German construction sector still in recession, civil engineering only bright spot

Autodesk Inc (NASDAQ:ADSK) reported strong second-quarter fiscal 2026 results on August 28, 2025, with accelerating revenue growth and substantial increases in billings and cash flow. The design software leader’s stock edged up 0.79% in after-hours trading to $288.20, following a regular session close of $285.95.

Quarterly Performance Highlights

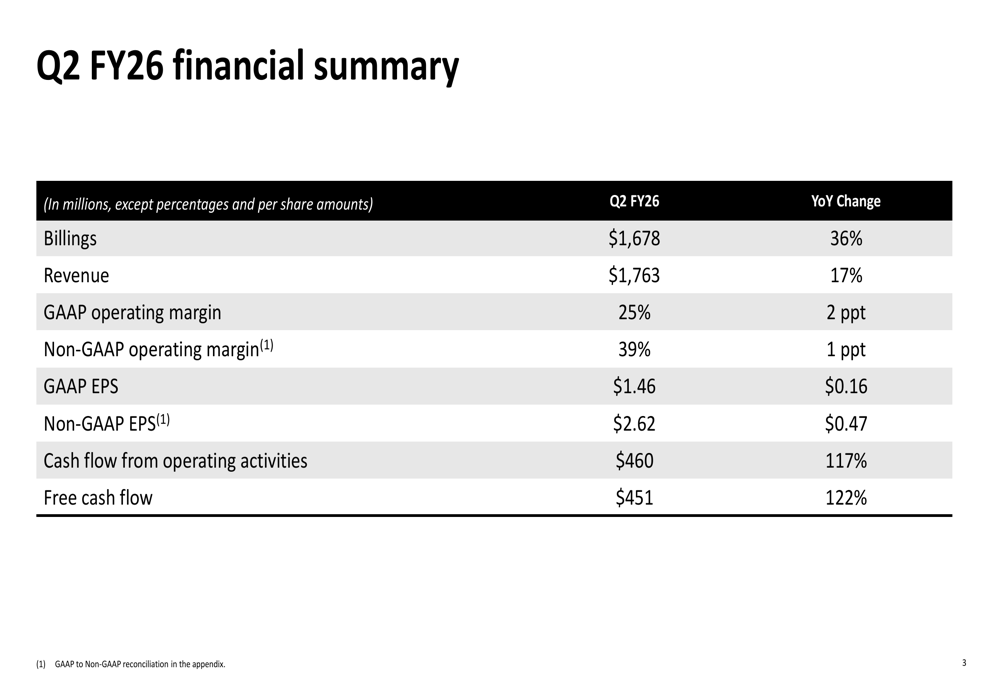

Autodesk delivered impressive financial results across all key metrics in Q2 FY26. Revenue reached $1.76 billion, representing 17% year-over-year growth, while billings surged 36% to $1.68 billion. The company also demonstrated significant margin improvements, with GAAP operating margin increasing by 2 percentage points to 25% and non-GAAP operating margin rising 1 percentage point to 39%.

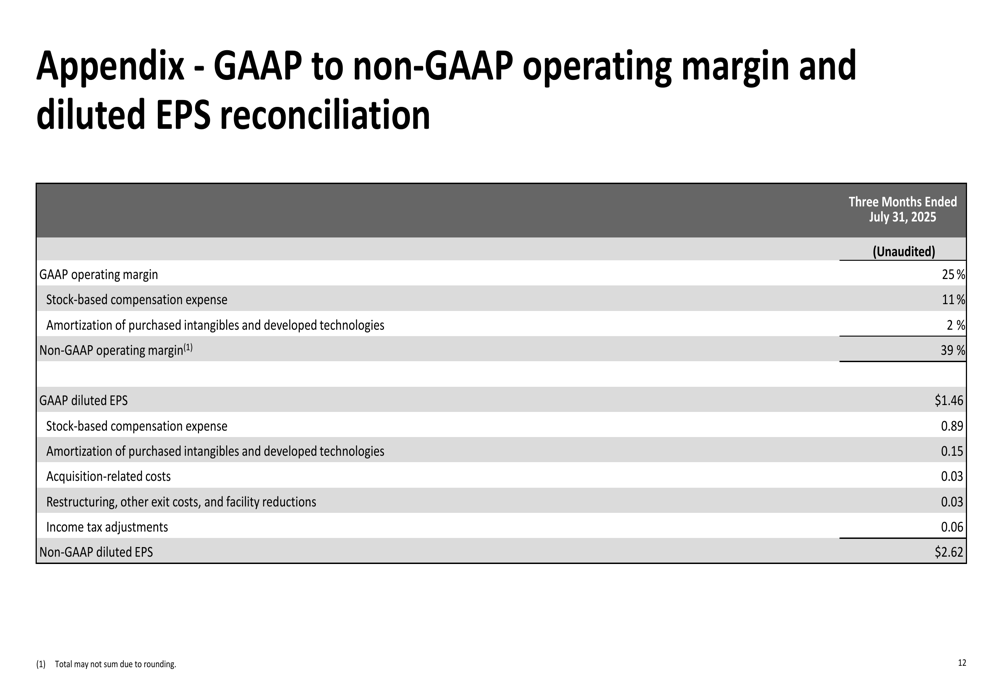

As shown in the following financial summary chart, Autodesk’s earnings per share also showed substantial growth, with GAAP EPS increasing by $0.16 to $1.46 and non-GAAP EPS climbing $0.47 to $2.62:

Cash flow metrics were particularly strong, with cash flow from operating activities more than doubling to $460 million (up 117%) and free cash flow rising 122% to $451 million. The company also returned $356 million to shareholders through share repurchases during the quarter.

Detailed Financial Analysis

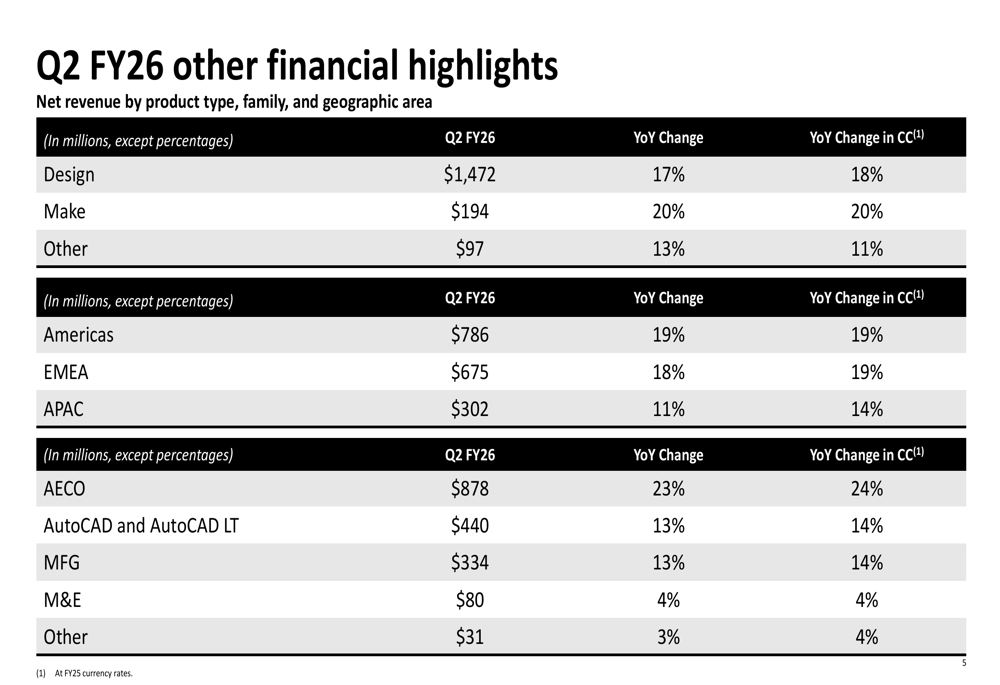

Autodesk’s growth was broad-based across product categories and geographic regions. The company’s core Design business generated $1.47 billion in revenue (up 17%), while the Make segment grew 20% to $194 million. From a geographic perspective, the Americas led with 19% growth to $786 million, followed by EMEA (Europe, Middle East, and Africa) at 18% growth to $675 million, and Asia-Pacific at 11% growth to $302 million.

The following breakdown illustrates Autodesk’s diversified revenue streams by product type, geographic area, and product family:

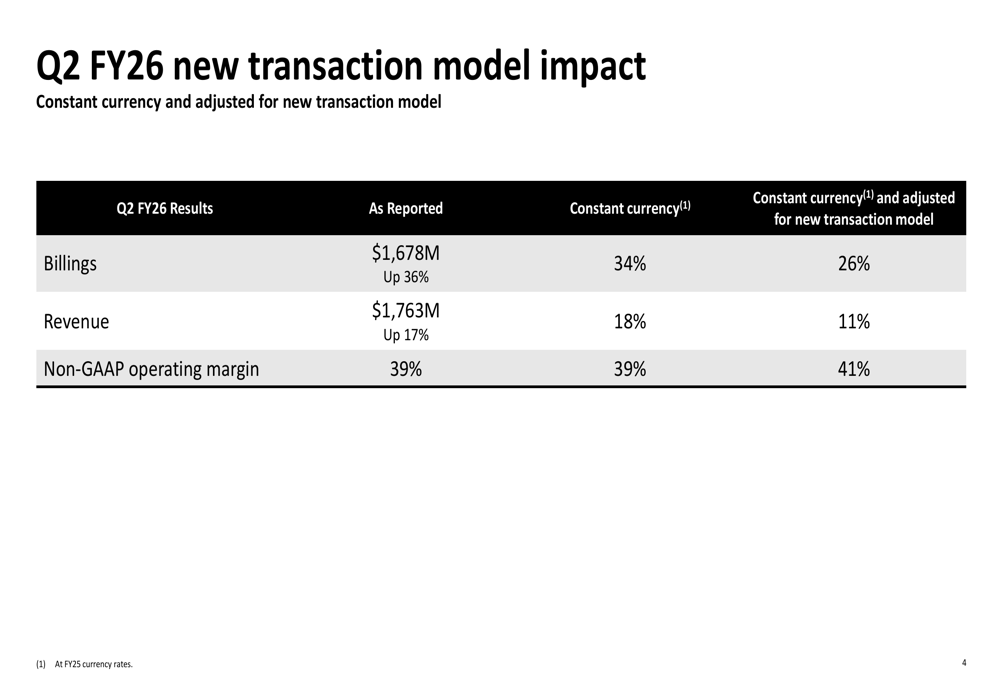

A significant factor affecting Autodesk’s reported results is its new transaction model. When adjusted for constant currency and the impact of this new model, the company’s underlying growth rates remain solid but are more modest than the headline figures. Billings growth would be 26% (versus the reported 36%), while revenue growth would be 11% (versus the reported 17%).

The following chart details how currency fluctuations and the new transaction model impact the reported results:

Autodesk also reported strong metrics related to future revenue visibility. Remaining performance obligations (RPO) increased 24% to $7.3 billion, while current RPO grew 20% to $4.68 billion. The company’s net revenue retention rate remained healthy at above 110% in constant currency, partly influenced by the new transaction model.

Forward-Looking Statements

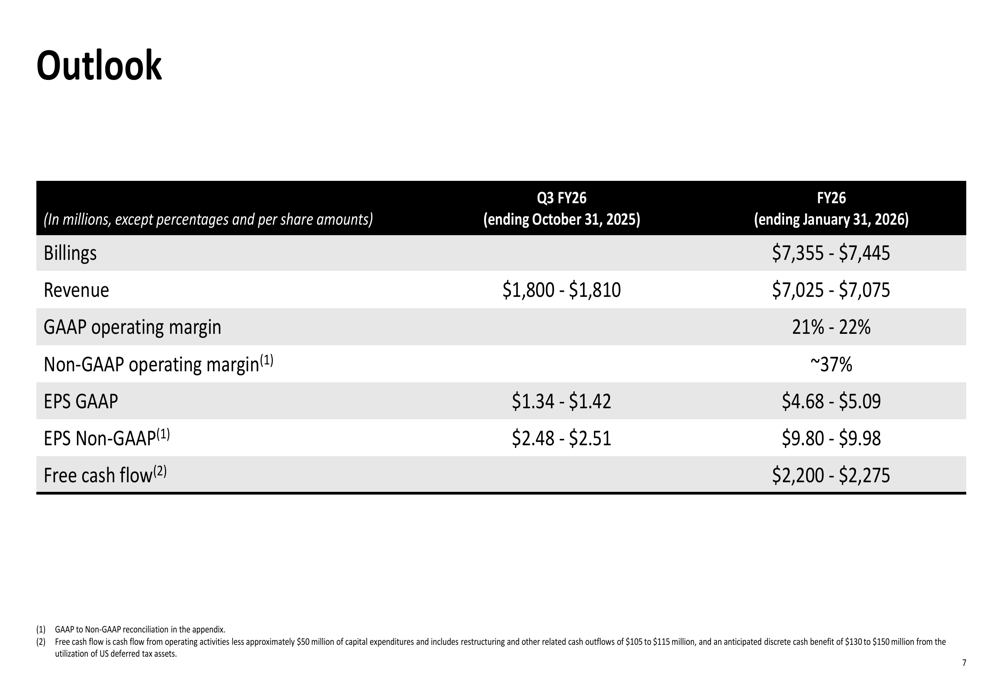

For the third quarter of fiscal 2026, Autodesk expects revenue between $1.80 billion and $1.81 billion, with non-GAAP EPS ranging from $2.48 to $2.51. For the full fiscal year 2026, the company projects revenue of $7.03-$7.08 billion, representing approximately 15% growth.

The company’s detailed financial outlook is presented in the following guidance table:

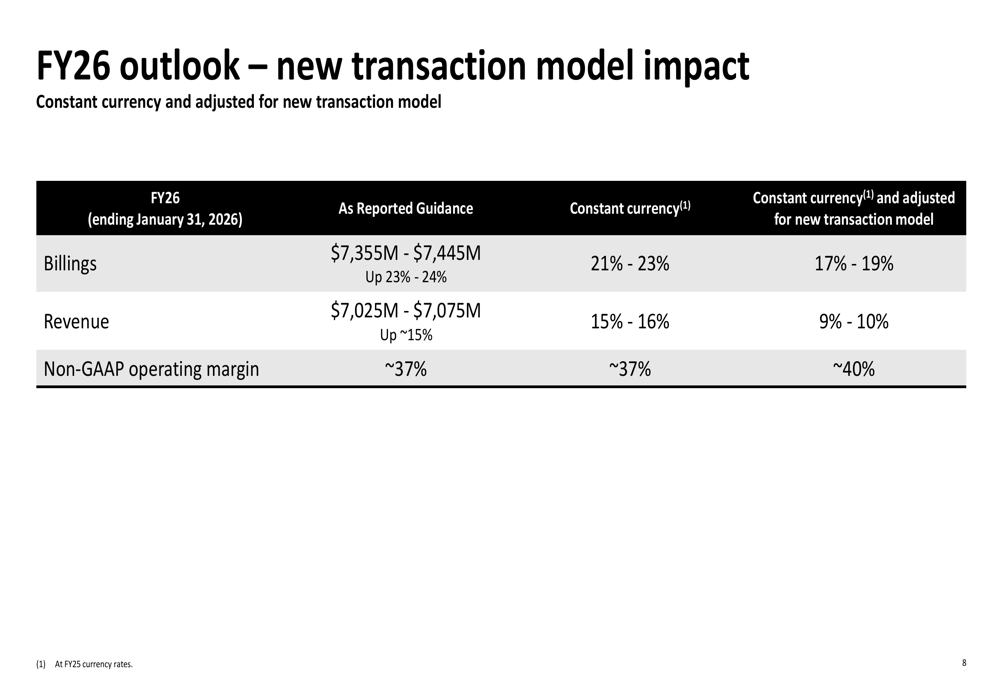

Similar to the quarterly results, Autodesk’s full-year outlook is significantly impacted by the new transaction model. When adjusted for constant currency and the new model, the underlying revenue growth for FY26 is projected at 9-10%, compared to the reported outlook of approximately 15%.

The following chart illustrates how the new transaction model affects the company’s full-year guidance:

Autodesk expects its non-GAAP operating margin to remain at approximately 37% for fiscal 2026, while free cash flow is projected to reach $2.20-$2.28 billion. The company anticipates that the majority of second-half free cash flow will be weighted toward the fourth quarter.

Strategic Initiatives

Autodesk’s strong performance reflects its successful execution across multiple product families. The Architecture, Engineering, Construction, and Operations (AECO) segment led growth with a 23% increase to $878 million, while AutoCAD and AutoCAD LT grew 13% to $440 million. The Manufacturing segment also showed solid performance with 13% growth to $334 million.

The company’s transition to a subscription-based business model continues to progress, with subscription revenue driving the majority of growth. This shift provides Autodesk with greater revenue predictability and customer retention, as evidenced by the net revenue retention rate exceeding 110%.

Autodesk’s reconciliation of GAAP to non-GAAP metrics highlights the impact of stock-based compensation and amortization of intangibles on its reported results:

With a 52-week trading range of $232.67 to $326.62, Autodesk’s current stock price of $285.95 sits in the middle of its yearly range. The company’s strong Q2 results and solid outlook suggest continued momentum as it executes on its strategic initiatives and navigates the transition to its new transaction model.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.