BofA sees higher gold prices, likely to hit $5,000/oz in 2026

US consumer confidence dipped again and remains on par with where we were during the pandemic. Concerns about the potential for tariff-induced price rises, a rapidly cooling jobs market and uncertainties over wealth are all having an influence and point to subdued consumer spending growth over the coming months.

Sentiment Resumes Its Slide

The October Conference Board measure of US consumer confidence dropped to 94.6 from an upwardly revised 95.6 print for September. The size of the dip was in line with the consensus survey.

The details show a decent pick-up in perceptions surrounding current conditions to 129.3 from 127.5, which likely reflects a combination of stronger stock markets and falling gasoline prices, but the expectations component fell from 74.4 to 71.5. This measure is the more useful indicator as it has had a decent relationship with consumer spending growth over the last few decades. It is currently consistent with annualised spending growth of about 1-1.5%. That’s not terrible, but is well short of what we have experienced since the end of the pandemic.

It’s likely that lingering anxiety about the potential for tariff-induced price hikes and a cooling of the jobs market are the main drivers of this softer outcome.

Job Perceptions Remain Weak

The "plentiful" vs "hard to get" jobs metric was little changed and continues to suggest upside risks for the unemployment rate. The premise being that workers see and feel changes in the jobs market before they show up in the official data – not that we are going to get another jobs report for a while, given the government shutdown. All in all, nothing here to argue against a 25bp Federal Reserve rate cut tomorrow.

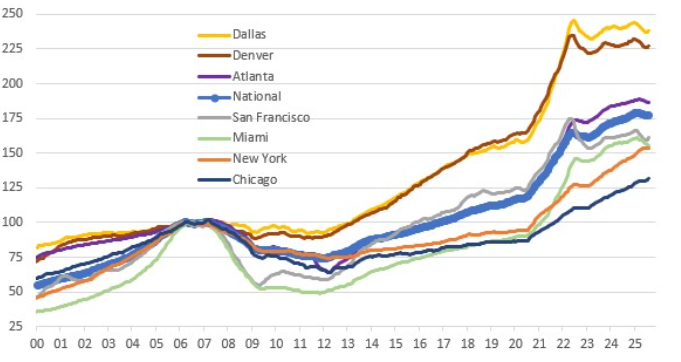

House Prices Buck the Downward Trend, but Challenges Linger

The other data report from earlier was the S&P Case Shiller US house price index, which snapped a five-month falling streak and rose 0.2% month-on-month in August. Expectations had been for a sixth consecutive monthly drop based on a lack of affordability due to elevated prices and high mortgage rates constraining demand, coming up against rising supply of homes for sale.

To highlight this, based on the median-sized mortgage for a home purchase taken out last week of $438,900 on a 30Y fixed mortgage at 6.37%, this works out at a monthly payment of $2,764, which is equivalent to 47% of median after-tax incomes in the US.

Source: Macrobond, ING

Today’s outcome leaves national house prices 1.5% higher than a year ago. Chicago is seeing the strongest gains right now (up 0.6% MoM/5.3% three-month annualised), with Minneapolis in second place (0.35% MoM/3.7% 3M ann.), but they had lagged well behind most markets over the previous five years.

Phoenix, Miami and Las Vegas are the weakest, seeing prices fall 0.5-0.6% MoM, leaving the 3M annualised rates in a -8 to -10% range. The chart above is of house price levels rebased to 2006 = 100 to show how different markets have performed.

***

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more