Domo signs strategic collaboration agreement with AWS for AI solutions

Introduction & Market Context

Arcus Biosciences (NYSE:RCUS) presented its corporate update on February 25, 2025, showcasing its oncology pipeline and development strategy. The presentation comes at a challenging time for the clinical-stage biopharmaceutical company, which recently reported disappointing Q1 2025 earnings with an EPS of -$1.14 (missing the -$1.02 forecast) and revenue of $28 million (below the expected $38.61 million). Despite these financial headwinds, Arcus maintains a strong cash position of over $1 billion to fund operations through multiple Phase 3 readouts.

The company’s stock, currently trading at $8.46, remains significantly below its 52-week high of $18.98, reflecting investor concerns about high R&D expenses, which reached $122 million in Q1 2025. Nevertheless, Arcus continues to advance its promising oncology pipeline, with CEO Terry Rosen emphasizing during the recent earnings call that "Our number one priority is unequivocally castadefan."

Pipeline Overview and Strategic Focus

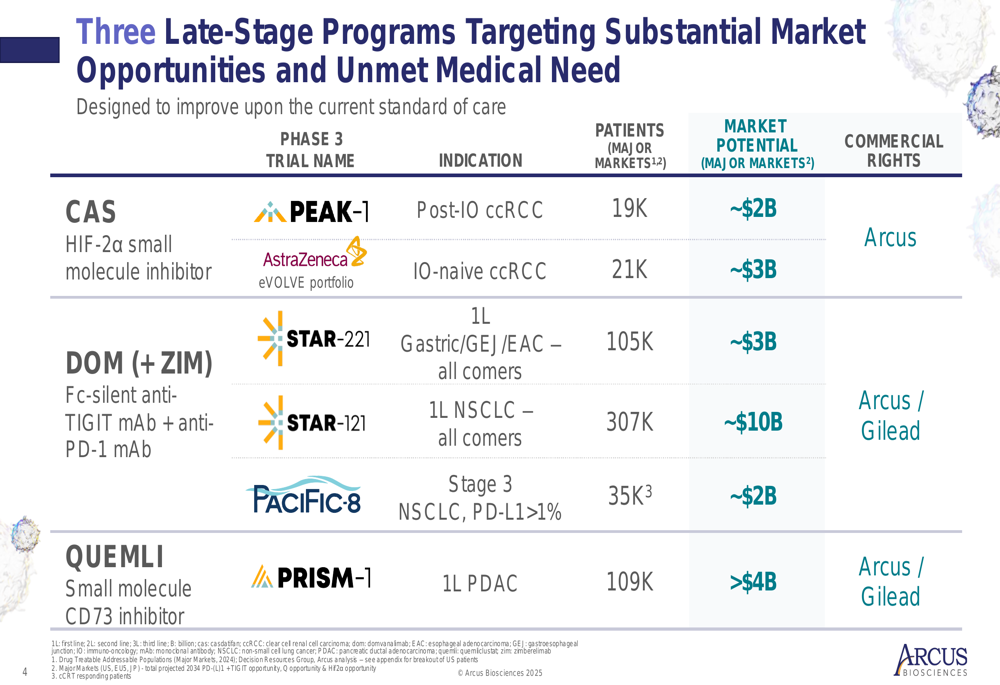

Arcus has built a diverse late-stage oncology portfolio targeting significant market opportunities across multiple cancer types. The company’s strategy centers on developing combination therapies with best-in-class potential for cancer treatment.

As shown in the following overview of Arcus’s late-stage programs and their respective market opportunities:

The company is targeting substantial markets, including clear cell renal cell carcinoma (ccRCC) with an estimated $5 billion opportunity, first-line gastric/GEJ/EAC cancer ($3 billion), first-line non-small cell lung cancer (NSCLC) ($10 billion), and first-line pancreatic cancer (PDAC) ($4 billion). These programs are supported by strategic partnerships with Gilead (NASDAQ:GILD), Taiho, and AstraZeneca (NASDAQ:AZN), which provide additional funding and global commercialization capabilities.

Casdatifan: Potential Best-in-Class HIF-2α Inhibitor

Casdatifan (CAS), Arcus’s HIF-2α inhibitor for ccRCC, has emerged as the company’s lead candidate. The ARC-20 study results presented at ASCO GU demonstrated a potentially best-in-class profile compared to competitor belzutifan ( Merck (NSE:PROR)’s LITESPARK-005).

The following data summary highlights casdatifan’s advantages across multiple efficacy measures:

Key findings include lower primary progressive disease rates (14-19% vs. 34% for belzutifan), higher objective response rates (25-33%), higher disease control rates (81-86% vs. 61%), and improved median progression-free survival (mPFS). Notably, the 50mg QD and 100mg QD cohorts had not yet reached median PFS at 12 and 5 months follow-up, respectively, while the 50mg BID cohort showed mPFS of 9.7 months compared to 5.6 months for belzutifan.

The company is advancing casdatifan into the PEAK-1 Phase 3 study, which will evaluate casdatifan plus cabozantinib versus placebo plus cabozantinib in post-IO ccRCC patients. This represents a significant market opportunity with approximately 19,000 patients.

A key advantage for casdatifan is its reduced pill burden compared to competitors, with a single 100mg QD tablet versus multiple pills for belzutifan (3 x 40mg).

Domvanalimab: First-to-Market TIGIT Inhibitor Potential

Domvanalimab (DOM), Arcus’s Fc-silent anti-TIGIT antibody, is positioned as potentially the first-to-market TIGIT inhibitor in upper GI cancers and the only Fc-silent anti-TIGIT in Phase 3 NSCLC trials.

The EDGE-Gastric study showed unprecedented median PFS in first-line gastric cancer patients:

The combination of domvanalimab, zimberelimab (anti-PD-1), and chemotherapy achieved a median PFS of 12.9 months in the intent-to-treat population and 13.8 months in PD-L1 high patients. These results significantly exceed historical benchmarks and support the ongoing STAR-221 Phase 3 study, which is fully enrolled with data expected in 2026.

In NSCLC, the ARC-7 and ARC-10 studies showed consistent improvement for domvanalimab plus zimberelimab in first-line PD-L1 high patients:

The ARC-10 study demonstrated a 36% reduction in the risk of death (HR 0.64) with the combination versus zimberelimab alone, while ARC-7 showed a 33% reduction in the risk of progression (HR 0.67). These promising results support the ongoing STAR-121 Phase 3 study in first-line NSCLC across all PD-L1 subgroups.

Adenosine Pathway Inhibitors and Early Pipeline

Arcus is also advancing programs targeting the CD73-adenosine axis, with quemliclustat (QUEMLI) showing promising results in pancreatic cancer. The company presented three datasets demonstrating the potential benefits of combining adenosine blockade with chemotherapy:

These results include a 63% reduction in the risk of death in third-line colorectal cancer and 33-37% reductions in the risk of death in first-line metastatic pancreatic cancer. Based on these findings, Arcus initiated the PRISM-1 Phase 3 study of quemliclustat plus chemotherapy in first-line metastatic pancreatic cancer in Q4 2024.

Additionally, the company is advancing AB801, potentially the most potent and selective AXL inhibitor in clinical development, with a Phase 1 study in patients with advanced solid tumors ongoing and an expansion cohort planned in second-line+ NSCLC in the second half of 2025.

Financial Position and Future Catalysts

Despite the recent Q1 2025 earnings miss, Arcus maintains its full-year 2025 revenue guidance between $75 million and $90 million. The company’s $1 billion cash position is expected to fund operations through multiple Phase 3 readouts, though high R&D expenses (projected to peak in 2025) remain a concern for investors.

Several key data readouts are expected throughout 2025:

- Early 2025: Updated data from casdatifan 50mg BID, 50mg QD, and initial data from 100mg QD tablet

- Mid-2025: Safety and initial efficacy data for casdatifan plus cabozantinib

- Fall 2025: EDGE-Gastric Phase 2 OS data for domvanalimab plus zimberelimab plus chemotherapy

- Fall 2025: More mature safety and efficacy data for all casdatifan cohorts

- 2026 (event-driven): STAR-221 Phase 3 data for domvanalimab plus zimberelimab plus chemotherapy

Outlook and Analyst Perspectives

Arcus Biosciences faces a critical period as it advances multiple Phase 3 programs while managing high R&D expenses. The company’s strategic partnerships, particularly with AstraZeneca in RCC treatments, could enhance its competitive position in this $5 billion market.

According to the recent earnings report, analysts maintain a strong buy consensus on Arcus with price targets ranging from $14 to $46, suggesting significant upside potential from current levels. However, the company must navigate the challenge of high development costs while delivering on its promising pipeline to regain investor confidence.

The company’s focus on casdatifan as its top priority aligns with the data presented in February, which positions it as a potential best-in-class therapy in RCC. If successful, this program could drive a paradigm shift in RCC treatment and serve as a foundation for Arcus’s long-term growth, despite the near-term financial challenges reflected in its Q1 2025 results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.