Stock market today: S&P 500 climbs as health care, tech gain; Nvidia earnings loom

Introduction & Market Context

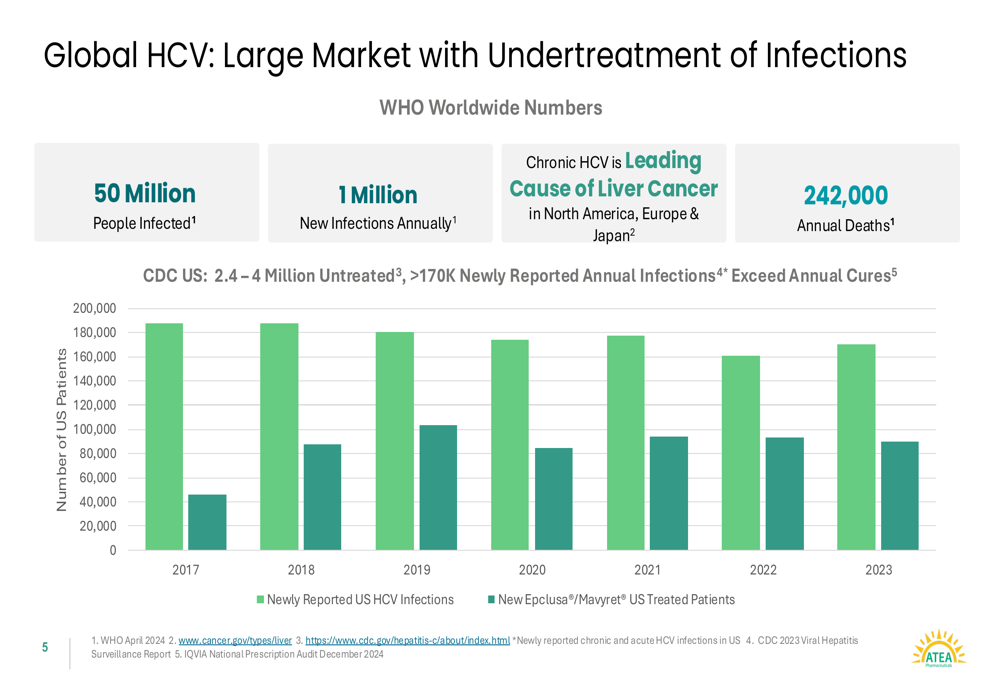

Atea Pharmaceuticals (NASDAQ:AVIR) presented its Q2 2025 corporate update on August 7, highlighting significant progress in its hepatitis C virus (HCV) treatment program and providing insights into its financial position. The company is developing a fixed-dose combination of bemnifosbuvir (BEM) and ruzasvir (RZR) for HCV, targeting a global market with 50 million infected individuals and approximately 1 million new infections annually.

The HCV market represents a substantial commercial opportunity, with global net sales estimated at approximately $3 billion in 2024, of which the U.S. accounts for roughly $1.5 billion. According to Atea, the market is primarily dominated by two products, with no competitors currently in clinical development, positioning the company favorably if its treatment receives regulatory approval.

As shown in the following chart detailing the global HCV market opportunity:

Quarterly Performance Highlights

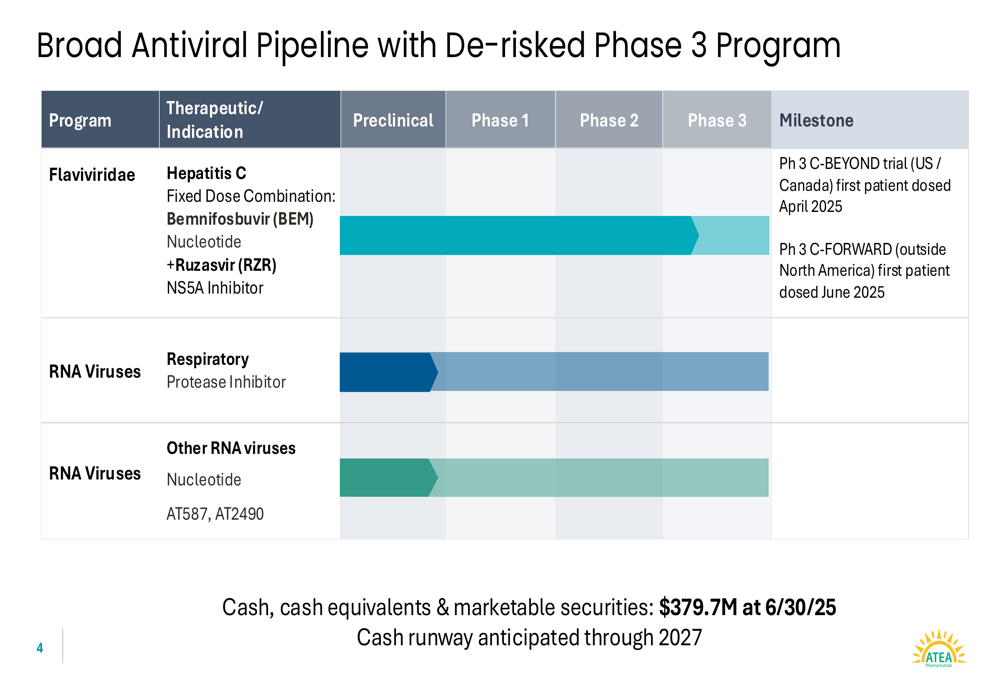

The second quarter of 2025 marked several key milestones for Atea’s HCV program. In April, the company dosed the first patient in its Phase 3 C-BEYOND trial in the U.S. and Canada, followed by the first patient dosed in the C-FORWARD trial outside North America in June. The company also presented four scientific posters at the European Association for the Study of the Liver (EASL) Congress in May 2025, showcasing final results from its global Phase 2 study.

On the business front, Atea authorized the repurchase of up to $25 million of the company’s common stock in April and reported that 4.6 million shares had been repurchased as of June 30, 2025. The company also refreshed its Board of Directors with the addition of Howard H. Berman, PhD, who brings over 20 years of entrepreneurial and life science industry experience.

Atea’s comprehensive antiviral pipeline, with its HCV program as the centerpiece, is illustrated below:

HCV Program Progress and Clinical Data

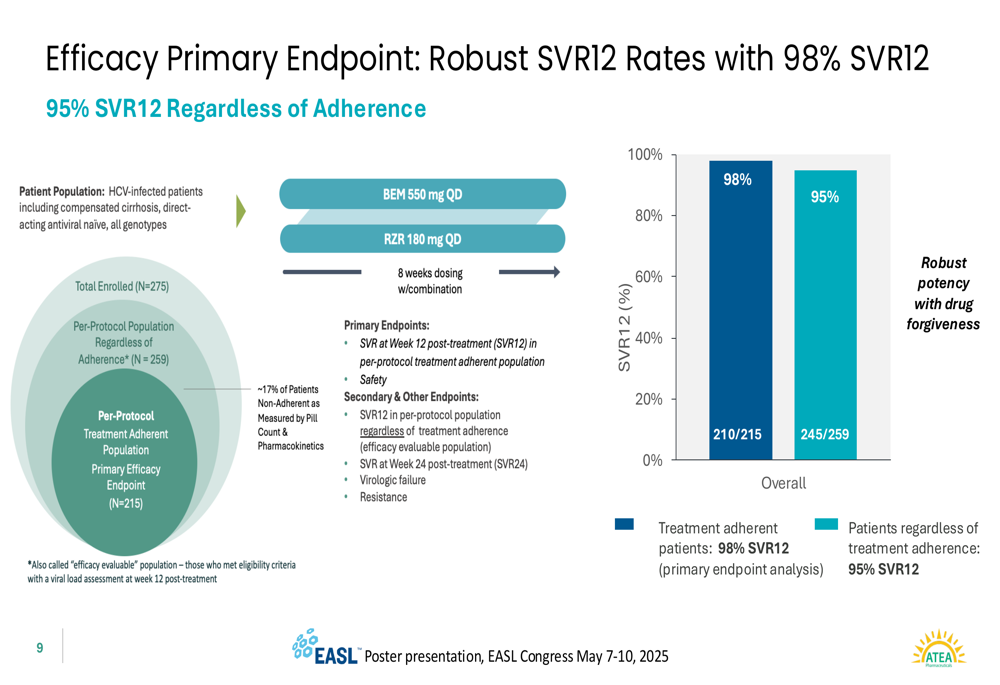

The BEM/RZR combination demonstrated impressive efficacy in Phase 2 trials, achieving a 98% sustained virologic response at 12 weeks post-treatment (SVR12) in treatment-adherent patients and 95% SVR12 regardless of adherence. The following chart illustrates these primary efficacy endpoints:

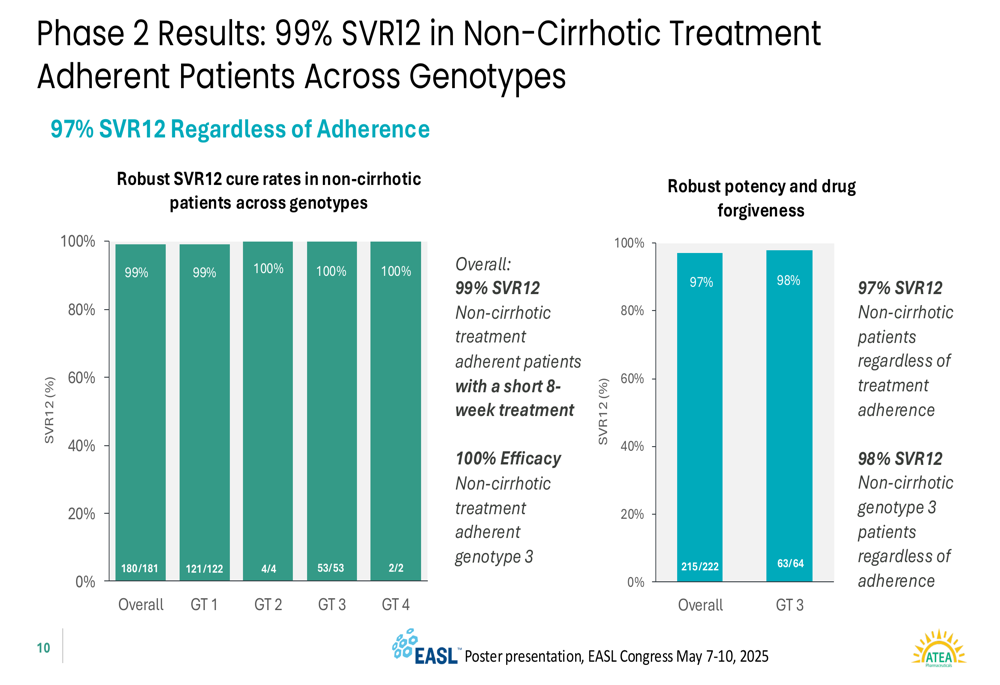

Particularly noteworthy were the results in non-cirrhotic treatment-adherent patients, where the regimen achieved a 99% SVR12 rate across genotypes with an 8-week treatment duration. The efficacy was consistent across different HCV genotypes, with 100% SVR12 rates observed in genotypes 2, 3, and 4.

The detailed breakdown of Phase 2 results across different genotypes is shown below:

Atea’s global Phase 3 program consists of two trials: C-BEYOND in the U.S. and Canada and C-FORWARD outside North America. These open-label studies will randomize approximately 1,760 patients (1:1) to receive either BEM/RZR or an active comparator (SOF/VEL). The trials include both non-cirrhotic patients (8 weeks of BEM/RZR vs. 12 weeks of comparator) and those with compensated cirrhosis (12 weeks of treatment for both regimens).

Commercial Opportunity (SO:FTCE11B) and Market Research

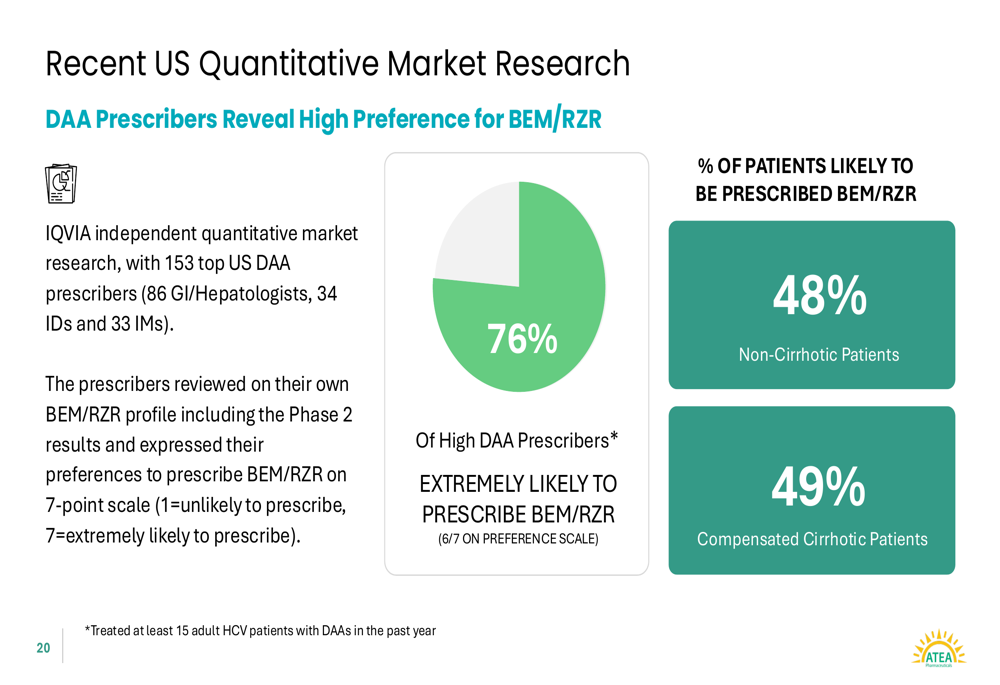

Atea presented compelling market research data suggesting strong physician preference for its BEM/RZR regimen. In a recent quantitative study conducted by IQVIA involving 153 top U.S. direct-acting antiviral (DAA) prescribers, 76% indicated they were extremely likely to prescribe BEM/RZR. This preference has been consistent across multiple studies, with predicted market share ranging from 34% to 48% between December 2023 and June 2025.

The strong prescriber preference for BEM/RZR is illustrated in the following chart:

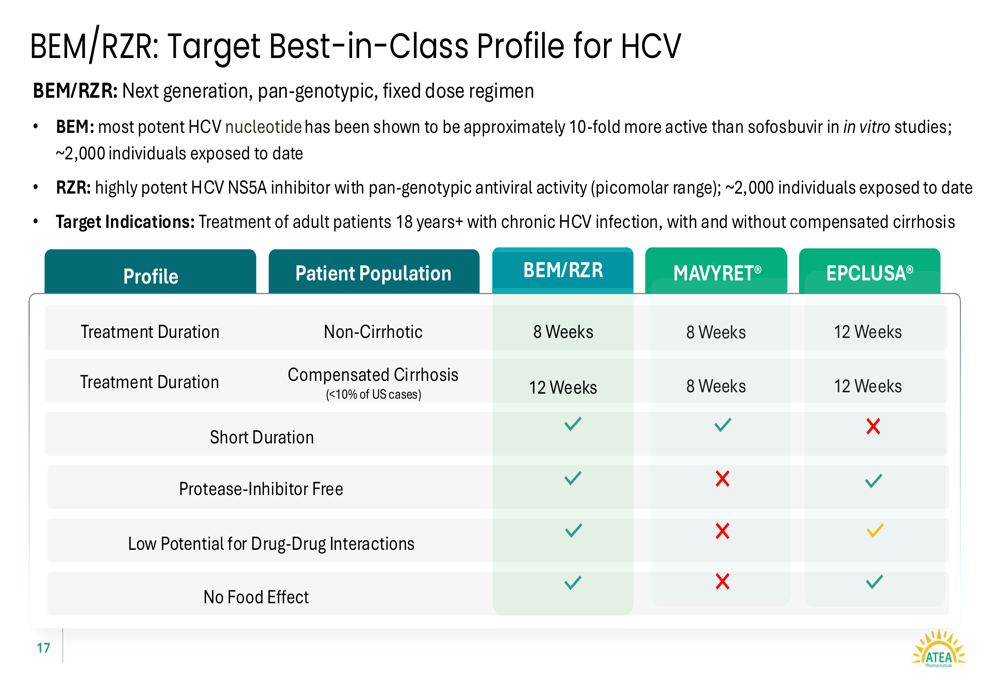

Atea positions BEM/RZR as a potential best-in-class treatment with several advantages over existing therapies, including shorter treatment duration for non-cirrhotic patients (8 weeks vs. 12 weeks for EPCLUSA), no protease inhibitor component, low potential for drug-drug interactions, and no food effect requirements. The competitive positioning of BEM/RZR compared to market leaders MAVYRET and EPCLUSA is shown below:

Financial Analysis

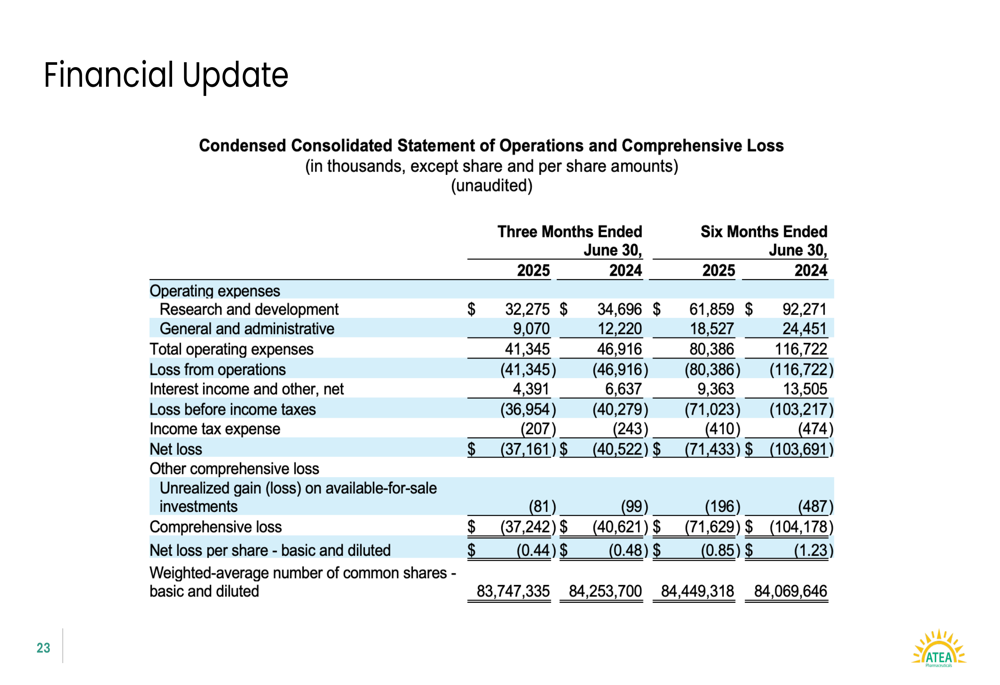

For the three months ended June 30, 2025, Atea reported research and development expenses of $32.3 million and general and administrative expenses of $9.1 million, resulting in a net loss of $37.2 million ($0.44 per share). For the six-month period, the company posted a net loss of $71.4 million ($0.85 per share).

The company’s condensed consolidated statement of operations is presented below:

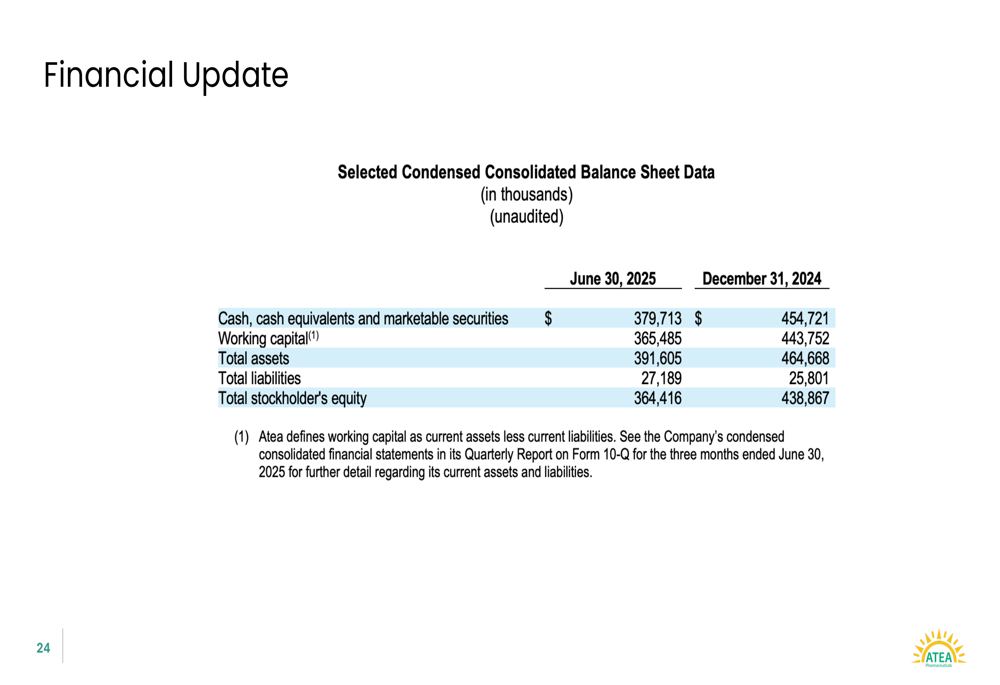

Atea maintained a strong balance sheet with $379.7 million in cash, cash equivalents, and marketable securities as of June 30, 2025, compared to $454.7 million at the end of 2024. The company expects its cash runway to extend through 2027, providing sufficient resources to advance its clinical programs.

The key balance sheet metrics are shown in the following table:

Forward-Looking Statements

Looking ahead, Atea is focused on advancing its Phase 3 HCV program, with both the C-BEYOND and C-FORWARD trials now enrolling patients. The company is targeting approximately 240 clinical trial sites globally, with 120 sites in the U.S. and Canada for C-BEYOND and 120 sites across 16 countries for C-FORWARD.

Based on the strong Phase 2 data and positive market research, Atea believes BEM/RZR has the potential to become a best-in-class treatment for HCV. The company’s cash position is expected to support operations through 2027, though this represents a slight reduction from the previous projection of runway into 2028 mentioned in the Q4 2024 earnings report.

Atea’s stock closed at $3.46 on August 7, 2025, down 0.86% for the day. The stock has traded between $2.46 and $4.15 over the past 52 weeks, reflecting the ongoing challenges faced by clinical-stage biotech companies in the current market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.