Gold prices buoyed by tariff fears; US duties on 1-kilo bars spur supply concerns

Introduction & Market Context

AngloGold Ashanti Ltd ADR (NYSE:AU) presented its second-quarter 2025 earnings results on August 1, showcasing exceptional financial performance driven primarily by higher gold prices and disciplined operational execution. The gold producer capitalized on gold’s continued outperformance against most major asset classes, with the average realized gold price reaching $3,287 per ounce, a 41% increase year-over-year.

The company’s shares were trading down 2.51% at $46.25 in the previous session, with premarket activity showing a further slight decline of 0.43% to $46.05. Despite this short-term movement, AngloGold Ashanti’s stock has demonstrated significant strength over the past year, trading well above its 52-week low of $22.45.

Quarterly Performance Highlights

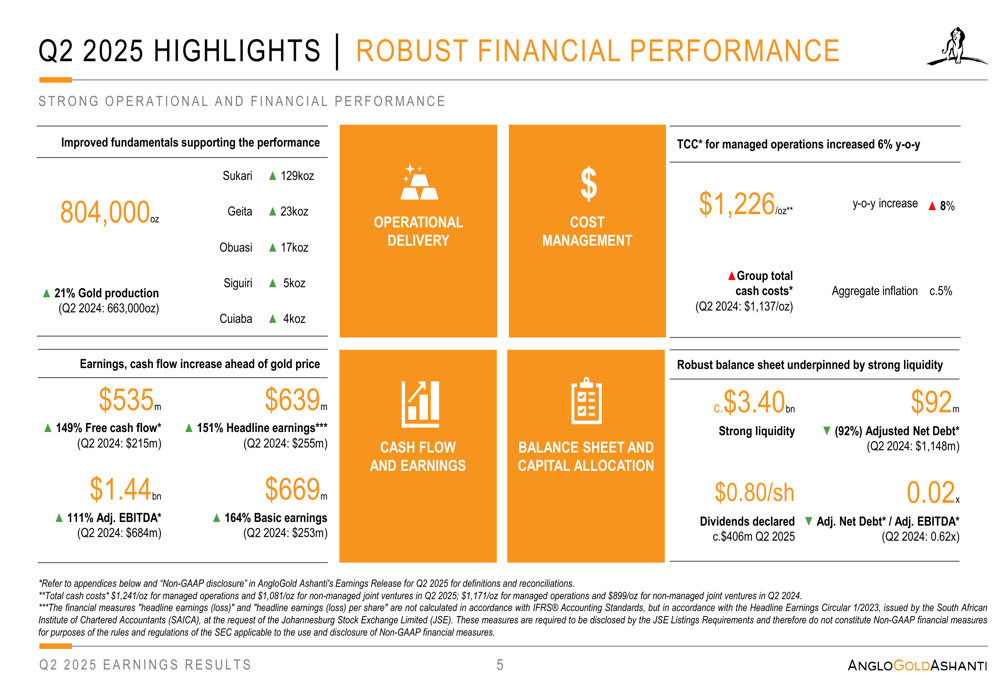

AngloGold Ashanti reported substantial improvements across all key financial metrics for Q2 2025, with gold production reaching 804,000 ounces, representing a 21% increase compared to the same period last year. This production growth, combined with higher gold prices, translated into exceptional financial results.

As shown in the following comprehensive financial summary:

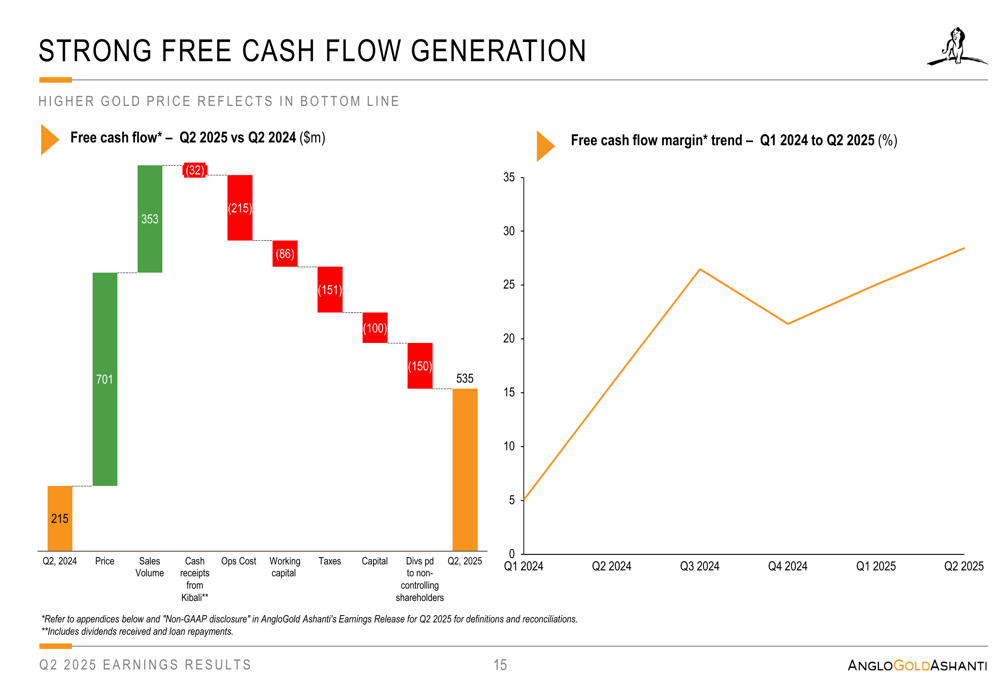

Free cash flow surged to $535 million, a 149% increase year-over-year, while headline earnings grew 151% to $639 million. Adjusted EBITDA more than doubled to $1.44 billion, representing a 111% increase from Q2 2024. The company maintained disciplined cost control despite inflationary pressures, with total cash costs for managed operations increasing by only 6% to $1,226 per ounce.

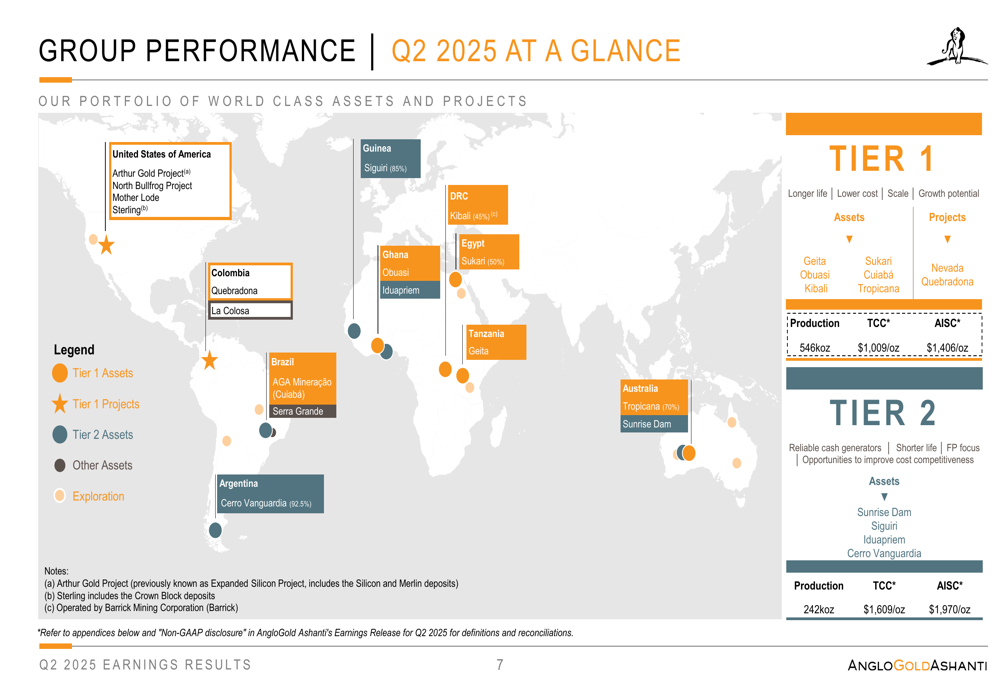

The company’s operational performance was supported by contributions from key assets, with the Sukari mine in Egypt being the largest contributor at 129,000 ounces. The company’s portfolio is strategically distributed across multiple geographies, as illustrated in this asset map:

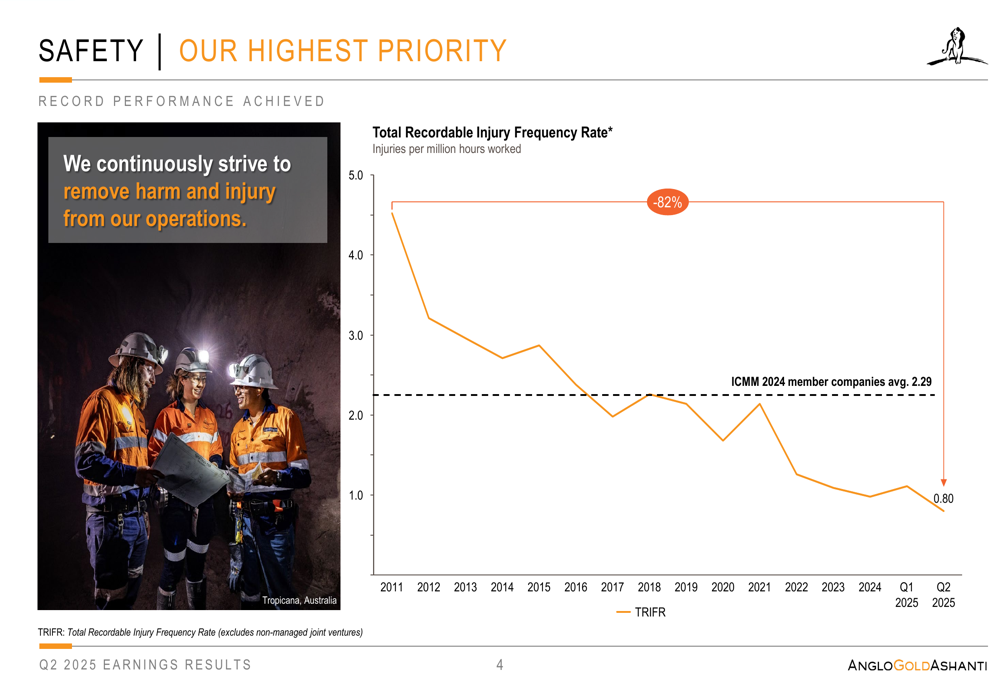

Safety performance continues to be a priority for AngloGold Ashanti, with the company achieving a Total (EPA:TTEF) Recordable Injury Frequency Rate (TRIFR) of 0.80 in Q2 2025, representing an 82% improvement since 2011 and significantly outperforming the industry average of 2.29 for ICMM member companies.

Strategic Growth Initiatives

AngloGold Ashanti outlined several strategic growth initiatives during the presentation, with particular emphasis on its expansion in Nevada’s Beatty District through the proposed $111 million acquisition of Augusta Gold. This strategic move consolidates the company’s position in one of North America’s premier gold mining regions.

"This acquisition enables AngloGold Ashanti to maximize value from the Beatty District by leveraging synergies and optimizing the development sequence," the company stated in its presentation. The deal adds the permitted Reward deposit with a completed feasibility-level study and establishes AngloGold Ashanti as the leading developer in the district with multiple Tier 1 prospects.

Beyond Nevada, the company highlighted progress at its Obuasi mine, where gold production increased 31% year-over-year to 71,000 ounces in Q2 2025. The operation is tracking around the midpoint of its 2025 guidance range of 250,000-300,000 ounces. Additional brownfield growth opportunities are being pursued across the portfolio, including at Cuiabá, Iduapriem, Siguiri, and Geita.

Balance Sheet Strength & Shareholder Returns

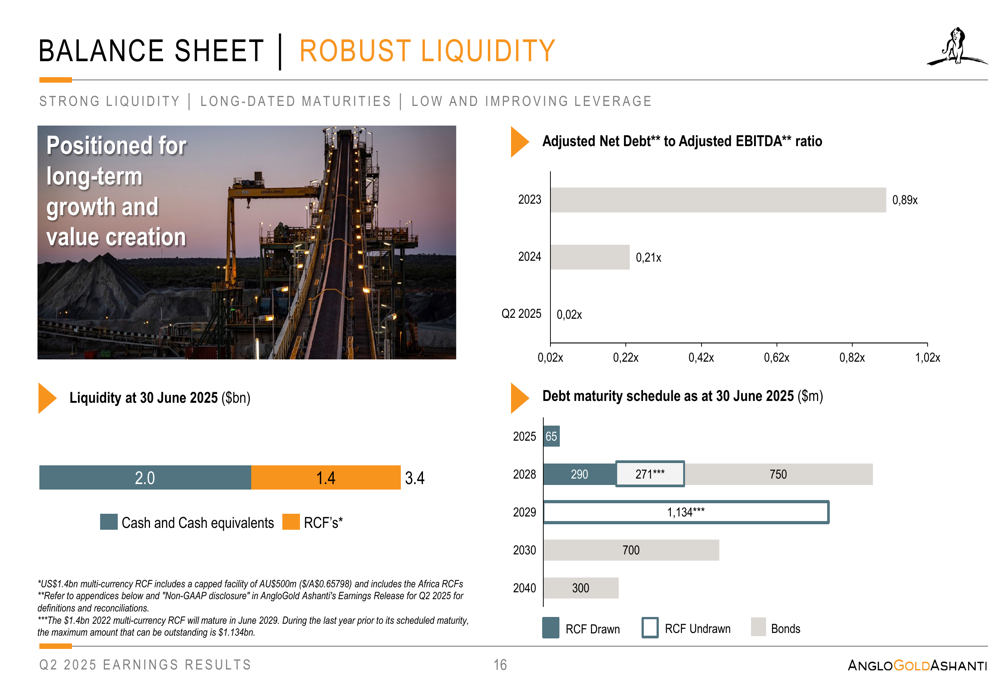

AngloGold Ashanti’s balance sheet has strengthened considerably, with adjusted net debt reduced by 92% to just $92 million. This dramatic improvement has resulted in an adjusted net debt to adjusted EBITDA ratio of only 0.02x, providing the company with significant financial flexibility.

The company’s robust liquidity position of approximately $3.4 billion and long-dated debt maturity profile further enhance its financial stability, as illustrated in this debt maturity schedule:

This financial strength has enabled AngloGold Ashanti to significantly increase shareholder returns, declaring a dividend of $0.80 per share ($406 million total). The company noted that this dividend "includes minimum + top-up for 50% of first six months of free cash flow," reflecting management’s confidence in sustained cash generation.

The free cash flow margin has shown consistent improvement, as demonstrated in the following chart:

Forward Guidance

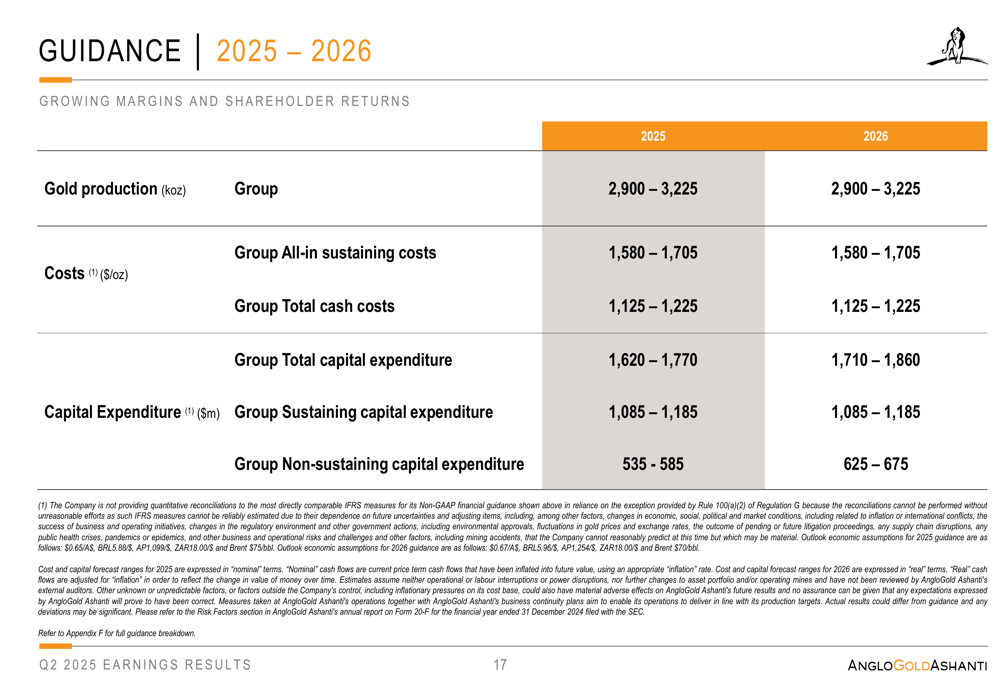

Looking ahead, AngloGold Ashanti maintained its production and cost guidance for 2025-2026, projecting annual gold production of 2,900,000-3,225,000 ounces for both years. All-in sustaining costs are expected to remain in the range of $1,580-$1,705 per ounce.

The company’s detailed guidance provides investors with clear expectations for the coming years:

Management emphasized that AngloGold Ashanti trades at an attractive valuation compared to North American peers, highlighting its compelling free cash flow and dividend yields. The company’s recent inclusion in the Russell 1000®, 3000®, and Midcap® indexes is expected to create broader appeal among U.S. institutional investors.

As summarized in the company’s concluding remarks, AngloGold Ashanti is focused on "delivering superior, predictable operating performance" through best-in-class safety practices, tier one production growth, and leading cost performance, while continuing to enhance capital returns through its robust balance sheet.

With gold prices remaining elevated and the company’s operational improvements continuing to yield results, AngloGold Ashanti appears well-positioned to maintain its strong performance through the remainder of 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.