Two National Guard members shot near White House

Introduction & Market Context

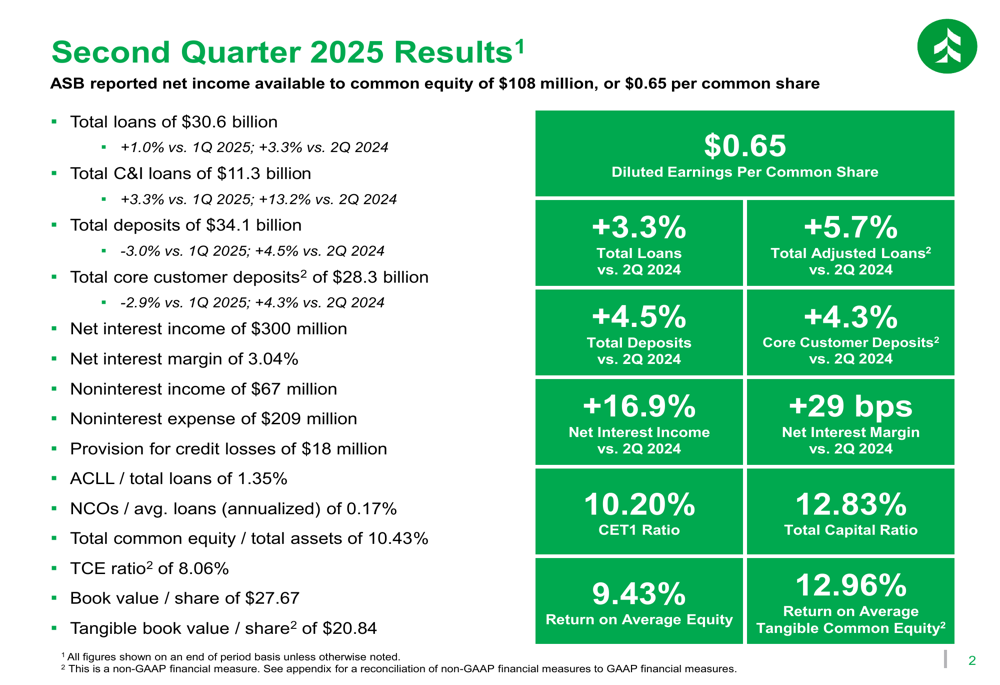

Associated Banc-Corp (NYSE:ASB) released its second quarter 2025 earnings presentation on July 24, 2025, revealing solid financial performance highlighted by record net interest income and continued commercial loan growth. The bank reported net income of $108 million, or $0.65 per common share, in line with market expectations.

The stock responded positively to the results, rising 3.53% to close at $25.37 on the day of the announcement, reflecting investor confidence in the company's strategic direction and financial performance. According to available market data, ASB has delivered a strong price return over the past six months, significantly outperforming broader market indices.

Quarterly Performance Highlights

Associated Banc-Corp's second quarter results demonstrated continued momentum in its core business lines. The bank reported net income of $108 million ($0.65 per share), supported by record net interest income of $300 million, which increased 16.9% year-over-year.

As shown in the following summary of quarterly results, the bank saw improvement across several key metrics:

Total loans grew to $30.6 billion, up 3.3% year-over-year, while deposits increased to $34.1 billion, representing 4.5% growth compared to the same period last year. The efficiency ratio improved to 55.8%, down from 59.5% in Q2 2024, reflecting the company's focus on operational efficiency.

Loan and Deposit Trends

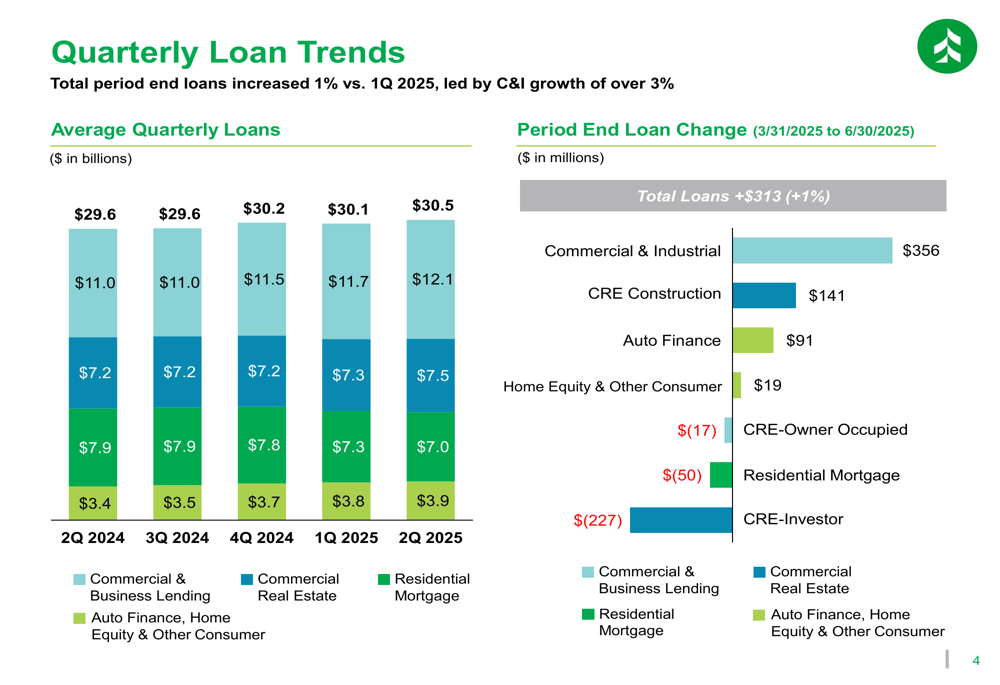

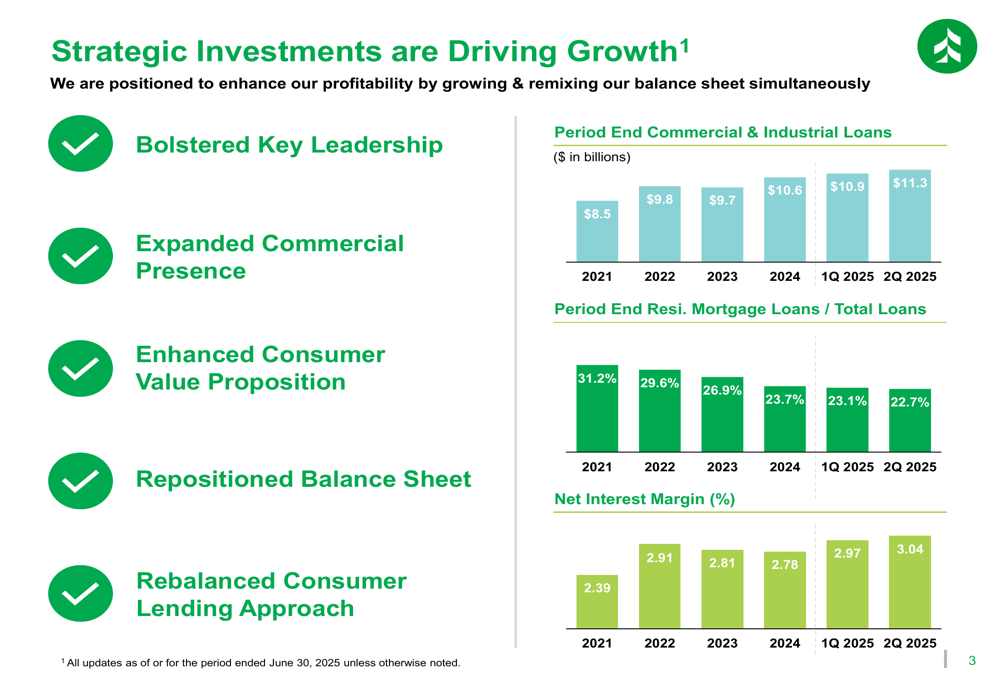

Commercial and industrial (C&I) lending remained a key growth driver for Associated Banc-Corp, with C&I loans increasing 13.2% year-over-year to $11.3 billion. This growth aligns with the bank's strategic focus on expanding its commercial banking presence.

The quarterly loan trends illustrate this strategic shift, with C&I loans showing the strongest growth among all loan categories:

Period-end loan changes from Q1 to Q2 2025 show C&I loans increased by $356 million, while CRE-investor loans decreased by $227 million, reflecting the bank's deliberate portfolio rebalancing. The bank has been strategically reducing its residential mortgage concentration, which now represents 22.7% of total loans, down from 23.1% in Q1 2025 and 31.2% in 2021.

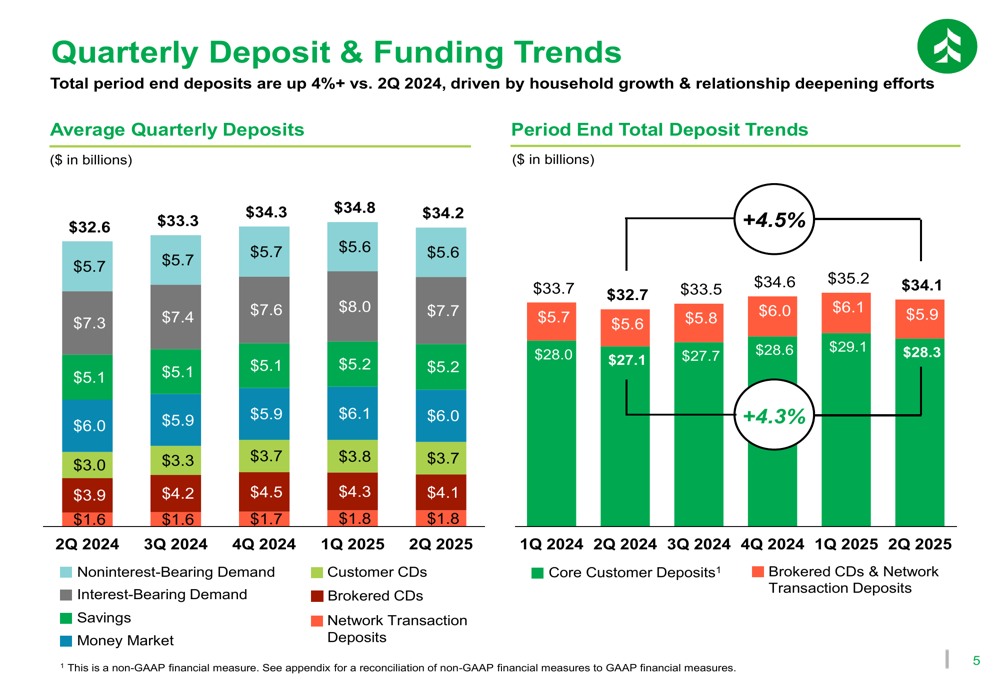

On the funding side, total deposits decreased 3.0% quarter-over-quarter but increased 4.5% year-over-year to $34.1 billion:

Core customer deposits, which represent 83% of total deposits, followed a similar pattern, decreasing 2.9% from the previous quarter but growing 4.3% year-over-year. The bank maintains a stable and granular deposit base, with liquidity sources covering 173% of uninsured, uncollateralized deposits as of June 30, 2025.

Net Interest Income and Margin Expansion

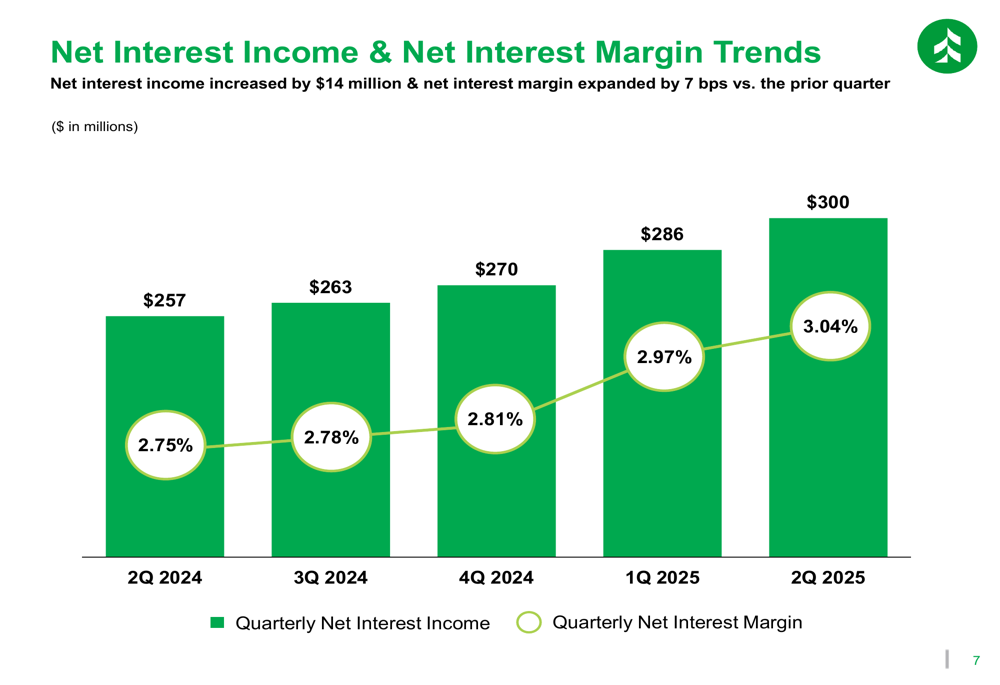

One of the most significant highlights of Associated's Q2 results was the continued expansion of net interest income and margin. Net interest income reached a record $300 million, up $14 million from the previous quarter and $43 million (16.9%) from the same period last year.

The net interest margin expanded to 3.04%, representing a 7 basis point increase from the previous quarter and a 29 basis point improvement year-over-year:

This margin expansion was driven by a 5 basis point increase in earning asset yields and a 4 basis point decrease in interest-bearing liability costs. The bank's strategic investments and balance sheet repositioning have contributed significantly to this improvement, as illustrated in the following chart:

The bank has been proactively managing its interest rate risk to protect net interest income in a potential falling rate environment. This includes extending funding duration and implementing hedging strategies through swaps.

Credit Quality and Capital Position

Credit quality remained generally stable in the second quarter. The allowance for credit losses on loans (ACLL) increased slightly to 1.35% of total loans, up 1 basis point from the previous quarter. Nonaccrual loans decreased by $22 million from Q1 2025 to $113 million, while net charge-offs were $13 million for the quarter.

However, total criticized loans increased to $1.47 billion, up from $1.33 billion in the previous quarter, suggesting some potential pressure in certain segments of the loan portfolio.

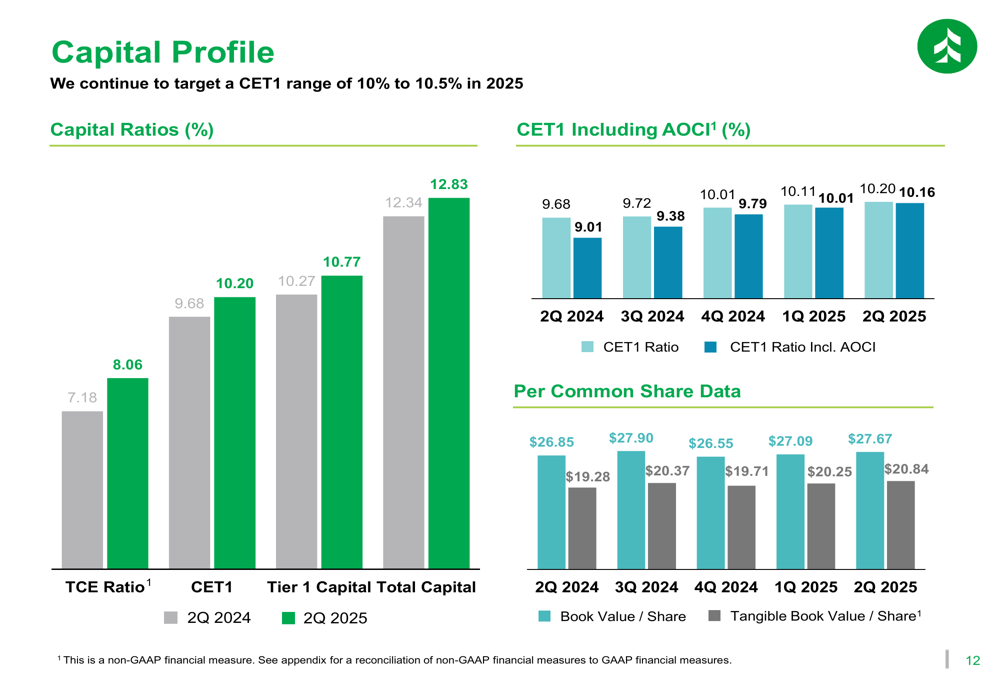

Capital levels remained strong, with the CET1 ratio improving to 10.20%, up from 9.68% in Q2 2024:

The tangible common equity (TCE) ratio also improved to 8.06%, compared to 7.18% a year earlier. Book value per share increased to $27.67, while tangible book value per share rose to $20.84.

Forward-Looking Statements

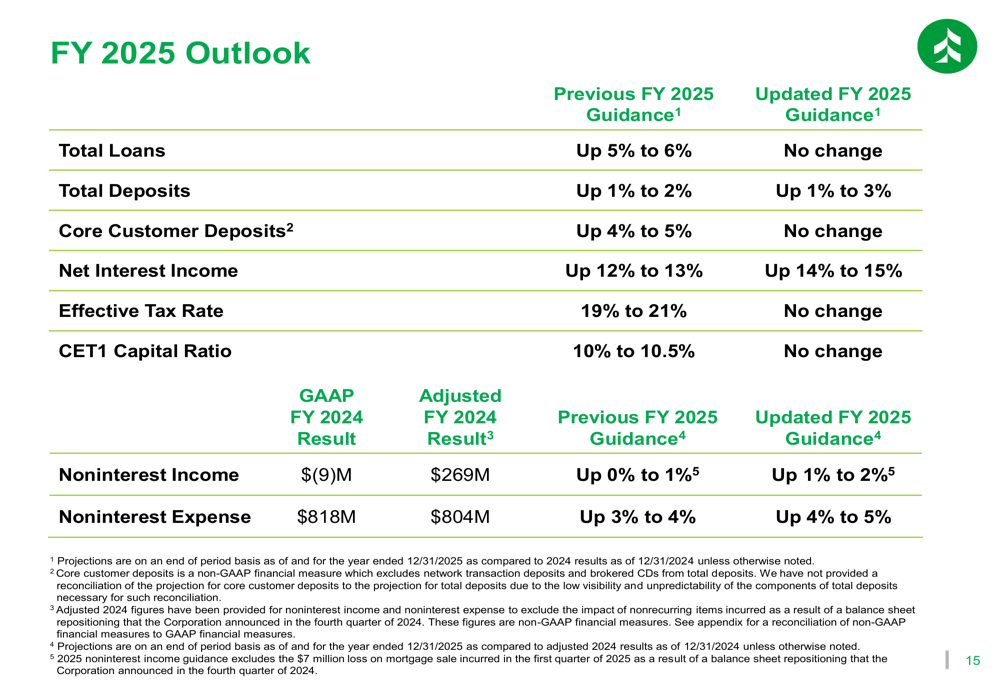

Associated Banc-Corp provided updated guidance for fiscal year 2025, maintaining or slightly adjusting several key targets:

The bank slightly reduced its net interest income growth forecast to 12-13% (from 14-15%) and noninterest income growth to 0-1% (from 1-2%). Noninterest expense growth is now expected to be 3-4%, down from the previous guidance of 4-5%.

Loan growth targets remain unchanged at 5-6% for total loans, while the deposit growth forecast was adjusted to 1-2% (from 1-3%). Core customer deposit growth is still expected to be 4-5%.

CEO Andy Harmening expressed confidence in the company's momentum, stating, "We continue to feel well positioned to build on our momentum in the back half of the year." CFO Derek Meyer highlighted the strength of the company's asset side as a key driver of margin strength.

The bank continues to target a CET1 ratio range of 10-10.5% for 2025, indicating a commitment to maintaining strong capital levels while supporting growth initiatives. Associated Banc-Corp's strategic focus on commercial banking expansion, particularly in C&I lending, appears to be yielding positive results as reflected in the Q2 2025 performance metrics.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.