SoFi stock falls after announcing $1.5B public offering of common stock

Introduction & Market Context

Actic Group AB (ATIC) released its second quarter 2025 results on July 16, showing substantial improvements in profitability and financial position despite a reduction in the number of facilities. The fitness center operator’s stock closed at 25.7 SEK on July 15, 2025, with a slight decrease of 0.1 SEK (-0.39%) ahead of the earnings release.

The company’s strategic divestment of twelve Norwegian facilities has significantly strengthened its financial position while allowing it to focus on core markets. This move comes as the fitness industry continues to recover from pandemic-related disruptions, with companies streamlining operations and enhancing member experiences.

Quarterly Performance Highlights

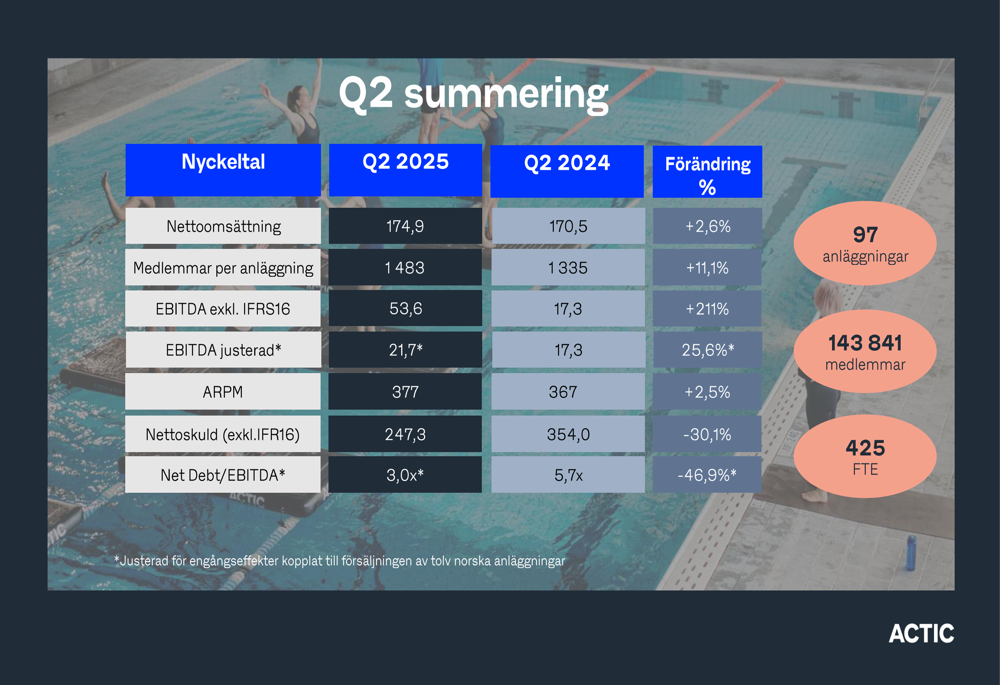

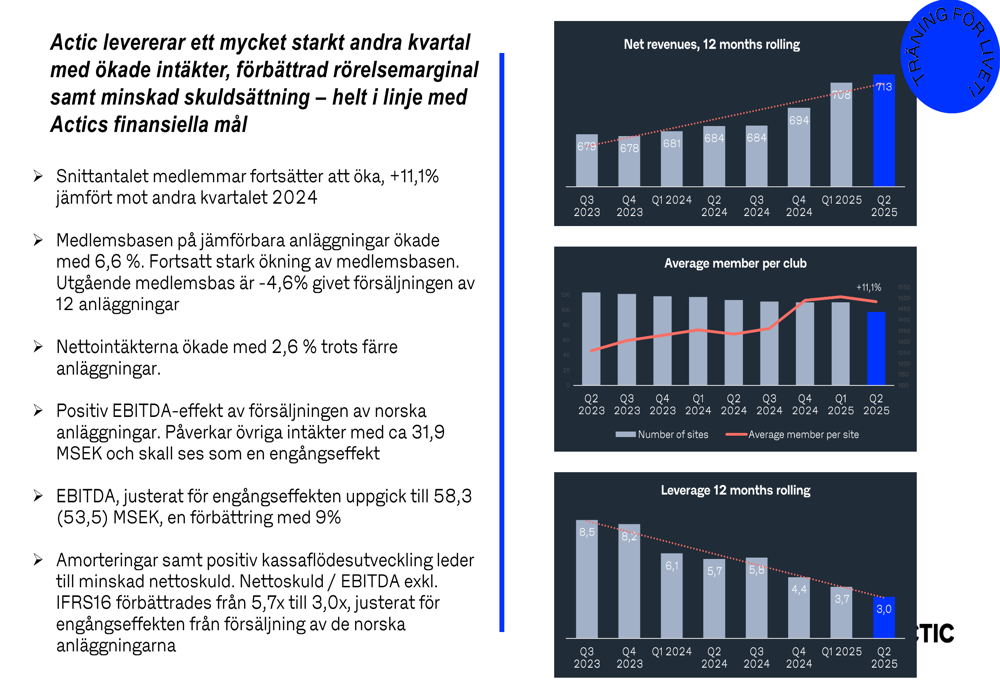

Actic reported net sales of 174.9 million SEK for Q2 2025, representing a 2.6% increase compared to 170.5 million SEK in Q2 2024, despite operating fewer facilities. This growth was primarily driven by an 11.1% increase in members per facility, reaching 1,483 compared to 1,335 in the same period last year.

The company’s EBITDA (excluding IFRS16) saw a dramatic improvement, reaching 53.6 million SEK, a 211% increase from 17.3 million SEK in Q2 2024. However, this figure includes a one-time effect of approximately 31.9 million SEK from the sale of Norwegian facilities. When adjusted for this one-time effect, EBITDA still showed a healthy 25.6% improvement.

As shown in the following key figures summary:

Average Revenue Per Member (ARPM) increased by 2.5% to 377 SEK, indicating Actic’s ability to maintain pricing power while growing its membership base. The company now operates 97 facilities with a total of 143,841 members after the Norwegian divestment.

Detailed Financial Analysis

Actic’s financial position improved substantially during the quarter, with net debt (excluding IFRS16) decreasing by 30.1% to 247.3 million SEK compared to 354.0 million SEK in Q2 2024. This reduction, combined with improved EBITDA, resulted in a significant improvement in the Net Debt/EBITDA ratio, which fell from 5.7x to 3.0x, representing a 46.9% improvement.

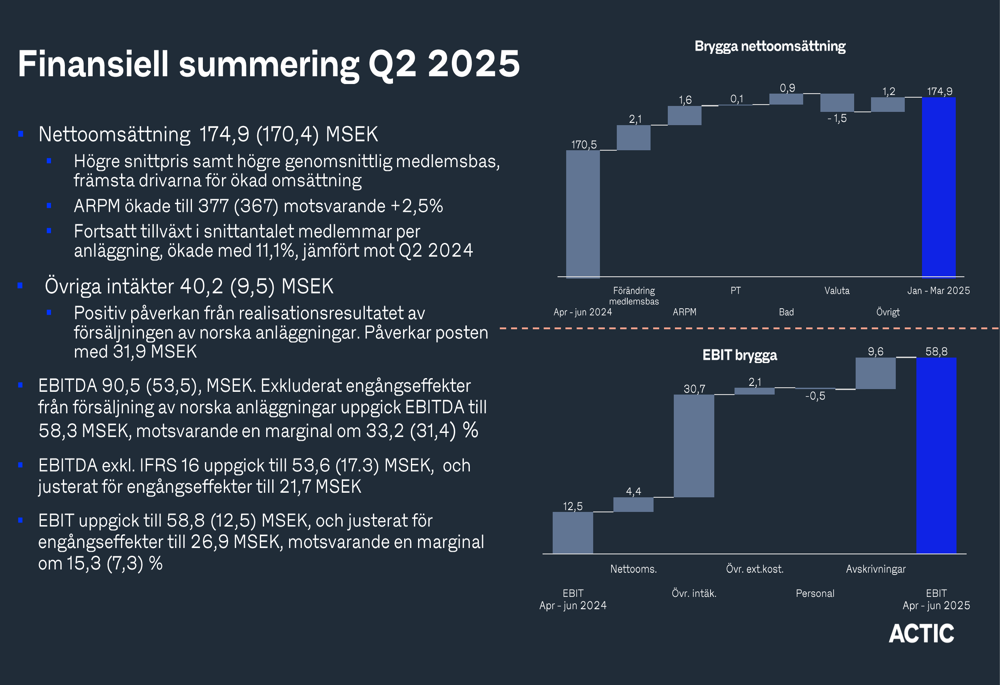

The company’s cash flow from operating activities reached 77.1 million SEK, compared to 25.1 million SEK in Q2 2024. After investments of -3.1 million SEK and loan amortization of -38.2 million SEK, Q2 cash flow was positive at 5.3 million SEK, a significant improvement from -16.9 million SEK in the same period last year.

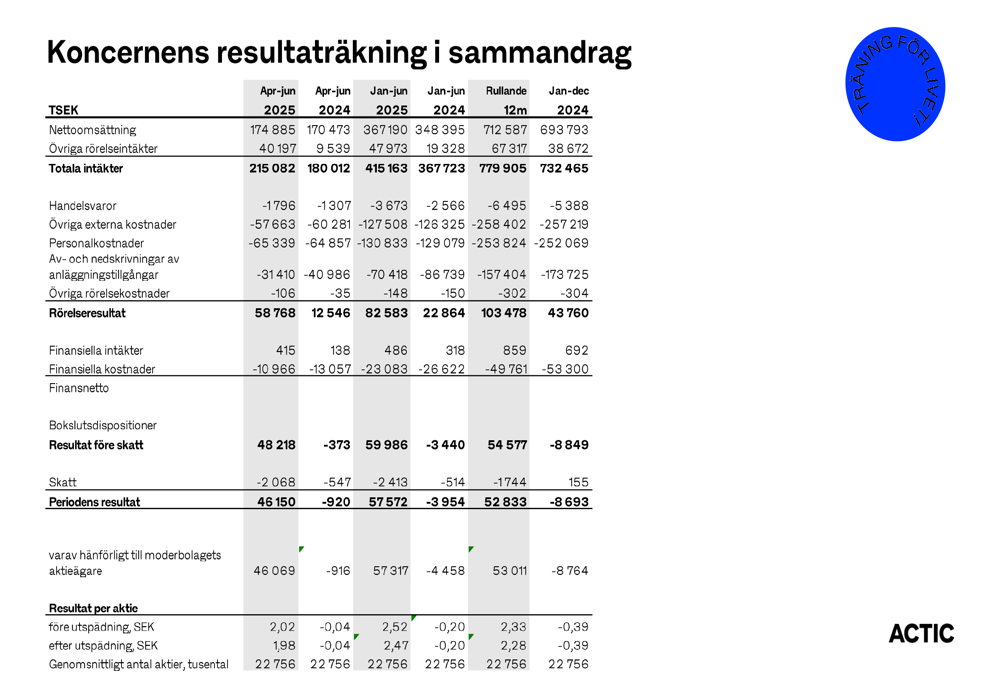

The following financial summary provides a detailed breakdown of revenue and EBIT development:

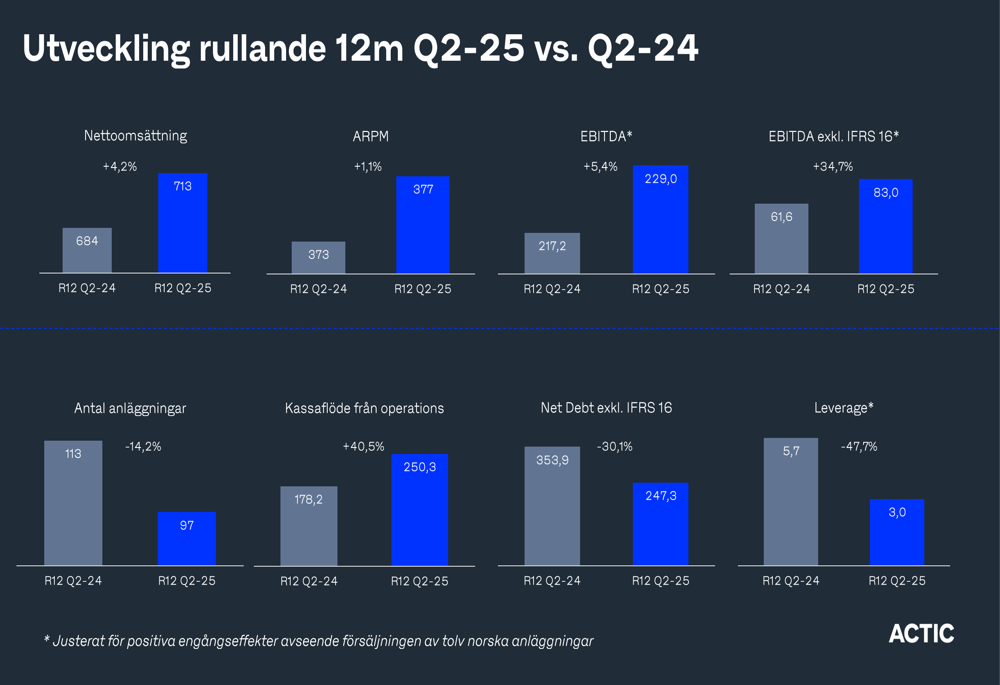

On a rolling 12-month basis, Actic’s key indicators show consistent improvement across most metrics, with net sales up 4.2% and adjusted EBITDA increasing by 5.4% despite a 14.2% reduction in the number of facilities:

Cash flow from operations showed particularly strong growth on a rolling 12-month basis, increasing by 40.5% to 250.3 million SEK, while net debt decreased by 30.1%, reflecting the company’s improved financial discipline and operational efficiency.

Strategic Initiatives

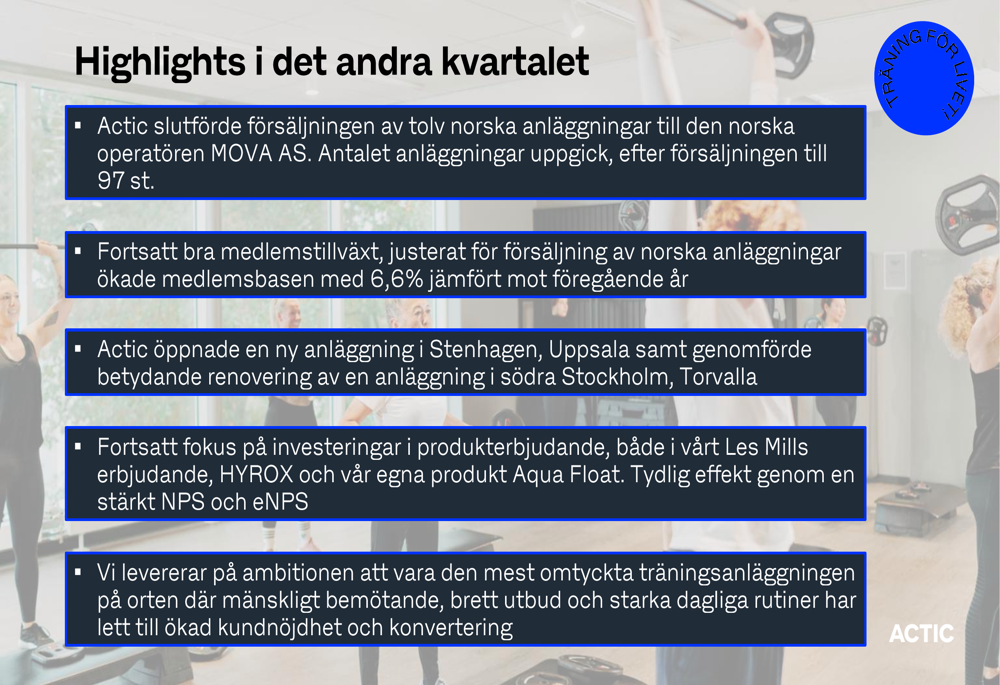

During Q2 2025, Actic completed several strategic initiatives aimed at strengthening its market position and enhancing customer experience. The company opened a new facility in Stenhagen, Uppsala, and completed a significant renovation in Torvalla, Stockholm, demonstrating its commitment to maintaining high-quality facilities.

As highlighted in the quarterly presentation:

The company continues to invest in expanding its product offerings, including Les Mills, HYROX, and Aqua Float, which has contributed to strengthened Net Promoter Scores (NPS) and Employee Net Promoter Scores (eNPS). These investments align with Actic’s strategy of being the most popular training facility in its locations, with an emphasis on human interaction and a broad range of offerings.

Actic’s focus on strong daily routines has also been driving customer satisfaction and conversion rates, as illustrated in the performance metrics:

Forward-Looking Statements

Looking ahead, Actic appears well-positioned to continue its positive trajectory, with a stronger balance sheet and improved operational metrics. The company’s strategic focus on being the preferred training facility in its locations, combined with its investment in product offerings and facility improvements, suggests a continued emphasis on quality over quantity.

The reduction in leverage to 3.0x (from 5.7x a year ago) provides Actic with greater financial flexibility, potentially enabling future strategic investments or further debt reduction. Without the one-time effect from the Norwegian divestment, the company noted that leverage would have been even lower at 2.2x.

The consistent growth in membership per facility (+11.1%) and ARPM (+2.5%) indicates that Actic’s value proposition remains strong, with customers willing to pay premium prices for quality fitness experiences. This trend, if maintained, should support continued revenue and profit growth despite the reduced facility count.

The company’s consolidated income statement provides additional context for assessing future performance:

With its streamlined operations, improved financial position, and continued focus on enhancing customer experience, Actic appears to be executing a strategy that balances growth with financial discipline, positioning the company for sustainable long-term performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.