Robinhood shares gain on Q2 beat, as user and crypto growth accelerate

Introduction & Market Context

Arlo Technologies (NYSE:ARLO) presented its Q1 2025 investor deck on May 8, highlighting the company’s continued transformation into a subscription-based software business in the smart home security segment. The presentation emphasized Arlo’s positioning in the $25 billion U.S. home security market, which remains significantly underpenetrated with paid smart home security services at just 7% adoption.

The company’s stock closed at $10.40 on May 8, up 2.31% for the day, with after-hours trading showing a slight decline of 0.19% to $10.64, according to available market data. This follows Arlo’s Q4 2024 earnings report, which showed a slight EPS miss but continued service revenue growth.

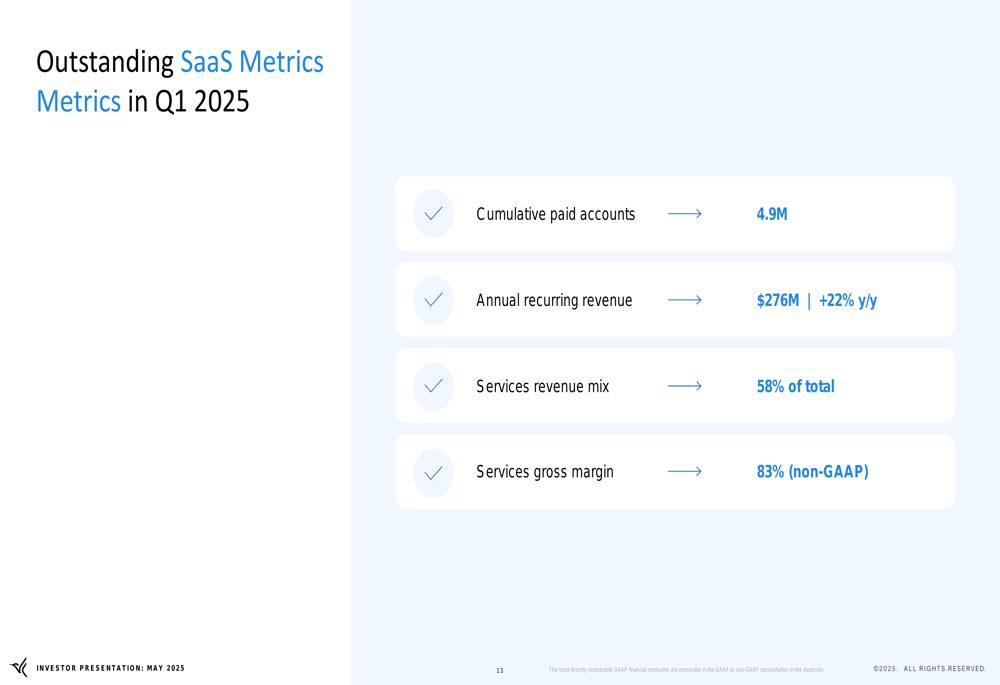

As shown in the following overview of Arlo’s key metrics:

Quarterly Performance Highlights

Arlo reported strong Q1 2025 results, with significant growth in both subscribers and recurring revenue. The company’s cumulative paid accounts reached 4.9 million, while annual recurring revenue (ARR) grew to $276 million, representing a 22% year-over-year increase. Services now account for 58% of total revenue, with an impressive non-GAAP gross margin of 83%.

The following slide highlights these key SaaS metrics from Q1 2025:

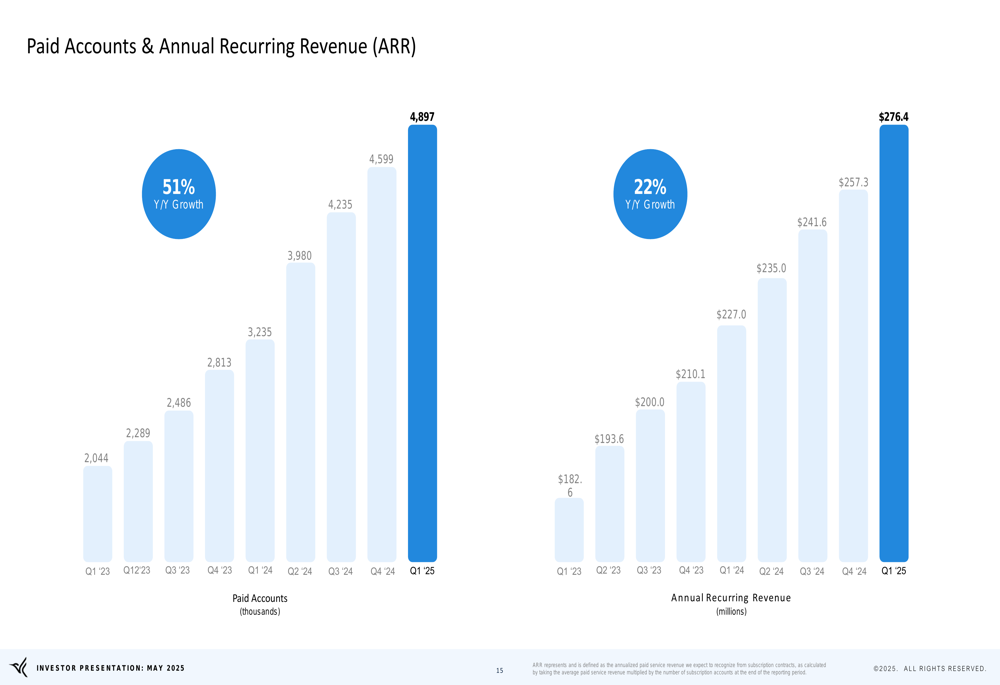

The growth trajectory becomes more apparent when examining the trend over the past two years. Paid accounts have shown remarkable growth, increasing from 2,044,000 in Q1 2023 to 4,897,000 in Q1 2025, representing a 51% year-over-year growth rate. Similarly, ARR has grown steadily from $182.6 million to $276.4 million over the same period.

This consistent growth pattern is visualized in the following chart:

Detailed Financial Analysis

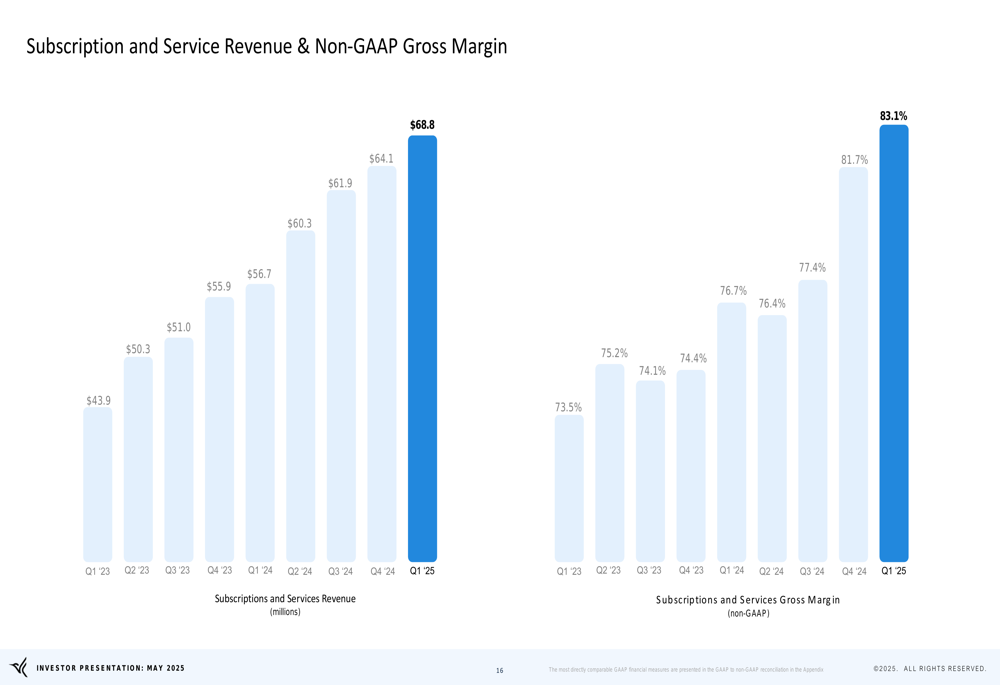

Arlo’s financial performance shows significant improvement across key metrics. Subscription and services revenue reached $68.8 million in Q1 2025, continuing its upward trend from previous quarters. More importantly, the non-GAAP gross margin for subscription and services has expanded substantially, reaching 83.1% in Q1 2025, up from 73.5% in Q1 2023.

The following chart illustrates this positive trend in both revenue growth and margin expansion:

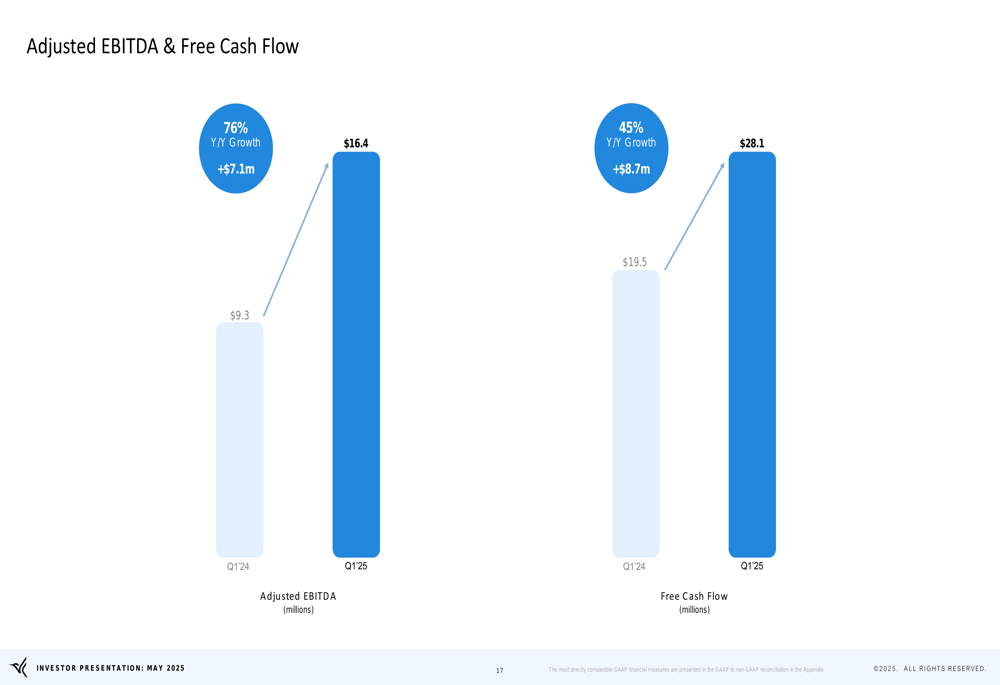

Profitability metrics also showed strong improvement. Adjusted EBITDA reached $16.4 million in Q1 2025, representing a 76% year-over-year increase from $9.3 million in Q1 2024. Free cash flow grew to $28.1 million, up 45% from $19.5 million in the same period last year.

These profitability improvements are visualized in the following chart:

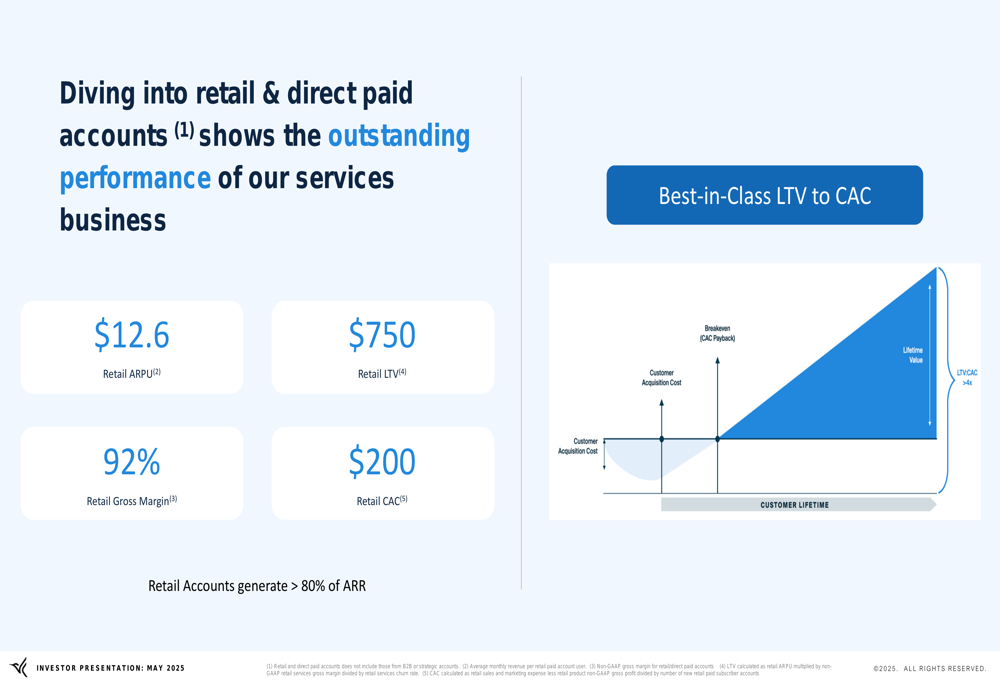

The company’s retail business continues to be a significant driver of growth, with retail accounts generating over 80% of ARR. Arlo’s retail metrics demonstrate the efficiency of its business model, with a retail ARPU of $12.6, customer lifetime value (LTV) of $750, gross margin of 92%, and customer acquisition cost (CAC) of $200. This results in an impressive LTV/CAC ratio of approximately 4x, indicating highly efficient customer acquisition.

The following slide illustrates these retail performance metrics:

Strategic Initiatives

Arlo’s strategic positioning centers around its AI-powered SaaS platform, which has been built over the last decade. The platform processes over 170 billion AI alerts annually, handles 1,700+ hours of video per minute, and manages 26+ billion API calls daily. This sophisticated infrastructure supports the 34+ million devices shipped to date.

The comprehensive ecosystem is illustrated in the following diagram:

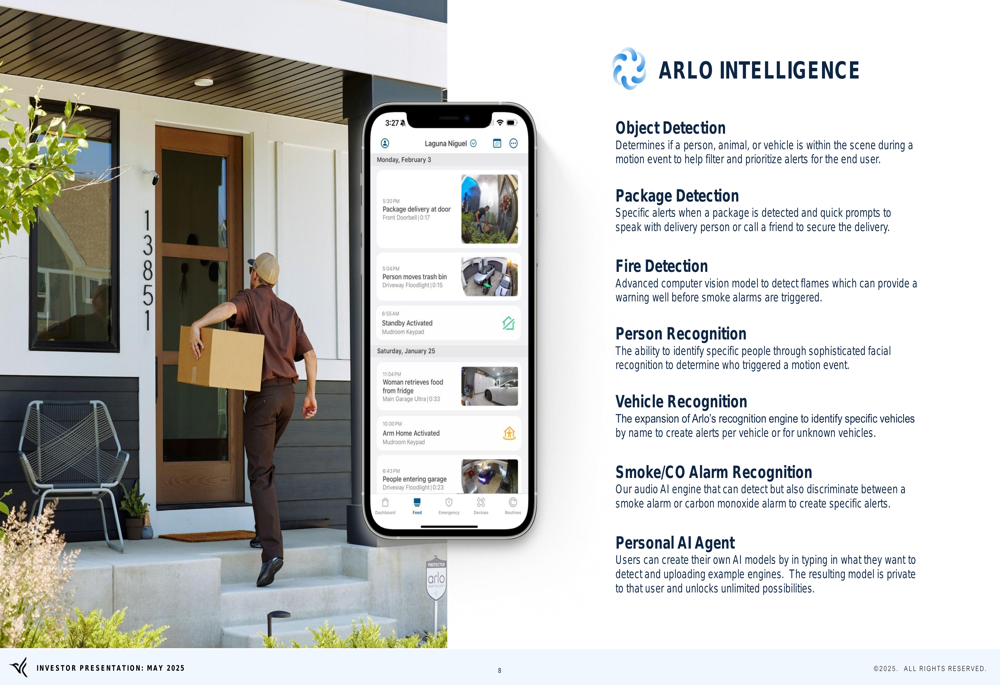

A key differentiator for Arlo is its AI capabilities, branded as "Arlo Intelligence." These features include object detection, package detection, fire detection, person recognition, vehicle recognition, smoke/CO alarm recognition, and a personal AI agent. These capabilities drive subscription value and help maintain Arlo’s competitive edge.

The AI features are showcased in this slide:

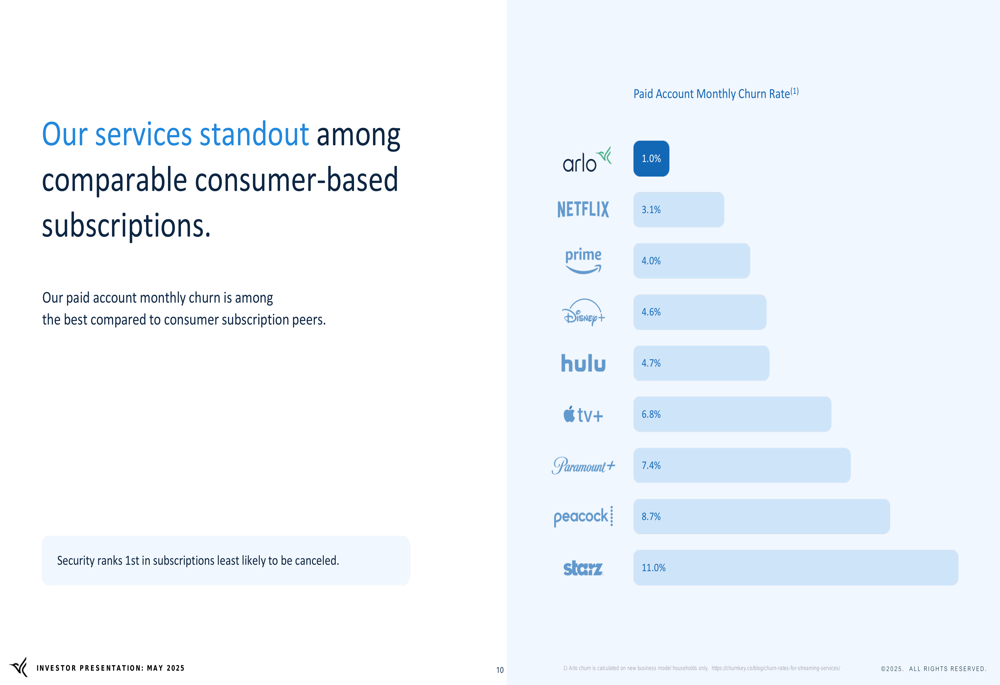

Arlo’s subscription retention metrics are particularly impressive when compared to other consumer subscription services. With a monthly churn rate of just 1.0%, Arlo significantly outperforms major streaming services like Netflix (NASDAQ:NFLX) (3.1%), Amazon (NASDAQ:AMZN) Prime (4.0%), and Disney+ (4.6%). This low churn rate underscores the essential nature of security services compared to entertainment subscriptions.

The comparative churn rates are displayed in the following chart:

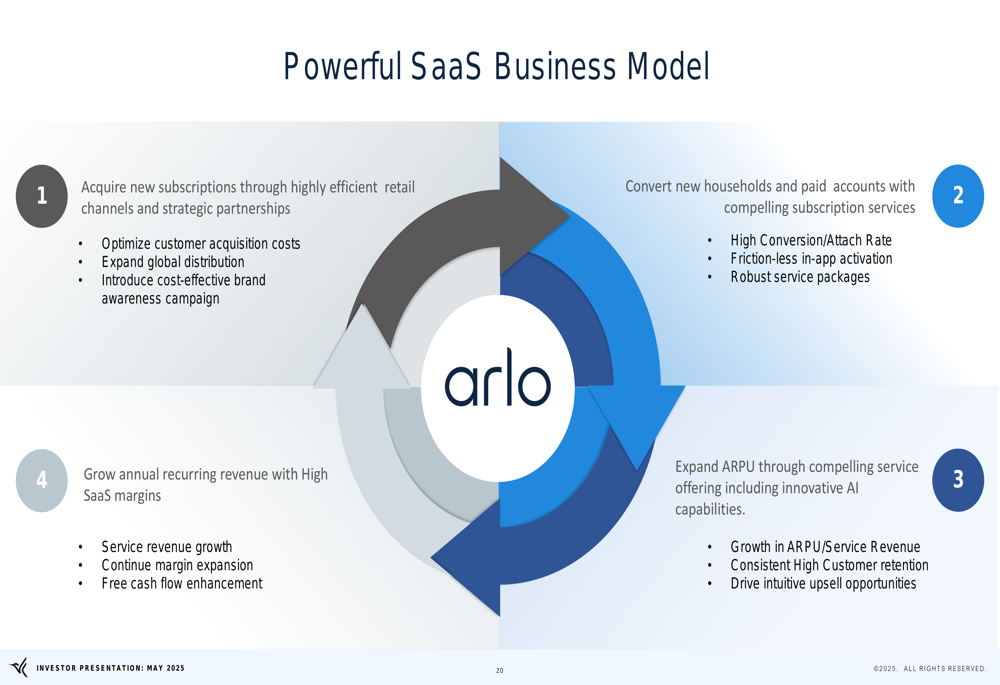

The company’s business model follows a clear SaaS approach: acquiring new subscriptions through retail channels and partnerships, converting new households to paid accounts, expanding ARPU through AI capabilities, and growing ARR with high SaaS margins.

This model is visualized in the following diagram:

Forward-Looking Statements

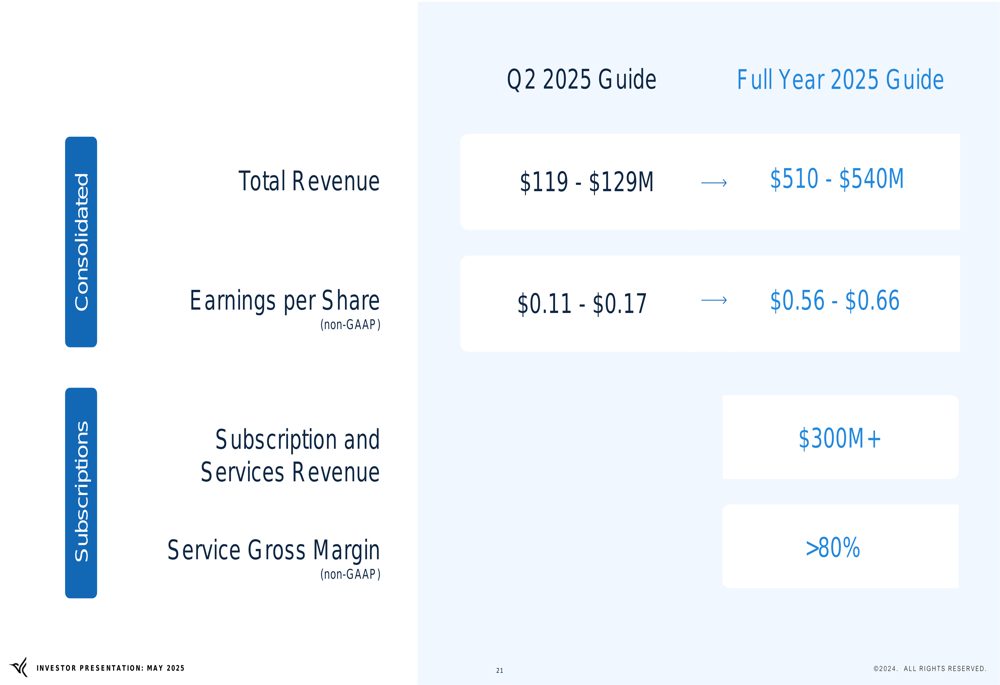

For Q2 2025, Arlo projects total revenue between $119-$129 million and non-GAAP earnings per share of $0.11-$0.17. For the full year 2025, the company expects total revenue of $510-$540 million, non-GAAP EPS of $0.56-$0.66, subscription and services revenue exceeding $300 million, and service gross margin remaining above 80%.

The detailed financial guidance is presented in this slide:

Perhaps most notably, Arlo has significantly updated its long-range plan. The original plan (from March 2022) targeted 5 million paid accounts, $300 million in ARR, and at least 10% non-GAAP operating margin by 2027. The current plan is substantially more ambitious, targeting 10 million paid accounts, $700 million in ARR, and over 25% non-GAAP operating margin by 2030.

This outlook represents a significant improvement from the Q4 2024 results reported earlier, where the company posted an EPS of $0.10 (missing the $0.11 forecast) on revenue of $122 million. The presentation suggests Arlo has gained momentum in Q1 2025, with improved metrics across the board.

The company also outlined its product roadmap, which includes a complete refresh of all camera lines in 2025-2026, followed by the introduction of a next-generation ecosystem in 2026-2027. These product innovations, combined with the company’s AI capabilities and subscription model, form the foundation for Arlo’s ambitious growth targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.