Tesla could be a $10,000 stock in a decade, says longtime bull Ron Baron

Introduction & Market Context

Arrow Electronics (NYSE:ARW) reported its third quarter 2025 results on October 30, showing solid revenue growth despite ongoing margin challenges. The global electronic components and enterprise computing solutions distributor posted double-digit sales growth year-over-year, though investors responded cautiously to the mixed results.

The company’s stock fell 2.47% to $116.10 in after-hours trading following the announcement, despite beating both revenue and earnings estimates. This suggests investors may be concerned about declining margins and the sustainability of growth in certain segments.

Quarterly Performance Highlights

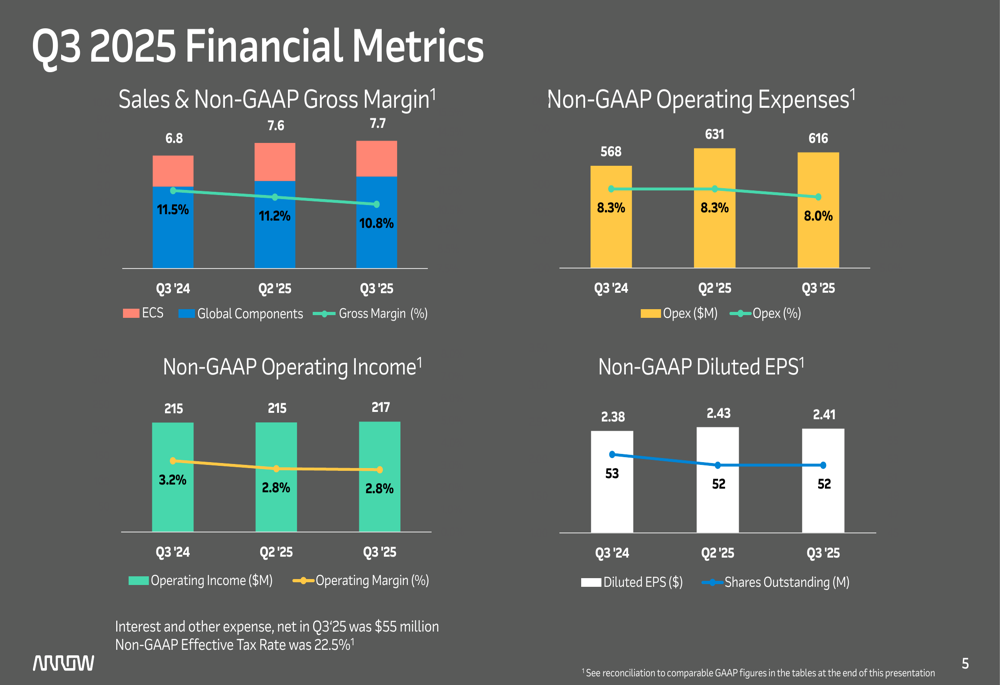

Arrow’s Q3 2025 consolidated sales reached $7.7 billion, representing a 13% year-over-year increase and exceeding the midpoint of the company’s guidance range. Non-GAAP earnings per share came in at $2.41, surpassing both the high end of guidance and analyst expectations of $2.29.

As shown in the following key financial metrics slide:

However, the company’s operating margin declined to 2.8% from 3.2% in the same quarter last year, reflecting ongoing pressure on profitability. Gross margin also contracted to 10.8% from 11.5% year-over-year, though operating expenses as a percentage of sales improved to 8.0% from 8.3%.

The detailed financial metrics reveal this margin compression alongside the revenue growth:

Segment Analysis

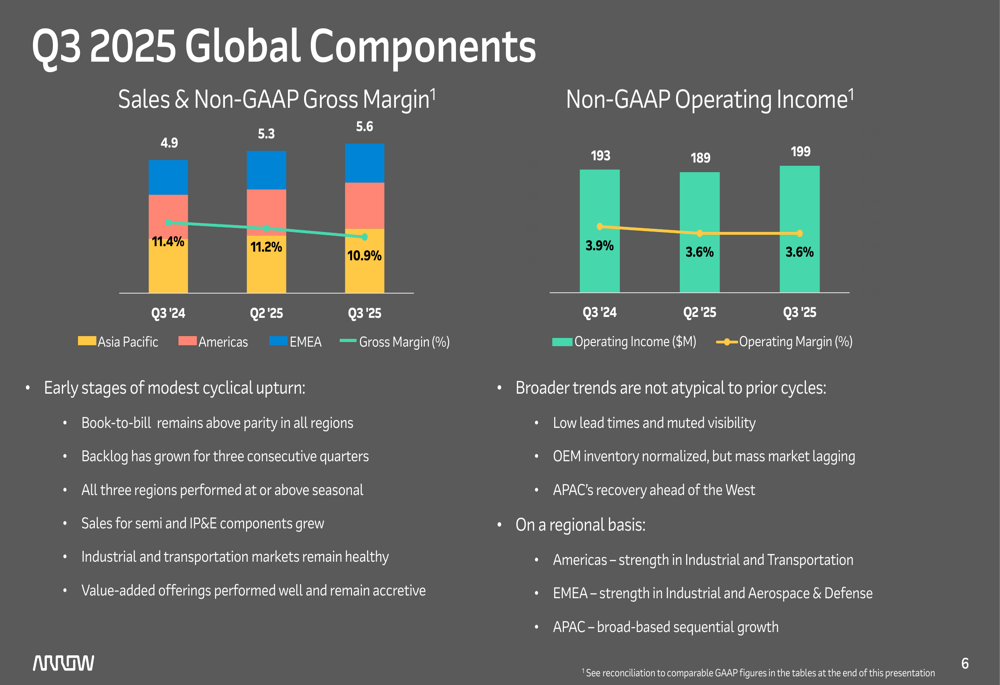

Arrow’s Global Components segment, which accounts for approximately 72% of total revenue, showed signs of recovery with sales of $5.56 billion, up 12.3% year-over-year. The segment maintained a 3.6% operating margin, though this was down from 3.9% in Q3 2024.

The presentation highlighted several positive indicators for the components business:

The Asia Pacific region led growth with a 19.1% year-over-year increase, followed by EMEA at 11.9% and Americas at 4.3%. Management noted that book-to-bill ratios remain above parity in all regions, and backlog has grown for three consecutive quarters, suggesting continued momentum into 2026.

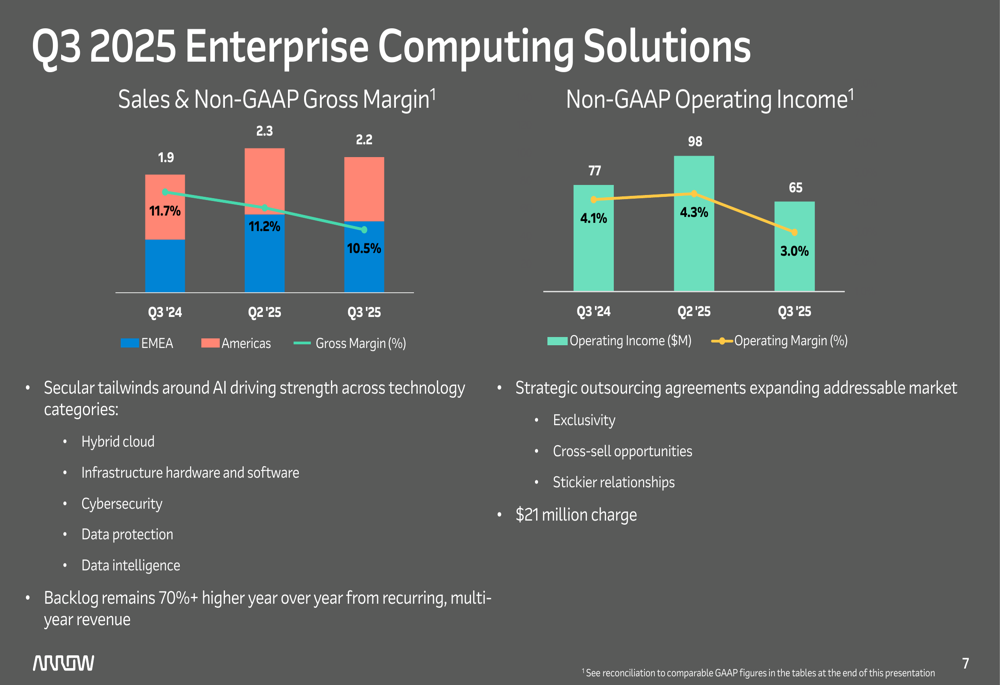

Meanwhile, the Enterprise Computing Solutions (ECS) segment posted sales of $2.16 billion, up 14.9% year-over-year, but faced significant margin challenges:

The ECS segment took a $21 million charge due to underperforming multi-year contracts, which reduced EPS by approximately $0.31. This contributed to the decline in operating margin from 4.1% in Q3 2024 to 3.0% in Q3 2025. While EMEA ECS sales grew impressively by 34.4%, Americas ECS sales declined by 1.1%.

Strategic Initiatives & Market Positioning

Arrow emphasized its strategic positioning in large and growing markets, with a focus on expanding its mix of higher-margin value-added services. The company highlighted its differentiated capabilities and diversified business model as key competitive advantages:

Management pointed to secular tailwinds around artificial intelligence driving strength across technology categories, including hybrid cloud, infrastructure hardware and software, cybersecurity, and data protection. Strategic outsourcing agreements are expanding Arrow’s addressable market, with backlog remaining more than 70% higher year-over-year from recurring, multi-year revenue.

Interim CEO William Austen remarked during the earnings call, "We are seeing trends in our Global Components business that suggest we are in the early stages of a gradual recovery," while CFO Raj Agrawal emphasized that "strategic outsourcing agreements will be margin-accretive and a key part of our long-term business."

Forward-Looking Statements & Guidance

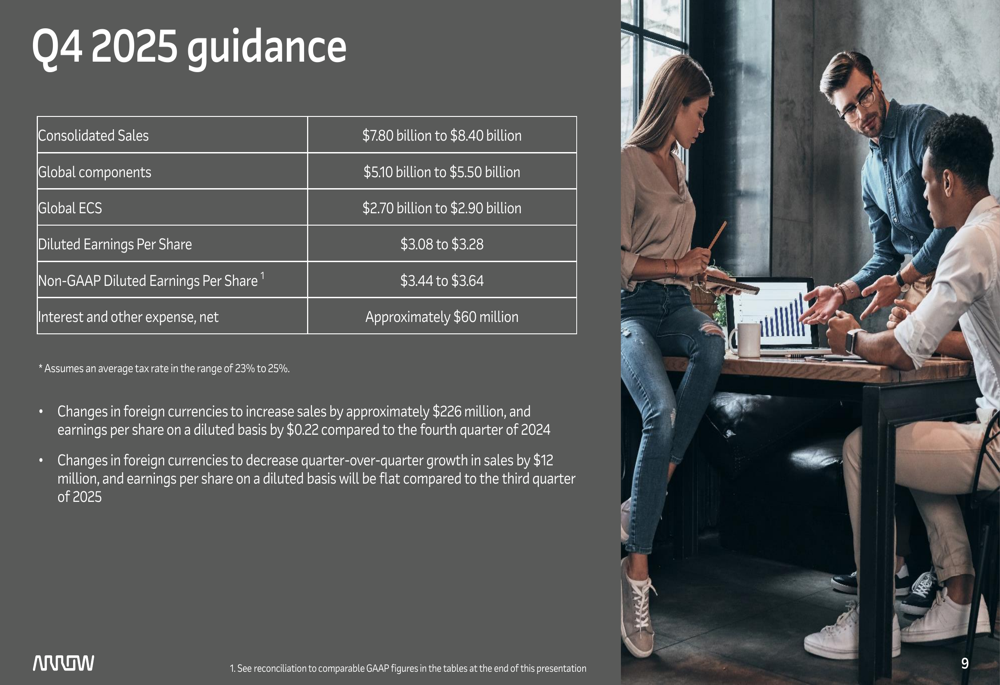

Looking ahead to Q4 2025, Arrow provided the following guidance:

The company expects consolidated sales between $7.80 billion and $8.40 billion for Q4 2025, with non-GAAP diluted earnings per share ranging from $3.44 to $3.64. This guidance incorporates a positive impact from foreign currency changes, which are expected to increase sales by approximately $226 million and earnings per share by $0.22 compared to Q4 2024.

Arrow’s management expressed confidence in the company’s long-term outlook, emphasizing that the Global Components cyclical recovery is underway and that secular trends in cloud computing and AI are driving growth across both operating segments:

Despite the positive outlook, investors should note the ongoing margin challenges and the competitive pressures in the technology distribution sector. Arrow’s ability to successfully execute its strategy of shifting toward higher-margin value-added services while navigating the cyclical recovery in components will be crucial for its performance in 2026 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.