Futures lower; Tesla’s much-anticipated announcement - what’s moving markets

Introduction & Executive Summary

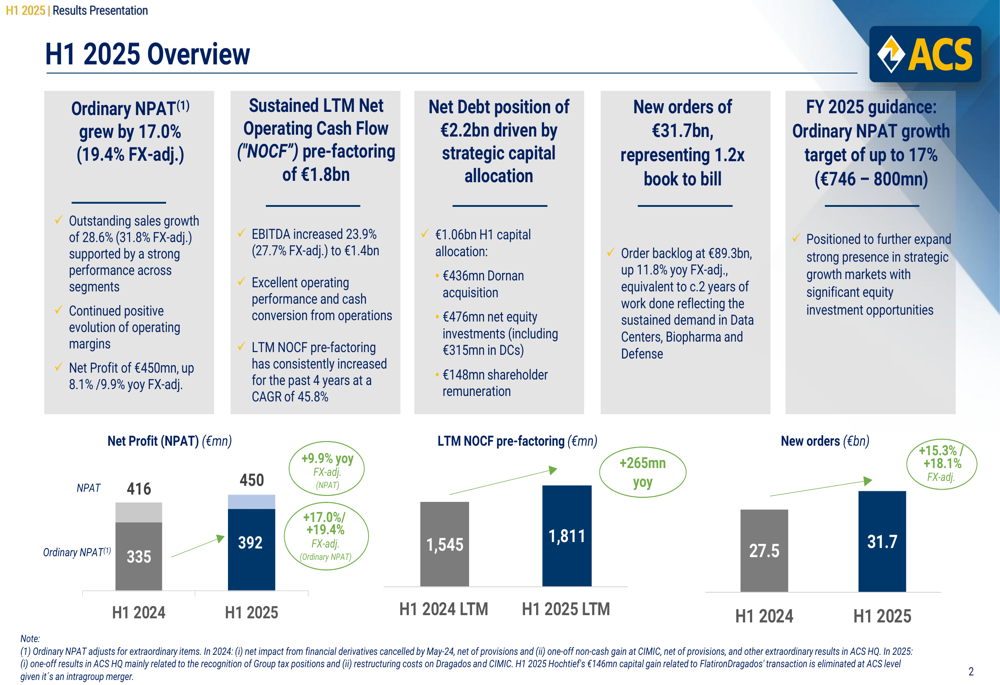

ACS Group (BME:ACS) reported robust financial results for the first half of 2025, with ordinary net profit growing 17.0% year-over-year to €392 million, according to the company’s presentation on July 30, 2025. The construction and infrastructure giant saw sales surge 28.6% to €24.1 billion, driven by exceptional performance in its Turner segment and strategic investments in high-growth sectors.

The company maintained its full-year 2025 guidance, targeting ordinary net profit growth of up to 17% to reach between €746-800 million. This performance builds upon the strong momentum seen in Q1 2025, when the company reported a 17.2% increase in net profit to €191 million.

As shown in the following overview of key financial metrics, ACS demonstrated growth across most performance indicators while continuing to build its order backlog:

Quarterly Performance Highlights

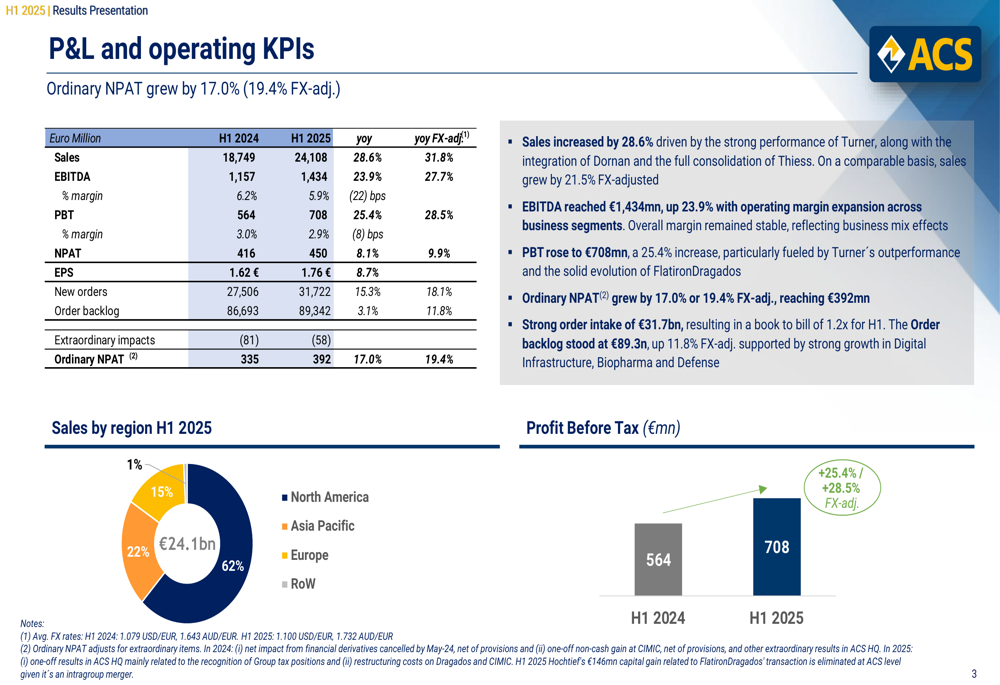

ACS delivered impressive financial results in H1 2025, with sales reaching €24.1 billion, representing a 28.6% increase (31.8% FX-adjusted) compared to the same period last year. EBITDA grew 23.9% to €1.43 billion, while profit before tax increased 25.4% to €708 million.

The company’s ordinary net profit, which excludes extraordinary items, rose 17.0% (19.4% FX-adjusted) to €392 million. This growth trajectory aligns with the company’s Q1 performance and supports its full-year guidance.

The detailed profit and loss statement reveals strong performance across key metrics, with particularly robust growth in the North American market:

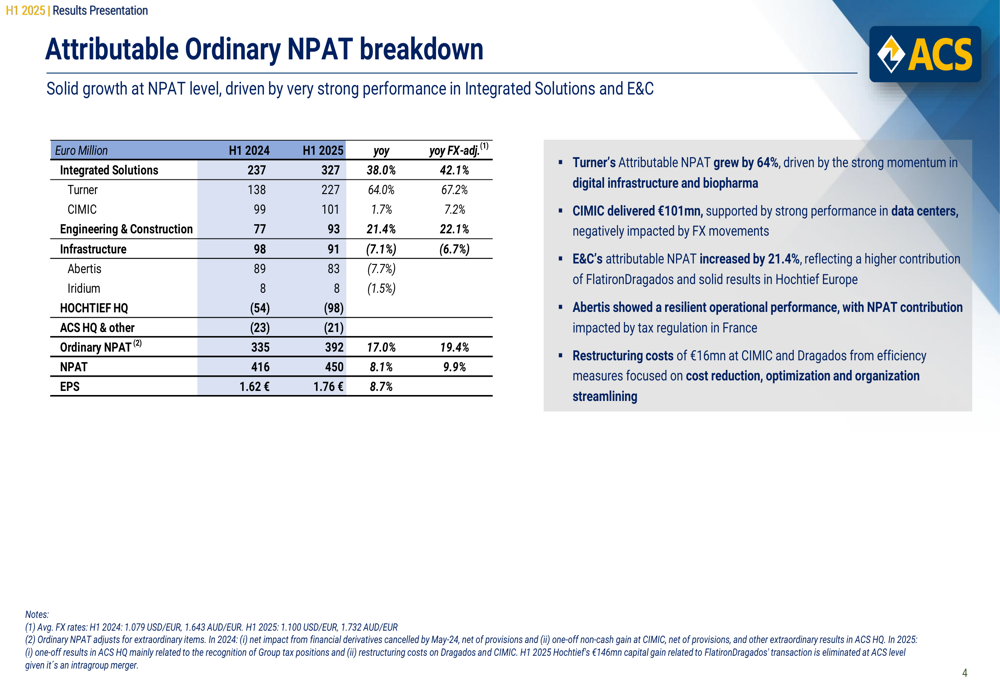

Breaking down the attributable ordinary net profit by segment shows varied performance across the company’s divisions. The Integrated Solutions segment, particularly Turner, delivered exceptional results with a 64.0% increase in attributable NPAT. The Engineering & Construction segment also performed well with 21.4% growth, while the Infrastructure segment experienced a slight decline of 7.1%.

Cash Flow and Financial Position

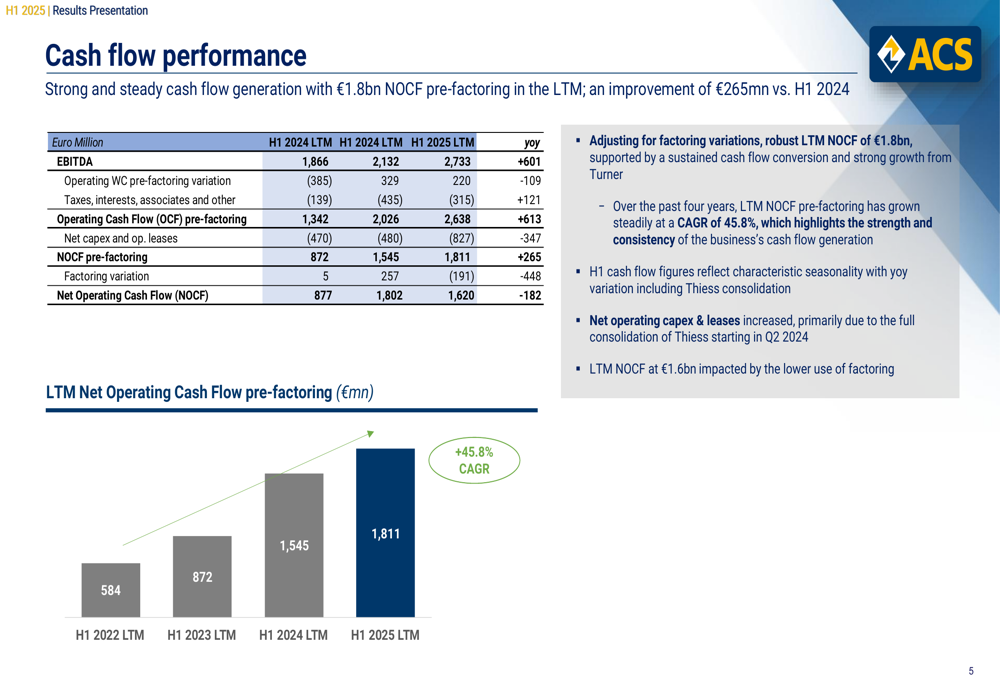

ACS maintained strong cash flow generation with €1.8 billion in net operating cash flow pre-factoring over the last twelve months, representing an improvement of €265 million compared to H1 2024. This sustained cash flow performance provides the company with financial flexibility to pursue its strategic initiatives.

The following chart illustrates the company’s consistent improvement in cash flow generation over recent years:

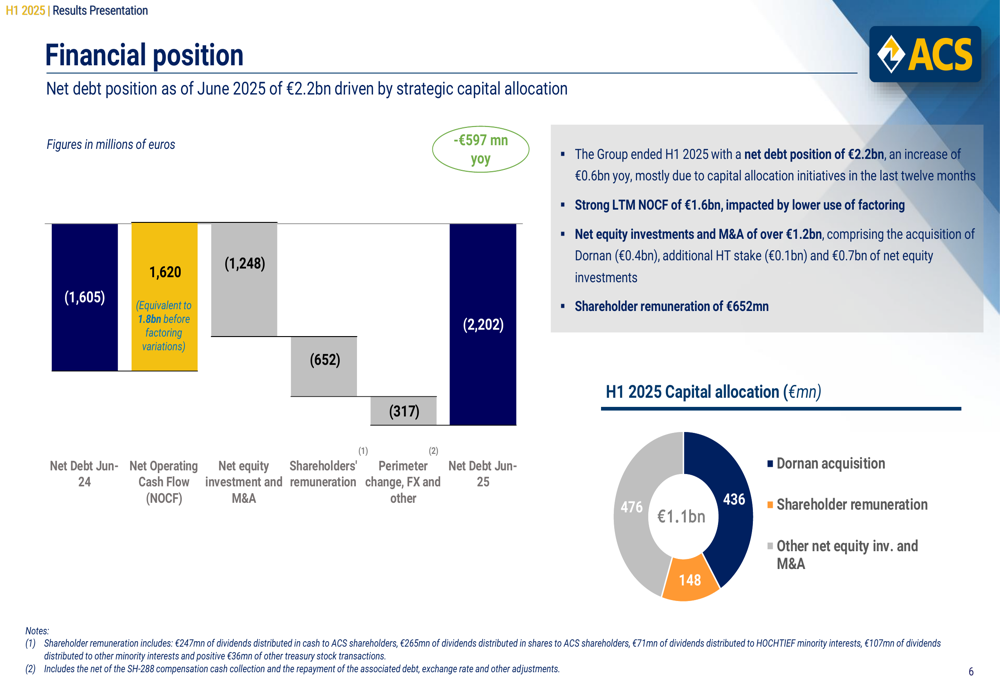

The company’s net debt position increased to €2.2 billion as of June 2025, primarily driven by strategic capital allocation decisions. This represents an increase from the €1.6 billion reported at the end of June 2024, but remains below the €2.8 billion reported in Q1 2025, suggesting some debt reduction during Q2.

Major capital allocation during H1 2025 included €436 million for the Dornan acquisition, €476 million for shareholder remuneration, and €148 million for other net equity investments and M&A activities, totaling approximately €1.1 billion.

Order Backlog and Growth Markets

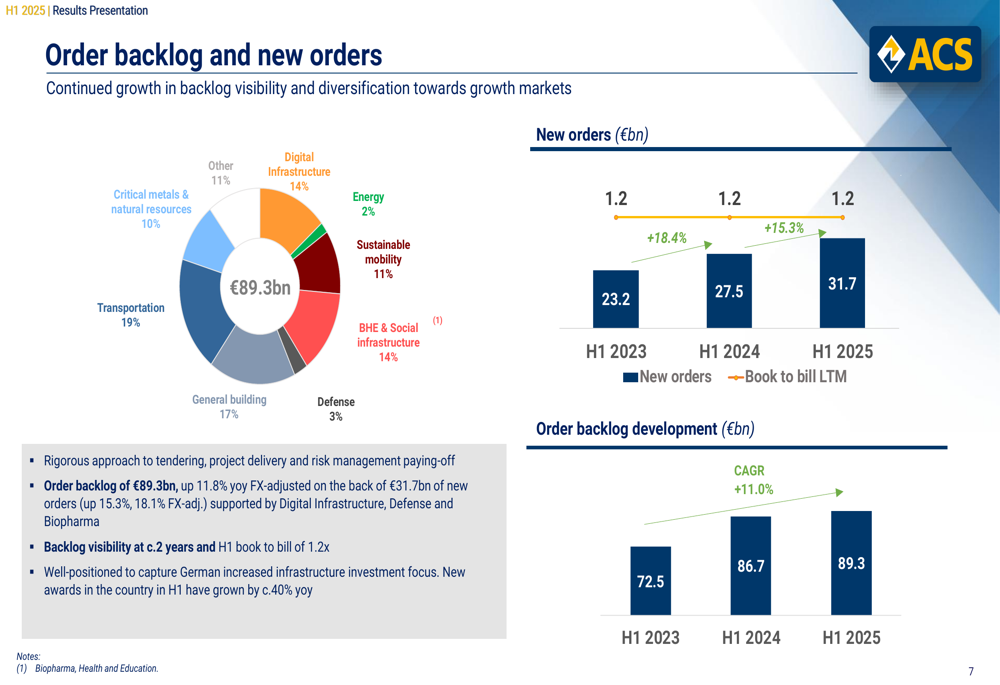

ACS reported new orders of €31.7 billion in H1 2025, representing a 15.3% increase year-over-year and a book-to-bill ratio of 1.2x. The company’s order backlog stood at €89.3 billion, up 3.1% (11.8% FX-adjusted) compared to H1 2024. This represents a slight decrease from the €90.8 billion reported in Q1 2025.

The company’s backlog is increasingly diversified toward growth markets, with significant exposure to transportation (19%), general building (17%), digital infrastructure (14%), and social infrastructure (14%). This strategic positioning aligns with the company’s focus on high-growth sectors.

Recent significant new orders span multiple sectors, including energy infrastructure projects, data centers in various locations including Lancaster, Melbourne, and Louisiana, critical metals and natural resources projects, transport infrastructure, and social infrastructure developments.

Segment Performance Analysis

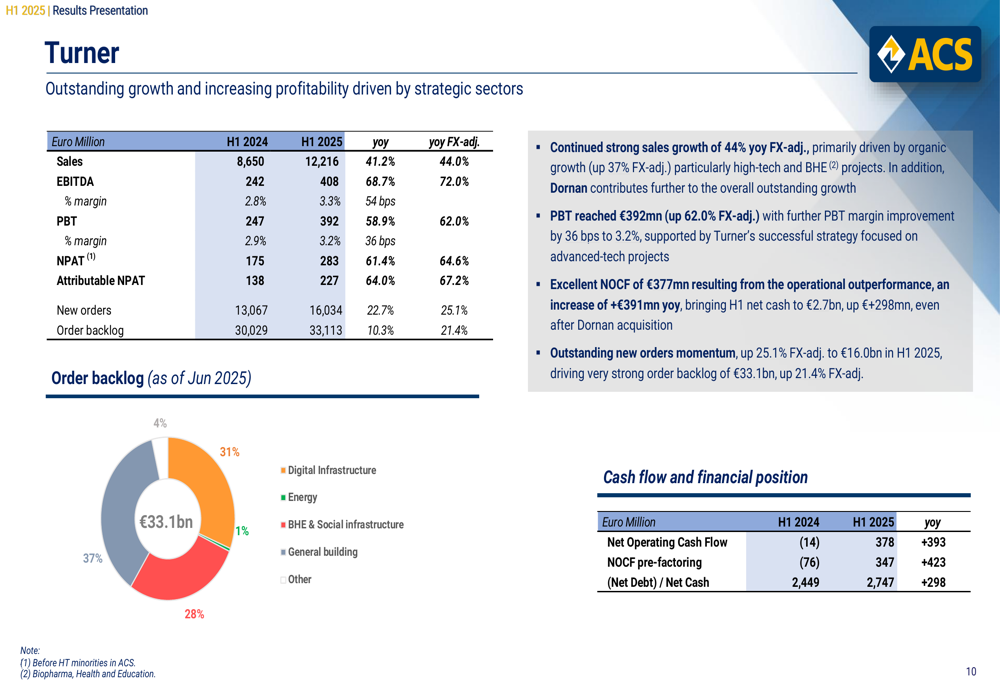

Turner, part of the Integrated Solutions segment, delivered outstanding growth with sales increasing 41.2% to €12.2 billion and attributable net profit surging 64.0% to €227 million. This exceptional performance was driven by strategic sectors, particularly in digital infrastructure, which represents 31% of Turner’s €33.1 billion order backlog.

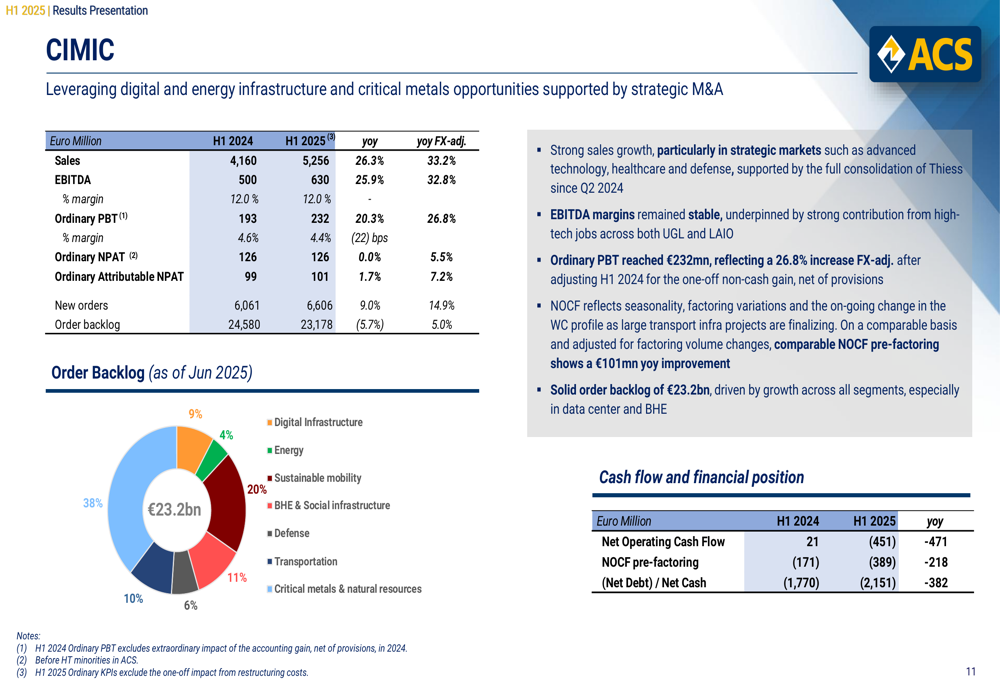

CIMIC, also part of the Integrated Solutions segment, reported sales growth of 26.3% to €5.3 billion, leveraging opportunities in digital and energy infrastructure and critical metals. However, ordinary attributable net profit showed more modest growth of 1.7% (7.2% FX-adjusted) to €101 million.

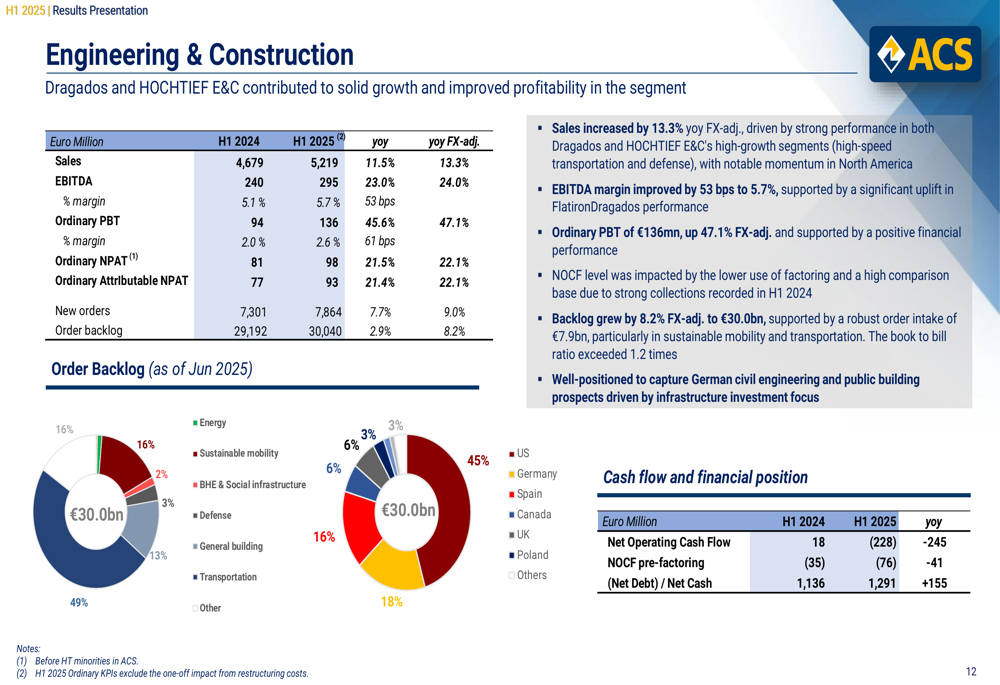

The Engineering & Construction segment, comprising Dragados and HOCHTIEF E&C, contributed to solid growth with sales increasing 11.5% to €5.2 billion and ordinary attributable net profit rising 21.4% to €93 million. The segment’s order backlog of €30.0 billion is well-diversified across regions and sectors, with significant exposure to transportation (49%) and energy (16%).

Strategic Initiatives and Outlook

ACS continues to focus on strategic growth initiatives, particularly in data centers and infrastructure investments. The company highlighted its capital allocation priorities, including significant greenfield infrastructure investment opportunities in data centers and managed lanes in the US, strategic M&A in brownfield core infrastructure, and bolt-on acquisitions to enhance engineering capabilities.

The company’s SR-400 project in Georgia represents a significant milestone as the first privately managed express lane project in the state, with a construction value of $4.6 billion and an estimated concession fee of $4.1 billion. ACS holds a 33.33% equity stake in the project.

Looking ahead, ACS maintains its full-year 2025 guidance of up to 17% growth in ordinary net profit, supported by its robust order backlog and strategic positioning in high-growth markets. The company’s focus on data centers aligns with statements made during its Q1 earnings call, where management highlighted plans to invest an additional €300 million in data centers in 2025.

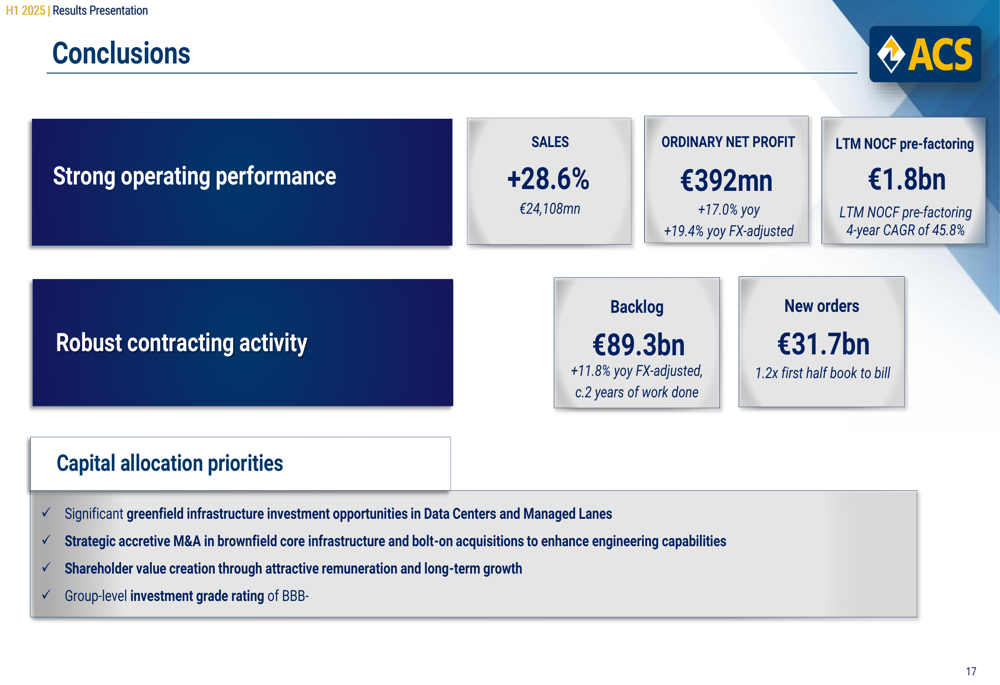

As summarized in the company’s conclusion slide, ACS is well-positioned for continued growth with strong operating performance, robust contracting activity, and clear capital allocation priorities:

With its diversified business model, strong cash flow generation, and strategic focus on high-growth sectors, ACS appears well-positioned to deliver on its 2025 targets despite the increased debt position resulting from its strategic investments and acquisitions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.