Two National Guard members shot near White House

Introduction & Market Context

AstroNova Inc (NASDAQ:ALOT) presented its second quarter fiscal 2026 financial results on September 9, 2025, revealing a challenging quarter marked by revenue declines and margin compression. The specialized printing technology company, currently trading at $11.50, has been implementing strategic changes under new leadership to address operational challenges and position itself for future growth.

The presentation, delivered by President and CEO Jorik Ittmann and CFO Tom DeByle, outlined both current financial headwinds and the company's strategic roadmap for recovery. This marks a significant shift from the previous quarter's performance, which had shown 14.4% year-over-year revenue growth.

Quarterly Performance Highlights

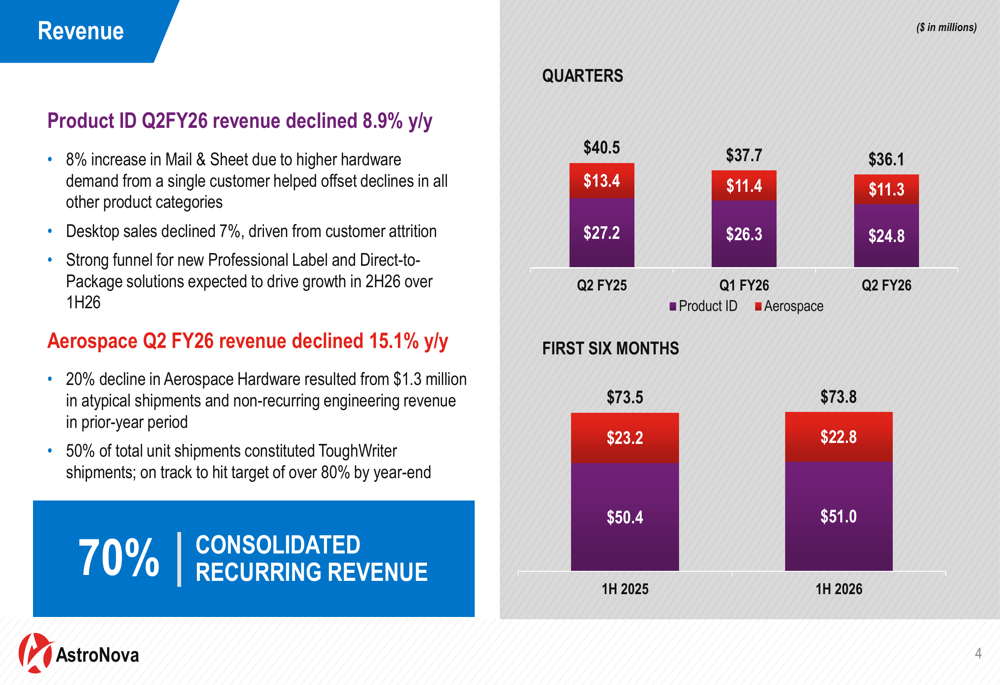

AstroNova reported Q2 FY26 revenue of $36.1 million, representing a 10.9% decrease from $40.5 million in the same period last year. Both of the company's business segments experienced declines, with Product ID down 8.9% and Aerospace falling 15.1% year-over-year.

As shown in the following revenue performance chart:

Gross profit declined to $11.6 million (32.2% margin) from $14.3 million (35.3% margin) in Q2 FY25, primarily due to lower sales volume. The company expects gross margin to improve in the second half of fiscal 2026 as volume increases.

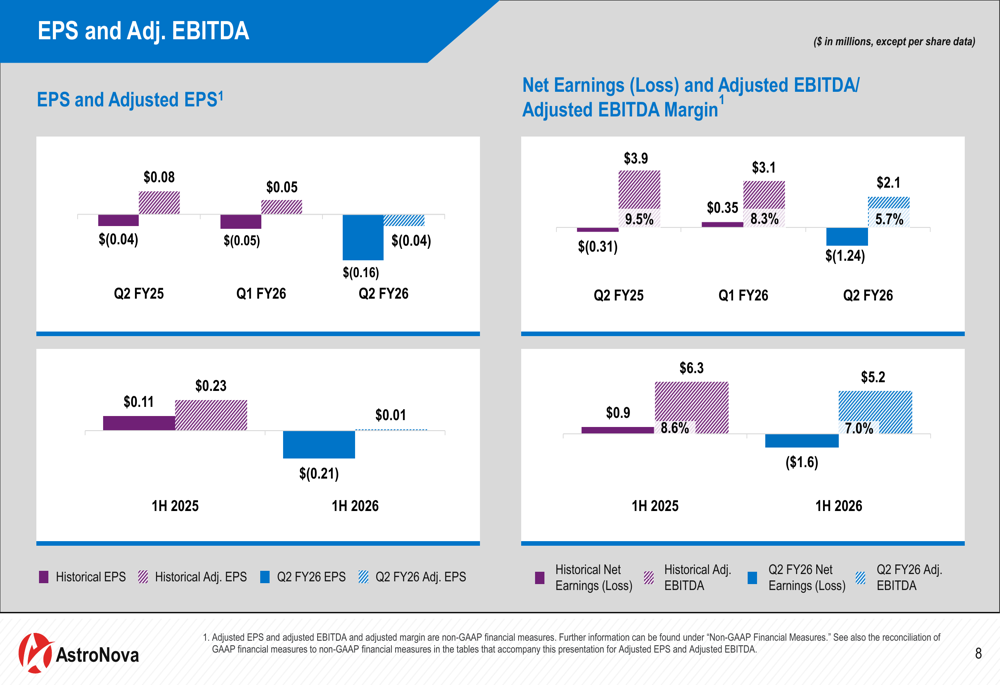

The earnings picture showed further deterioration, with Q2 FY26 reporting a loss per share of $(0.16), compared to $(0.04) in the prior year period. On an adjusted basis, EPS was $(0.04), down from $0.08 in Q2 FY25.

The following chart illustrates the EPS and Adjusted EBITDA trends:

Adjusted EBITDA for Q2 FY26 was $2.1 million with a 5.7% margin, a significant decline from $3.9 million and 9.5% margin in the prior year period. This represents a continued challenge for the company's profitability metrics.

Segment Analysis

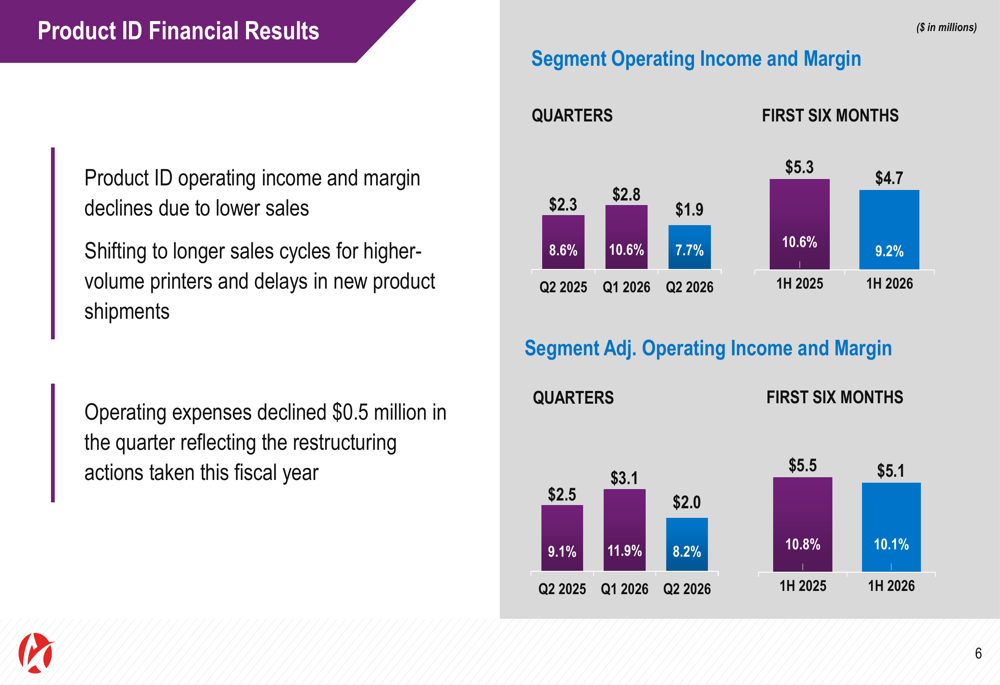

The Product ID segment, which accounts for approximately 69% of total revenue, generated $24.8 million in Q2 FY26, down from $27.2 million in Q2 FY25. The decline was primarily attributed to a 7% decrease in Desktop sales, with some offset from Mail & Sheet products, which grew by 8%.

The segment's operating income and margin also declined, as illustrated in the following chart:

The company noted a shift to longer sales cycles for higher-volume printers and delays in new product shipments as contributing factors to the segment's performance challenges.

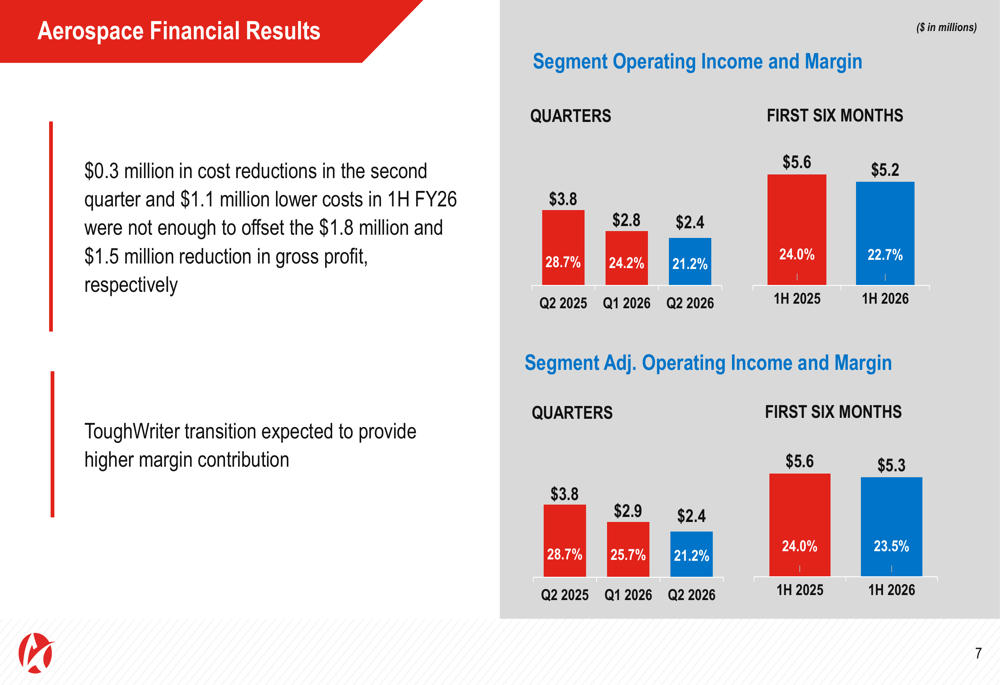

The Aerospace segment, representing about 31% of total revenue, reported $11.3 million in Q2 FY26, down 15.1% from $13.4 million in Q2 FY25. The decline was primarily driven by a 20% reduction in Aerospace Hardware sales. Despite cost reductions of $0.3 million in the quarter, these were insufficient to offset the $1.8 million reduction in gross profit.

The segment's operating performance is illustrated below:

On a positive note, the company highlighted that 70% of its revenue is recurring, providing some stability amid the challenging environment. Additionally, orders remained relatively stable year-over-year at $35.9 million in Q2 FY26 compared to $35.8 million in Q2 FY25, though backlog decreased to $25.3 million from $29.9 million in the prior year period.

Strategic Initiatives

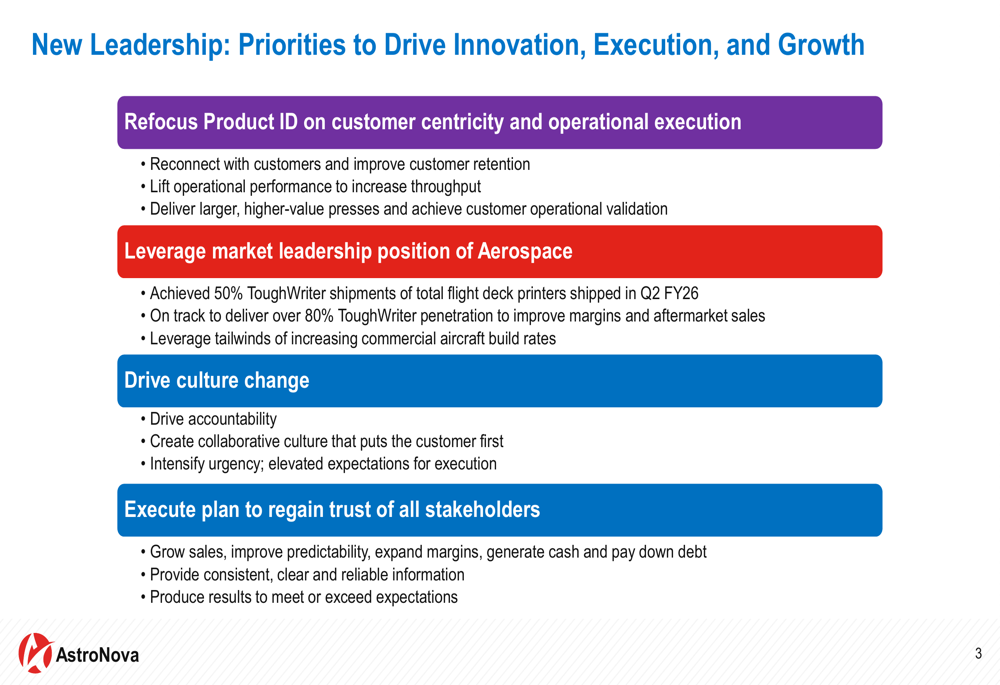

Under new leadership, AstroNova has outlined a comprehensive plan to address current challenges and drive future growth. The company's strategic priorities focus on four key areas, as shown in the following chart:

The company is emphasizing customer centricity and operational execution in its Product ID segment, while leveraging its market leadership position in Aerospace, where it achieved 50% ToughWriter shipments in Q2 FY26 and is on track to deliver over 80% ToughWriter penetration.

AstroNova is also implementing significant cultural changes, driving accountability and creating a collaborative environment focused on customer needs. Management is executing a plan to regain stakeholder trust through sales growth, margin expansion, cash generation, and consistent information sharing.

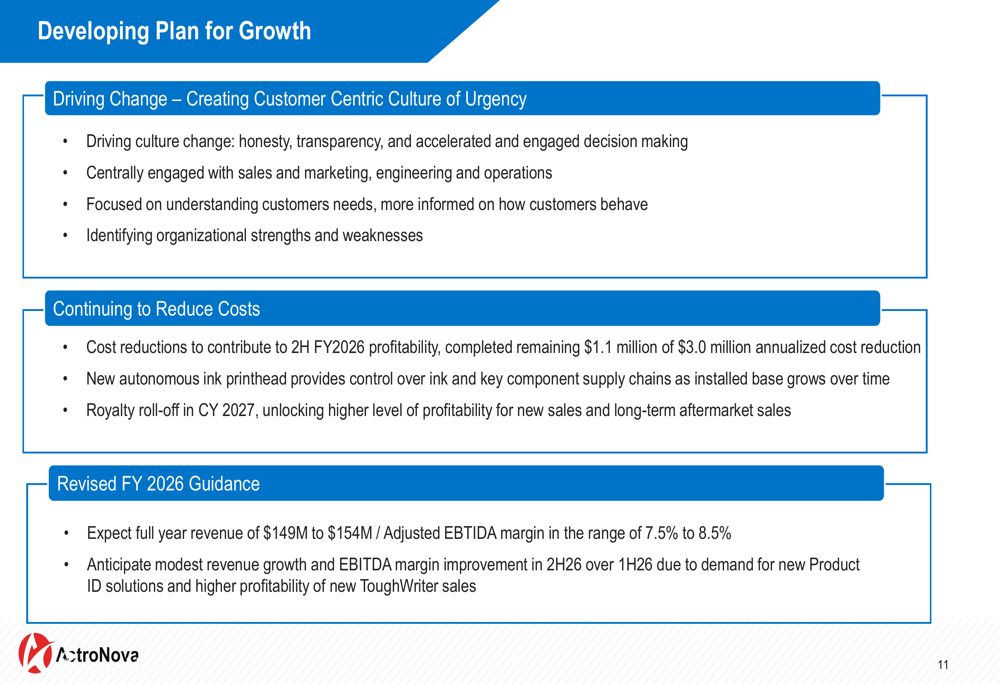

Cost reduction initiatives are a critical component of the company's strategy, as outlined in its plan for growth:

Notable developments include a new autonomous ink printhead that will provide greater control over ink supply chains, and an expected royalty roll-off in calendar year 2027, both of which should contribute to margin improvement.

Revised Guidance & Outlook

In light of current performance challenges, AstroNova has revised its fiscal 2026 guidance downward. The company now expects full-year revenue of $149 million to $154 million, compared to the previous guidance of $160 million to $165 million provided in the first quarter.

Similarly, the Adjusted EBITDA margin guidance has been lowered to a range of 7.5% to 8.5%, down from the previous 8.5% to 9.5%. Despite these revisions, management anticipates modest revenue growth and EBITDA margin improvement in the second half of fiscal 2026.

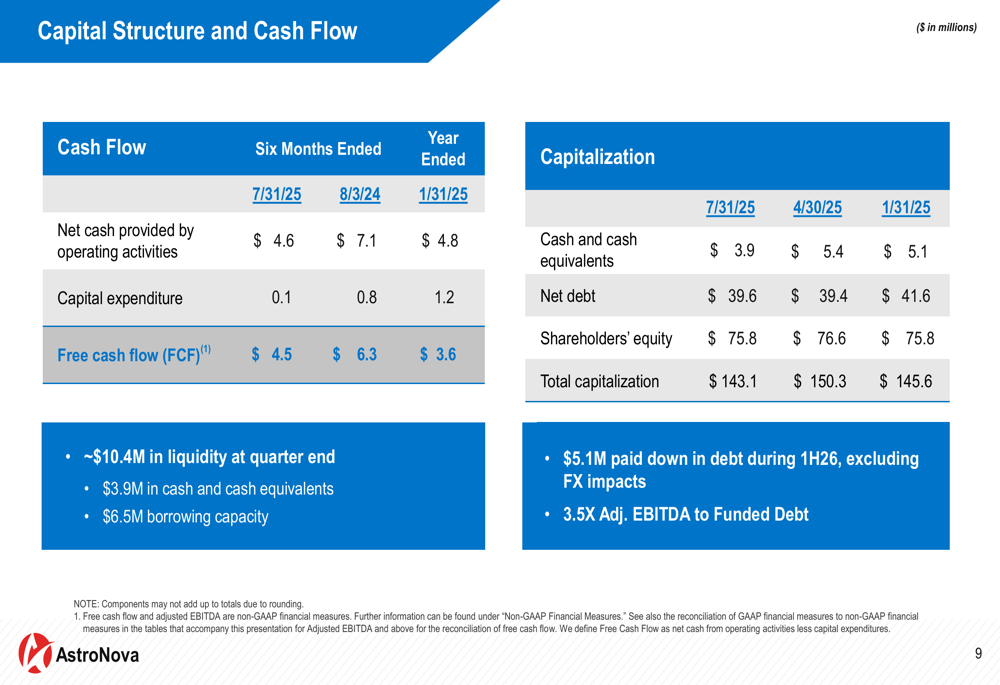

The company's capital structure remains relatively stable, with approximately $10.4 million in liquidity at quarter end, including $3.9 million in cash and cash equivalents and $6.5 million in borrowing capacity. AstroNova paid down $5.1 million in debt during the first half of fiscal 2026, excluding foreign exchange impacts, and reported an Adjusted EBITDA to Funded Debt ratio of 3.5x.

The following chart details the company's capital structure and cash flow:

While AstroNova faces significant near-term challenges, management's strategic reset and focus on operational improvements, cost reductions, and customer-centric initiatives aim to position the company for recovery and long-term growth. Investors will be closely monitoring the execution of these strategies and whether the anticipated second-half improvements materialize as projected.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.