Gold prices steady with focus on Ukraine-Russia, Jackson Hole

Introduction & Market Context

Antero Midstream Corp (NYSE:AM) released its second quarter 2025 earnings presentation on July 31, showcasing record operational performance and significant financial improvements. The midstream energy company’s stock surged 6.42% following the release, closing at $18.24, reflecting strong investor confidence in the company’s results and outlook. This performance builds on momentum from Q1, when the company beat analyst expectations with an EPS of $0.25 against a forecast of $0.23.

The company continues to benefit from growing natural gas demand in the Appalachian region, particularly from increasing LNG export capacity and data center-driven power consumption. With its shares trading near the upper end of their 52-week range ($13.12-$19.09), Antero Midstream has positioned itself as a key infrastructure provider in the evolving energy landscape.

Quarterly Performance Highlights

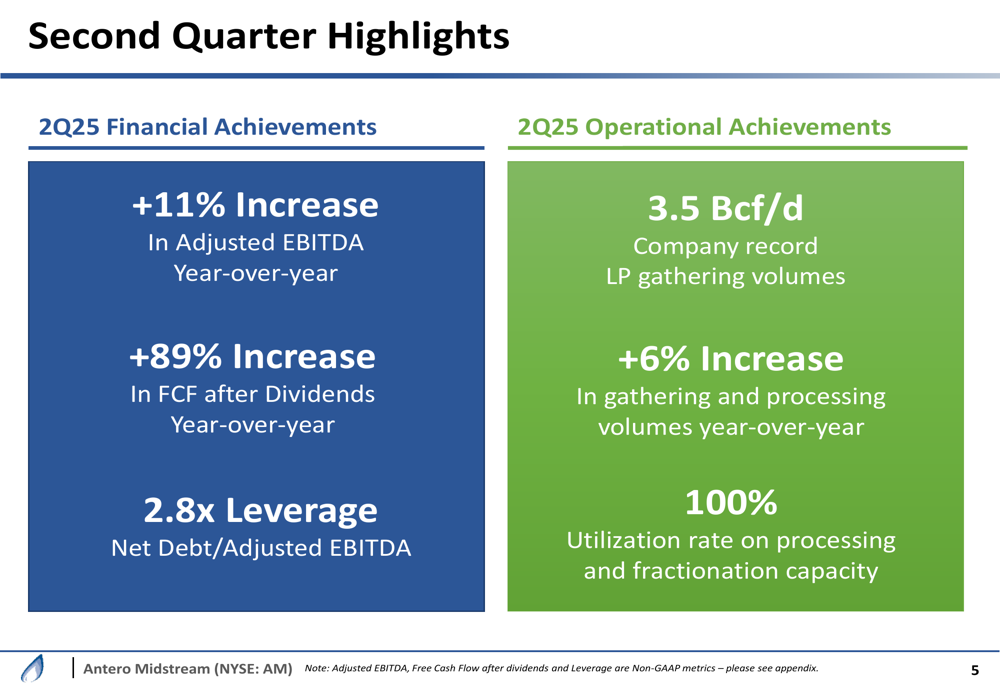

Antero Midstream reported impressive financial and operational achievements for Q2 2025, headlined by an 11% year-over-year increase in Adjusted EBITDA and an 89% jump in free cash flow after dividends compared to the same period last year.

As shown in the following quarterly highlights chart:

The company achieved record low pressure gathering volumes of 3.5 Bcf/d, marking a company record, while gathering and processing volumes increased 6% year-over-year. Perhaps most notably, Antero reported 100% utilization rate on its processing and fractionation capacity, indicating maximum operational efficiency.

Financial results were equally strong, with Q2 2025 net income reaching $124.5 million, up significantly from $86.0 million in Q2 2024. Adjusted EBITDA grew to $284.3 million from $255.0 million in the prior year period. The company’s leverage ratio improved to 2.8x (Net Debt/Adjusted EBITDA), continuing the deleveraging trend noted in Q1 when leverage stood at 2.9x.

Financial Outlook and Guidance

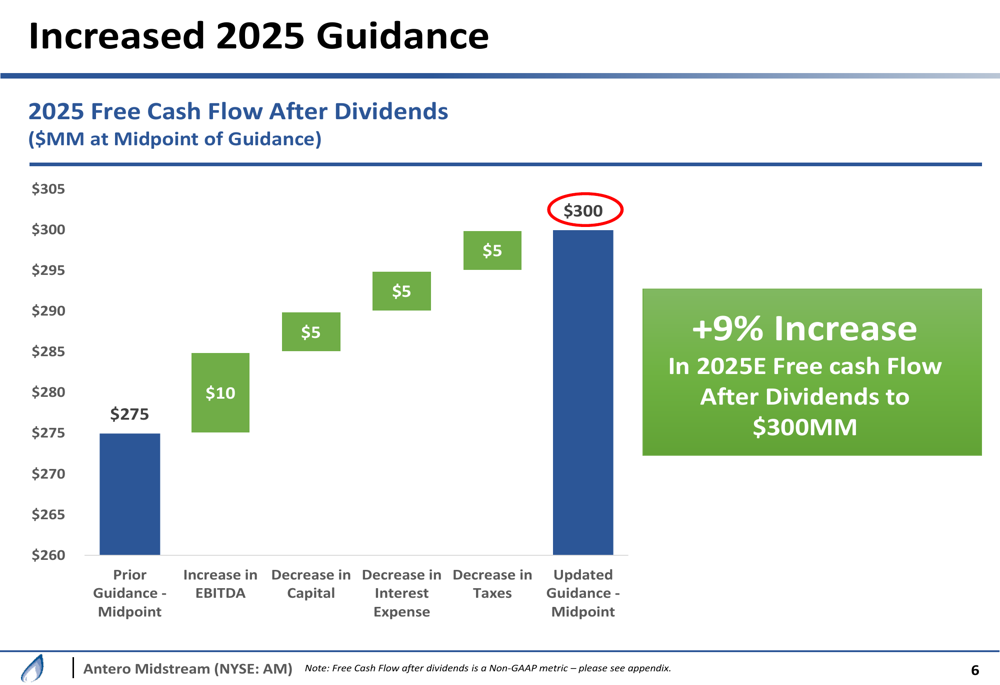

Based on strong first-half performance, Antero Midstream has increased its 2025 financial guidance while narrowing its capital expenditure range. The company now expects to generate $300 million in free cash flow after dividends for 2025, representing a 9% increase from the previous guidance of $275 million.

The following chart illustrates the key drivers behind this guidance increase:

The improved outlook stems from multiple factors: a $5 million increase in EBITDA, a $5 million decrease in capital expenditures, a $5 million reduction in interest expense, and a $5 million decrease in taxes. This balanced improvement across multiple financial metrics suggests comprehensive operational and financial efficiency.

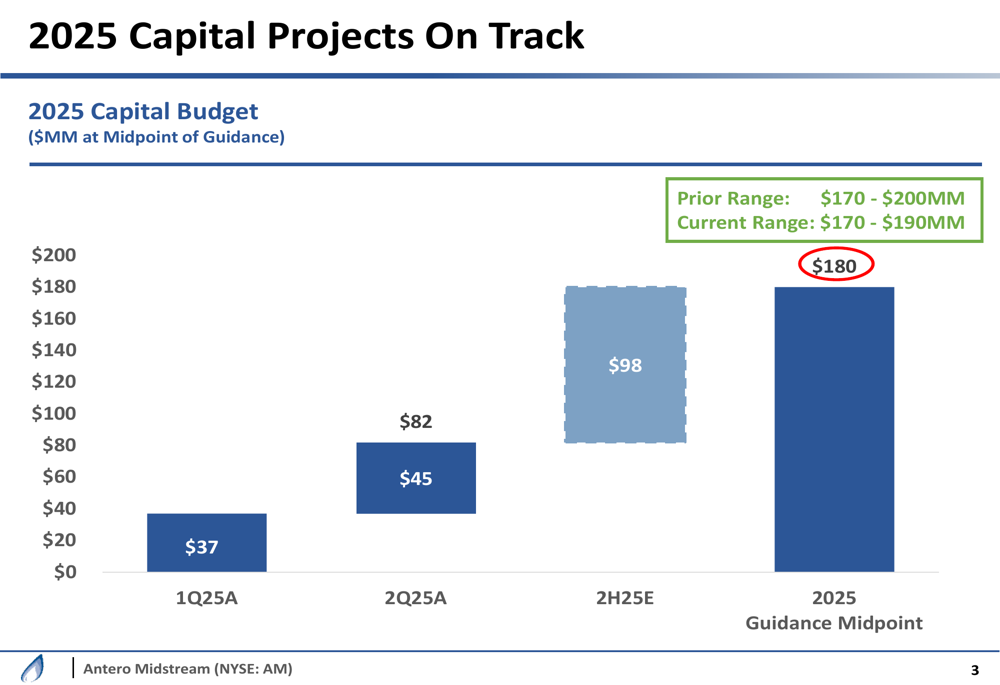

On the capital expenditure front, Antero has narrowed its 2025 guidance range to $170-190 million from the previous $170-200 million, while maintaining its strategic growth initiatives:

With $37 million spent in Q1 and $45 million in Q2, the company projects $98 million in capital expenditures for the second half of 2025. This disciplined capital approach aligns with management’s Q1 commentary about directing "capital to the highest rate of return opportunities that will accrue directly to our shareholders."

Strategic Initiatives

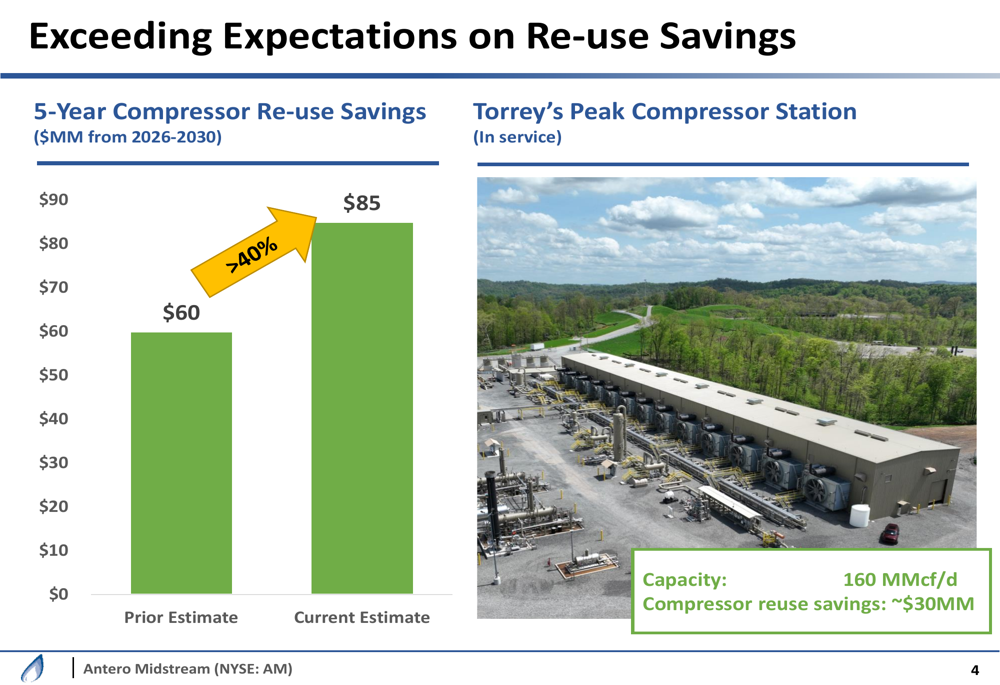

A key component of Antero’s capital efficiency strategy involves compressor re-use, which is exceeding initial expectations. The company has increased its five-year compressor re-use savings estimate by over 40%, from $60 million to $85 million for the 2026-2030 period.

The following chart illustrates this significant improvement in projected savings:

The Torrey’s Peak Compressor Station, which was mentioned in the Q1 earnings call as being commissioned early, exemplifies this approach with approximately $30 million in compressor reuse savings. With a capacity of 160 MMcf/d, this facility represents the company’s efficient capital allocation strategy.

Strategic Positioning

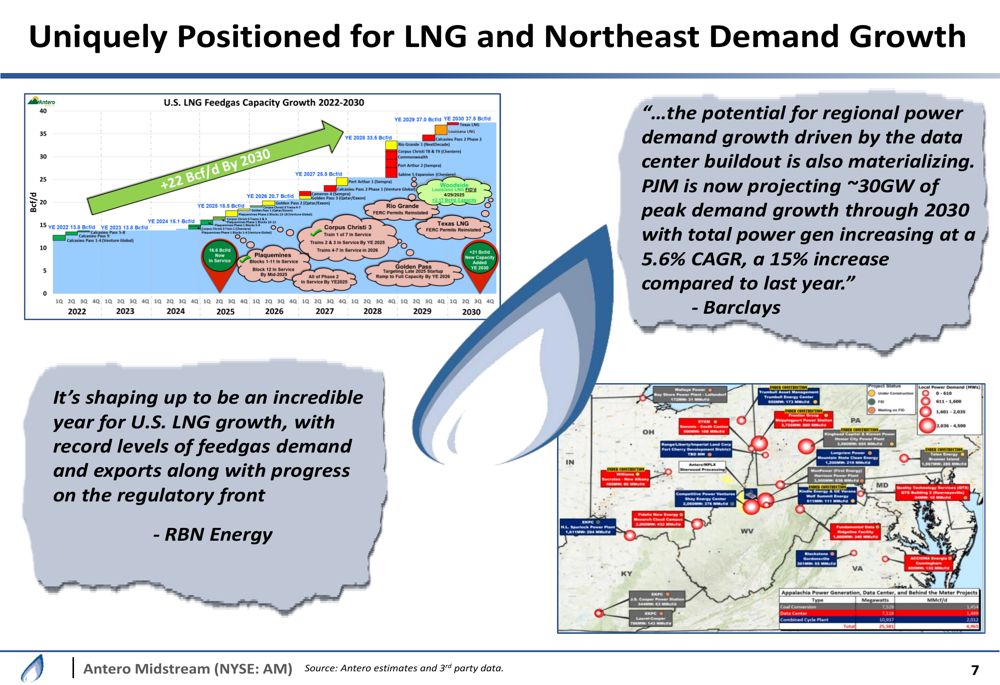

Antero Midstream highlighted its advantageous position to capitalize on both LNG export growth and increasing Northeast regional demand, particularly from data centers. The company’s infrastructure serves areas experiencing significant growth in natural gas consumption.

As illustrated in the following strategic positioning chart:

U.S. LNG Feedgas Capacity is projected to grow by 22 Bcf/d by 2030, creating substantial opportunities for midstream operators like Antero. Additionally, the company cited Barclays (LON:BARC) research projecting approximately 30GW of peak demand growth in the PJM region through 2030, with total power generation increasing at a 5.6% CAGR – a 15% increase compared to last year’s forecast.

This positioning aligns with management’s Q1 commentary about "behind-the-meter power opportunities" and the company’s proactive approach to emerging market trends in the LPG market.

Forward-Looking Statements

While maintaining an optimistic outlook, Antero Midstream faces potential challenges including supply chain disruptions, natural gas price fluctuations, regulatory changes, and regional competition. However, the company’s strong operational performance, improved financial metrics, and strategic positioning suggest it is well-equipped to navigate these challenges.

The narrowed capital expenditure guidance and increased free cash flow projections indicate management’s confidence in continued strong performance through the remainder of 2025. With leverage continuing to improve and operational metrics at record levels, Antero Midstream appears positioned to maintain its trajectory of financial and operational growth while delivering value to shareholders through its dividend program.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.