US LNG exports surge but will buyers in China turn up?

Introduction & Market Context

Ambac Financial Group, Inc. (NYSE:AMBC) released its first quarter 2025 investor presentation on May 13, highlighting strong growth in its insurance distribution segment while making progress on its strategic transformation. The company, which is pivoting from its legacy financial guarantee business to specialty property and casualty insurance, reported a 27% increase in total revenue to approximately $63 million.

The presentation emphasized Ambac’s continued execution of its strategic plan, including the completion of all pre-closing conditions for the sale of its legacy business to funds managed by Oaktree Capital Management, a transaction that will allow the company to focus entirely on its specialty P&C distribution and underwriting operations.

Quarterly Performance Highlights

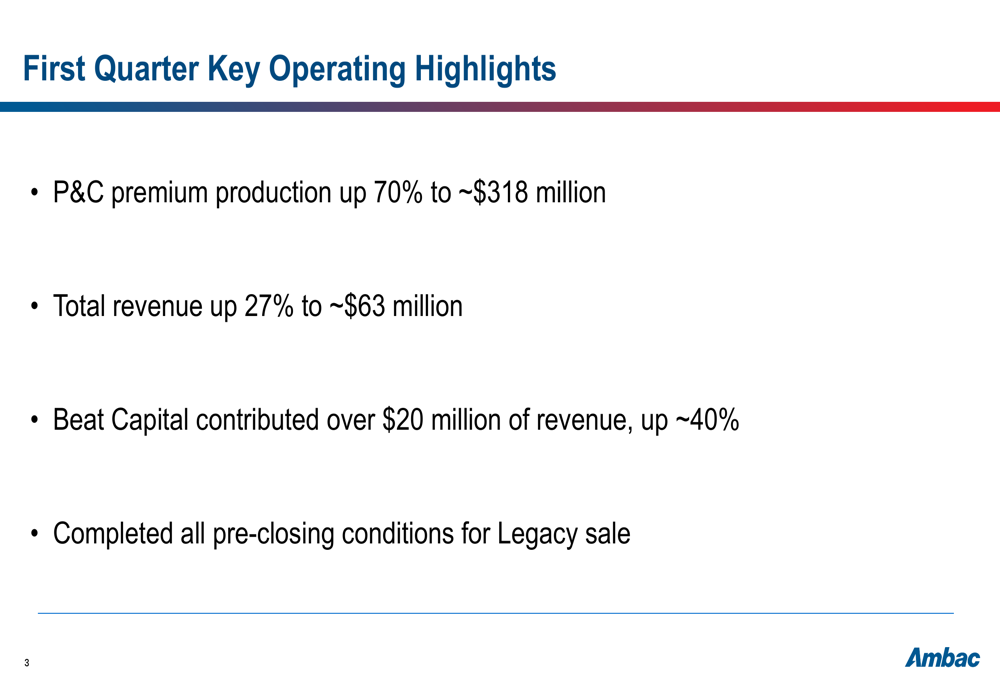

Ambac reported several key operating highlights for the first quarter of 2025, demonstrating significant growth in premium production and revenue generation across its business segments.

As shown in the following summary of key operating metrics:

The company’s P&C premium production increased by 70% year-over-year to approximately $318 million, while total revenue grew 27% to approximately $63 million. Beat Capital, one of Ambac’s strategic investments, contributed over $20 million of revenue, representing growth of approximately 40% compared to the prior year.

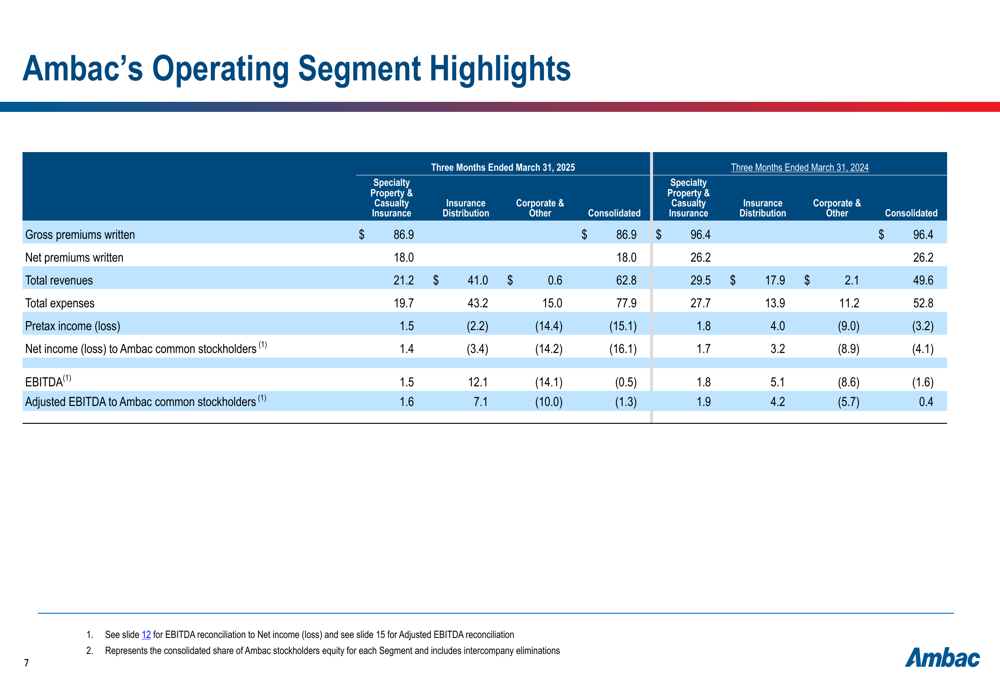

A detailed breakdown of Ambac’s operating segments reveals mixed performance across the business:

Consolidated results for the three months ended March 31, 2025, showed total revenues of $62.8 million and total expenses of $77.9 million, resulting in a pretax loss of $15.1 million. Net loss to Ambac common stockholders was $16.1 million, compared to a net loss of $4.1 million in the same period of 2024. The company reported negative EBITDA of $0.5 million and negative Adjusted EBITDA to Ambac common stockholders of $1.3 million.

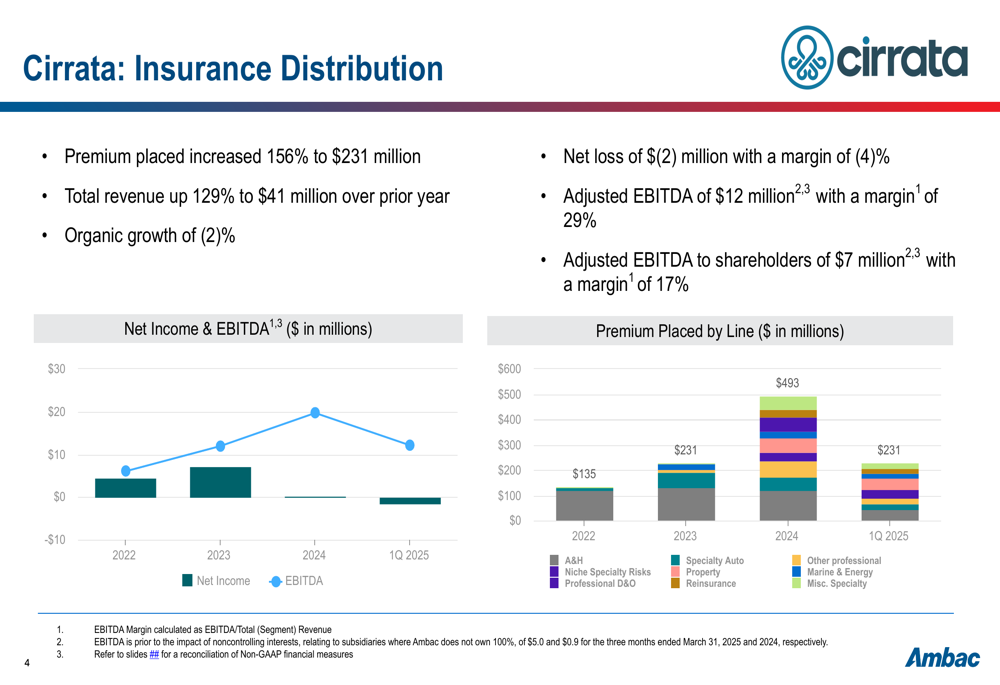

Segment Analysis: Cirrata Insurance Distribution

Ambac’s insurance distribution segment, Cirrata, delivered exceptional growth during the quarter, with premium placed increasing 156% to $231 million and total revenue up 129% to $41 million compared to the prior year.

The following chart illustrates Cirrata’s performance metrics and premium growth by line of business:

Despite the impressive top-line growth, Cirrata reported a net loss of $2 million with a margin of (4)%. However, the segment generated Adjusted EBITDA of $12 million with a margin of 29%, and Adjusted EBITDA to shareholders of $7 million with a margin of 17%. The segment’s organic growth was slightly negative at (2)%, suggesting that acquisitions drove most of the revenue increase.

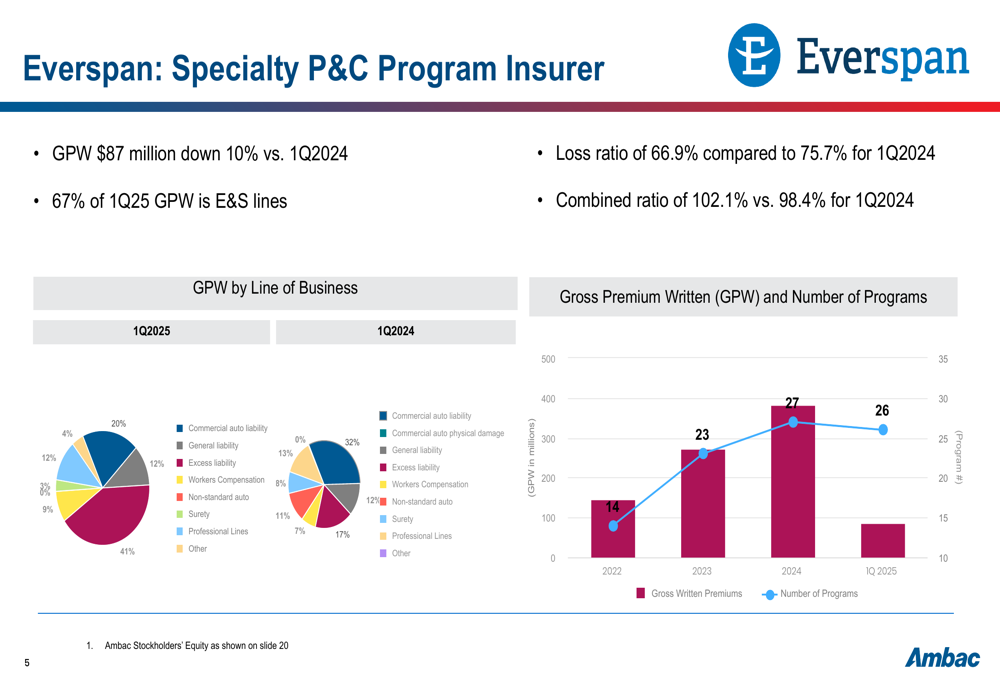

Segment Analysis: Everspan Specialty P&C

Everspan, Ambac’s specialty P&C program insurer, showed more mixed results for the quarter. Gross premiums written (GPW) declined 10% year-over-year to $87 million, with 67% of Q1 2025 GPW coming from excess and surplus (E&S) lines.

The following chart details Everspan’s performance metrics and premium distribution:

On a positive note, Everspan’s loss ratio improved to 66.9% from 75.7% in Q1 2024, indicating better underwriting performance. However, the combined ratio deteriorated slightly to 102.1% from 98.4% in the prior-year period, suggesting increased expenses relative to premiums earned.

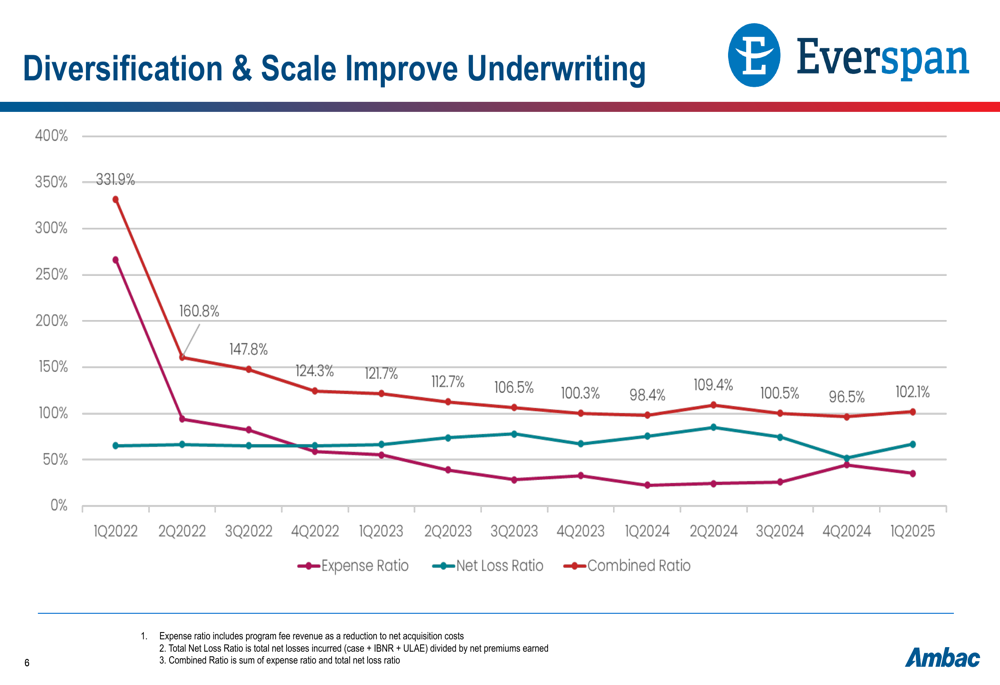

Ambac highlighted how diversification and scale have been improving Everspan’s underwriting performance over time, as illustrated in this trend chart:

The chart demonstrates a significant improvement in Everspan’s combined ratio from over 300% in early 2022 to around 102% in Q1 2025, reflecting the benefits of increased scale and diversification across programs and lines of business.

Strategic Initiatives and Financial Outlook

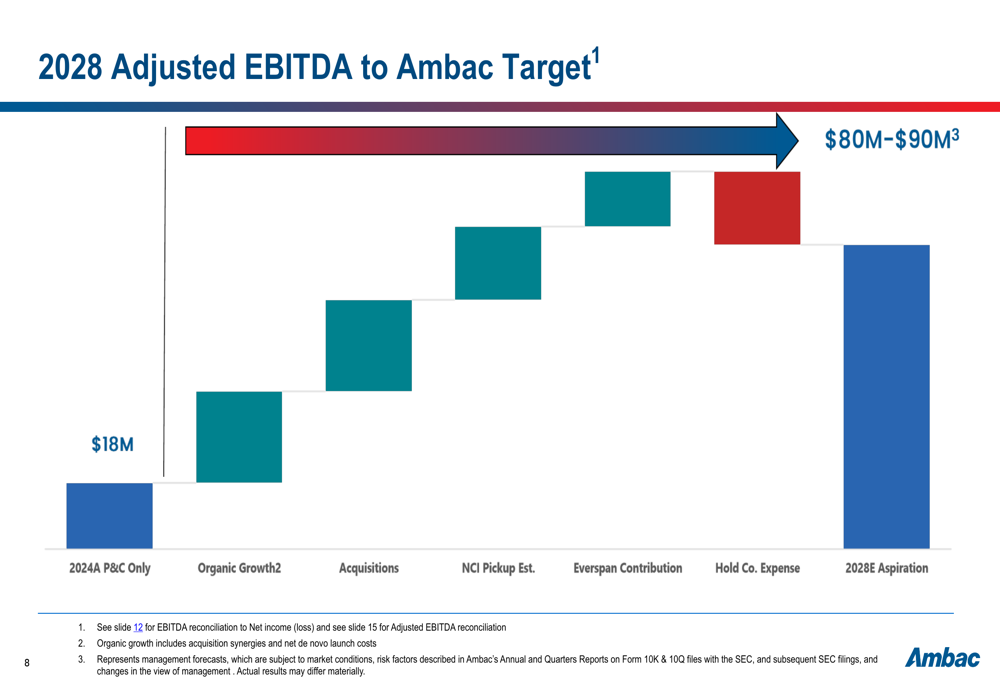

Ambac outlined its path to achieving its 2028 Adjusted EBITDA target of $80-90 million, starting from a 2024 P&C-only base of $18 million. The company plans to reach this target through a combination of organic growth, acquisitions, and improved performance from Everspan.

The following waterfall chart illustrates the company’s roadmap to its 2028 EBITDA target:

A key strategic milestone highlighted in the presentation was the completion of all pre-closing conditions for the sale of Ambac’s legacy financial guarantee business. This transaction, once finalized, will allow the company to focus entirely on growing its specialty P&C distribution and underwriting operations.

Forward-Looking Statements

While Ambac’s presentation painted an optimistic picture of its growth trajectory, investors should note that the company continues to report net losses despite revenue growth. The transition from a legacy financial guarantee business to a specialty P&C insurer remains ongoing, with profitability challenges still evident in the current financial results.

The company’s strategy relies heavily on continued organic growth, successful integration of acquisitions, and improved underwriting performance at Everspan to achieve its 2028 EBITDA targets. Execution risks remain, particularly in maintaining growth momentum in the insurance distribution segment while simultaneously improving profitability metrics across the business.

As Ambac completes the sale of its legacy business and focuses on its specialty P&C operations, investors will be watching closely for signs of sustainable profitability and continued progress toward the company’s long-term financial goals.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.