Asia FX steady as Fed, BOJ rate decisions loom; US-China talks in focus

Introduction & Market Context

Agilon Health Inc (NYSE:AGL) presented its first quarter 2025 earnings results on May 6, 2025, revealing an earnings beat that sent shares up 8.25% to close at $4.45 despite year-over-year declines in key metrics. The healthcare company reported earnings per share (EPS) of $0.03, significantly surpassing the forecast of $0.0016, while revenue reached $1.533 billion, exceeding expectations of $1.51 billion.

The stock has demonstrated remarkable momentum with a 116.84% return year-to-date, though it remains below its 52-week high of $7.73. This positive market reaction reflects investor confidence in the company’s strategic direction despite ongoing challenges in the Medicare Advantage space.

Quarterly Performance Highlights

Agilon Health’s Q1 2025 financial results showed mixed performance with solid revenue generation despite declining membership numbers compared to the previous year.

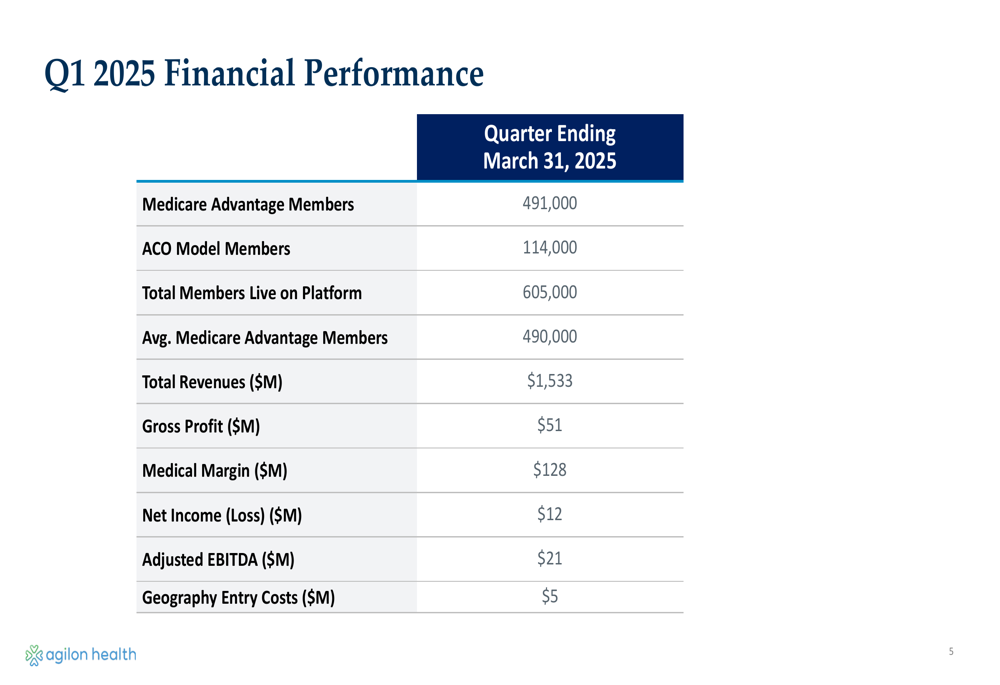

As shown in the following financial performance summary:

The company reported 491,000 Medicare Advantage members, down from 523,000 in Q1 2024, and 114,000 ACO Model members, bringing total platform membership to 605,000. Despite the membership decline, Agilon generated $1.533 billion in total revenue, with a gross profit of $51 million and a medical margin of $128 million. The company achieved a net income of $12 million and adjusted EBITDA of $21 million, while incurring $5 million in geography entry costs.

These results demonstrate the company’s ability to maintain profitability despite membership challenges, with adjusted EBITDA of $21 million representing a decrease from $29 million in Q1 2024 but still exceeding analyst expectations.

Strategic Initiatives

Agilon Health outlined several strategic initiatives aimed at strengthening its business for long-term success while addressing near-term challenges in the Medicare Advantage market.

The company’s approach focuses on three key areas as illustrated in their strategic framework:

These initiatives are further detailed in the company’s strategic action plan:

Key strategic actions include reducing exposure to Part D (now less than 30% of membership), maintaining flat year-over-year G&A expenses, and implementing a more disciplined growth strategy with a smaller class of 2025 partners. The company is also investing in advanced clinical capabilities, including expanding palliative care programs, launching heart failure initiatives, and enhancing data analytics capabilities.

During the earnings call, CEO Steve Sell emphasized that 2025 represents "both a transition year financially and an inflection year in terms of quality and clinical programs," highlighting the company’s focus on balancing near-term financial performance with long-term strategic positioning.

Financial Outlook

Agilon Health provided a detailed financial outlook for the remainder of 2025, projecting stabilization in key metrics with modest growth expected.

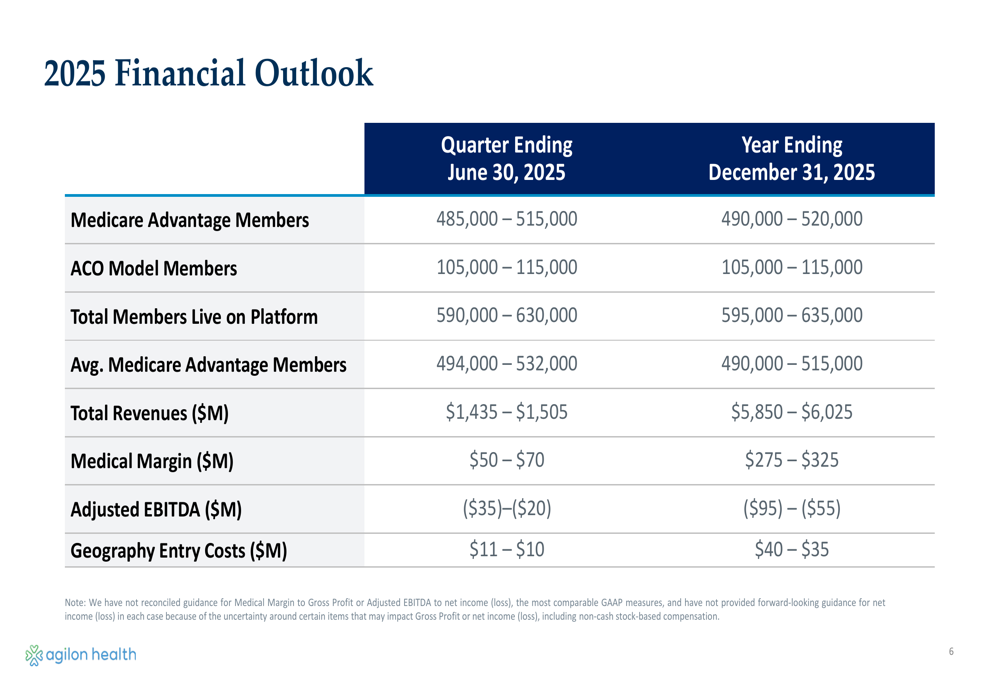

The following outlook details the company’s financial projections:

For the full year 2025, Agilon expects Medicare Advantage membership to range between 490,000 and 520,000, with total platform membership projected between 595,000 and 635,000. The company forecasts total revenue between $5.85 billion and $6.025 billion, with medical margin between $275 million and $325 million.

Adjusted EBITDA is expected to remain negative for the year, ranging from ($95) million to ($55) million, reflecting continued investments in growth and platform development. Geography entry costs are projected between $35 million and $40 million as the company continues its measured expansion strategy.

Balance Sheet and Cash Position

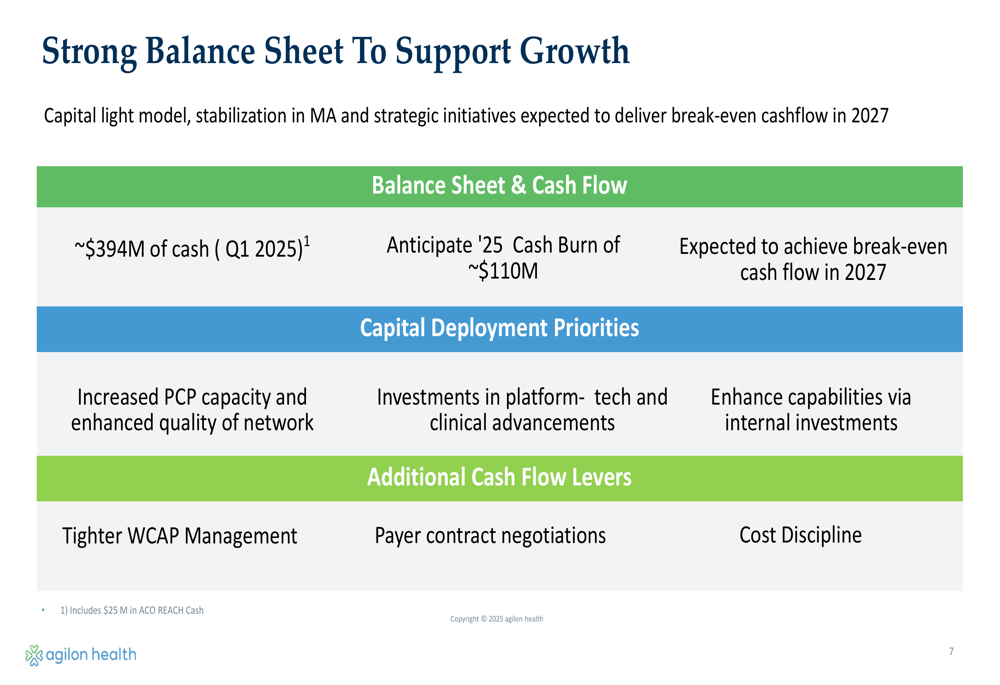

Agilon Health emphasized its strong balance sheet position as a key enabler of its strategic initiatives and pathway to profitability.

The company’s capital position and deployment priorities are outlined in the following summary:

With approximately $394 million in cash as of Q1 2025, Agilon anticipates a cash burn of approximately $110 million for the full year. The company expects to achieve break-even cash flow by 2027, supported by its capital-light model and strategic initiatives aimed at stabilizing Medicare Advantage performance.

Capital deployment priorities include increasing primary care physician capacity, enhancing network quality, investing in platform technology and clinical advancements, and building capabilities through internal investments. Additional cash flow levers include tighter working capital management, payer contract negotiations, and continued cost discipline.

Forward-Looking Statements

Agilon Health’s presentation reflects a cautiously optimistic outlook, acknowledging near-term challenges while emphasizing long-term growth potential in the value-based care space. The company’s strategic focus on reducing variability, enhancing quality outcomes, and driving operational efficiencies aims to position it for sustainable profitability.

Management highlighted strong demand for value-based care partnerships, with CEO Steve Sell noting that "the demand from groups that are looking for partners that are experienced in moving them to value is highly strong." This positive market sentiment, combined with the company’s strategic initiatives, supports Agilon’s path toward break-even cash flow by 2027.

However, investors should consider potential risks, including declining Medicare Advantage membership, medical cost trends, and challenges related to the transition to the V-28 risk model. The company’s ability to execute on its strategic initiatives while navigating these challenges will be critical to achieving its long-term financial goals.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.