Trump announces trade deal with EU following months of negotiations

Introduction & Market Context

Archer-Daniels-Midland Company (NYSE:ADM) reported a steep decline in first-quarter 2025 earnings during its May 6 conference call, as challenging market conditions and policy uncertainties weighed heavily on the agricultural commodities giant. The company’s shares traded down 1.54% in premarket trading at $46.77, extending recent weakness that has seen the stock trade near its 52-week low of $40.98.

The agricultural processing company’s quarterly results reflect significant headwinds across most business segments, particularly in its core Ag Services & Oilseeds division, where operating profits were cut in half compared to the prior year. Management emphasized its "self-help" strategy focused on cost reduction, simplification, and capital discipline to navigate the challenging environment.

Quarterly Performance Highlights

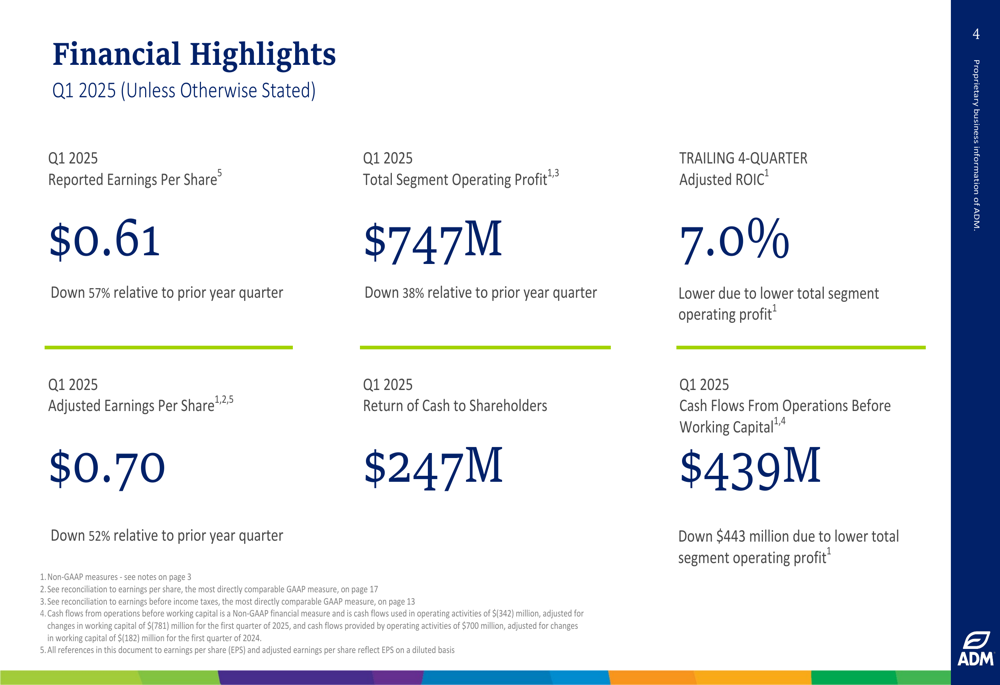

ADM reported first-quarter earnings per share of $0.61, down 57% compared to the same period last year. Adjusted EPS came in at $0.70, representing a 52% year-over-year decline. Total (EPA:TTEF) segment operating profit fell 38% to $747 million.

As shown in the following financial highlights chart:

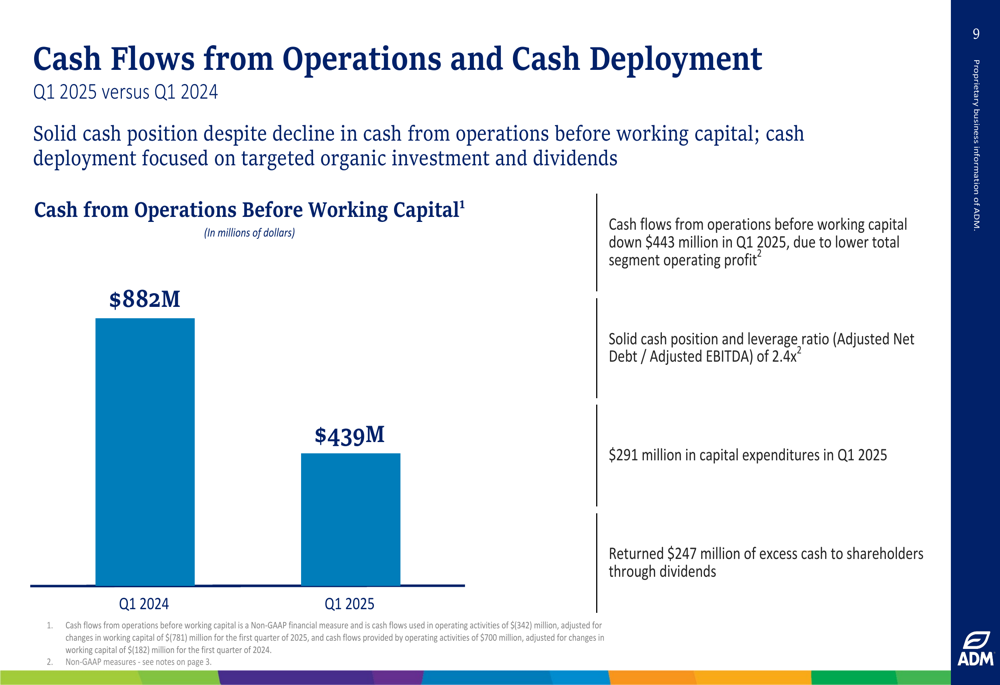

The company’s trailing four-quarter adjusted return on invested capital (ROIC) stood at 7.0%, below its weighted average cost of capital of 8.3% and its long-term ROIC objective of 10%. Cash flows from operations before working capital decreased to $439 million, down $443 million from the prior year quarter, primarily due to lower operating profits.

Despite the earnings decline, ADM maintained its shareholder returns, distributing $247 million in dividends during the quarter. The company reported capital expenditures of $291 million and maintained a leverage ratio (Adjusted Net Debt/Adjusted EBITDA) of 2.4x.

Segment Analysis

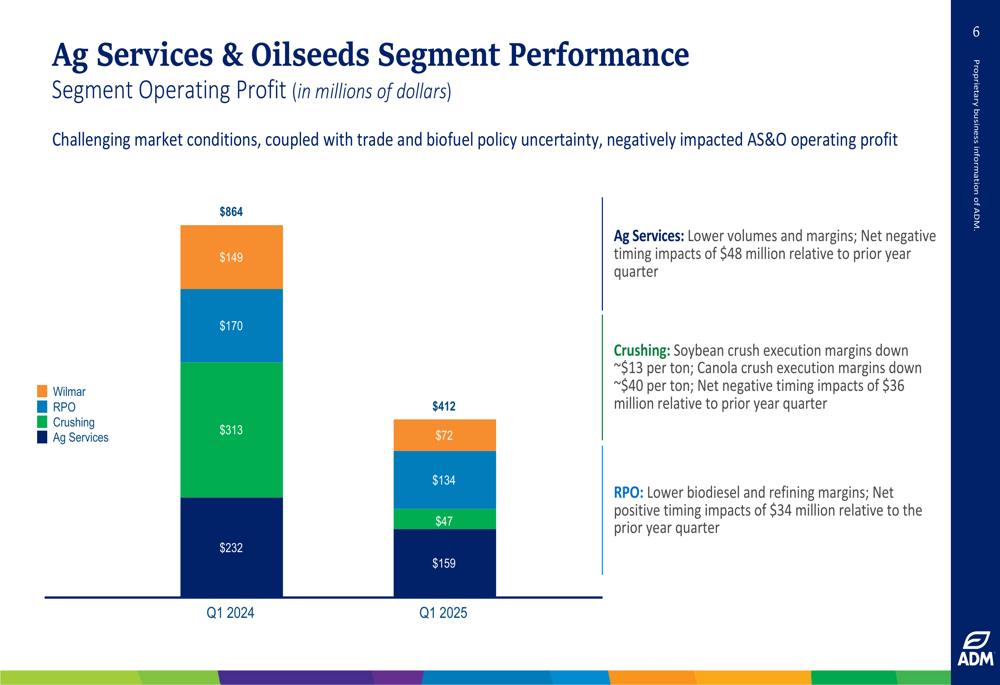

The Ag Services & Oilseeds segment, ADM’s largest business unit, experienced the most significant decline. Operating profit fell to $412 million in Q1 2025, less than half the $864 million reported in the same period last year. The company cited challenging market conditions, trade and biofuel policy uncertainty, lower volumes and margins, and negative timing impacts as key factors.

The segment breakdown shows dramatic declines across all business units:

Particularly notable was the collapse in crushing profits, which plummeted to $47 million from $313 million a year earlier. Management noted that soybean crush execution margins were down approximately $13 per ton, while canola crush execution margins fell about $40 per ton.

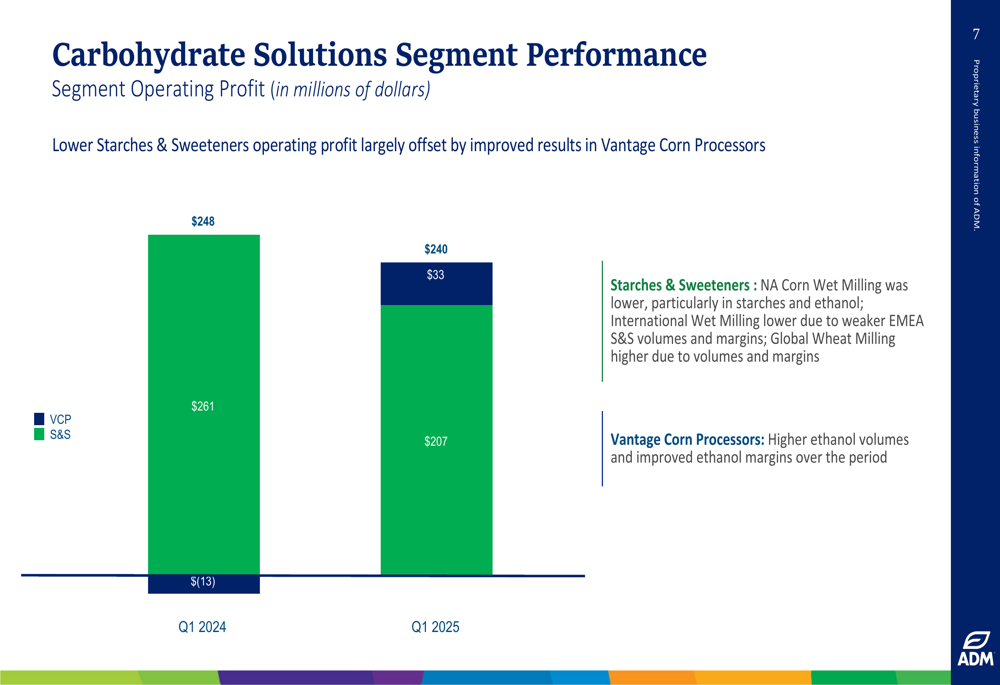

The Carbohydrate Solutions segment showed more resilience, with operating profit of $240 million, only slightly below the $248 million reported in Q1 2024. Improved results in Vantage Corn Processors, which swung from a $13 million loss to a $33 million profit, largely offset weakness in Starches & Sweeteners.

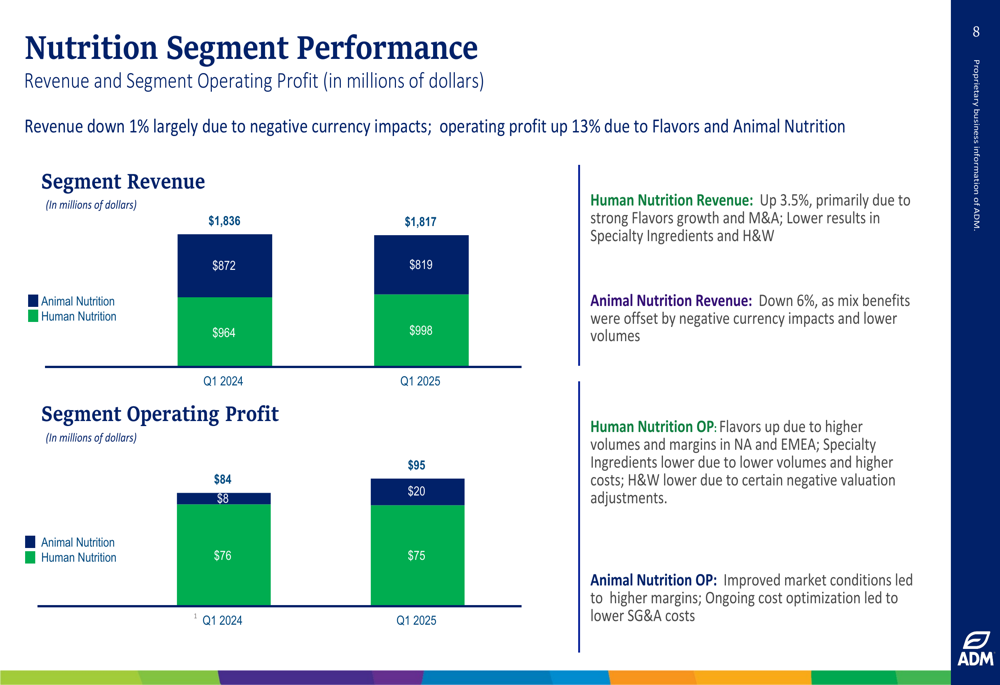

The Nutrition segment provided a bright spot amid the broader challenges, with operating profit increasing 13% to $95 million. This improvement was driven primarily by the Animal Nutrition business, which more than doubled its operating profit to $20 million due to improved market conditions and lower SG&A costs.

Strategic Initiatives

In response to the challenging environment, ADM outlined a comprehensive self-help strategy focused on four key areas: execution and cost focus, simplification, targeted organic growth investment, and capital discipline.

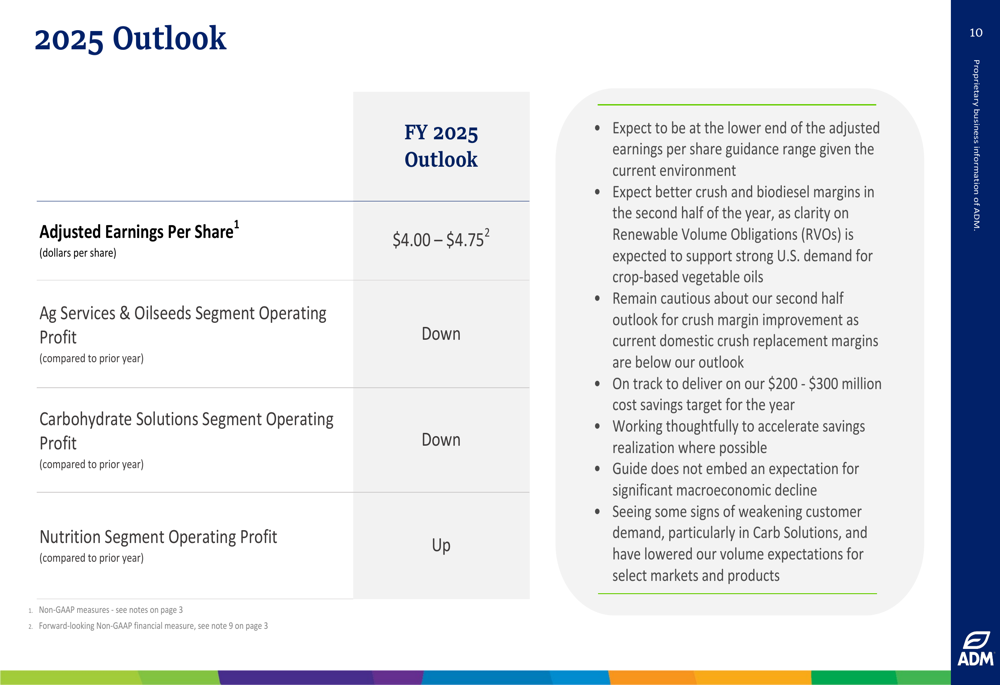

The company reported taking targeted organizational actions to support SG&A reduction and addressing operations uptime for North American soybean operations. Management stated they are on track to deliver on their $200-$300 million cost savings target for the year and are "working thoughtfully to accelerate savings realization where possible."

ADM is also implementing network optimization through the closure of its Kershaw crush facility and grain warehouse consolidation. The company announced it is exiting trading operations in China and Dubai to optimize customer service and has signed a memorandum of understanding with Mitsubishi Corporation to partner on new market opportunities.

On the investment front, ADM launched a partnership with Asahi to distribute postbiotics for stress, mood, and sleep management, while scaling up plant modernization projects to drive more efficient operations.

Forward-Looking Statements

ADM maintained its full-year 2025 adjusted earnings per share guidance of $4.00-$4.75 but indicated it expects to be at the lower end of this range given the current environment. This represents a continued downward trend from the previous year’s guidance.

The outlook for each segment shows:

The company expects better crush and biodiesel margins in the second half of the year as clarity on Renewable Volume Obligations (RVOs) is anticipated to support strong U.S. demand for crop-based vegetable oils. However, management remains cautious about the second half outlook for crush margin improvement, noting that "current domestic crush replacement margins are below our outlook."

ADM also acknowledged seeing some signs of weakening customer demand, particularly in Carbohydrate Solutions, and has lowered volume expectations for select markets and products. The guidance does not embed an expectation for significant macroeconomic decline.

Cash Flow and Balance Sheet

The company’s cash flow from operations before working capital changes declined significantly year-over-year, as shown in the following chart:

Despite the cash flow decline, ADM maintained a solid balance sheet with cash of $864 million as of Q1 2025. Total debt increased to $11.1 billion from $10.0 billion a year earlier, while shareholders’ equity declined to $22.1 billion from $23.2 billion.

The company’s adjusted net debt to adjusted EBITDA ratio stood at 2.4x, reflecting increased leverage compared to historical levels. This financial position gives ADM some flexibility to navigate the current challenging environment while continuing to invest in strategic initiatives and return cash to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.