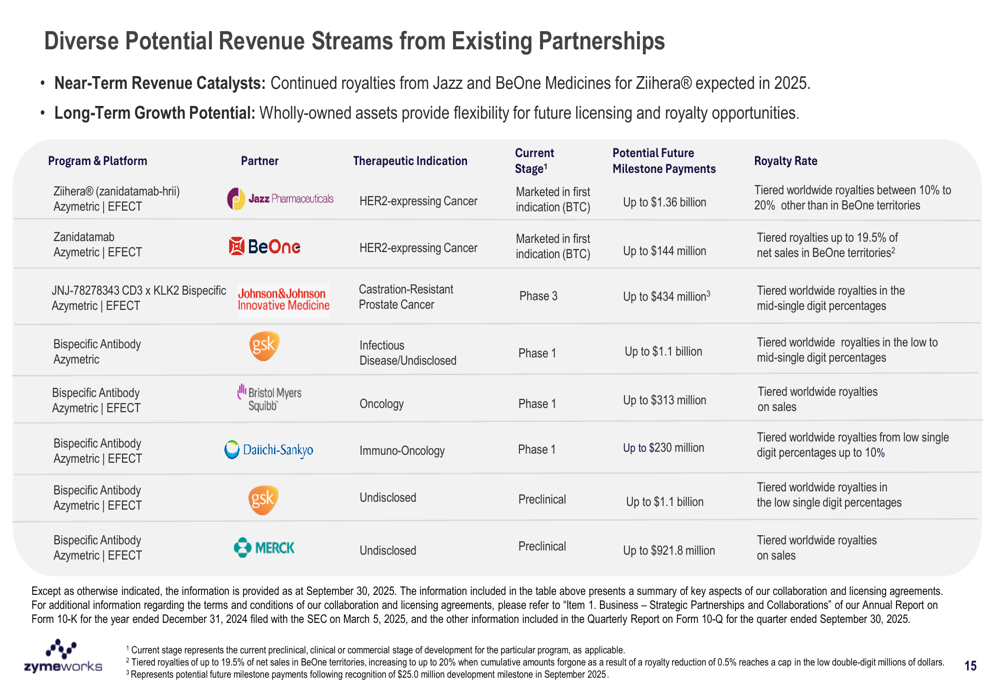

Strategic Partnerships

Zymeworks continues to leverage its partnership model to generate near-term revenue while building long-term value. The company’s diverse partnership portfolio includes eight programs with major pharmaceutical companies, offering substantial milestone payment potential and tiered royalties.

The following chart illustrates the company’s partnership landscape and potential revenue streams:

Notable partnership developments in Q3 2025 included:

- Johnson & Johnson Innovative Medicine initiated a Phase 3 study for pasritamig (JNJ-78278343), triggering a $25.0 million development milestone payment to Zymeworks

- Jazz Pharmaceuticals presented a trial-in-progress poster on the DiscovHER PAN-206 phase 2 study of zanidatamab in HER2-overexpressing solid tumors

- Jazz announced that the ITT population for the primary PFS and interim OS analyses of the HERIZON-GEA-01 trial will include the full patient population of 920 patients

- Zymeworks earned royalties of $1.0 million based on Ziihera® net product sales by Jazz and BeOne for Q3 2025

Forward-Looking Statements

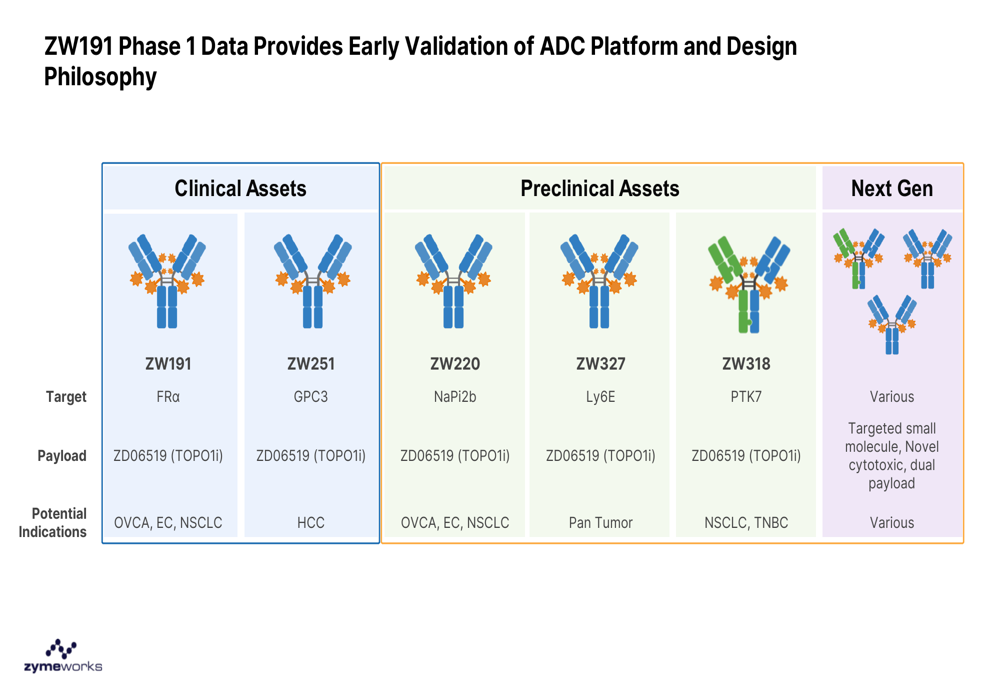

Zymeworks is advancing a diversified pipeline of ADCs and multispecific antibodies, with five programs currently in clinical development. The company’s ADC platform strategy is illustrated below:

Looking ahead, Zymeworks plans to leverage learnings from its ZW171 Phase 1 trial to enhance its next-generation T-cell engager pipeline, particularly through the incorporation of CD3-dependent CD28 co-stimulation to overcome challenges in solid tumors.

The company’s business progress across multiple fronts in Q3 2025 is summarized in this comprehensive overview:

With a strong cash position of $299.4 million and multiple potential revenue catalysts from partnerships, Zymeworks appears well-positioned to advance its pipeline while maintaining financial stability. The company’s focus on data-driven development and strategic partnerships suggests a balanced approach to maximizing the value of its proprietary platforms while managing development risks.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.