D-Wave Quantum falls nearly 3% as earnings miss overshadows revenue beat

Introduction & Market Context

Ameresco (NYSE:AMRC) released its second quarter 2025 supplemental information on August 4, revealing strong performance driven by its recurring revenue streams and substantial project backlog. The clean energy solutions provider’s stock responded positively, rising 4.16% in aftermarket trading to $16.53, continuing its recovery from a 52-week low of $8.49.

The presentation comes after a stronger-than-expected Q1 2025, where the company beat earnings estimates with a narrower-than-anticipated loss of $0.11 per share versus the forecasted $0.16 loss. The Q2 results further solidify Ameresco’s recovery trajectory, with the stock now up significantly from its recent lows despite remaining 66.1% below its six-month high.

Quarterly Performance Highlights

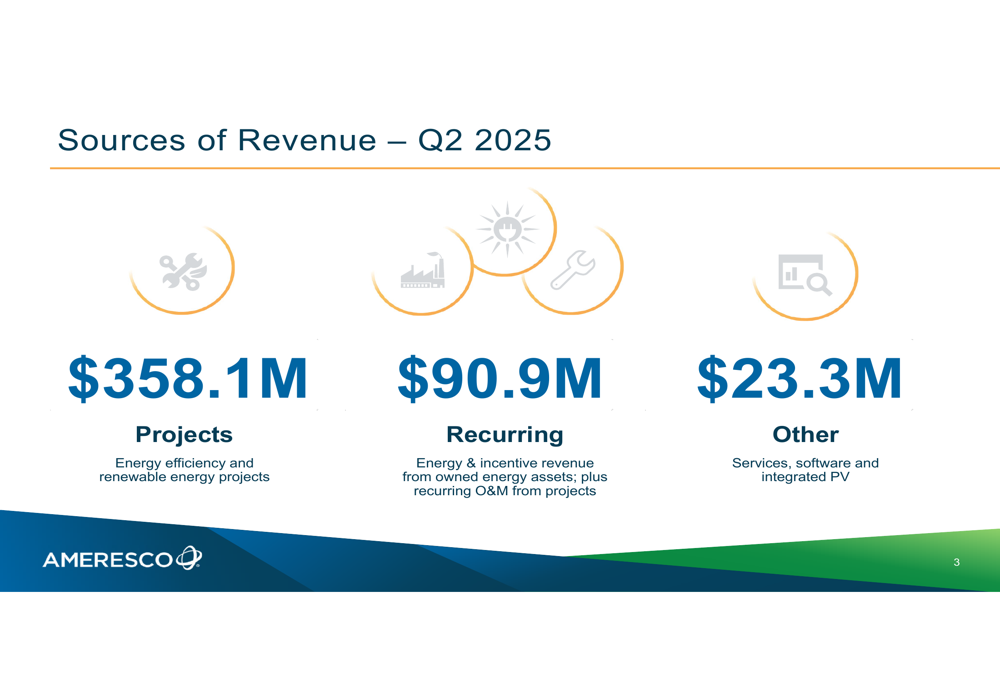

Ameresco reported Q2 2025 total revenue of $472.3 million, with the majority coming from projects at $358.1 million (76%). Recurring revenue contributed $90.9 million (19%), while other services added $23.3 million (5%). This performance continues the momentum from Q1, where revenue grew 18% year-over-year to $352.8 million.

As shown in the following breakdown of revenue sources for Q2 2025:

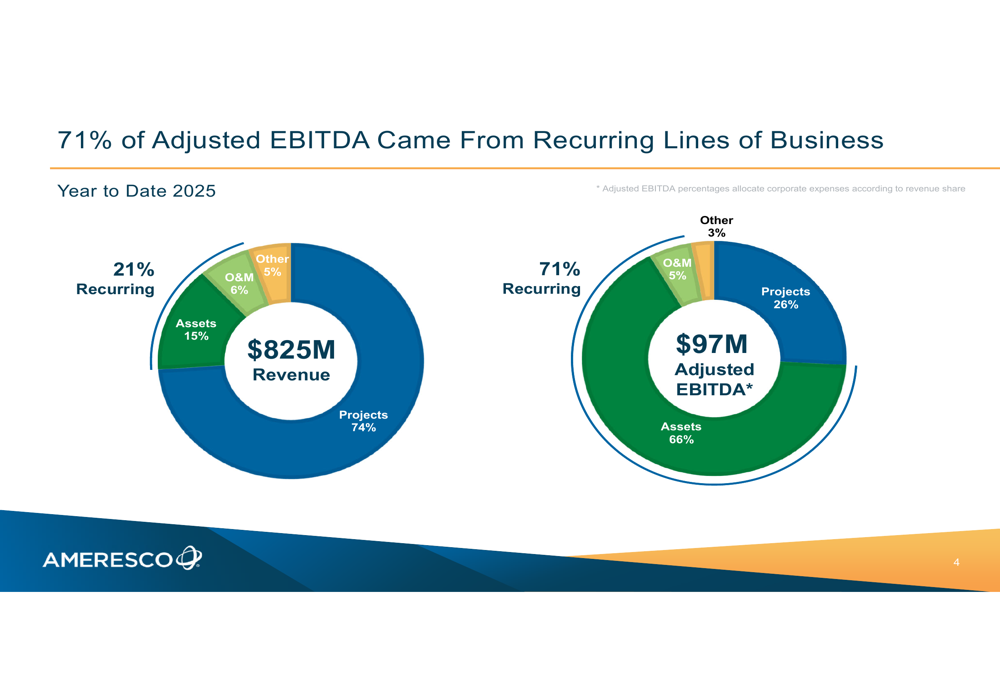

Year-to-date, the company has generated $825 million in revenue, with projects accounting for 74%, energy assets 15%, operations and maintenance 6%, and other services 5%. More impressively, recurring lines of business contributed 71% of the company’s adjusted EBITDA for the first half of 2025, highlighting Ameresco’s successful shift toward more stable, predictable revenue streams.

The following chart illustrates how Ameresco’s business model is increasingly weighted toward recurring revenue for profitability:

Energy Asset Portfolio

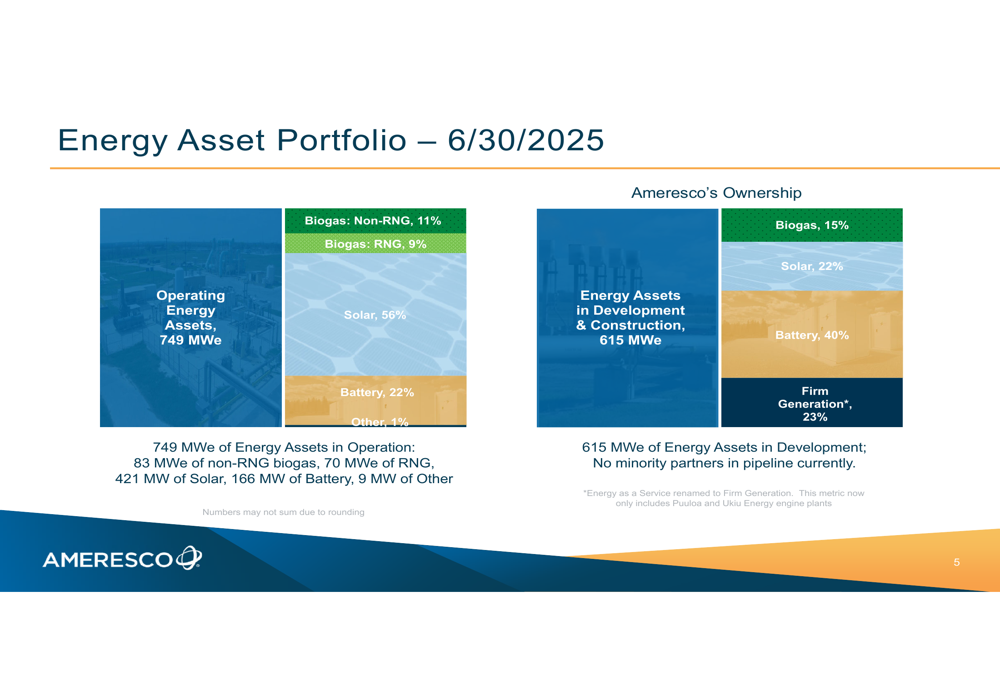

A key driver of Ameresco’s recurring revenue is its growing portfolio of owned energy assets. As of June 30, 2025, the company’s operating energy assets totaled 749 MWe, with solar representing the largest portion at 56%, followed by battery storage (22%), non-RNG biogas (11%), RNG biogas (9%), and other assets (1%).

The company is actively expanding this portfolio, with 615 MWe of energy assets currently in development and construction. This pipeline is diversified across battery storage (40%), firm generation (23%), solar (22%), and biogas (15%), positioning Ameresco for continued growth in recurring revenue.

The following chart shows the breakdown of Ameresco’s current and developing energy asset portfolio:

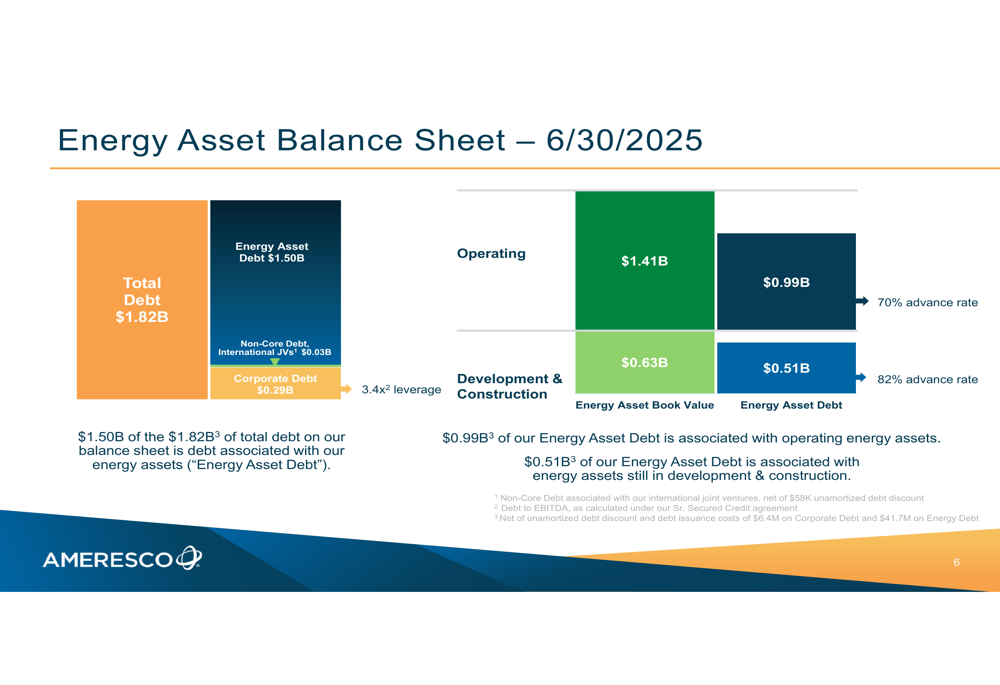

To finance this growth, Ameresco maintains a structured approach to its balance sheet. The company reported total debt of $1.82 billion as of June 30, 2025, with $1.50 billion in energy asset debt, $0.29 billion in corporate debt, and $0.03 billion in non-core debt related to international joint ventures. The company’s debt-to-EBITDA leverage ratio stands at 3.4x, which management considers appropriate given the long-term contracted nature of its assets.

The following chart details Ameresco’s energy asset balance sheet structure:

Project Backlog and Future Visibility

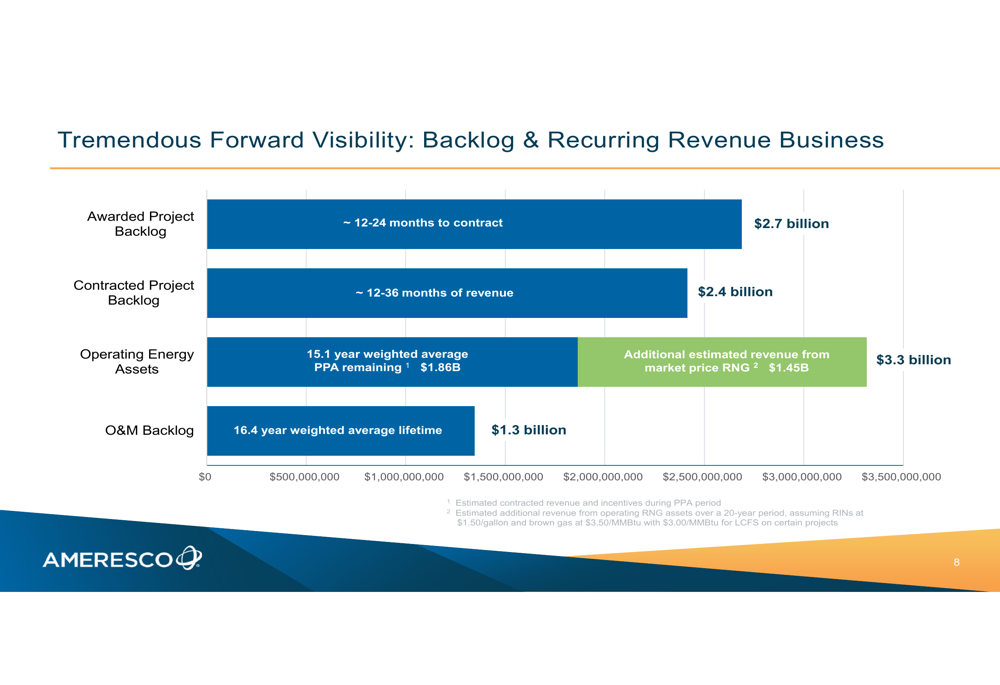

One of the most compelling aspects of Ameresco’s business model is its substantial backlog, which provides excellent visibility into future revenue. As of Q2 2025, the company reported a total project backlog of $5.1 billion, consisting of $2.7 billion in awarded projects (expected to convert to contracts within 12-24 months) and $2.4 billion in contracted projects (expected to generate revenue over the next 12-36 months).

Beyond projects, Ameresco’s operating energy assets have a weighted average power purchase agreement (PPA) remaining term of 15.1 years, representing $1.86 billion in contracted revenue. The company estimates an additional $1.45 billion in potential revenue from market-priced renewable natural gas (RNG). Additionally, the operations and maintenance backlog stands at $1.3 billion with a weighted average lifetime of 16.4 years.

The following chart illustrates Ameresco’s substantial backlog and recurring revenue visibility:

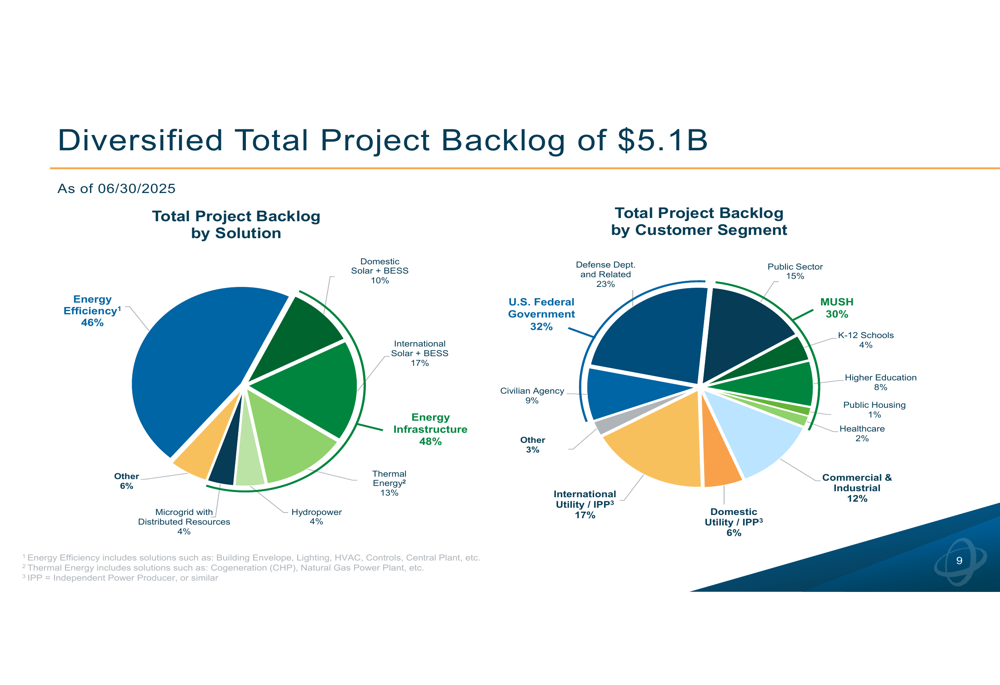

This backlog is well-diversified across both solution types and customer segments. By solution, energy efficiency projects represent 46% of the backlog, with energy infrastructure at 48%. By customer segment, the U.S. federal government accounts for 32%, followed by MUSH (municipalities, universities, schools, and hospitals) at 30%, and international utility/IPP projects at 17%.

The following chart demonstrates the diversification of Ameresco’s project backlog:

Financial Outlook

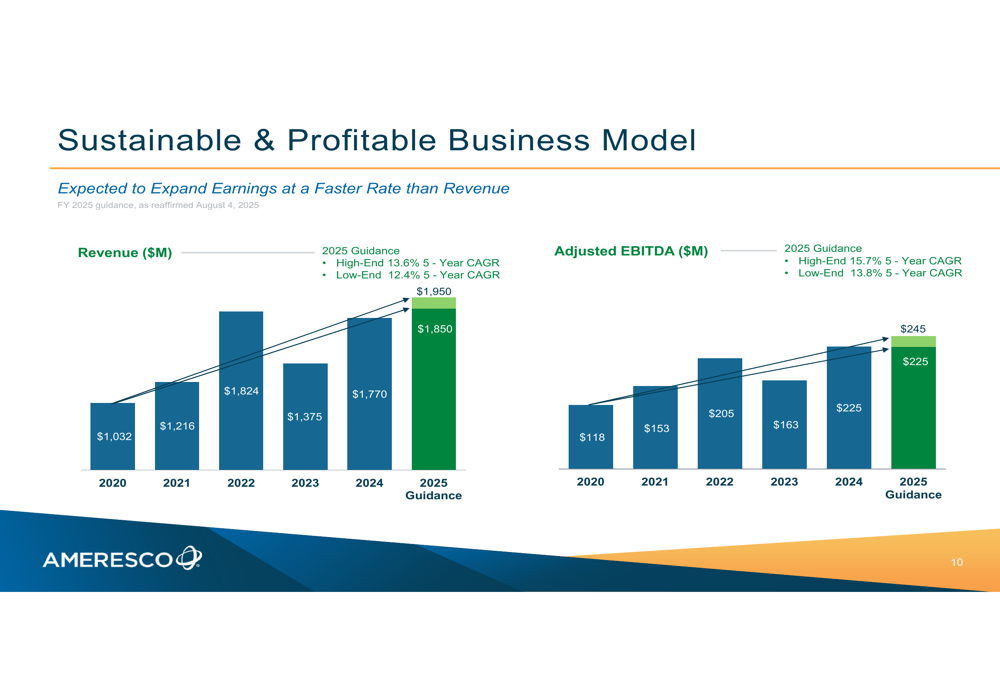

Ameresco’s presentation reaffirmed its 2025 guidance, projecting revenue between $1.85 billion and $1.95 billion and adjusted EBITDA between $225 million and $245 million. This represents a five-year compound annual growth rate (CAGR) of 12.4% to 13.6% for revenue and 13.8% to 15.7% for adjusted EBITDA from 2020 to 2025.

The company’s business model is designed to expand earnings at a faster rate than revenue, as demonstrated by the higher CAGR for adjusted EBITDA compared to revenue. This aligns with the company’s Q1 earnings call, where management indicated that approximately 60% of total 2025 revenue is expected in the second half of the year.

The following chart shows Ameresco’s historical and projected revenue and adjusted EBITDA growth:

Environmental Impact

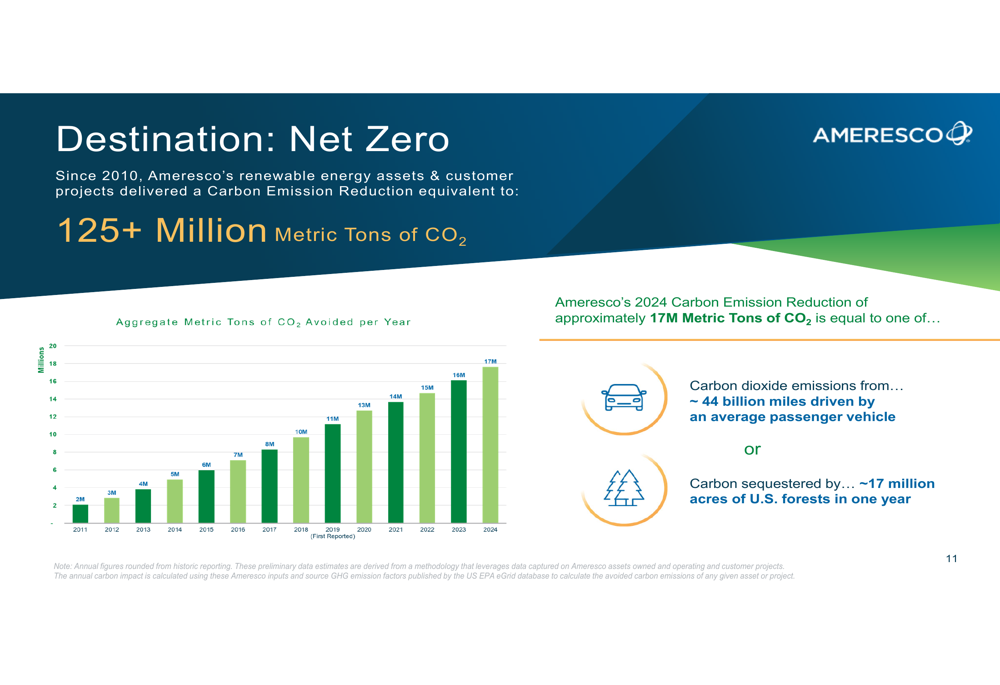

Beyond financial performance, Ameresco highlighted its environmental impact. Since 2010, the company’s renewable energy assets and customer projects have delivered carbon emission reductions equivalent to more than 125 million metric tons of CO2. In 2024 alone, Ameresco’s initiatives reduced carbon emissions by approximately 17 million metric tons, equivalent to the emissions from 44 billion miles driven by an average passenger vehicle or the carbon sequestered by 17 million acres of U.S. forests in one year.

The following chart illustrates Ameresco’s growing annual carbon reduction impact:

Forward-Looking Statements

While Ameresco’s presentation paints an optimistic picture, investors should consider potential challenges identified in the company’s Q1 earnings report, including supply chain disruptions, rising electricity costs, macroeconomic pressures affecting government and private sector spending, and integration challenges for renewable energy.

Nevertheless, with its diversified business model, substantial backlog, and growing portfolio of long-term contracted assets, Ameresco appears well-positioned to continue its recovery and growth trajectory through the remainder of 2025 and beyond. The positive market reaction to both Q1 and now Q2 results suggests growing investor confidence in the company’s strategy and execution.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.