ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

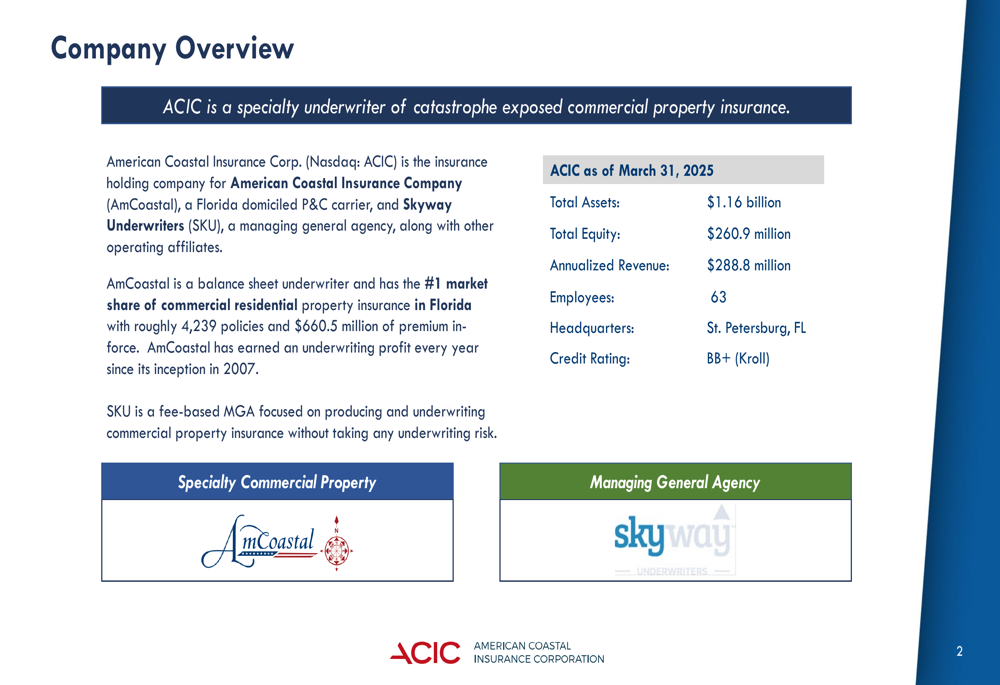

American Coastal Insurance Corporation (ACIC), a specialty underwriter of catastrophe-exposed commercial property insurance, presented its first quarter 2025 earnings results on May 8, 2025. The company maintained its position as the leading provider of commercial residential property insurance in Florida with approximately 4,239 policies and $660.5 million of premium in-force, despite facing a softening market environment.

The Florida-based insurer continues to leverage its expertise in catastrophe risk management while navigating market challenges. ACIC operates through two main subsidiaries: American Coastal Insurance Company (AmCoastal), a Florida-domiciled P&C carrier, and Skyway Underwriters (SKU), a fee-based managing general agency focused on commercial property insurance.

As shown in the company overview slide:

Quarterly Performance Highlights

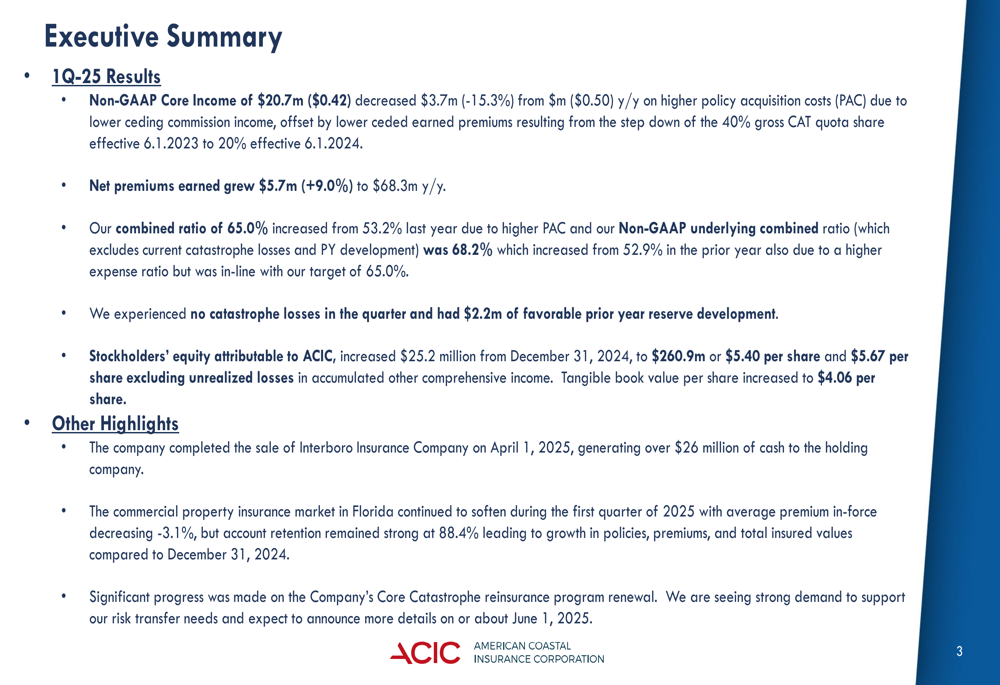

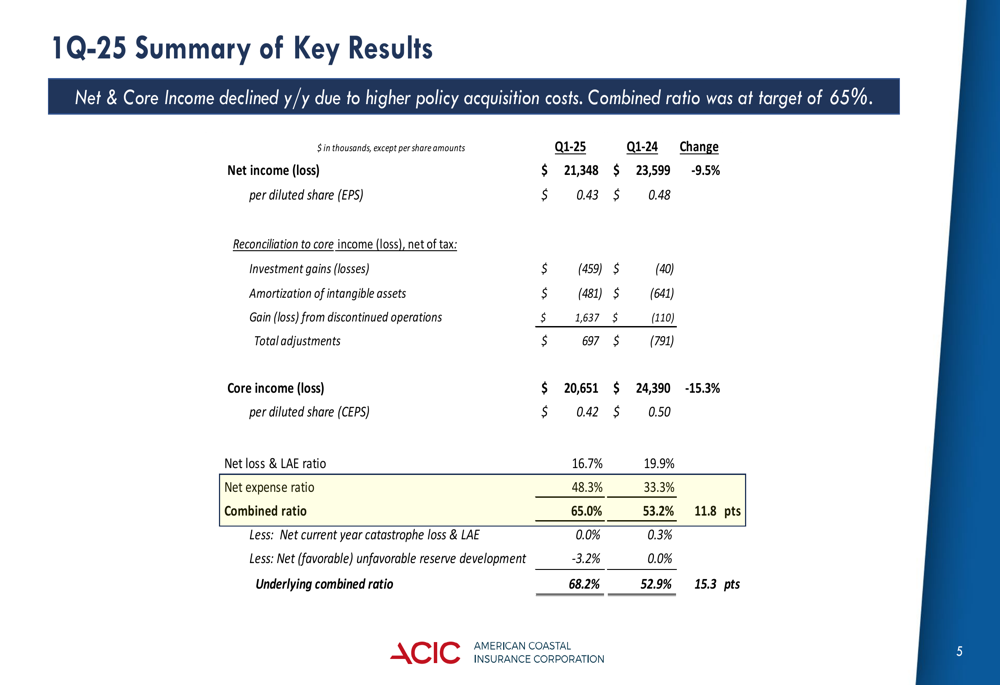

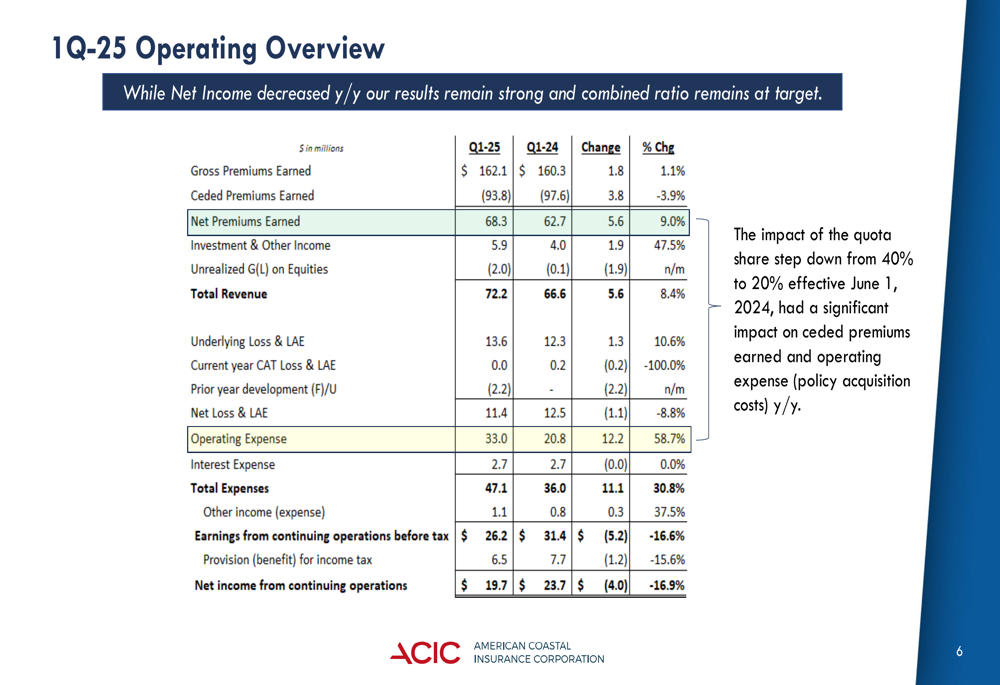

ACIC reported a decrease in Non-GAAP Core Income to $20.7 million ($0.42 per share) in Q1 2025, down from $24.4 million ($0.50 per share) in the same period last year. Despite this decline, the company achieved 9.0% growth in net premiums earned, reaching $68.3 million. The combined ratio increased to 65.0% from 53.2% year-over-year, while the underlying combined ratio rose to 68.2% from 52.9%.

The company’s executive summary highlights these key metrics along with other significant developments:

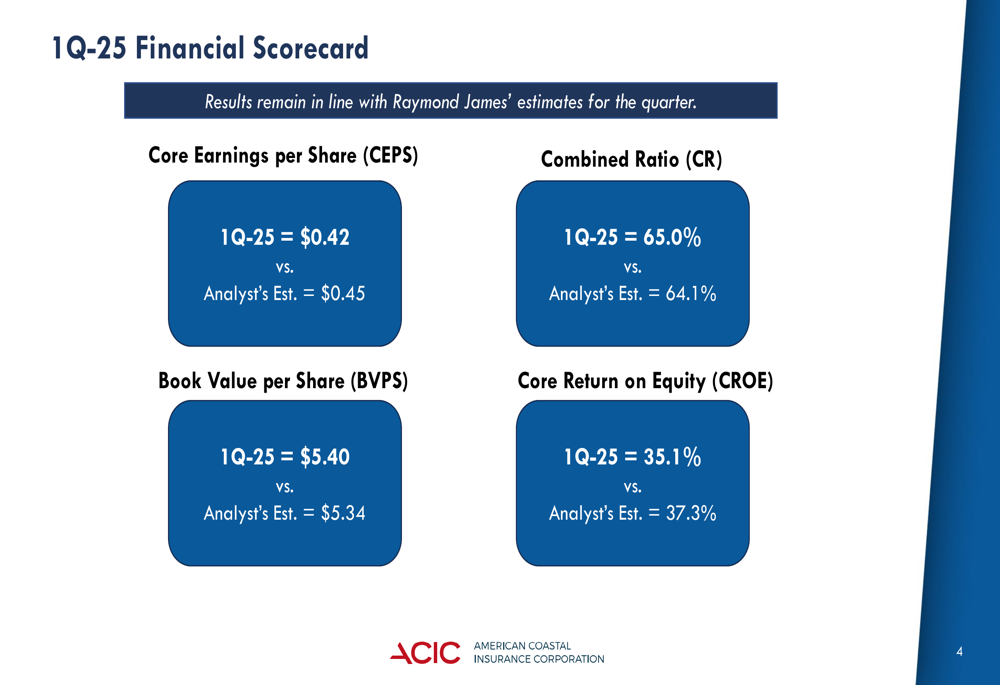

When measured against analyst expectations, ACIC’s performance was mixed. Core Earnings per Share came in at $0.42 versus an analyst estimate of $0.45, while Book Value per Share exceeded expectations at $5.40 compared to the estimated $5.34. The company’s Core Return on Equity reached 35.1%, slightly below the analyst estimate of 37.3%.

Detailed Financial Analysis

A closer examination of ACIC’s financial results reveals that the year-over-year decline in core income was primarily attributed to higher policy acquisition costs. The net loss and LAE ratio improved to 16.7% from 19.9% in Q1 2024, but this was offset by an increase in the net expense ratio to 48.3% from 33.3%. The company experienced no catastrophe losses during the quarter and benefited from $2.2 million in favorable prior year reserve development.

The following summary provides a comprehensive view of key financial metrics:

ACIC’s operating overview demonstrates that while net income decreased year-over-year, results remain strong with the combined ratio at the company’s target level. A significant factor affecting year-over-year comparisons was the impact of the quota share step down from 40% to 20% effective June 1, 2024, which substantially influenced ceded premiums earned and operating expenses (particularly policy acquisition costs).

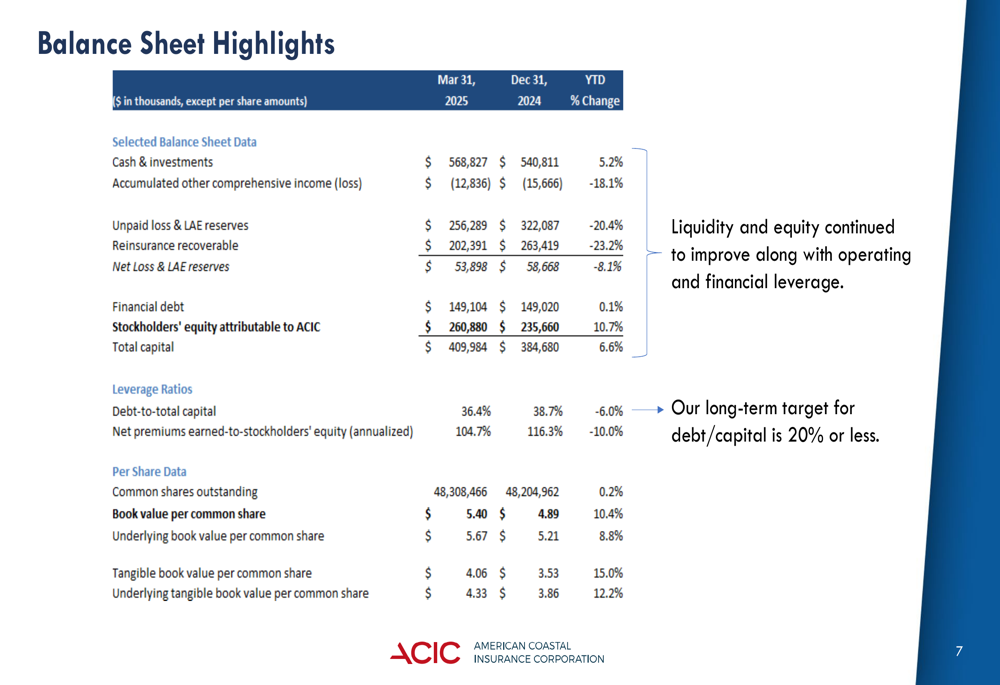

From a balance sheet perspective, ACIC reported continued improvement in liquidity and equity, along with operating and financial leverage. Total (EPA:TTEF) assets reached $1.16 billion, with cash and investments totaling $568.8 million as of March 31, 2025. Stockholders’ equity attributable to ACIC stood at $260.9 million, translating to a book value per common share of $5.40 ($5.67 excluding unrealized losses).

Strategic Initiatives & Reinsurance Strategy

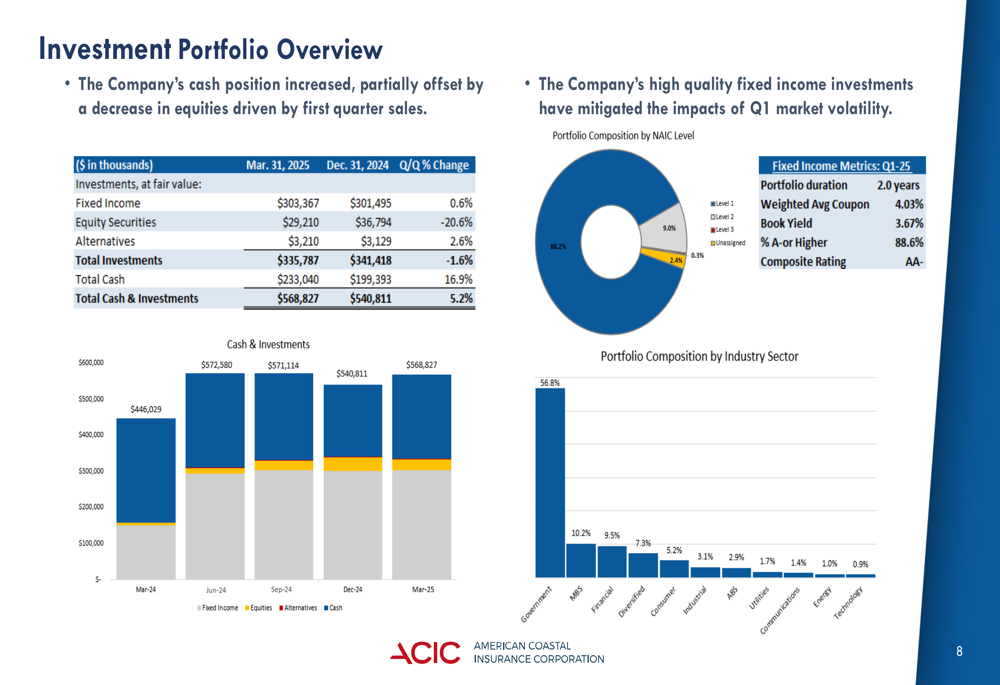

ACIC’s investment portfolio strategy shows a conservative approach with a focus on high-quality fixed income securities. As of March 31, 2025, the company held $303.4 million in fixed income investments, $29.2 million in equity securities, and $3.2 million in alternatives. The fixed income portfolio maintains a relatively short duration of 2.0 years with 88.6% of holdings rated A or higher. Government securities represent the largest sector allocation at 56.8%.

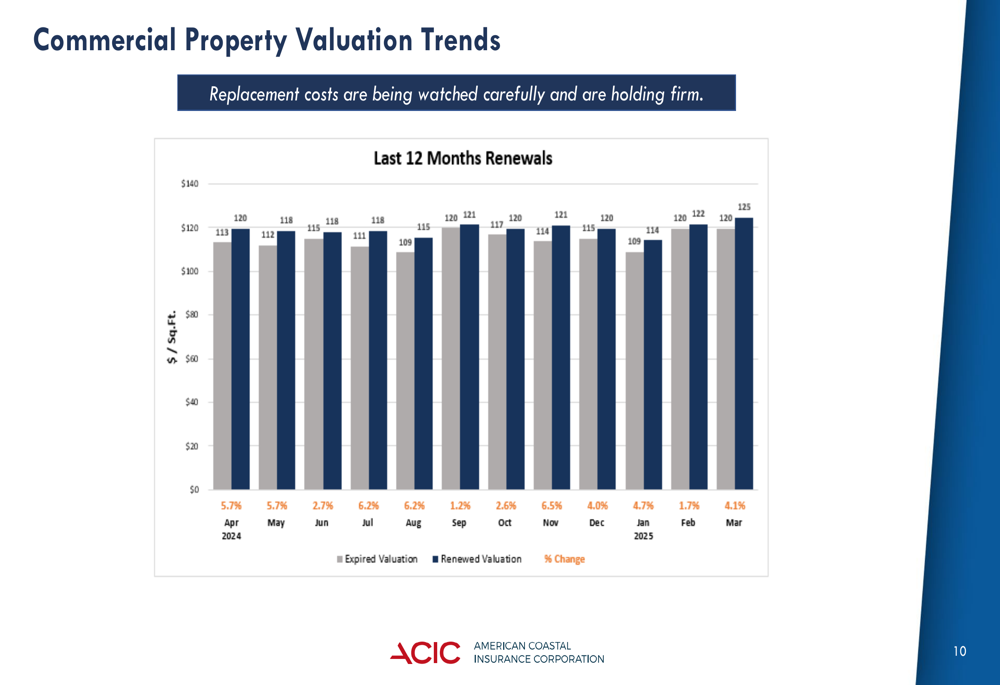

In response to market conditions, ACIC has been closely monitoring commercial property valuation trends. The company’s data indicates that replacement costs are holding firm, with valuation increases ranging from 1.2% to 6.5% over the past 12 months for renewed policies.

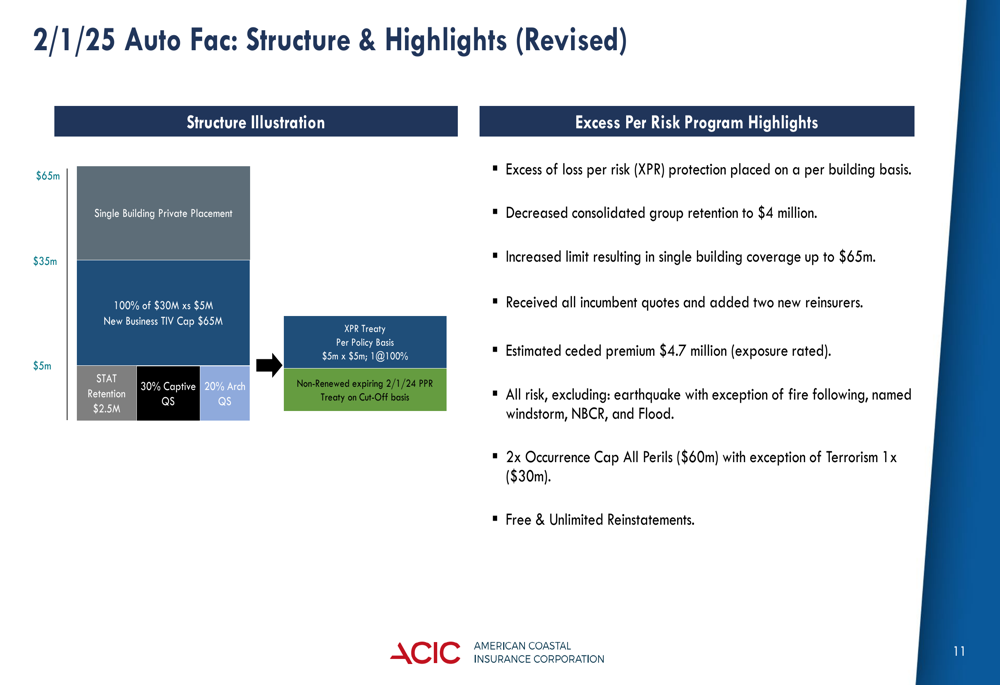

A cornerstone of ACIC’s strategy is its sophisticated reinsurance program. The company has restructured its Auto Fac reinsurance program effective February 1, 2025, decreasing the consolidated group retention to $4 million while increasing coverage limits to provide up to $65 million in single building coverage. This excess of loss per risk protection is placed on a per building basis with an estimated ceded premium of $4.7 million.

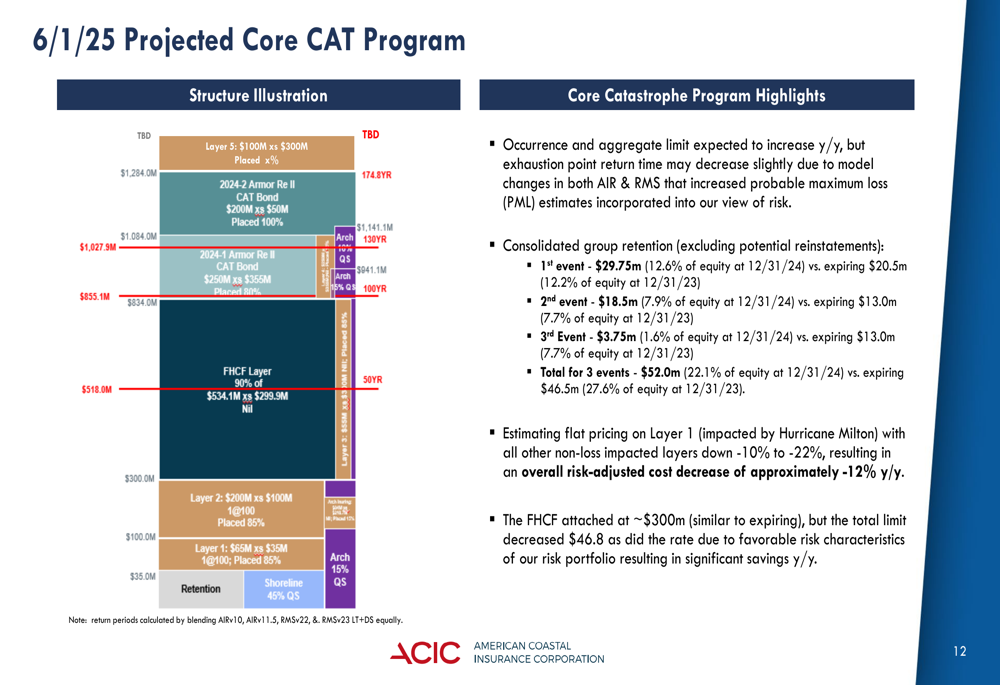

Looking ahead, ACIC’s projected Core Catastrophe reinsurance program for June 1, 2025, is expected to feature increased occurrence and aggregate limits year-over-year. The company anticipates flat pricing on Layer 1, with the Florida Hurricane Catastrophe Fund attaching at approximately $300 million.

Forward-Looking Statements

Despite the softening commercial property insurance market in Florida, with average premium in-force decreasing by 3.1%, ACIC appears well-positioned to navigate these challenges. The company completed the sale of Interboro Insurance Company on April 1, 2025, generating over $26 million, which further strengthens its financial position.

According to the earnings call transcript, CEO Bennett Bradford Martz highlighted the company’s approximately 6% growth in policies in force since year-end, emphasizing a cautious approach to portfolio building. The company has also launched a new apartment building insurance initiative targeting Central and Northeast Florida, which represents a strategic diversification effort not explicitly detailed in the presentation slides.

ACIC’s reinsurance program is set for renewal with increased protection and decreased rates, with the catastrophe reinsurance program effective June 1, 2025, expected to include a 16% increase in the first event limit to $1.35 billion. The aggregate protection is projected to increase by 32%, while the risk-adjusted reinsurance rate is anticipated to decrease by approximately 12%.

With a strong market position, disciplined underwriting approach, and strategic reinsurance program, ACIC appears well-equipped to maintain its competitive edge in Florida’s commercial property insurance market despite the current softening conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.