German construction sector still in recession, civil engineering only bright spot

Adeia Inc (NASDAQ:ADEA) reported its second-quarter 2025 results on August 5, showing a sequential revenue decline while maintaining its full-year guidance. The intellectual property licensing company posted $85.7 million in revenue and introduced new cooling technology for semiconductors amid ongoing efforts to expand its licensing business.

Quarterly Performance Highlights

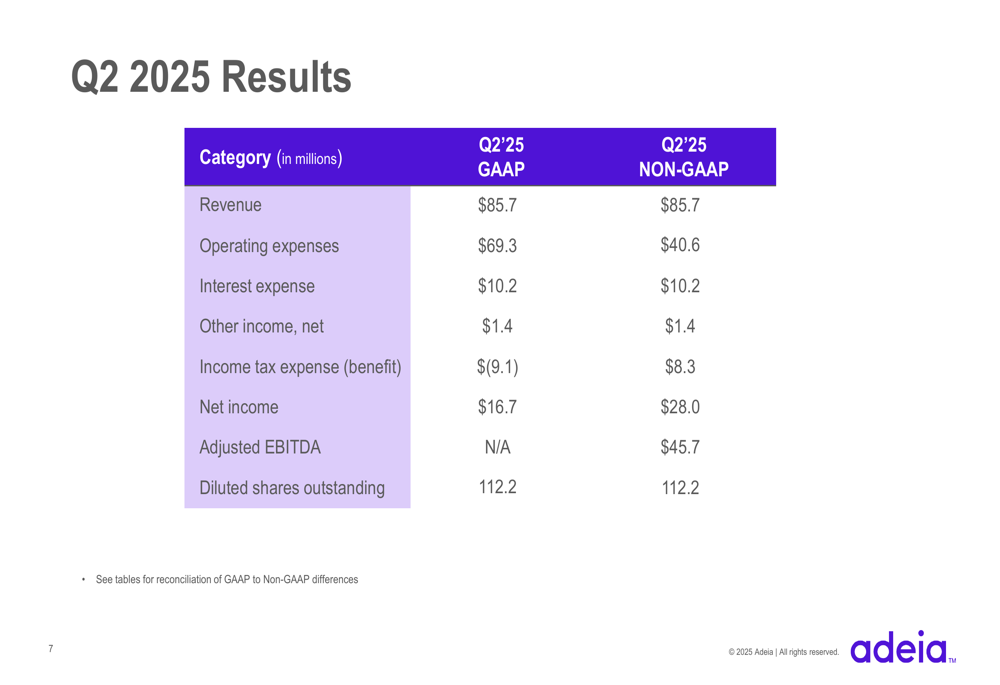

Adeia generated $85.7 million in revenue during Q2 2025, representing a slight decline from the $87.7 million reported in the previous quarter. The company produced $23.1 million in cash from operations and reported net income of $16.7 million under GAAP accounting standards and $28.0 million on a non-GAAP basis.

As shown in the following financial results slide, Adeia achieved an adjusted EBITDA of $45.7 million for the quarter:

The Q2 results continue a challenging trend for Adeia, which missed both EPS and revenue expectations in Q1 2025. The company’s stock closed at $12.39 on the day of the earnings release, up 0.81% but still trading well below its 52-week high of $17.46.

Despite the sequential revenue decline, Adeia highlighted several business achievements during the quarter:

Strategic Initiatives

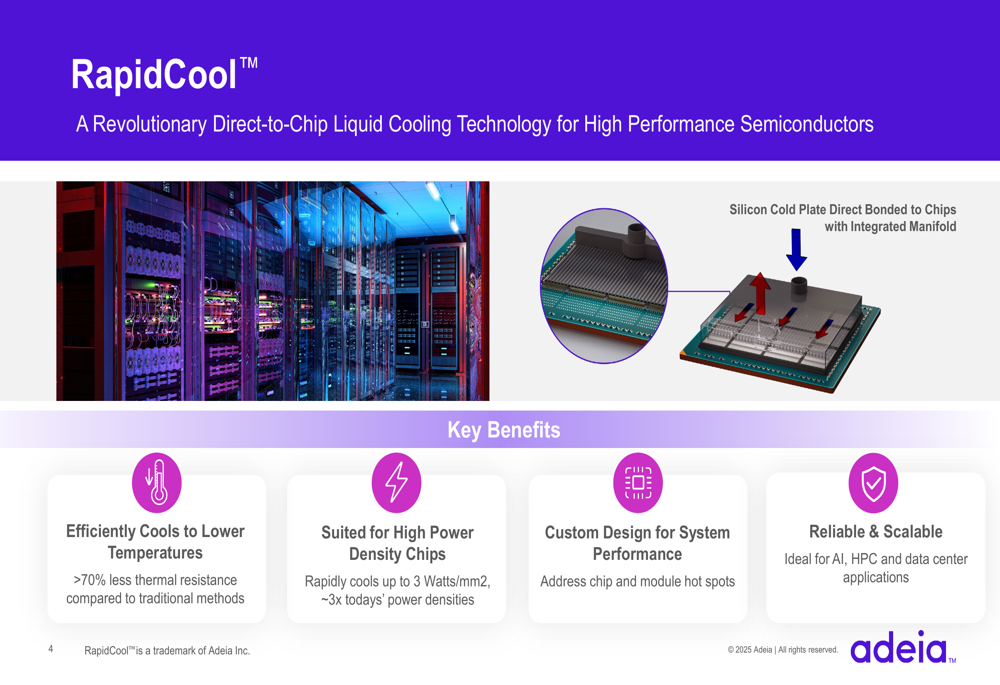

A key development during the quarter was the introduction of RapidCool™, a direct-to-chip liquid cooling technology designed for high-performance semiconductors. This innovation addresses growing thermal management challenges in AI, high-performance computing, and data center applications.

The technology offers significant advantages over traditional cooling methods, as illustrated in the presentation:

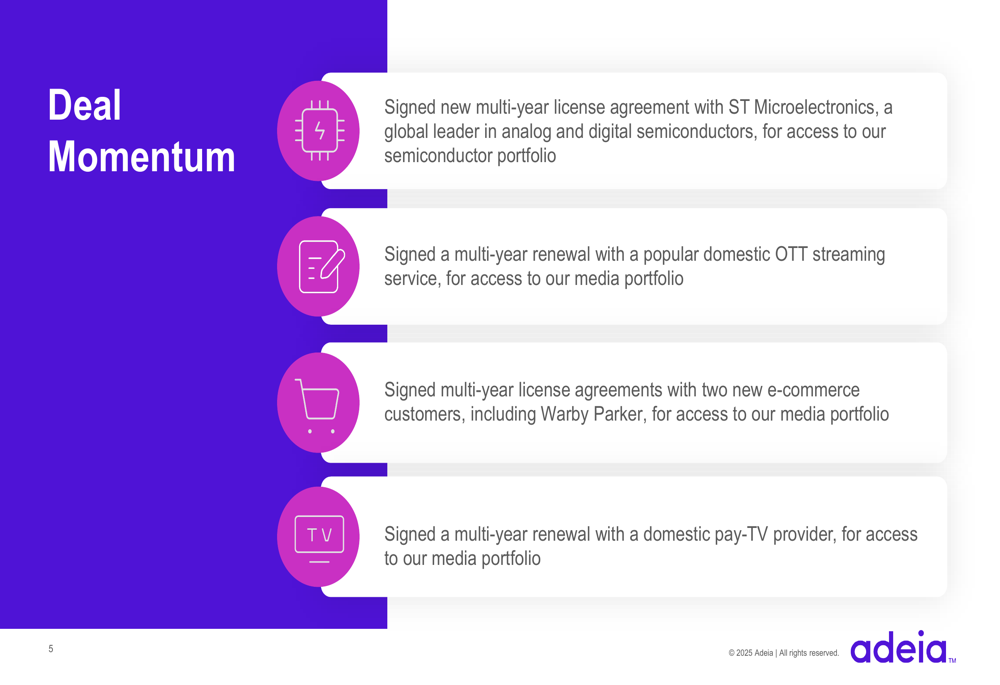

On the licensing front, Adeia signed five new agreements across multiple sectors, including three with new customers. The company specifically highlighted a multi-year agreement with ST Microelectronics for access to its semiconductor portfolio, and new e-commerce deals including one with Warby Parker (NYSE:WRBY).

The company continues to emphasize its balanced approach to capital allocation, focusing on debt reduction, shareholder returns, and strategic acquisitions to strengthen its intellectual property portfolio.

Forward-Looking Statements

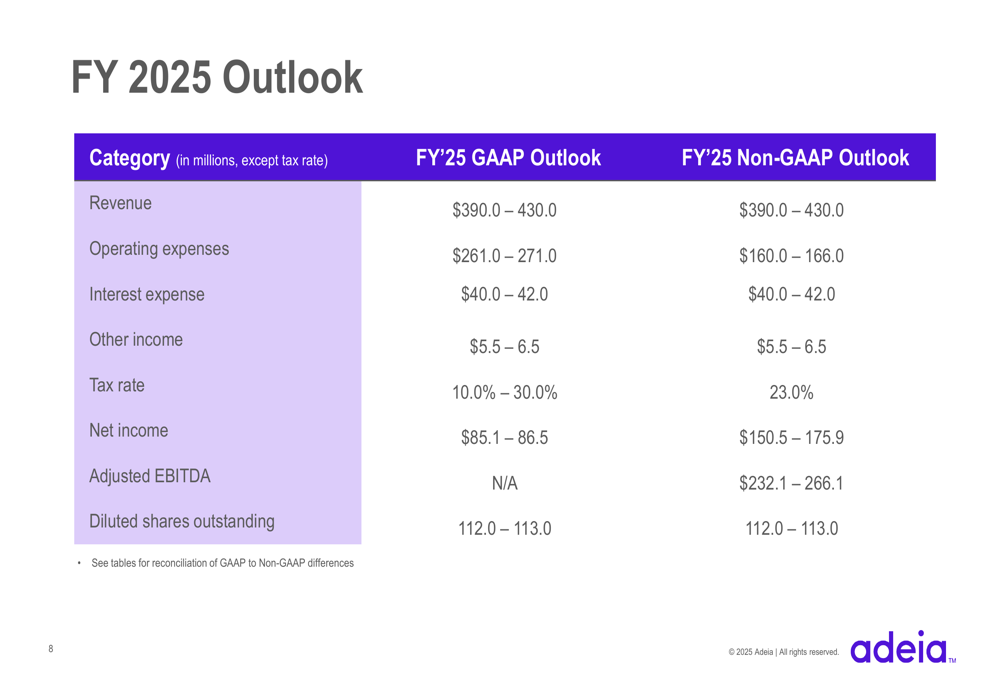

Despite the sequential revenue decline in Q2, Adeia maintained its full-year 2025 guidance, projecting revenue between $390 million and $430 million. The company expects adjusted EBITDA between $232.1 million and $266.1 million for the fiscal year.

This outlook aligns with previous guidance provided after Q1 results, suggesting management remains confident in its ability to accelerate revenue in the second half of the year. The company’s patent portfolio, now exceeding 13,000 assets, continues to be the foundation for its licensing business.

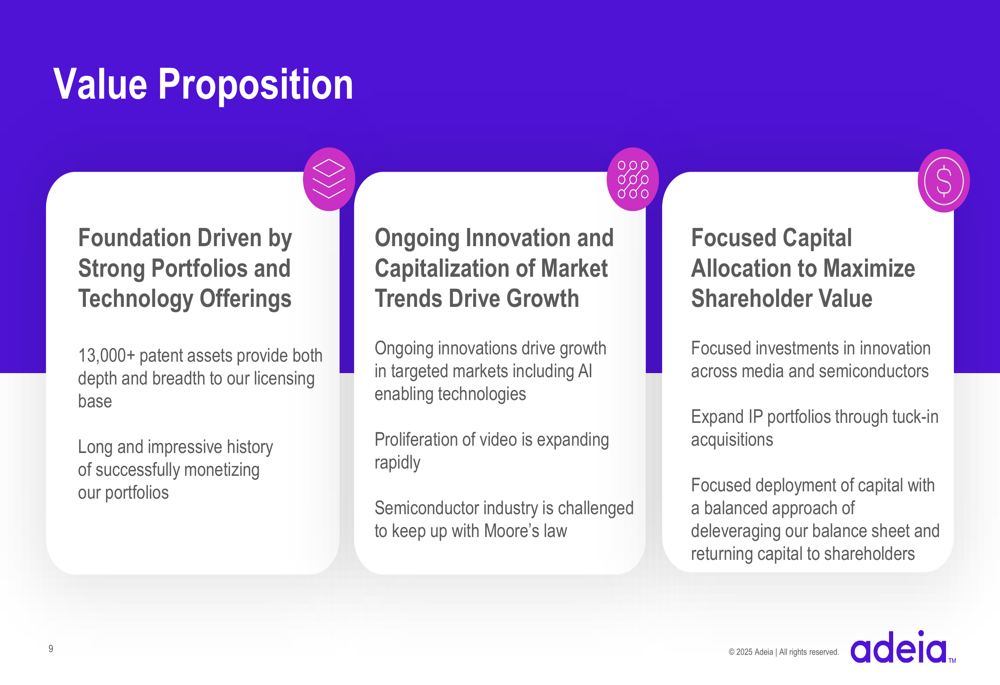

Competitive Industry Position

Adeia emphasized its value proposition as centered around strong patent portfolios and ongoing innovation in high-growth markets:

The company highlighted three strategic pillars: leveraging its extensive patent portfolio, capitalizing on market trends including AI and video proliferation, and maintaining a disciplined capital allocation approach to maximize shareholder value.

Adeia faces ongoing challenges in monetizing its intellectual property in competitive markets, particularly as it attempts to recover from its Q1 earnings miss. However, the introduction of RapidCool technology demonstrates the company’s continued focus on innovation in the semiconductor space, potentially opening new revenue streams beyond pure licensing.

With the stock trading closer to its 52-week low than high, investors will be watching closely to see if Adeia can deliver on its maintained full-year guidance, which would require significant revenue acceleration in the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.