Gold prices bounce off 3-week lows; demand likely longer term

Introduction & Market Context

Angel Oak Mortgage REIT, Inc. (NYSE:AOMR) released its first quarter 2025 earnings presentation showing strong financial performance with significant growth in net interest income and book value. The mortgage REIT, which specializes in non-QM residential mortgage loans, reported substantial improvements in key metrics while successfully executing its securitization strategy to reduce leverage.

The company’s stock closed at $9.55 on May 2, 2025, and gained 0.63% during regular trading hours, with an additional 1.05% increase to $9.65 in after-hours trading. This price remains below both the reported GAAP book value of $10.70 and economic book value of $13.41 per share.

Quarterly Performance Highlights

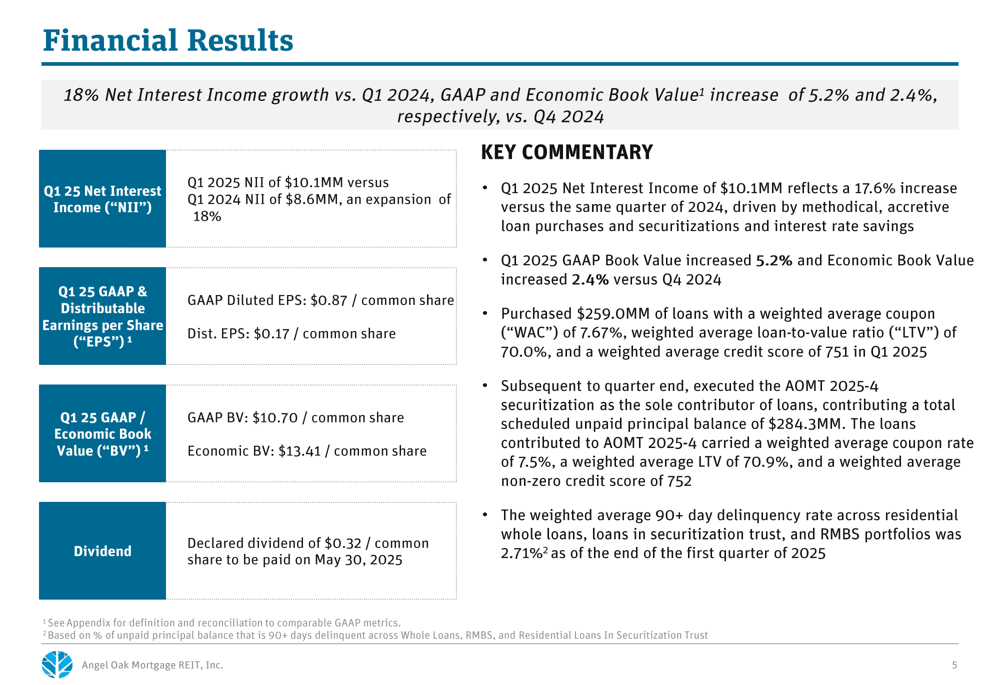

Angel Oak Mortgage delivered impressive financial results for Q1 2025, with net interest income reaching $10.1 million, an 18% increase compared to $8.6 million in Q1 2024. The company reported GAAP diluted earnings per share of $0.87 and distributable earnings per share of $0.17 for the quarter.

As shown in the following detailed financial results summary:

The company’s GAAP book value per share increased to $10.70, representing a 5.2% increase from Q4 2024 and a 1.5% increase year-over-year. Economic book value, which adjusts for the fair value of securitized debt held at amortized cost, reached $13.41 per share, a 2.4% increase from the previous quarter.

The quarterly dividend was maintained at $0.32 per common share, representing a yield of approximately 13.4% based on the current stock price.

Detailed Financial Analysis

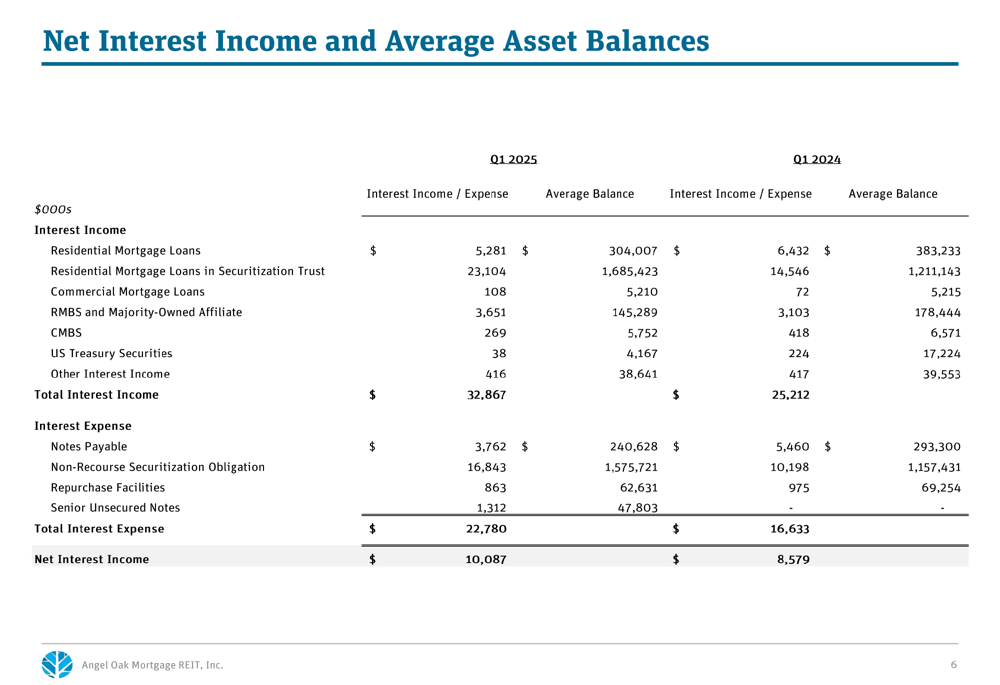

The company’s net interest income growth was driven by methodical loan purchases and securitizations, as well as interest rate savings. The following breakdown illustrates the components of this growth:

Interest income from residential mortgage loans in securitization trusts showed particularly strong performance, increasing to $23.1 million in Q1 2025 from $14.5 million in Q1 2024. This growth reflects the company’s successful execution of its securitization strategy and the increasing scale of its loan portfolio.

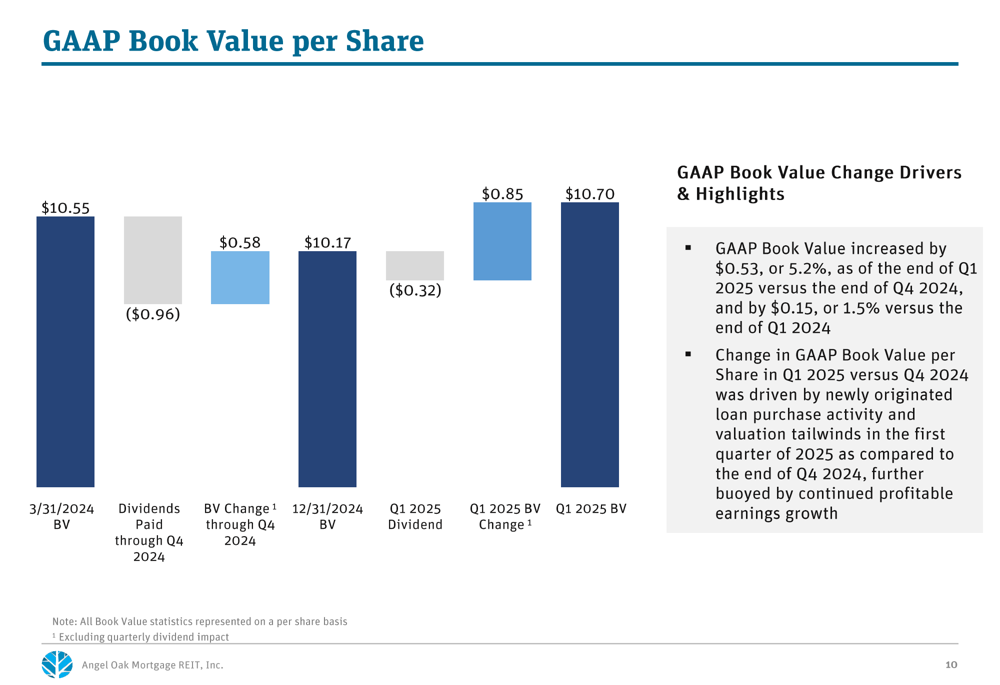

The company’s GAAP book value has shown resilience and growth over time, as illustrated in this chart:

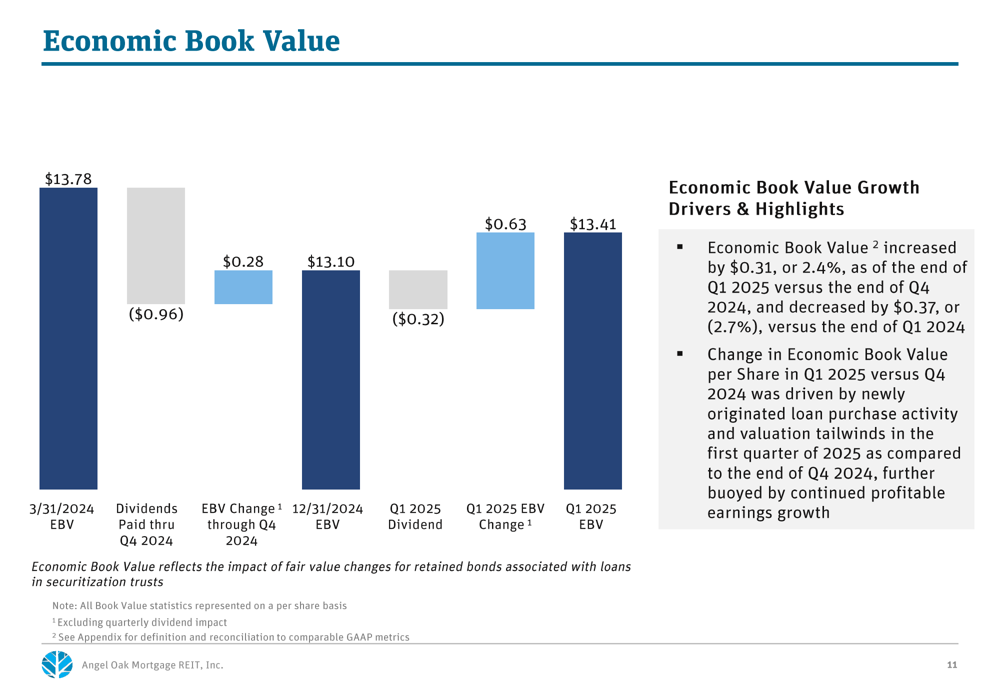

Similarly, the economic book value, which provides an alternative valuation metric, has maintained stability despite dividend payments:

Strategic Initiatives

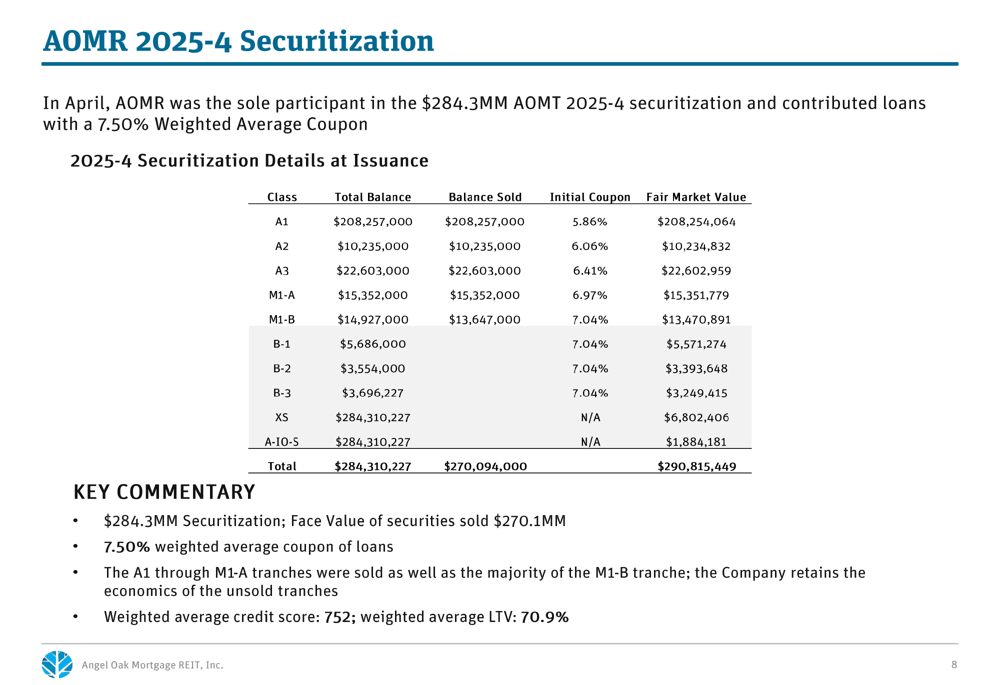

Angel Oak Mortgage’s securitization strategy remains a cornerstone of its business model. In April 2025, the company executed the AOMT 2025-4 securitization as the sole contributor of loans, with a total unpaid principal balance of $284.3 million. The securitization featured loans with a weighted average coupon of 7.5%, weighted average LTV of 70.9%, and weighted average credit score of 752.

The details of this securitization are presented in the following chart:

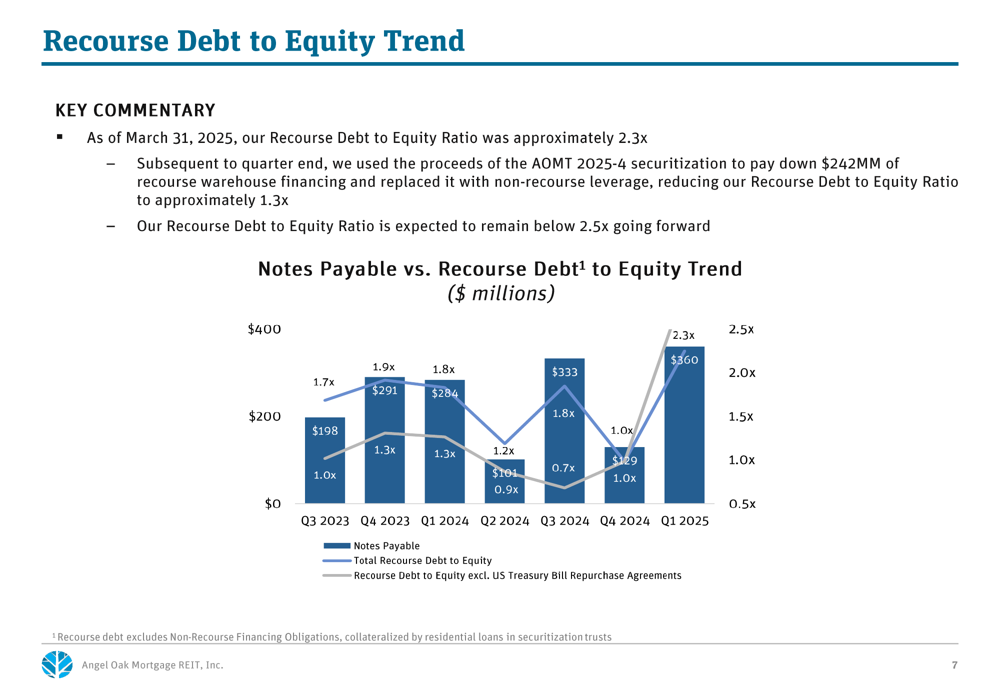

This securitization had a significant positive impact on the company’s leverage profile. As of March 31, 2025, the recourse debt to equity ratio stood at approximately 2.3x. Following the securitization, this ratio was reduced to approximately 1.3x as proceeds were used to pay down $242 million of recourse warehouse financing.

The leverage trend and its improvement are illustrated in this chart:

Competitive Industry Position

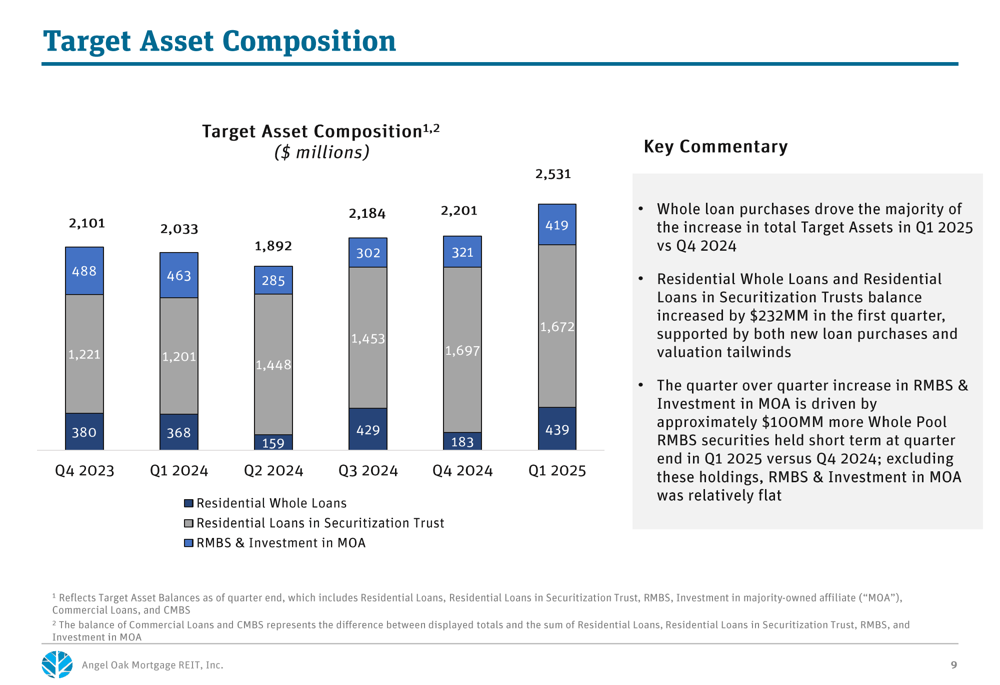

Angel Oak Mortgage has strategically positioned its portfolio to capitalize on opportunities in the non-QM loan market. The company’s target asset composition has evolved over time, with a significant increase in residential whole loans and loans in securitization trusts.

As shown in the following asset composition chart:

Total (EPA:TTEF) target assets increased from $2,101 million in Q4 2023 to $2,531 million in Q1 2025, with whole loan purchases driving the majority of the increase in Q1 2025 compared to Q4 2024. The residential whole loans and residential loans in securitization trusts balance increased by $232 million in the first quarter, supported by both new loan purchases and valuation tailwinds.

Portfolio Quality and Composition

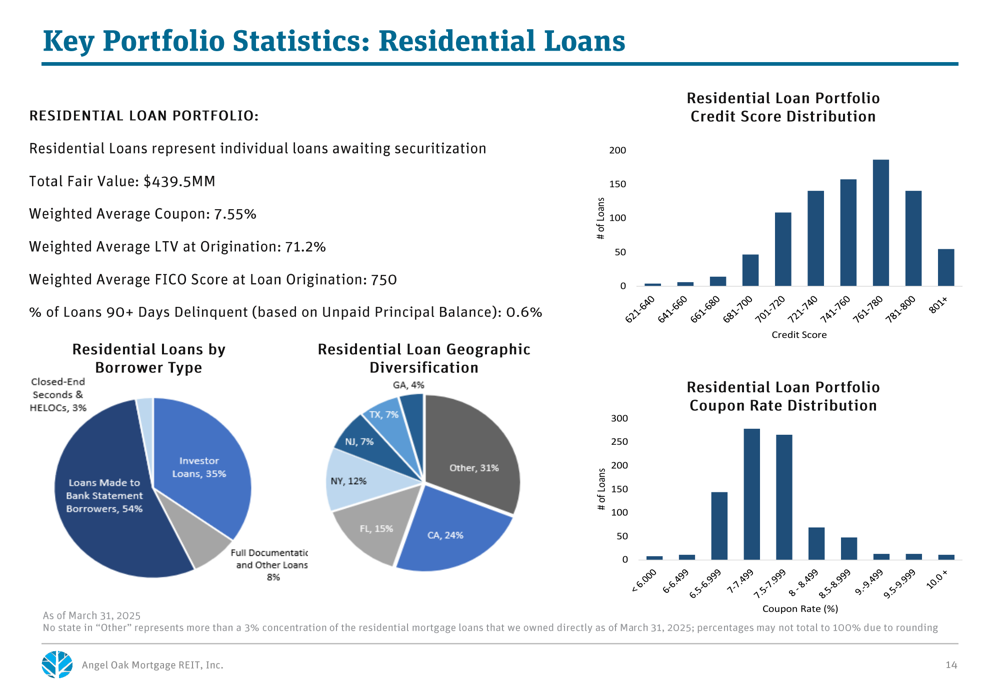

The company maintains a diversified portfolio of high-quality residential loans. As of Q1 2025, the residential loan portfolio had a weighted average coupon of 7.55%, weighted average LTV at origination of 71.2%, and weighted average FICO score at loan origination of 750. Importantly, only 0.6% of loans were 90+ days delinquent.

The portfolio characteristics are detailed in the following chart:

The portfolio shows significant geographic diversification, with California representing 24% of residential loans, followed by Florida (15%), New York (12%), Texas (7%), and New Jersey (7%). By borrower type, 54% of loans were made to bank statement borrowers, 35% were investor loans, 3% were closed-end seconds and HELOCs, and 8% were full documentation and other loans.

For loans in securitization trusts, the company reported a total unpaid principal balance of $1.74 billion across 4,107 loans. These securitized loans had a weighted average loan coupon of 5.55%, weighted average LTV of 67%, and weighted average credit score of 743. The 90+ day delinquency rate for these loans was 1.7% of UPB.

Forward-Looking Statements

Angel Oak Mortgage remains committed to its business model of acquiring predominantly non-QM loans, securitizing them to secure fixed cost of financing, retaining portions of securitizations for enhanced returns, and reinvesting proceeds to continue the cycle. The company targets approximately one securitization per quarter to lock in funding terms and rates and provide capital for additional loan purchases.

Management emphasized its long-term focus, stating that "AOMR is a business, not a trade" and that key decisions will be made in the best long-term interest of shareholders. The company expects the recourse debt to equity ratio to remain below 2.5x going forward, maintaining a conservative leverage profile while pursuing growth opportunities.

Given the company’s strong performance in Q1 2025 and the successful execution of its AOMT 2025-4 securitization in April, Angel Oak Mortgage appears well-positioned to continue its growth trajectory through 2025, with a focus on building book value while maintaining its attractive dividend yield.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.