Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

Alleima AB (ALLEI) shares jumped 7.18% on April 23, 2025, following the release of its first-quarter results, which revealed accelerating revenue growth and expanded margins despite mixed market conditions. The Swedish specialty steel manufacturer reported solid performance across its divisions, with particularly strong results in its Tube segment.

The company operates in a challenging global market environment characterized by soft European demand, but has benefited from solid development in Asia and recovery in North America. Alleima’s diverse sector exposure, with significant presence in Oil and Gas (23%), Chemical and Petrochemical (17%), and Industrial (17%) segments, has helped insulate it from regional market weaknesses.

Quarterly Performance Highlights

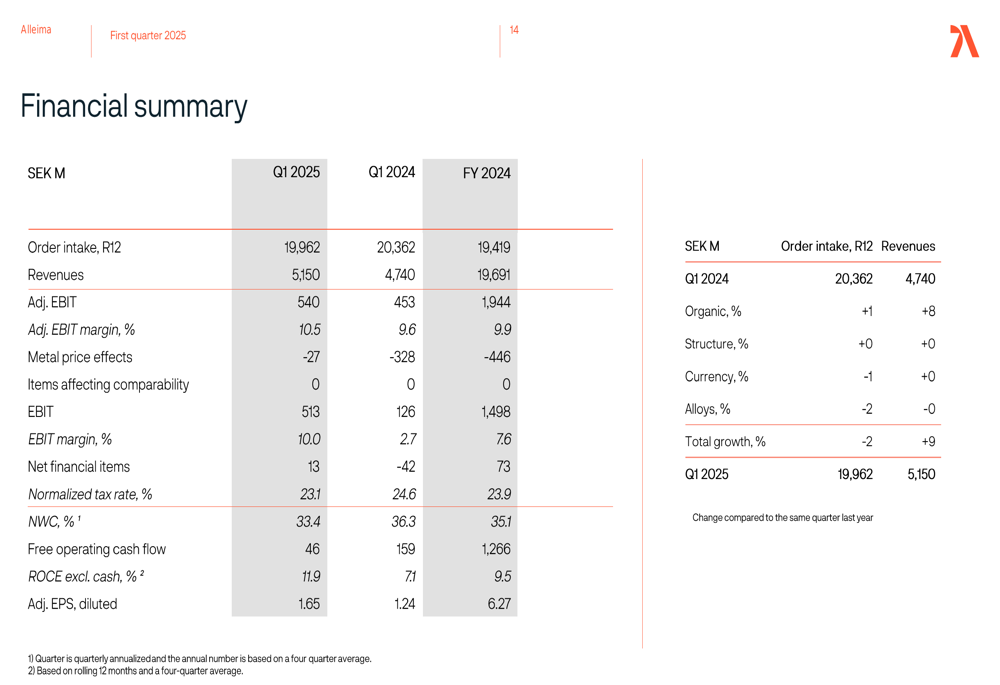

Alleima reported revenues of SEK 5,150 million for Q1 2025, representing organic growth of 8% compared to the same period last year. The company achieved an adjusted EBIT of SEK 540 million, up from SEK 453 million in Q1 2024, resulting in an improved adjusted EBIT margin of 10.5% versus 9.6% a year earlier.

As shown in the following comprehensive financial overview, the company demonstrated broad-based topline growth and solid financial performance:

Free operating cash flow came in at SEK 46 million, down from SEK 159 million in Q1 2024, with the company noting that cash flow is typically higher in the second half of the year. The company maintained a strong financial position with negative net debt of SEK 414 million, reflecting substantial cash reserves.

The detailed financial summary below provides a clear comparison with previous periods:

Detailed Financial Analysis

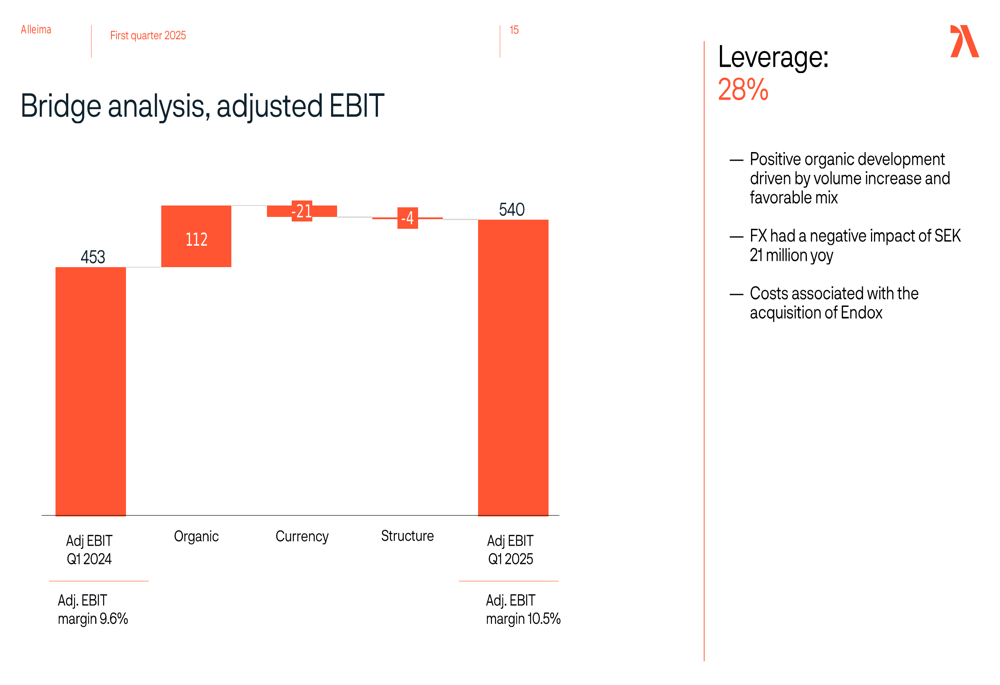

Alleima’s adjusted EBIT improved by SEK 87 million year-over-year, driven primarily by organic growth which contributed SEK 112 million. This positive impact was partially offset by currency headwinds of SEK 21 million and a small negative structural impact of SEK 4 million related to the acquisition of Endox.

The following bridge analysis illustrates the key drivers behind the EBIT improvement:

The company has demonstrated improved margin resilience over time, maintaining historically high margins despite approximately 15% lower production volumes in its steel plant compared to 2019 levels. This resilience highlights the effectiveness of Alleima’s operational efficiency initiatives and strategic positioning.

Looking at divisional performance, the Tube division reported strong results with a 12% organic revenue growth and an adjusted EBIT margin of 11.1%. The Kanthal division faced mixed market demand but maintained a solid margin of 16.6%, while the Strip division showed strong order intake growth of 34% (R12) with a margin of 6.9%.

Alleima’s balance sheet remains exceptionally strong, with a net debt to equity ratio of -0.02x and net debt to adjusted EBITDA of -0.14x, providing significant financial flexibility for future growth initiatives.

Strategic Initiatives

Alleima continues to strengthen its global footprint with sales in 80 markets, supported by 5 R&D centers, over 40 sales offices, and more than 25 production sites worldwide. This extensive network enables the company to maintain proximity to customers, ensure operational flexibility, and drive specialization across its business segments.

The company is actively supporting the sustainable energy transition, particularly in hydrogen infrastructure. Alleima highlighted its versatile on-site tubing solution launched in Canada and noted its involvement in over 70 hydrogen projects across Europe, positioning the company to benefit from growing investments in clean energy infrastructure.

Sustainability remains a core focus for Alleima, with the company tracking several key metrics. In Q1 2025, the company reported a Total (EPA:TTEF) Recordable Injury Frequency Rate (TRIFR) of 6.6, recycled steel usage in manufacturing of 80.6%, and a 3% reduction in CO2 emissions. The share of female managers reached 24.8% during the quarter.

Forward-Looking Statements

For the second quarter of 2025, Alleima provided guidance indicating expected currency headwinds of approximately SEK 130 million on operating profit and metal price effects of negative SEK 150 million. The company anticipates a normalized tax rate of 23-25% for the full year 2025, with capital expenditures projected at approximately SEK 1,200 million.

Management noted continuing uncertainties related to macroeconomic conditions and mixed market demand but highlighted positive development in several segments and a solid backlog in key areas. The company expects a similar product mix in Q2 as seen in Q1, with cash flow typically lower in the first half of the year.

Alleima’s outlook remains cautiously optimistic, supported by ongoing growth initiatives and its strong financial position, which provides flexibility to navigate market uncertainties while continuing to invest in strategic growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.