US stock futures inch lower after Wall St marks fresh records on tech gains

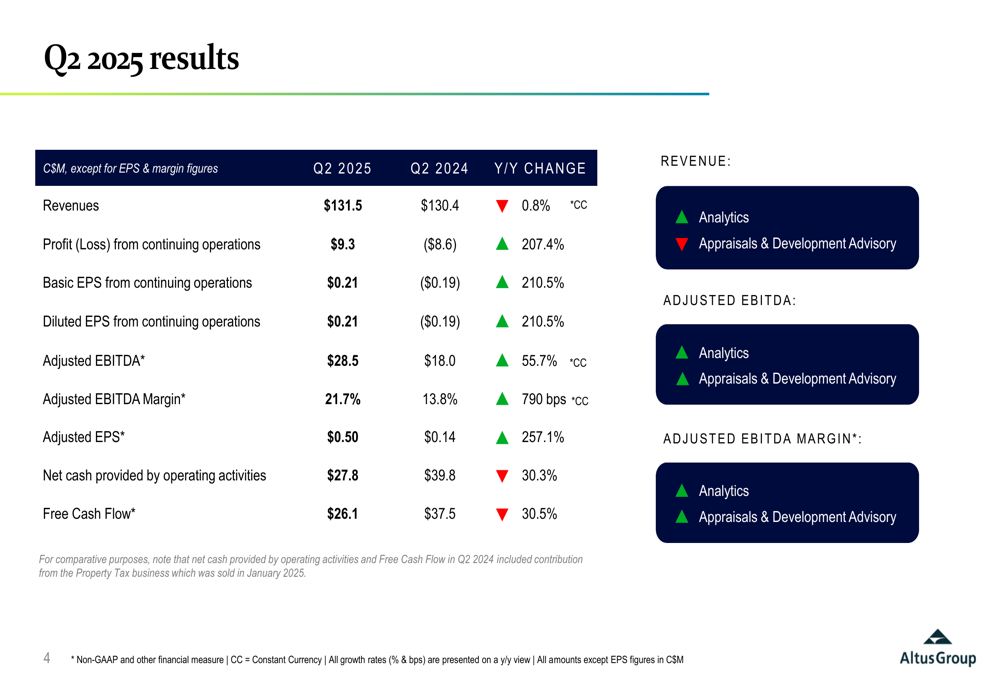

Altus Group Limited (TSX:AIF) reported a substantial increase in profitability for the second quarter of 2025, with profit from continuing operations surging 207.4% year-over-year despite modest revenue growth. The company’s shares fell 8.72% following the earnings release on August 7, 2025, closing at $47.26, as investors reacted to downward revisions in revenue guidance.

Quarterly Performance Highlights

Altus Group posted Q2 2025 revenue of $131.5 million, representing a modest 0.8% increase in constant currency compared to the same period last year. However, profit from continuing operations jumped to $9.3 million from a loss of $8.6 million in Q2 2024, translating to a 207.4% improvement. Basic and diluted earnings per share reached $0.21, up 210.5% from -$0.19 in the prior-year quarter.

Adjusted EBITDA showed significant improvement, rising 55.7% in constant currency to $28.5 million, with adjusted EBITDA margin expanding 790 basis points to 21.7%. Adjusted EPS more than tripled to $0.50, representing a 257.1% increase from $0.14 in Q2 2024.

As shown in the following comprehensive financial summary:

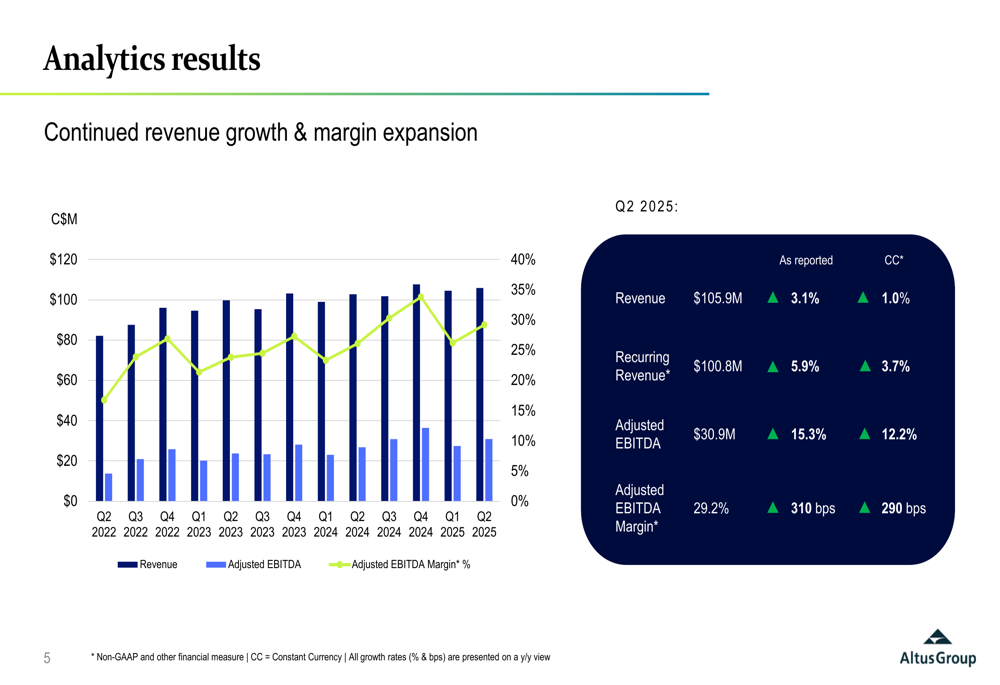

The Analytics segment, which accounts for approximately 80% of total revenue, delivered solid performance with revenue of $105.9 million, up 3.1% as reported (1.0% in constant currency). Recurring revenue within this segment grew 5.9% (3.7% in constant currency) to $100.8 million. The segment’s adjusted EBITDA increased 15.3% to $30.9 million, with margin expanding 310 basis points to 29.2%.

The following chart illustrates the Analytics segment’s performance:

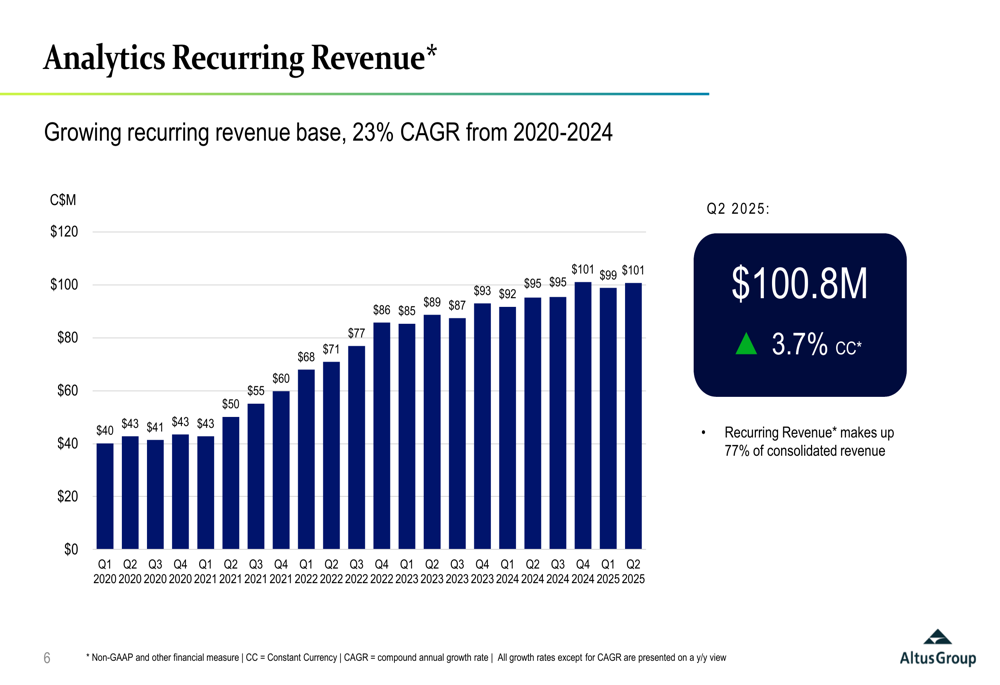

Altus Group has consistently grown its recurring revenue base over the past five years, achieving a 23% CAGR from 2020 to 2024. Recurring revenue now represents 77% of consolidated revenue, providing stability and predictability to the company’s financial performance.

The quarterly progression of recurring revenue is shown in this chart:

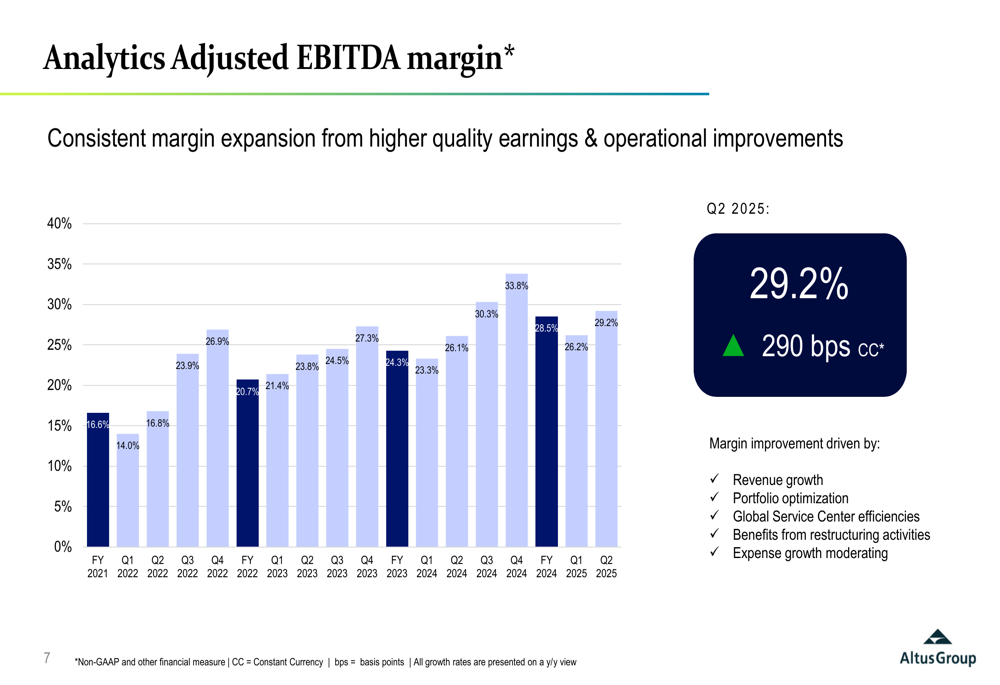

The company has also demonstrated consistent margin expansion in its Analytics segment, driven by revenue growth, portfolio optimization, Global Service Center efficiencies, benefits from restructuring activities, and moderating expense growth.

The following chart shows the steady improvement in Analytics adjusted EBITDA margin:

Operational Improvements and Strategic Initiatives

CEO Jim Hannon highlighted several positive developments during the quarter, including ARGUS software revenue returning to double-digit growth and the steady transition to ARGUS Intelligence, with approximately 1,900 clients contracted. The company also reported growing acceptance of its asset-based pricing model.

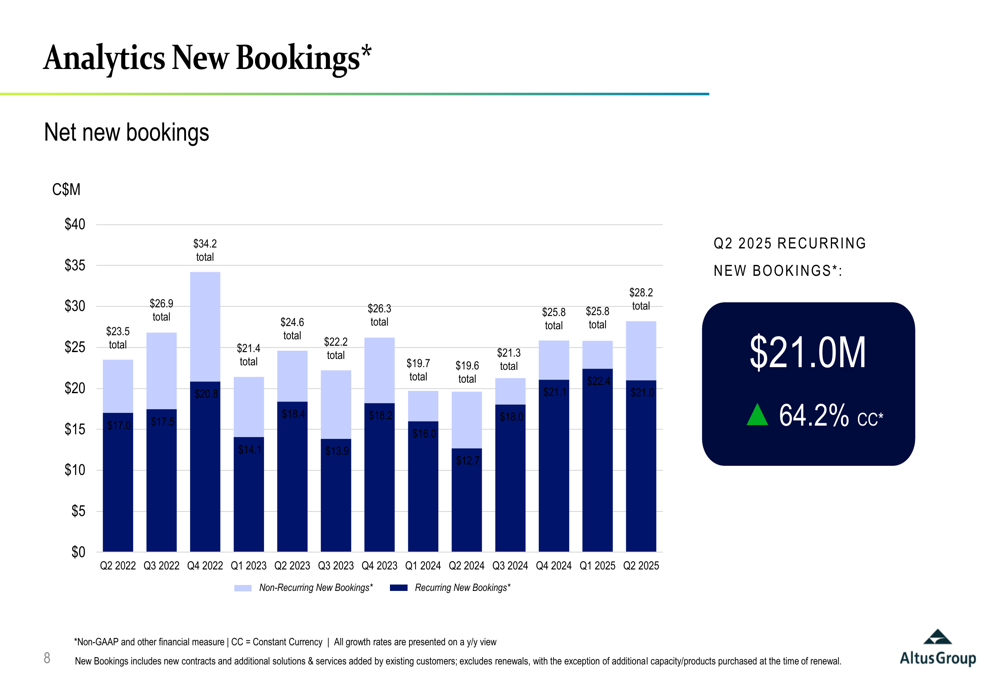

Recurring new bookings showed significant growth, up 64.2% in constant currency to $21.0 million, driven by strong performance in ARGUS and VMS products.

This growth in new bookings is illustrated in the following chart:

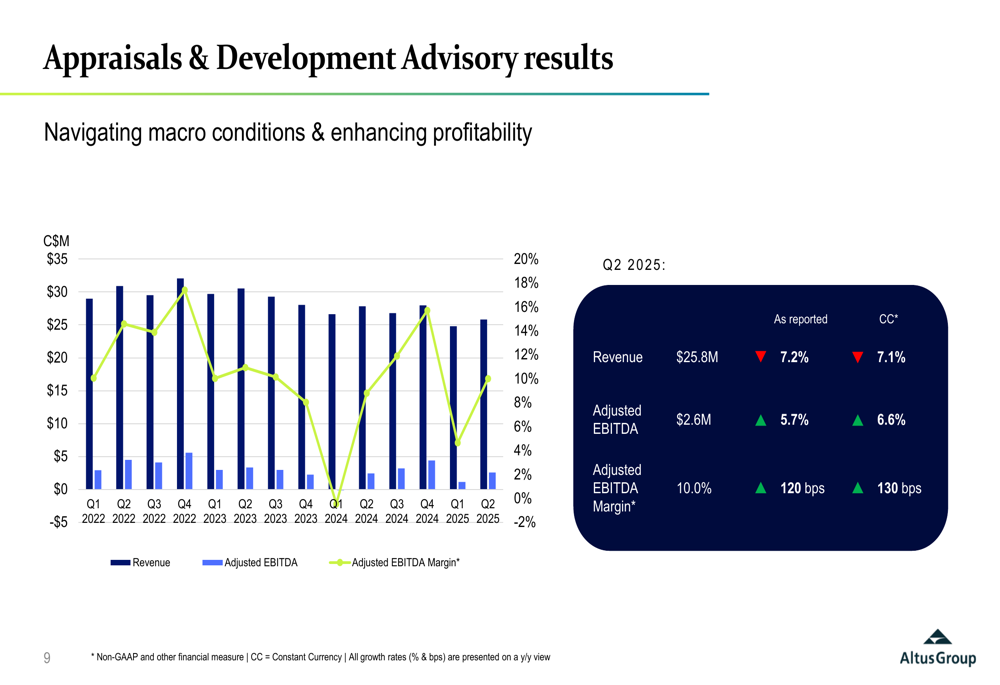

The Appraisals & Development Advisory segment faced headwinds, with revenue declining 7.2% to $25.8 million. However, the segment managed to improve profitability, with adjusted EBITDA increasing 5.7% to $2.6 million and margin expanding 120 basis points to 10.0%.

The performance of this segment is shown here:

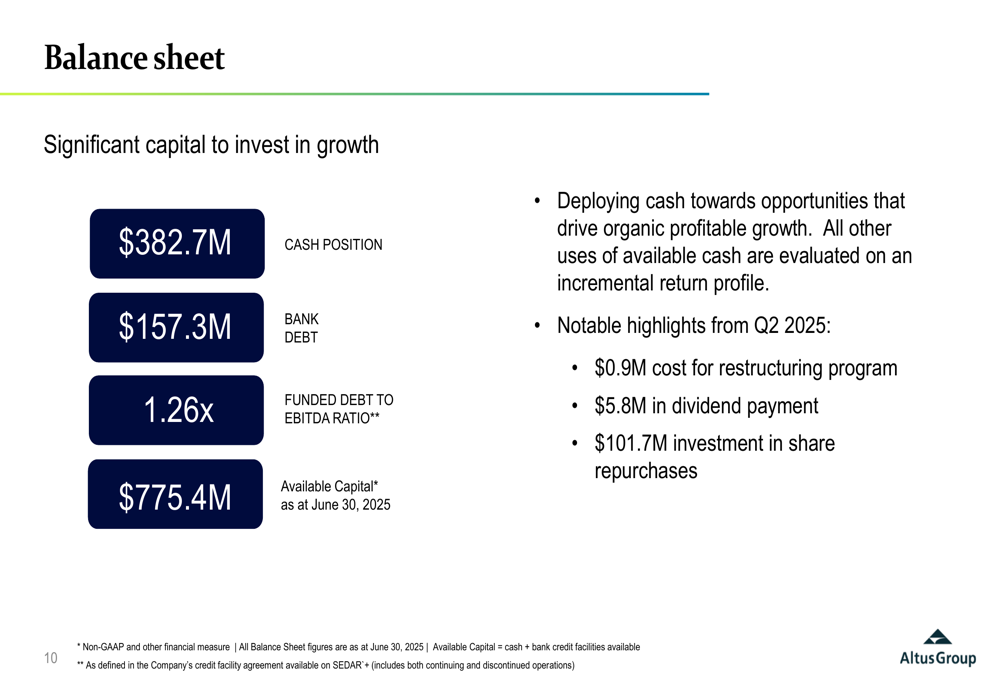

Strong Balance Sheet and Capital Allocation

Altus Group maintained a robust financial position with $382.7 million in cash and $157.3 million in bank debt as of June 30, 2025, resulting in a funded debt to EBITDA ratio of 1.26x. The company has $775.4 million in available capital to invest in growth opportunities.

During Q2, Altus Group deployed $101.7 million toward share repurchases, exhausting its 2025 buyback program which totaled approximately $179 million year-to-date. These repurchases reduced shares outstanding by 6.5% year-over-year. The company also paid $5.8 million in dividends during the quarter.

The following slide summarizes the company’s balance sheet position:

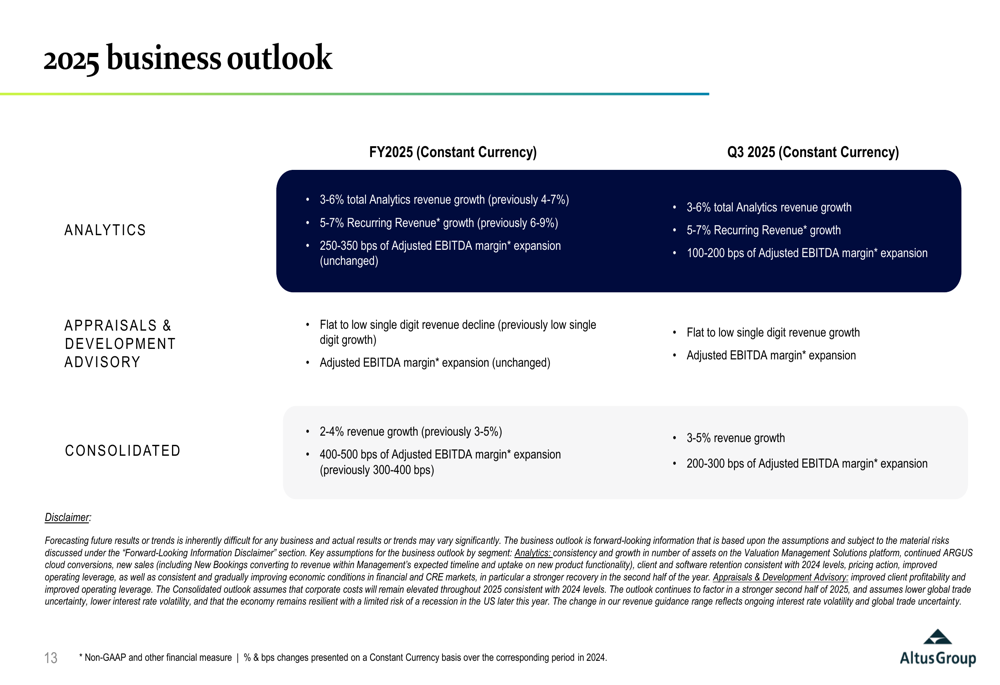

Revised Outlook for 2025

Altus Group revised its full-year 2025 guidance, lowering revenue growth expectations while raising margin expansion targets. The company now projects:

- Analytics revenue growth of 3-6% (down from previous 4-7%)

- Analytics recurring revenue growth of 5-7% (down from previous 6-9%)

- Appraisals & Development Advisory segment to see flat to low single-digit revenue decline (previously expected low single-digit growth)

- Consolidated revenue growth of 2-4% (down from previous 3-5%)

- Consolidated adjusted EBITDA margin expansion of 400-500 basis points (up from previous 300-400 bps)

For Q3 2025, Altus Group expects:

- 3-5% consolidated revenue growth

- 200-300 basis points of adjusted EBITDA margin expansion

The company’s updated outlook is detailed in this slide:

Market Reaction and Analysis

Despite the strong profit growth and margin expansion, Altus Group’s stock fell 8.72% following the earnings release. This negative reaction appears to be driven by the downward revision in revenue growth guidance, which may have raised concerns about the company’s long-term growth trajectory.

The reduction in revenue guidance for both the Analytics segment and the overall business, combined with the expected decline in the Appraisals & Development Advisory segment, suggests that macroeconomic challenges may be impacting the company more than previously anticipated.

However, the significant improvement in profitability metrics and the company’s ability to expand margins even in a challenging revenue environment demonstrate effective cost management and operational efficiency. The strong balance sheet and robust cash generation also provide flexibility for future investments and shareholder returns.

Altus Group announced it will hold an Investor Day on November 20, 2025, in New York City, where it is expected to provide more details on its long-term strategy and growth initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.