German construction sector still in recession, civil engineering only bright spot

Azenta Inc. (NASDAQ:AZTA) presented its fiscal second quarter 2025 financial results on May 7, 2025, showing a return to growth with revenue increases across both of its core business segments and significant margin improvement. The life sciences company, which has been undergoing a strategic transformation, reported positive momentum as it continues to execute on its "Ascend 2026" program.

Quarterly Performance Highlights

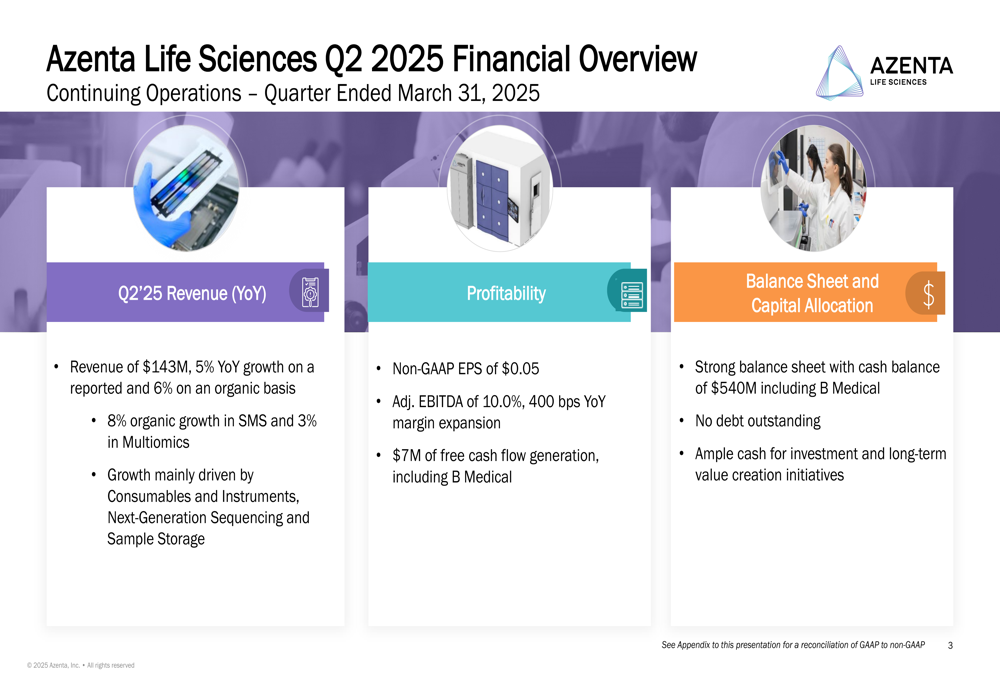

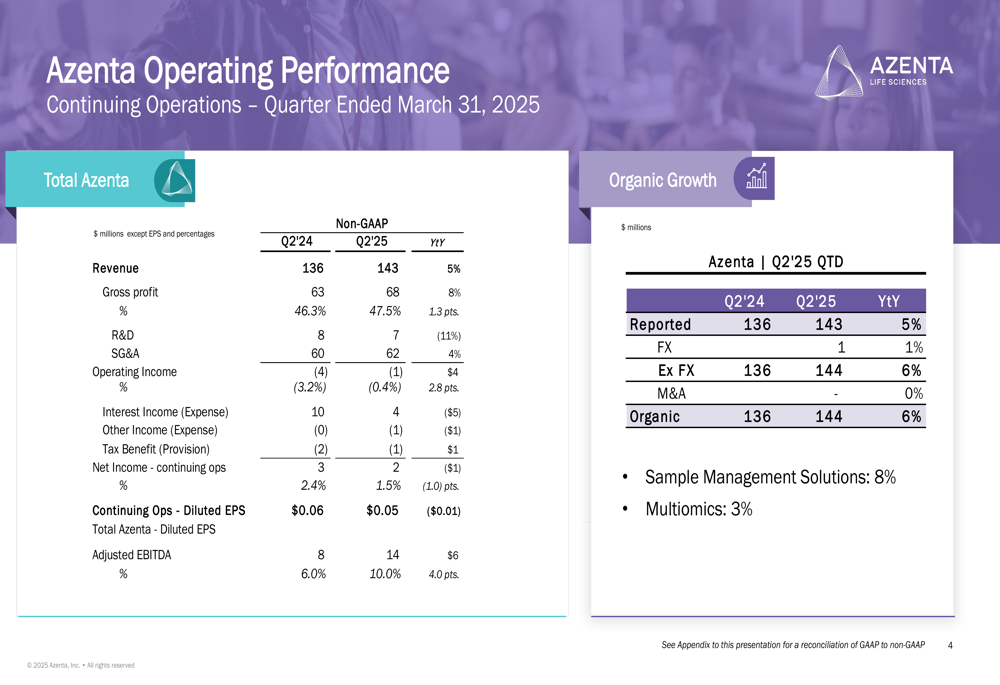

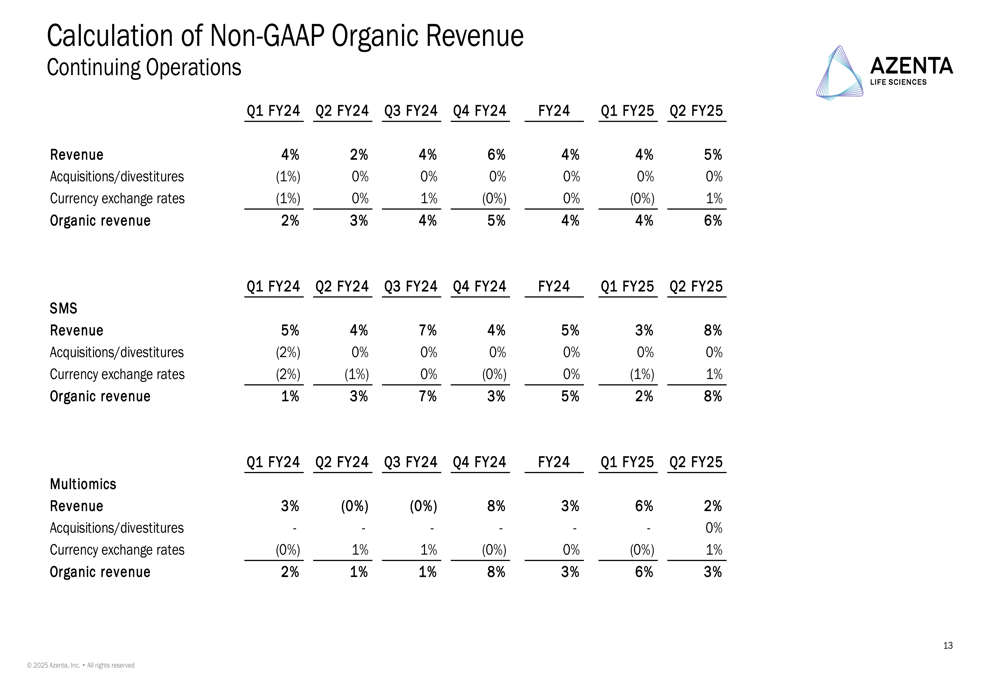

Azenta reported Q2 2025 revenue of $143 million, representing 5% year-over-year growth on a reported basis and 6% on an organic basis. The company achieved a non-GAAP EPS of $0.05 and an adjusted EBITDA margin of 10.0%, marking a substantial 400 basis points year-over-year expansion.

"Our second quarter results demonstrate meaningful progress in our transformation efforts, with both revenue growth and significant margin improvement," the company stated in its presentation.

The financial performance represents a notable improvement from the company’s fiscal 2024 results, when Azenta experienced an overall revenue decline of 2%. The current quarter’s positive trajectory aligns with management’s previously stated focus on enhancing profitability while driving growth in core segments.

Segment Analysis

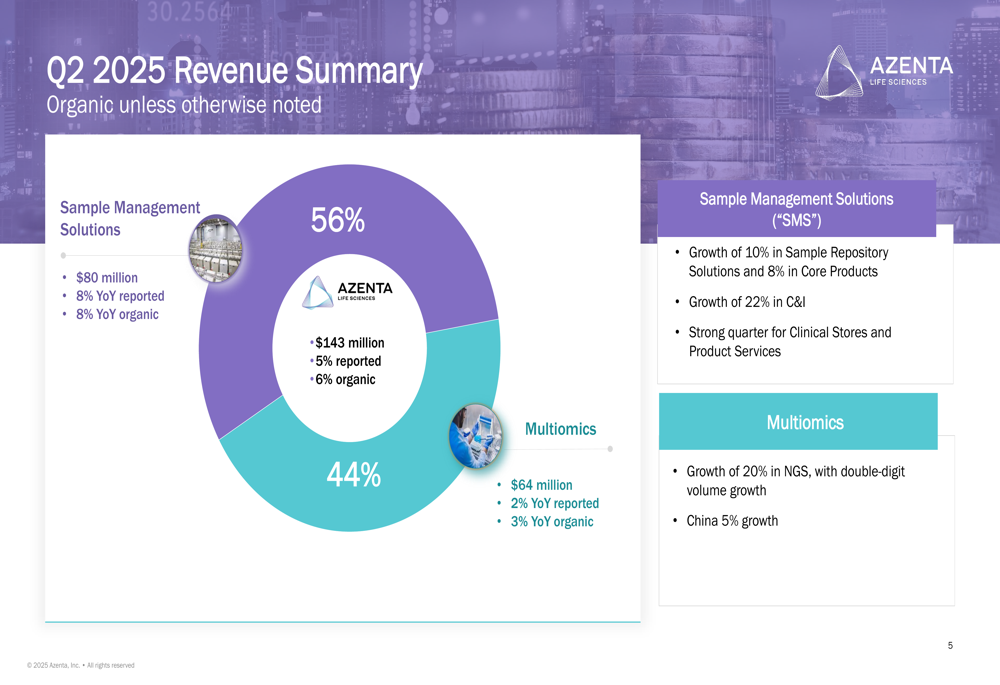

Sample Management Solutions (SMS) emerged as the stronger performer, accounting for 56% of total revenue at $80 million. This segment achieved 8% year-over-year growth on both a reported and organic basis, driven primarily by consumables, instruments, and sample storage services.

Multiomics, representing 44% of revenue at $64 million, delivered more modest growth of 2% year-over-year on a reported basis and 3% organically. Within this segment, Next-Generation Sequencing (NGS) services stood out with impressive 20% growth.

The company also highlighted 5% growth in China, suggesting resilience in this key market despite broader macroeconomic challenges.

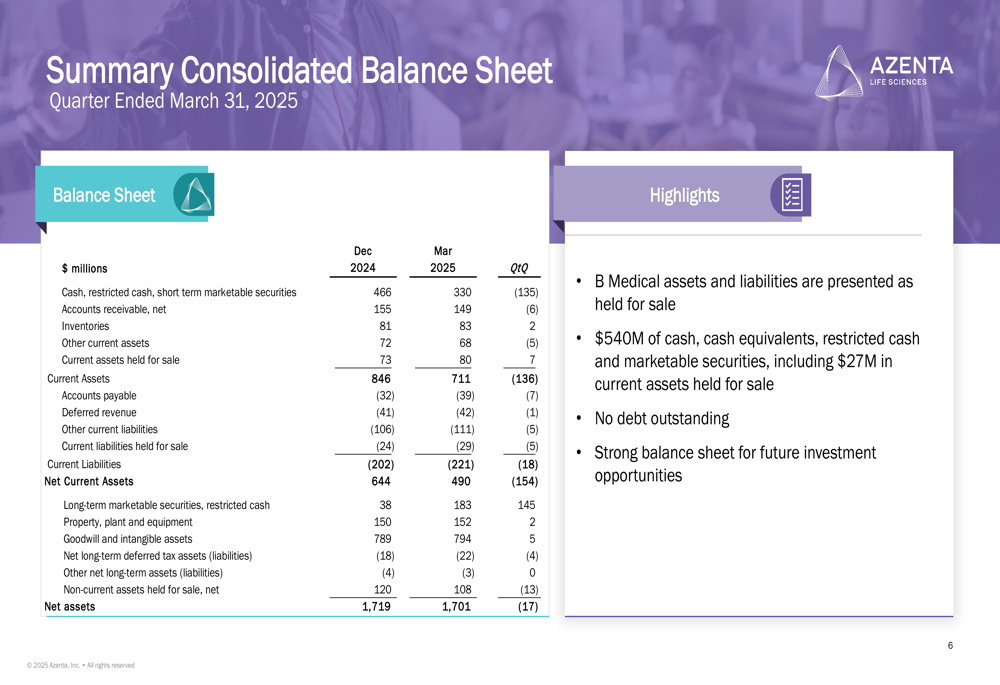

Balance Sheet and Cash Flow

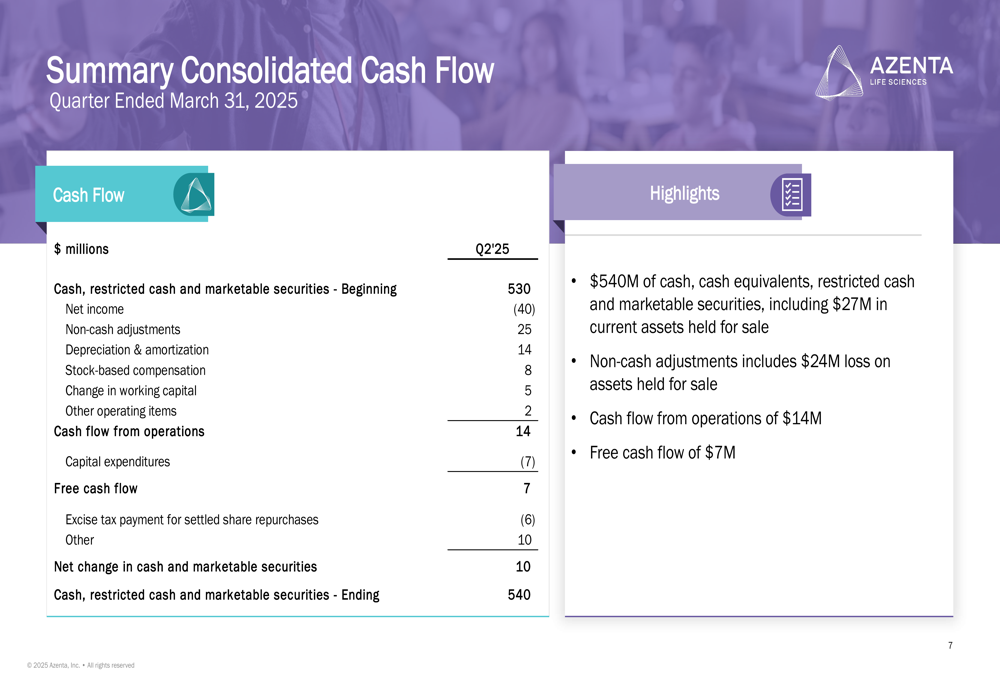

Azenta maintained a strong financial position with $540 million in cash (including B Medical (TASE:BLWV) assets), and no debt outstanding. The company generated $7 million in free cash flow during the quarter, including contributions from B Medical, which is being prepared for divestiture as announced in previous quarters.

"Our robust balance sheet provides us with ample flexibility for strategic investments and long-term value creation initiatives," the company noted in its presentation.

The consolidated balance sheet showed total current assets of $711 million and net current assets of $490 million as of March 31, 2025. B Medical assets and liabilities are presented as held for sale, consistent with the company’s previously announced strategic decision to divest this business unit.

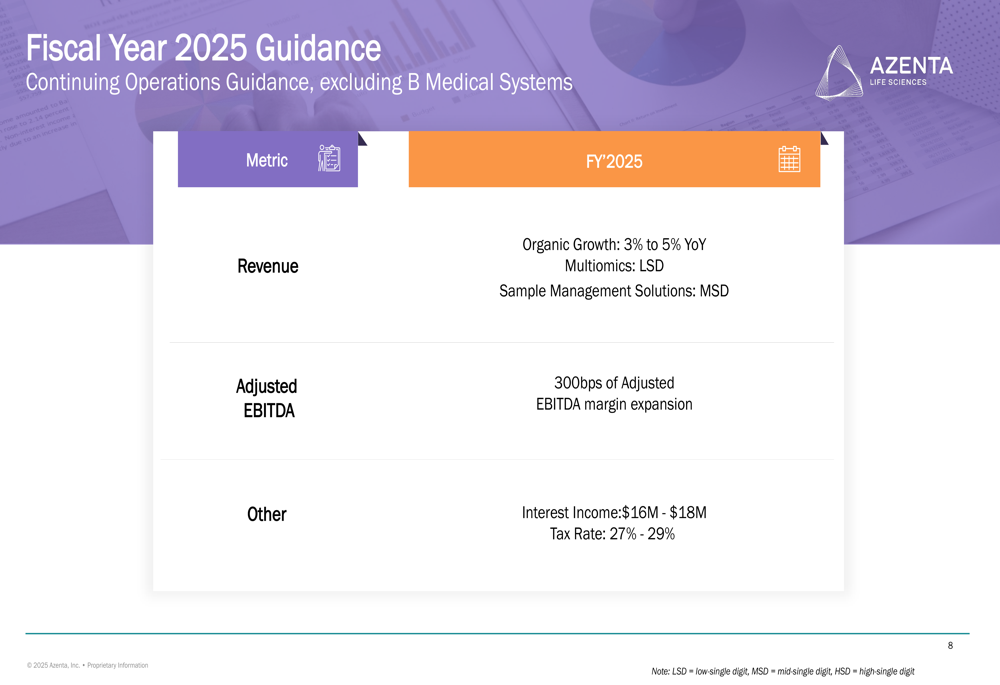

Forward Guidance

Looking ahead, Azenta provided fiscal year 2025 guidance that excludes B Medical Systems. The company projects organic revenue growth of 3% to 5% year-over-year, with Multiomics expected to deliver low-single-digit growth and Sample Management Solutions anticipated to achieve mid-single-digit growth.

Management forecasts a 300 basis point improvement in adjusted EBITDA margin for the full fiscal year, continuing the positive trend seen in Q2. Interest income is projected to be $16-18 million, with an expected tax rate of 27-29%.

Market Context and Stock Performance

The positive quarterly results come at a critical time for Azenta, whose stock has been trading near 52-week lows of $24.06, far below its 52-week high of $63.58. Following the earnings release, AZTA shares showed signs of recovery, trading up 5.35% in premarket activity to $26.78.

The company’s return to growth and margin expansion appear to be resonating with investors who have been waiting for tangible results from Azenta’s ongoing transformation program. The significant improvement in adjusted EBITDA margin suggests that cost-control measures and operational efficiencies are beginning to yield results.

Azenta’s Q2 2025 presentation demonstrates progress in the company’s strategic initiatives, with organic growth across both business segments and substantial margin improvement. As the company continues to execute on its transformation program and prepares to divest B Medical, investors will be watching closely to see if this positive momentum can be sustained throughout fiscal 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.