ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Align Technology (NASDAQ:ALGN) presented its Q2 2025 financial results on July 30, 2025, revealing a mixed performance as the company navigates economic challenges while maintaining its position as a leader in clear aligners and digital dentistry solutions.

The company continues to target a substantial global opportunity, with management highlighting a potential patient base of over 600 million individuals worldwide. According to the presentation, approximately 75% of the global population has some form of malocclusion that could benefit from orthodontic treatment.

As shown in the following slide highlighting the global opportunity:

The company segments the global orthodontic market into 22 million annual orthodontic starts, distributed across three main regions: 8 million in the Americas, 6 million in EMEA (Europe, Middle East, and Africa), and 8 million in APAC (Asia-Pacific).

Quarterly Performance Highlights

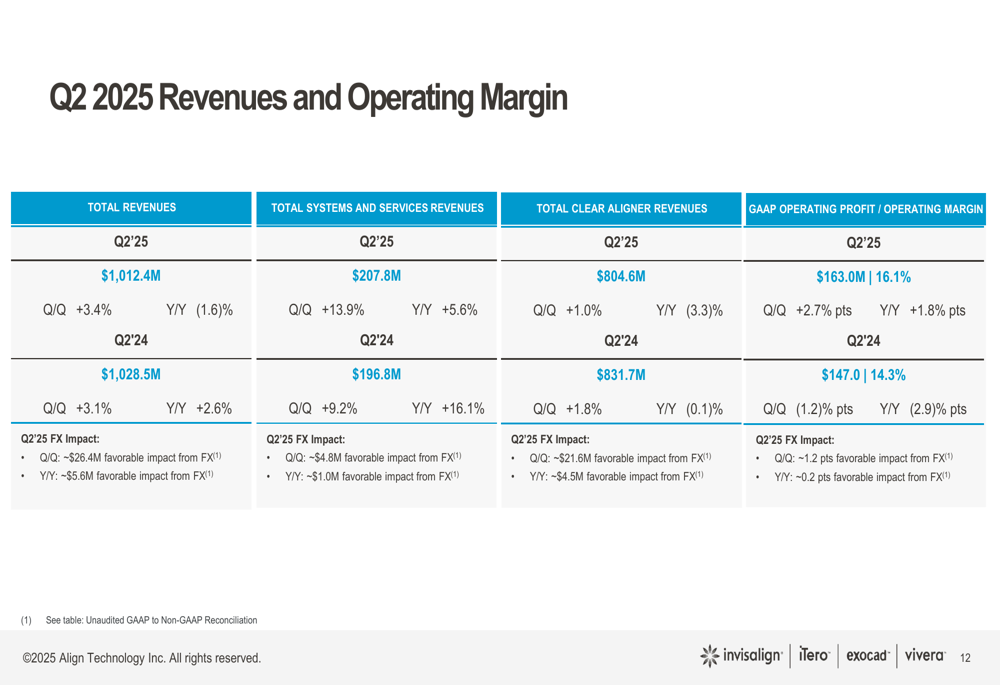

Align Technology reported total Q2 2025 revenues of $1,012.4 million, representing a 3.4% increase quarter-over-quarter but a 1.6% decrease year-over-year. The GAAP operating margin improved to 16.1%, up 2.7 percentage points sequentially and 1.8 percentage points year-over-year.

The following slide details the company's Q2 2025 revenue performance and operating margin:

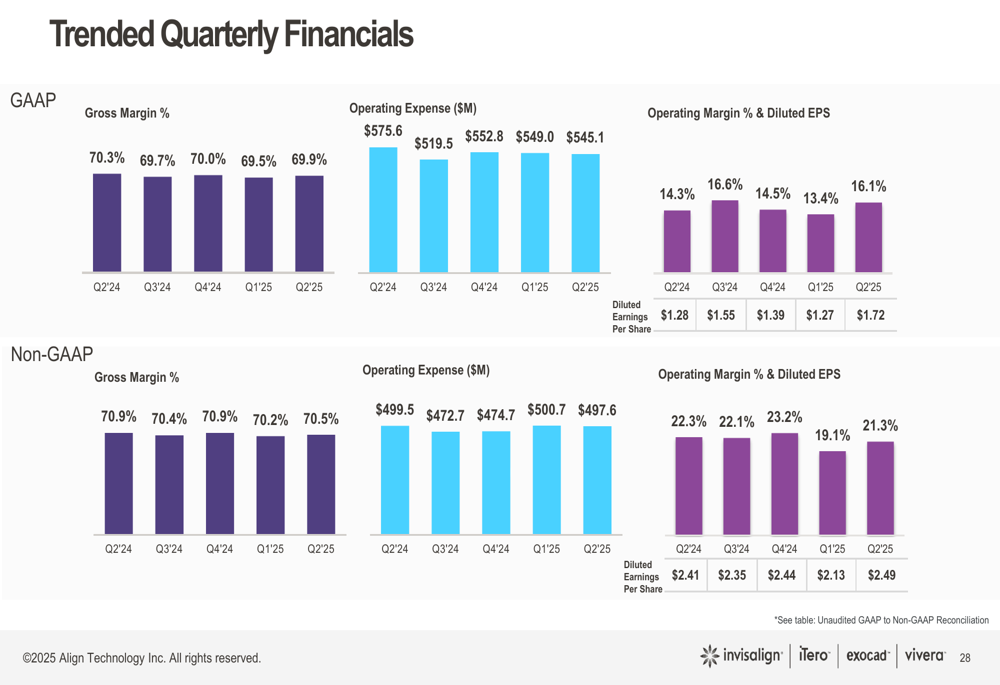

GAAP earnings per diluted share reached $1.72, while non-GAAP earnings per diluted share was $2.49. This represents the highest EPS figures in recent quarters, as shown in the comprehensive financial overview:

The company maintained a strong cash position with $901.2 million in cash and cash equivalents. During the quarter, Align repurchased approximately 585,100 shares of common stock at an average price of $164.14 per share.

Segment Performance

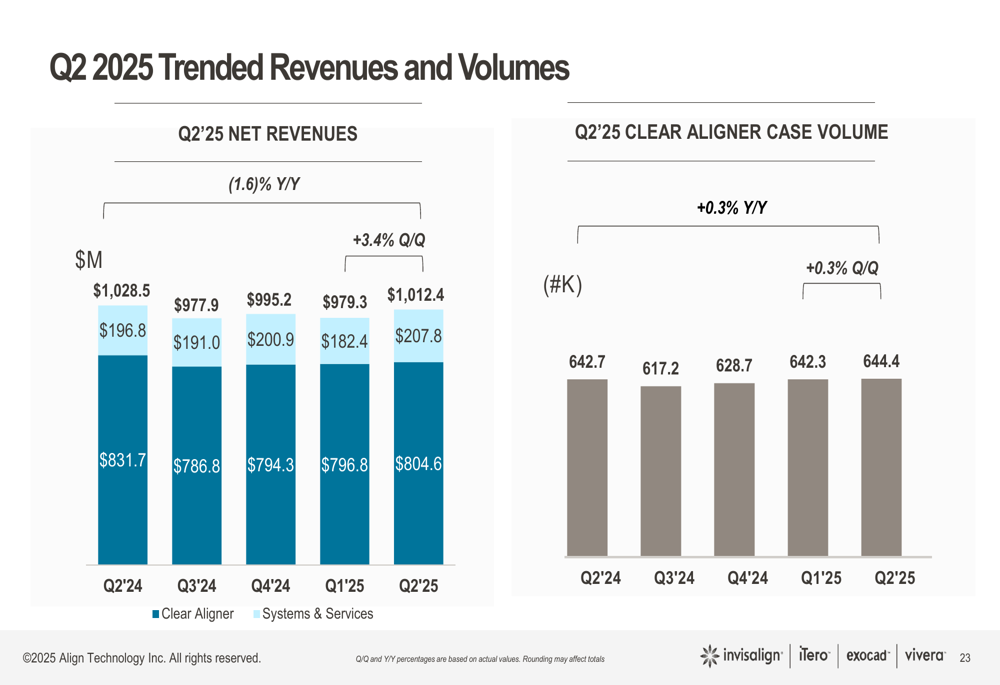

Align's business performance showed divergent trends across its two main segments. The Clear Aligner segment, which accounts for approximately 80% of total revenue, generated $804.6 million, up 1.0% quarter-over-quarter but down 3.3% year-over-year. Clear Aligner shipments showed minimal growth of 0.3% both sequentially and year-over-year.

The Systems and Services segment, which includes iTero scanners and CAD/CAM services, delivered $207.8 million in revenue, representing robust growth of 13.9% quarter-over-quarter and 5.6% year-over-year. This segment now accounts for approximately 20% of total company revenue.

The following chart illustrates the trended revenues and volumes:

Management noted that the average selling price (ASP) for Clear Aligners was $1,250 in Q2 2025, continuing a downward trend. The company expects ASPs to decline further throughout 2025.

Strategic Initiatives and Global Opportunity

Despite near-term challenges, Align continues to expand its global footprint, having treated approximately 20.8 million Invisalign patients to date, including 6.1 million teens and kids. The teen and kids segment grew 3.0% year-over-year, driven by growth in APAC, EMEA, and Latin America, partially offset by softness in North America.

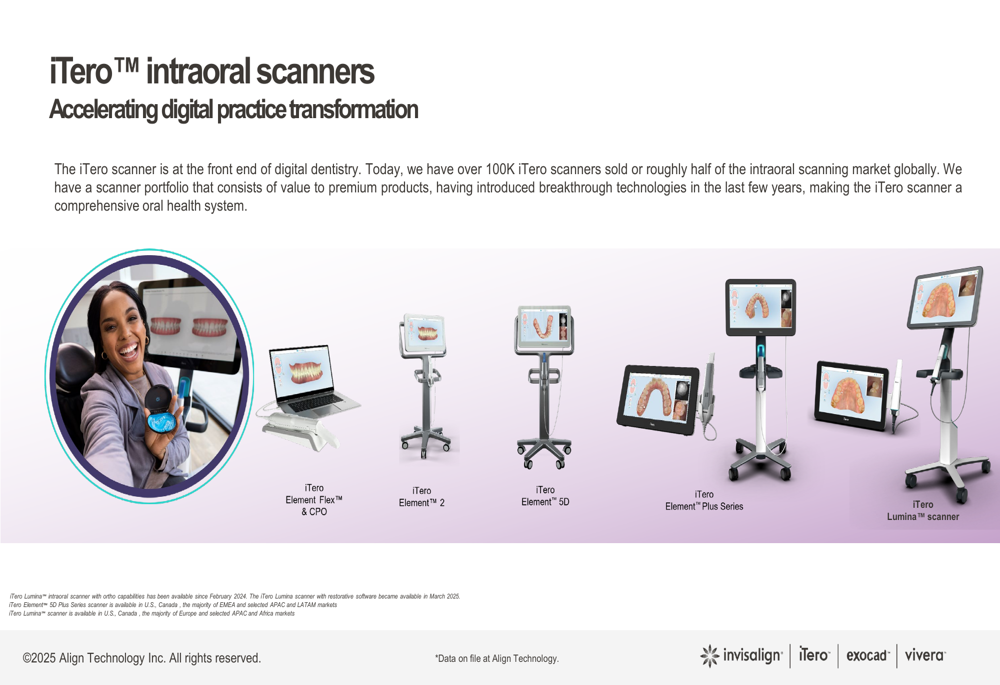

The company's iTero scanner business remains a strategic priority, with over 100,000 scanners sold to date. Management positions the scanner as the entry point to digital dentistry, as shown in the following product lineup:

Align's consumer marketing efforts generated significant engagement in Q2 2025, with 12.1 billion impressions and 54 million website visits across all regions. The My Invisalign app reached 5.66 million downloads with 494,000 monthly active users, representing 29% year-over-year growth.

Restructuring Plans and Outlook

In response to challenging market conditions, Align announced plans to implement a series of actions in the second half of fiscal 2025 to streamline operations and reallocate resources. The company expects to incur one-time charges of approximately $150-170 million, with approximately $40 million in cash charges. Of the total, about $50-60 million is expected to impact Q3 2025.

Management cited several factors affecting demand, including "uneven patient case conversion" impacted by "U.S. tariff turmoil" and "less affordable financing options for orthodontic treatment, as well as for capital equipment purchases."

The company also provided an update on UK VAT, noting that Align invoices will no longer include the United Kingdom VAT rate of 20% for Invisalign treatment packages.

Forward Guidance and Market Reaction

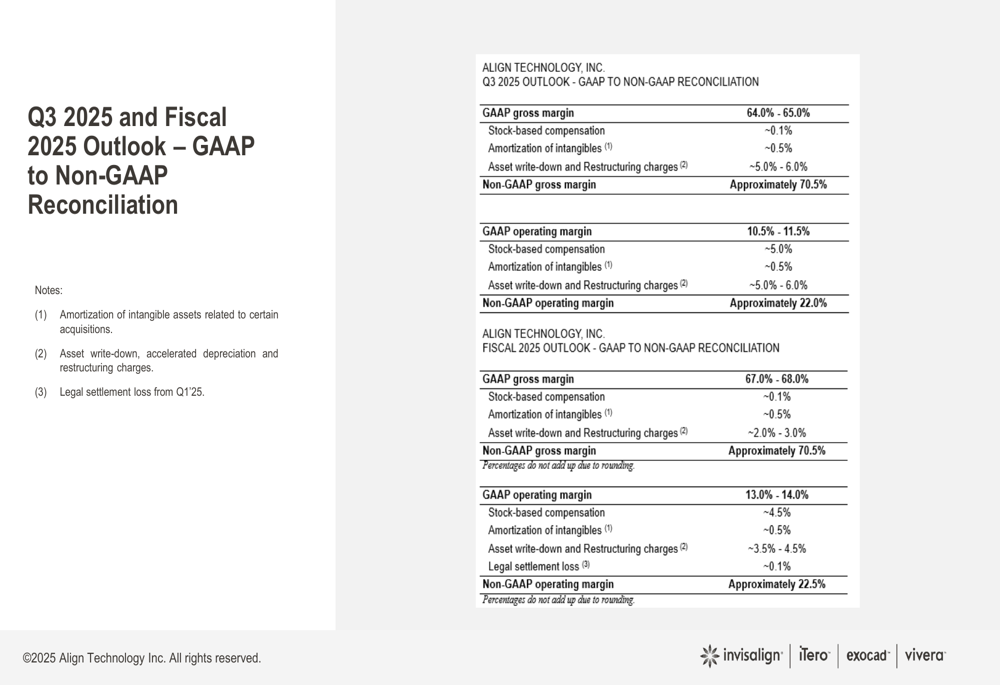

For Q3 2025, Align expects worldwide revenues to range between $965 million and $985 million, with GAAP gross margin of 64-65% and GAAP operating margin of 10.5-11.5%. For the full fiscal year 2025, the company projects GAAP gross margin of 67-68% and GAAP operating margin of 13-14%.

The following slide details the company's outlook for Q3 and fiscal 2025:

Notably, the actual Q3 2025 results (reported after this presentation) showed that Align exceeded these projections, with revenue reaching $995.7 million and earnings per share of $2.61, surpassing the forecasted $2.42. The company's stock, which initially declined in regular trading following the Q2 results, rebounded in aftermarket trading following the stronger-than-expected Q3 performance.

Clear aligner volume growth in Q3 reached 5%, significantly outpacing the minimal 0.3% growth seen in Q2, suggesting that the company's restructuring efforts and market positioning strategies began yielding positive results. The cash position also improved to $1,004.6 million by the end of Q3, up from $901.2 million in Q2.

As Align Technology continues to navigate market headwinds while implementing operational changes, investors will be watching closely to see if the company can maintain the positive momentum seen in its Q3 performance and achieve its long-term growth objectives in the expanding digital orthodontics market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.