ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Automatic Data Processing Inc (NASDAQ:ADP) presented its fourth quarter and full fiscal year 2025 results on July 30, 2025, showcasing strong performance across key metrics. The payroll and human resources services provider reported an 8% increase in total revenues for Q4, with adjusted earnings per share rising by 8% to $2.26.

The company’s shares, which closed at $308.64 on July 29, showed a modest increase of 0.28% in premarket trading following the presentation, indicating a cautiously positive market reception to the results and outlook.

Quarterly Performance Highlights

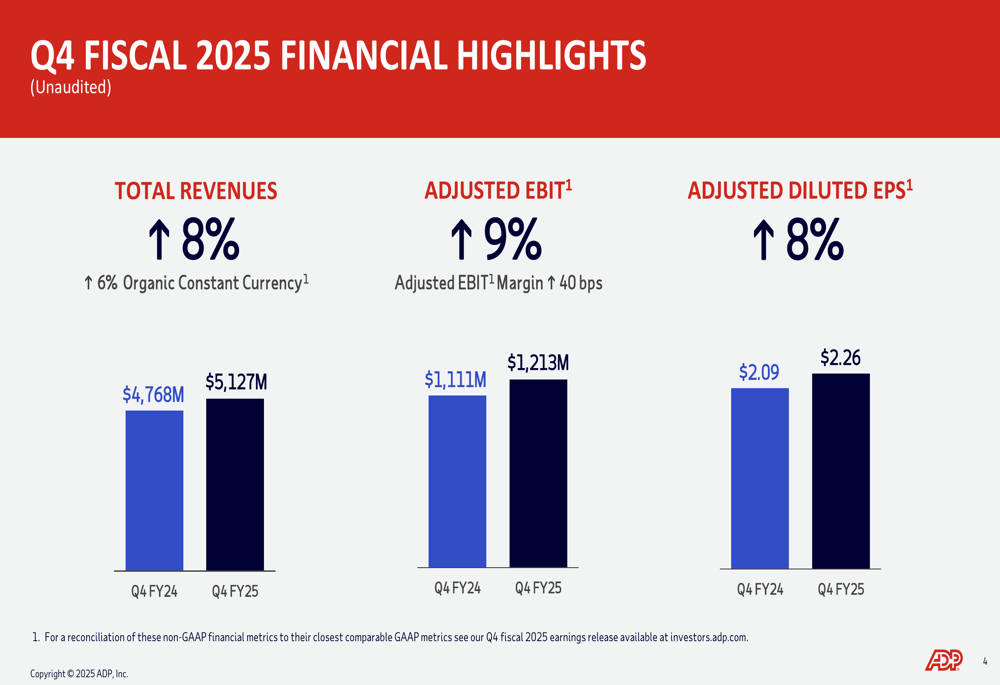

ADP’s fourth quarter results demonstrated robust growth, with total revenues reaching $5.13 billion, an 8% increase from $4.77 billion in the same quarter last year. On an organic constant currency basis, revenue grew by 6%. The company achieved a 9% increase in adjusted EBIT to $1.21 billion, with margin expansion of 40 basis points.

As shown in the following chart of quarterly financial performance:

The adjusted diluted earnings per share of $2.26 represented an 8% increase from $2.09 in Q4 FY24, continuing ADP’s trend of consistent earnings growth. This performance aligns with the company’s Q3 results, where ADP had also exceeded analyst expectations.

Full-Year Financial Analysis

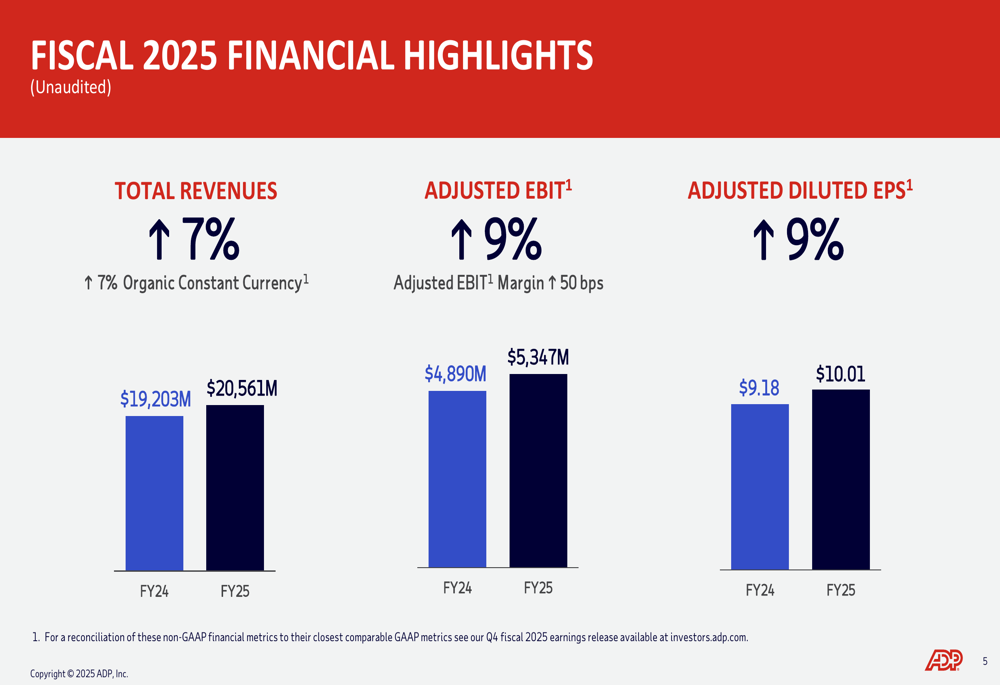

For the full fiscal year 2025, ADP delivered 7% revenue growth, reaching $20.56 billion, with both reported and organic constant currency growth at 7%. Adjusted EBIT increased by 9% to $5.35 billion, with margin expansion of 50 basis points. Adjusted diluted EPS grew 9% to $10.01.

The following chart illustrates ADP’s full-year financial performance:

These results reflect ADP’s consistent execution throughout the year, with the 7% revenue growth landing at the high end of the 6-7% range projected in the company’s Q3 guidance.

Segment Performance

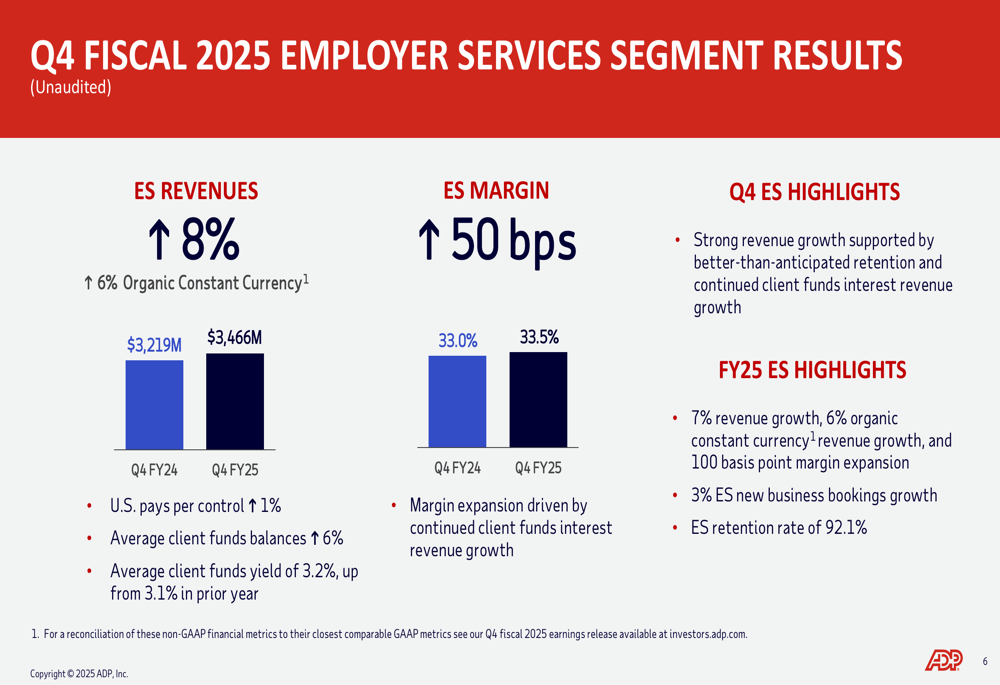

ADP’s Employer Services (ES) segment, which represents the core of its business, delivered strong results in Q4 with 8% revenue growth (6% on an organic constant currency basis) to $3.47 billion. The segment achieved margin expansion of 50 basis points to 33.5%, driven by continued client funds interest revenue growth.

The ES segment performance is illustrated in the following chart:

For the full fiscal year, the ES segment posted 7% revenue growth with impressive 100 basis point margin expansion. New business bookings grew 3%, while the client retention rate remained strong at 92.1%. U.S. pays per control, a key metric indicating the number of employees on ADP clients’ payrolls, increased by 1% in Q4.

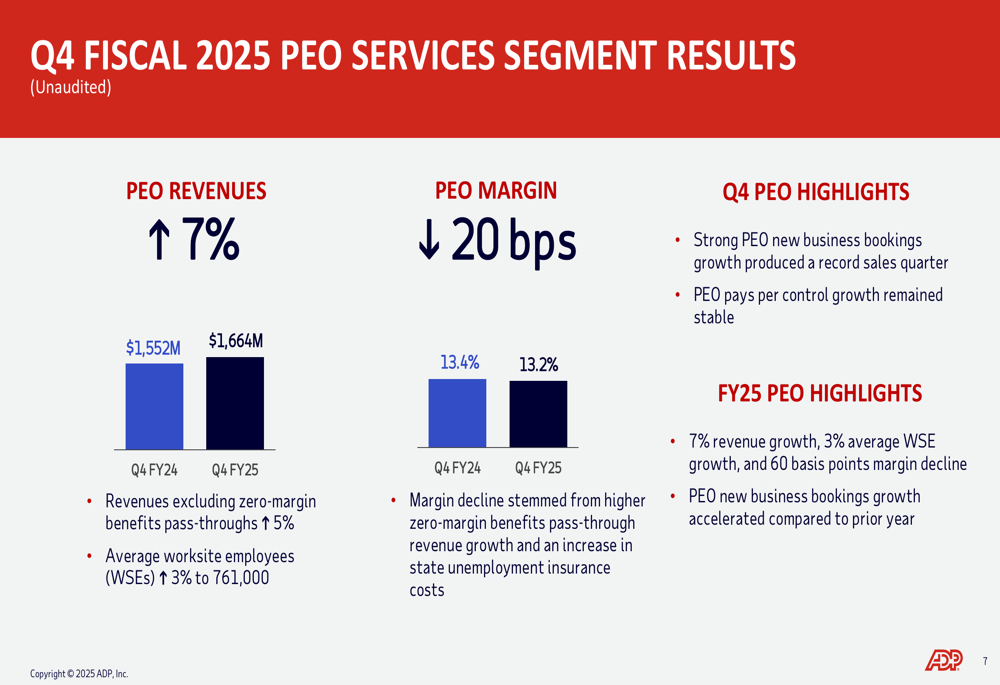

The PEO Services segment, which provides professional employer organization services, saw revenue growth of 7% to $1.66 billion in Q4, though margins declined by 20 basis points to 13.2%. This decline was attributed to higher zero-margin benefits pass-through revenue growth and increased state unemployment insurance costs.

The following chart details the PEO Services segment performance:

Average worksite employees (WSEs) in the PEO segment increased by 3% to 761,000 in Q4. For the full year, the segment delivered 7% revenue growth but experienced a 60 basis point margin decline. Notably, PEO new business bookings growth accelerated compared to the prior year, with Q4 producing a record sales quarter.

Strategic Initiatives

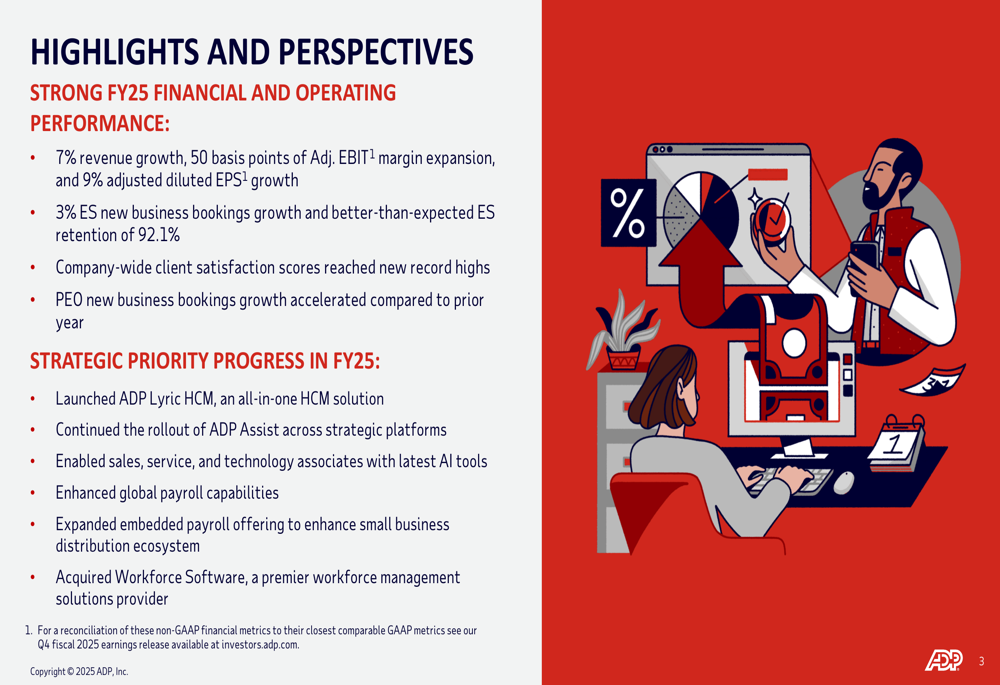

ADP highlighted several strategic achievements during fiscal 2025, positioning the company for future growth. Key initiatives included the launch of ADP Lyric HCM, an all-in-one human capital management solution, and the continued rollout of ADP Assist across strategic platforms.

The company has also focused on enabling sales, service, and technology associates with the latest AI tools, enhancing global payroll capabilities, and expanding its embedded payroll offering to strengthen the small business distribution ecosystem.

A significant strategic move was the acquisition of Workforce Software (ETR:SOWGn), a premier workforce management solutions provider, which aligns with CEO Maria Black’s previous statements about the essential nature of ADP’s services: "We are not discretionary. Companies have to pay people."

The following slide summarizes ADP’s key strategic initiatives and FY25 performance highlights:

Forward-Looking Statements

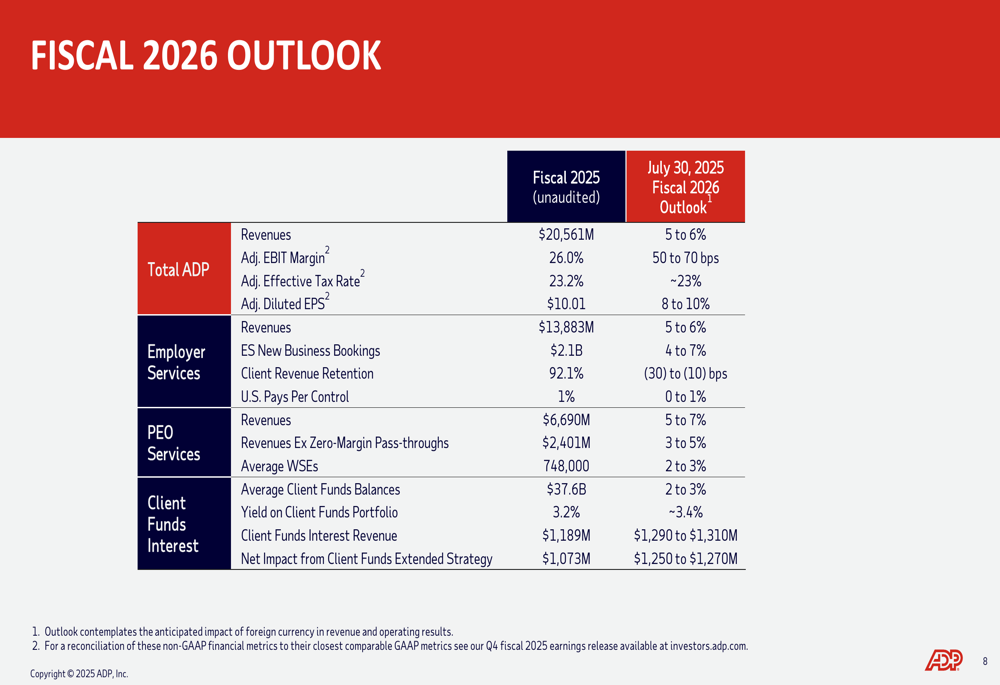

Looking ahead to fiscal 2026, ADP projects revenue growth of 5-6%, slightly below the 7% achieved in FY25. The company expects adjusted EBIT margin expansion of 50-70 basis points and adjusted diluted EPS growth of 8-10%, indicating confidence in continued profitability improvements despite moderating revenue growth.

For the Employer Services segment, ADP forecasts 5-6% revenue growth and new business bookings growth of 4-7%, suggesting acceleration from the 3% growth in FY25. However, client revenue retention is expected to decline slightly by 10-30 basis points.

The PEO Services segment is projected to grow revenues by 5-7%, with average worksite employees increasing by 2-3%.

The detailed fiscal 2026 outlook is presented in the following table:

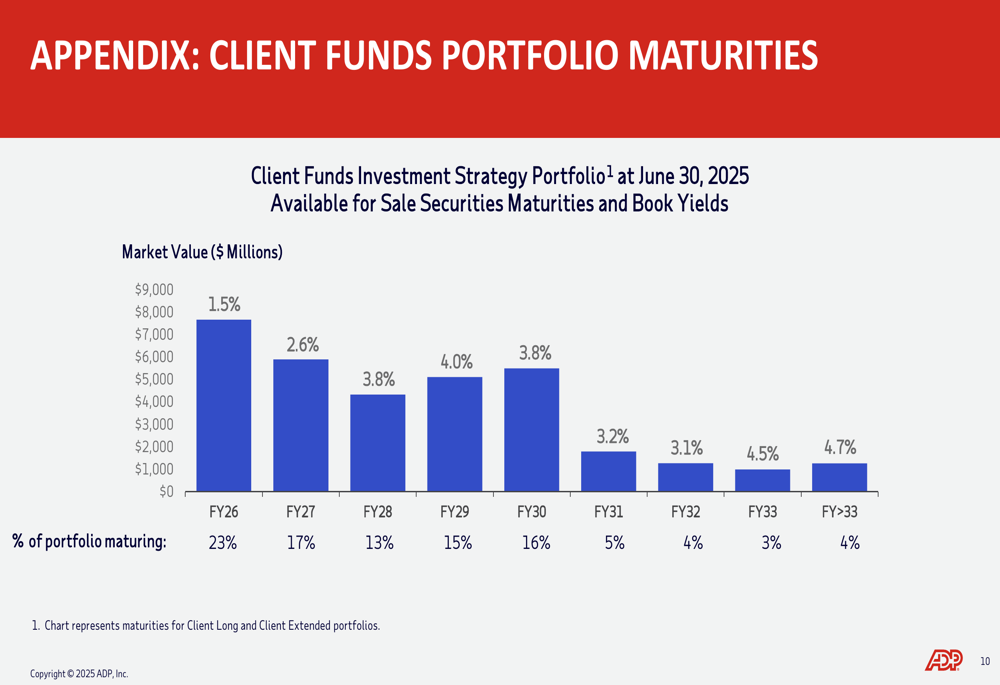

ADP’s client funds investment strategy remains a significant contributor to its financial performance. The company provided detailed information on its portfolio maturities, showing a well-structured approach to managing client funds with varying yields across different maturity periods:

The portfolio shows higher yields for longer-term maturities, with fiscal years 2033 and beyond offering yields of 4.5% and 4.7% respectively, while near-term maturities in FY26 yield 1.5%.

Market Implications

ADP’s consistent performance and forward-looking guidance reflect the company’s resilience in an uncertain economic environment. The slight moderation in growth expectations for FY26 appears to be a prudent approach given broader economic concerns, yet the projected 8-10% EPS growth indicates continued strong operational execution and margin improvements.

With a current dividend yield of approximately 2% and a history of 26 consecutive years of dividend increases, ADP continues to offer a compelling combination of growth and income for investors. The modest premarket trading increase of 0.28% suggests investors are cautiously optimistic about the company’s prospects while digesting the full implications of the FY26 guidance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.