Walmart halts H-1B visa offers amid Trump’s $100,000 fee increase - Bloomberg

- U.S. jobs report, PMI surveys, Fed speakers will be in focus this week.

- Fortinet is a buy as its annual ‘Accelerate 2024’ event kicks off.

- Tesla is a sell with weak Q1 deliveries expected.

- Looking for more actionable trade ideas? Join InvestingPro for under $9 a month for a limited time only and never miss another bull market by not knowing which stocks to buy!

U.S. stocks ended slightly higher on Thursday to notch another winning week as the S&P 500 closed out its strongest first quarter in five years.

The benchmark index rallied 10.2% in the first three months of the year for its best Q1 gain since 2019. Meanwhile, the blue-chip Dow Jones Industrial Average added 5.6% during the period for its strongest first-quarter performance since 2021.

The tech-heavy Nasdaq Composite ended the quarter with a gain of 9.1%.

Source: Investing.com

The week ahead is expected to be another busy one as the second quarter kicks off and investors continue to gauge the path for the Federal Reserve’s interest rate outlook.

Most important on the economic calendar will be Friday’s U.S. employment report for March, which is forecast to show the economy added 198,000 positions, compared to jobs growth of 275,000 in February. The unemployment rate is seen holding steady at 3.9%.

Ahead of the jobs report, the ISM manufacturing and services PMIs will also be closely watched.

Source: Investing.com

Those releases will be accompanied by a heavy slate of Fed speakers, with the likes of district governors John Williams, Loretta Mester, Mary Daly, and Thomas Barkin set to make public appearances.

Meanwhile, Fed Chairman Jerome Powell will participate in a moderated discussion before Stanford University's Business, Government, and Society Forum on Wednesday.

Traders now see about a 60% chance of the first rate cut hitting in June, according to the Investing.com Fed Monitor Tool, down from over 80% just a few weeks ago.

Regardless of which direction the market goes, below I highlight one stock likely to be in demand and another which could see fresh downside. Remember though, my timeframe is just for the week ahead, Monday, April 1 - Friday, April 5.

Stock to Buy: Fortinet

I expect Fortinet (NASDAQ:FTNT) to outperform this week as the cybersecurity solutions provider hosts its highly anticipated ‘Accelerate 2024’ event, at which it is likely to show off its latest advancements in AI applications.

The four-day conference, titled ‘Step Into the Platform Era’, will kick off on Monday from the Mandalay Bay Convention Center, in Las Vegas.

Most of the spotlight will fall on founder and CEO Ken Xie’s keynote speech scheduled for Tuesday at 12:00PM PDT/9:00AM EST.

According to the description, Xie will showcase cutting-edge strategies and provide invaluable insights into how emerging trends and innovations in modern artificial intelligence are driving transformation in the rapidly evolving digital economy.

Furthermore, other key members of Fortinet’s leadership team are expected to reveal fresh details on the cybersecurity specialist’s intrusion prevention systems and endpoint security components.

Now in its eighth year, shares of Fortinet tend to rally during the week of its annual ‘Accelerate’ event. At its last conference in April 2023, FTNT shares jumped after Xie highlighted new cybersecurity features and functions.

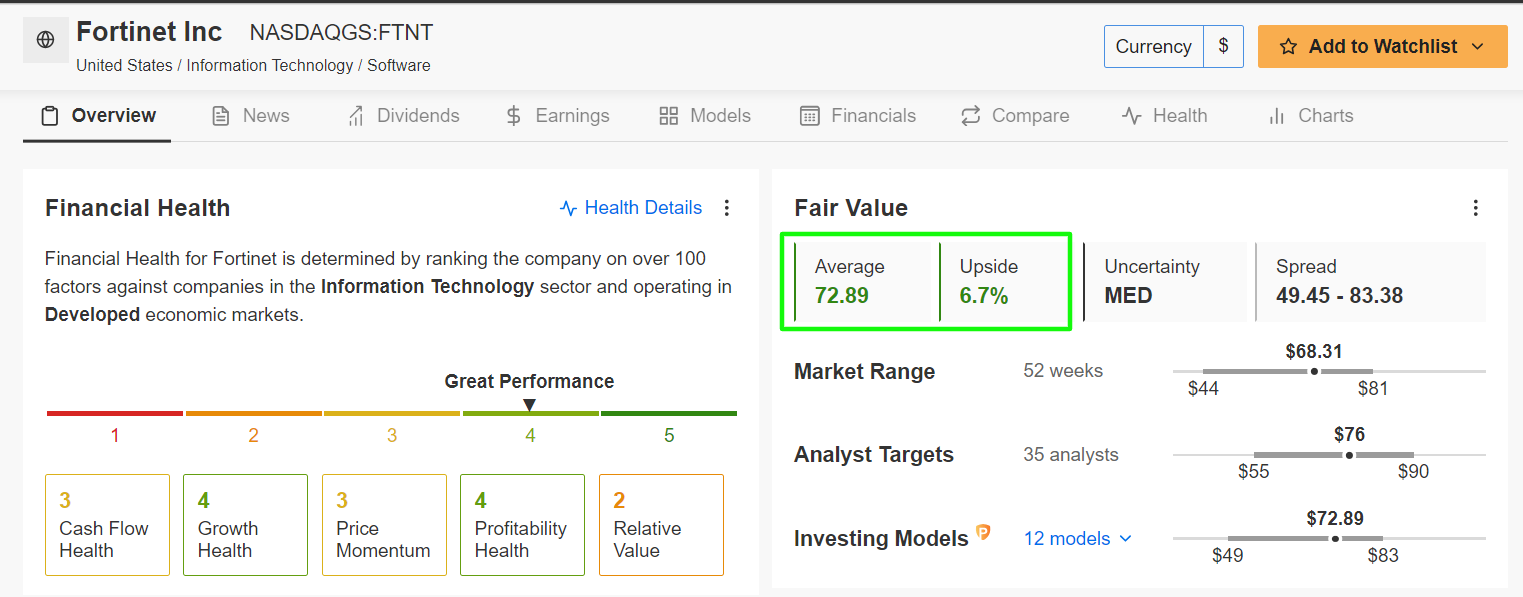

FTNT stock ended Thursday’s session at $68.31, within sight of its 2024 peak of $73.91 reached on February 7. The Sunnyvale, California-based network-security firm has a valuation of $52.1 billion.

Source: Investing.com

Shares have been on a major uptrend since the start of the year, gaining about 17% so far in 2024, as the security-software maker benefits from strong demand from large enterprises for its cloud-based security solutions.

As ProTips points out, Fortinet has a near-perfect Financial Health Score of 4/5, thanks to robust earnings and sales growth prospects.

Source: InvestingPro

It is also worth noting that the quantitative models in InvestingPro point to a potential upside of 6.7% in FTNT stock, which would bring shares closer to their Fair Value price target of about $73.

Stock to Sell: Tesla

I believe Tesla (NASDAQ:TSLA) will suffer a disappointing week ahead, as the struggling electric vehicle maker’s first quarter delivery numbers will likely underwhelm investors due to the negative impact of various headwinds on its business.

Tesla will report Q1 deliveries sometime on Tuesday and results are expected to take a hit from soft demand in China and Europe, as well as production outages at its Shanghai, and Berlin factories.

The Elon Musk-led EV pioneer is expected to have shipped around 457,000 vehicles in the first three months of the year, as per consensus estimates.

However, sell-side sentiment has been extremely bearish in the days leading up to the report, with several analysts - including those at Goldman Sachs, Citibank, and Deutsche Bank - lowering their Q1 estimates for the period to around 420,000 deliveries.

By comparison, Tesla delivered 484,507 vehicles in Q4 and 422,875 in the first quarter of 2023.

Despite its price-slashing strategy and various incentives to customers in the U.S., China, and Europe, Tesla has been struggling with demand concerns and elevated inventory levels amid the current environment.

The ongoing price cuts have fueled concerns that it is having to offer discounts on its vehicles to retain market share in the face of weakening demand and growing competition from traditional legacy automakers as well as Chinese EV startups, such as BYD (SZ:002594), Li Auto (NASDAQ:LI), and Xpeng (NYSE:XPEV).

TSLA stock closed at $175.79 on Thursday, not far from a recent year-to-date low of $160.51 touched on March 14. At its current valuation, the Austin, Texas-based EV giant has a market cap of $560 billion.

Source: Investing.com

It should be noted that Tesla shares plunged 29% in the first quarter to earn the dubious title of the worst performing stock in the S&P 500 during the first three months of 2024.

Tesla is scheduled to report first quarter earnings on April 24. Underscoring several near-term challenges facing Tesla amid the current environment, 12 out of the 13 analysts surveyed by InvestingPro cut their profit estimates in the past 90 days to reflect a drop of roughly 50% from their initial expectations.

Source: InvestingPro

Consensus estimates call for a profit of $0.59 per share, plunging 31% from EPS of $0.85 in the same quarter last year. Revenue is forecast to increase less than 4% annually to $24.19 billion.

Be sure to check out InvestingPro to stay in sync with the market trend and what it means for your trading.

Readers of this article enjoy an extra 10% discount on the yearly and bi-yearly plans with the coupon codes PROTIPS2024 (yearly) and PROTIPS20242 (bi-yearly).

Subscribe here and never miss a bull market again!

Disclosure: At the time of writing, I am long on the S&P 500, and the Nasdaq 100 via the SPDR S&P 500 ETF (SPY), and the Invesco QQQ Trust ETF (QQQ). I am also long on the Technology Select Sector SPDR ETF (NYSE:XLK).

I regularly rebalance my portfolio of individual stocks and ETFs based on ongoing risk assessment of both the macroeconomic environment and companies' financials.

The views discussed in this article are solely the opinion of the author and should not be taken as investment advice.