German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

Backblaze Inc. (NASDAQ:BLZE) presented its Q2 2025 results on August 7, 2025, revealing accelerated growth in its cloud storage business and improved profitability metrics. The company’s stock surged 18.27% following the presentation, reflecting investor optimism about the company’s performance and outlook.

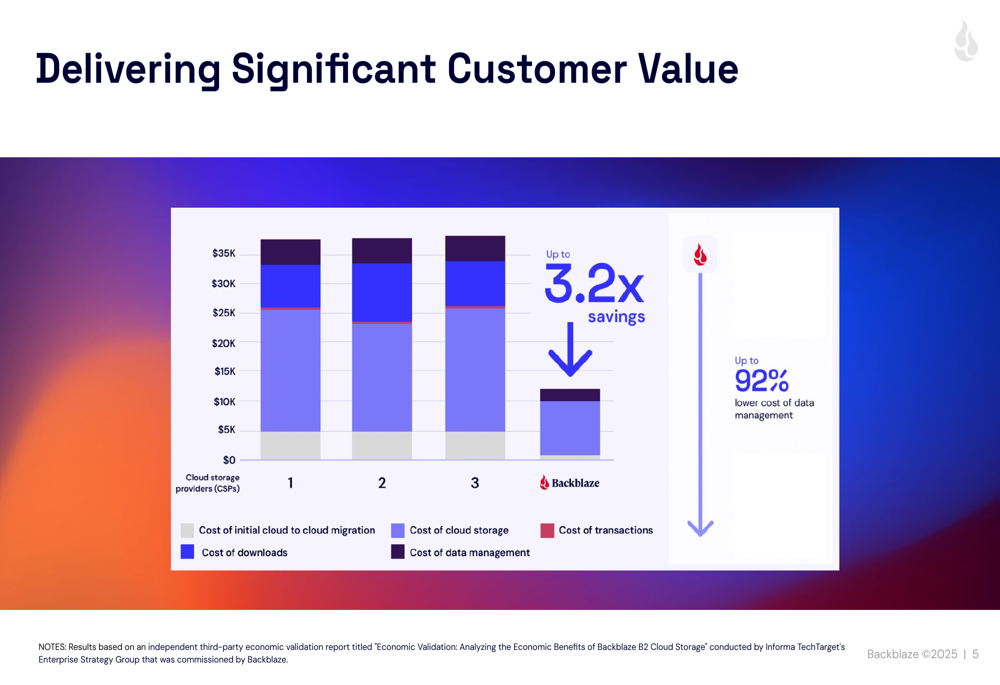

The cloud storage provider highlighted its cost advantage over larger competitors, positioning itself as a value alternative in an increasingly competitive market. According to an independent third-party economic validation, Backblaze offers up to 3.2x savings compared to other cloud storage providers (CSPs) and up to 92% lower cost of data management.

As shown in the following comparison of costs between Backblaze and other cloud storage providers:

Quarterly Performance Highlights

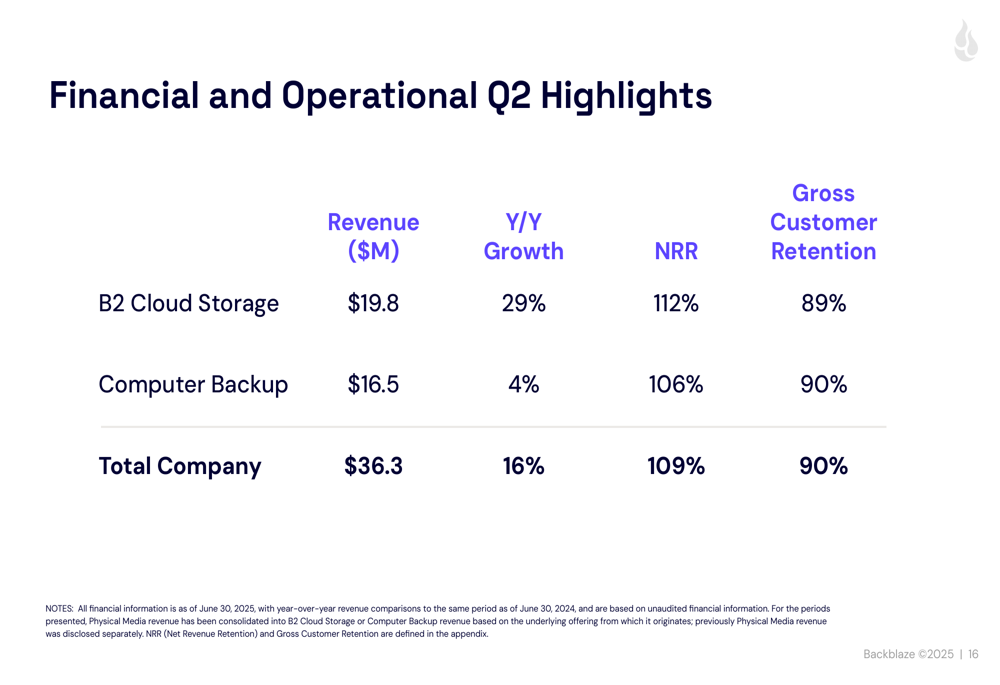

Backblaze reported total Q2 2025 revenue of $36.3 million, representing 16% year-over-year growth. The company’s B2 Cloud Storage segment continued to be the primary growth driver, with revenue reaching $19.8 million, up 29% year-over-year – a significant acceleration from the 23% growth recorded in Q1 2025.

The Computer Backup segment generated $16.5 million in revenue, growing at a more modest 4% year-over-year. The company maintained strong customer retention metrics, with 90% gross customer retention across all products and a net revenue retention (NRR) rate of 109% for the total company and 112% specifically for B2 Cloud Storage.

The following slide details the comprehensive financial and operational metrics for Q2 2025:

CEO Gleb Budman and CFO Marc Suidan emphasized several key highlights from the quarter, including the accelerated B2 growth, doubled Adjusted EBITDA compared to last year, a new $20 million line of credit, and the approval of a cash-neutral stock buyback program.

As shown in the key financial highlights from Q2 2025:

AI Growth Strategy

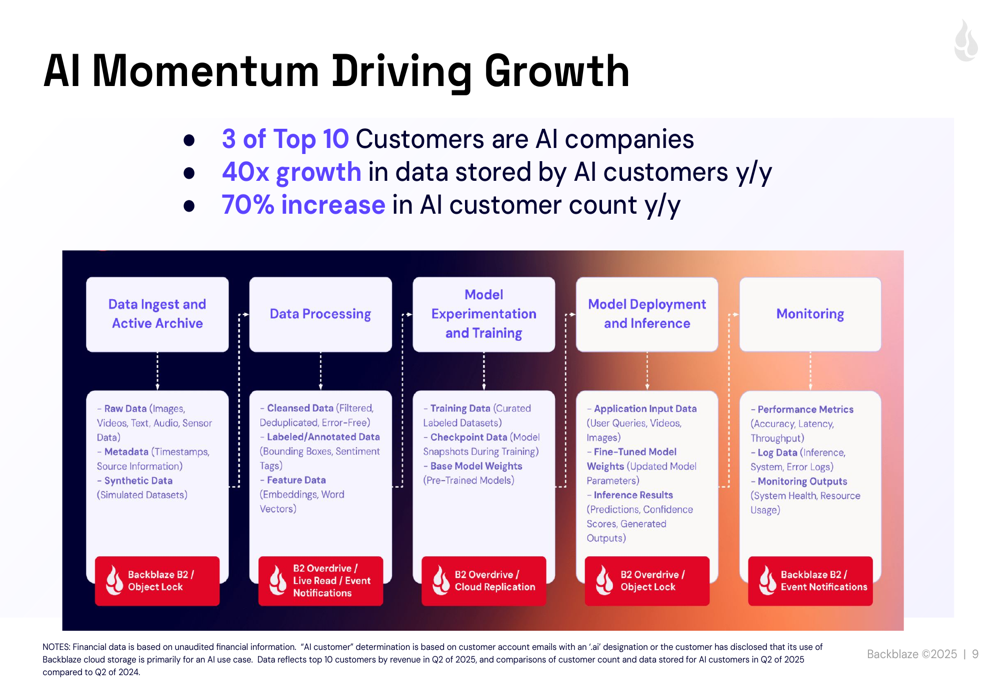

A significant driver of Backblaze’s accelerating growth is the company’s success in the artificial intelligence sector. The presentation revealed that three of Backblaze’s top 10 customers are AI companies, with data stored by AI customers growing 40x year-over-year and a 70% increase in AI customer count over the same period.

The company is strategically positioning its storage solutions within the AI workflow, from data ingest and active archive to model training and deployment. This approach appears to be gaining traction with AI-focused customers seeking cost-effective storage solutions.

The following slide illustrates the AI momentum driving Backblaze’s growth:

Backblaze also highlighted a customer win with a generative AI video company that chose B2 Overdrive, resulting in a six-figure deal and displacement of a hyperscaler competitor. According to a testimonial from the customer’s Head of AI: "Backblaze B2 Overdrive delivered the speed and flexibility we needed-with unlimited egress and real human support. The performance and cost savings were clear."

Financial Analysis & Profitability Path

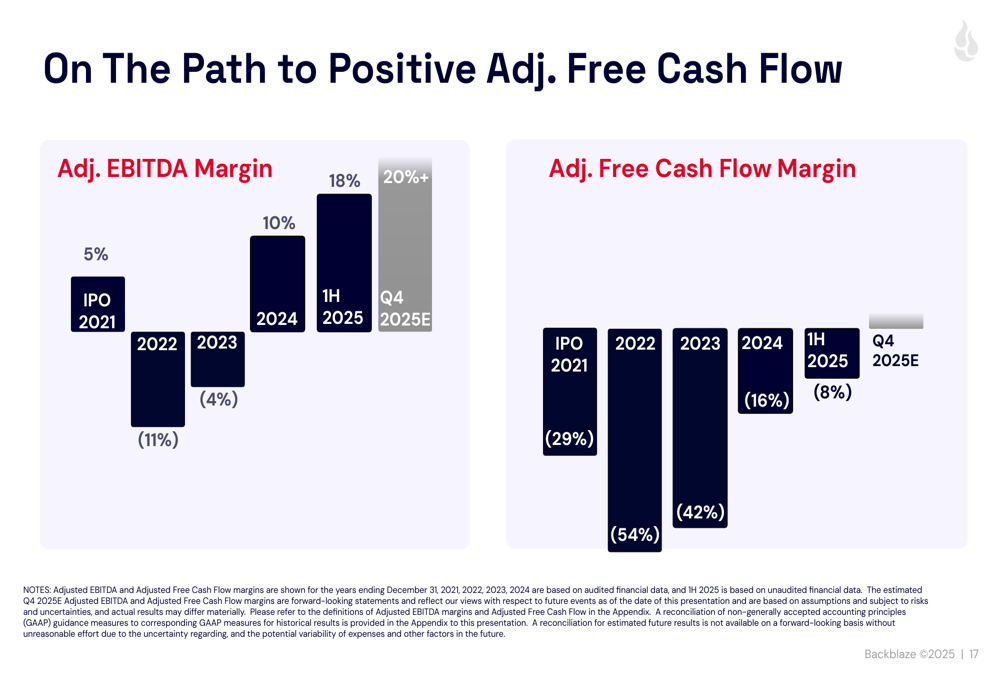

Backblaze continues to make progress toward sustainable profitability. The company’s Adjusted EBITDA margin reached 18% in the first half of 2025, doubling compared to the previous year. The Adjusted Free Cash Flow margin improved to -8% in 1H 2025, compared to -16% in 2024 and -42% in 2023.

The company’s financial transformation over the past year has focused on three key areas: solidifying the balance sheet, achieving sustainable profitability, and accelerating growth. Recent achievements include improving the current ratio to above 1, securing a new line of credit, implementing zero-based budgeting, and delivering two consecutive quarters of accelerated B2 revenue growth.

The following chart illustrates Backblaze’s progress toward positive adjusted free cash flow:

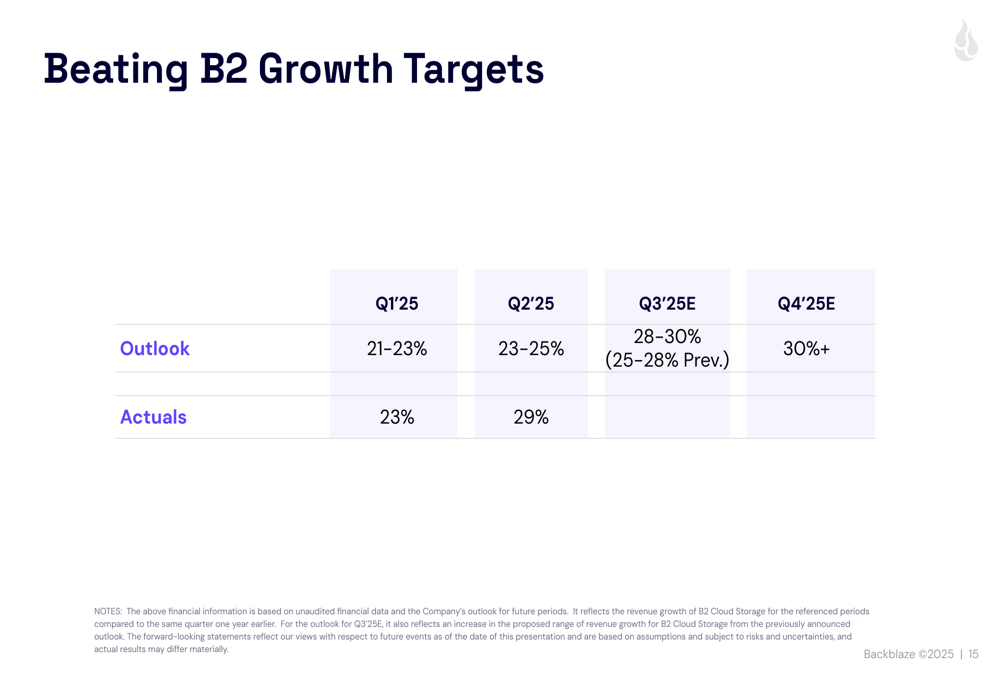

Backblaze has consistently exceeded its B2 growth targets in recent quarters. For Q2 2025, the company had projected 23-25% growth but delivered 29%. This outperformance has led to increased confidence in future growth, with the company now targeting 30%+ B2 growth by Q4 2025.

As shown in the comparison between outlook and actual results:

The company also approved a $10 million stock buyback program designed to reduce equity dilution. The program will be funded with proceeds from stock options exercised and the Employee Stock Purchase Plan over a 12-month window, making it cash neutral.

Forward Guidance & Strategic Initiatives

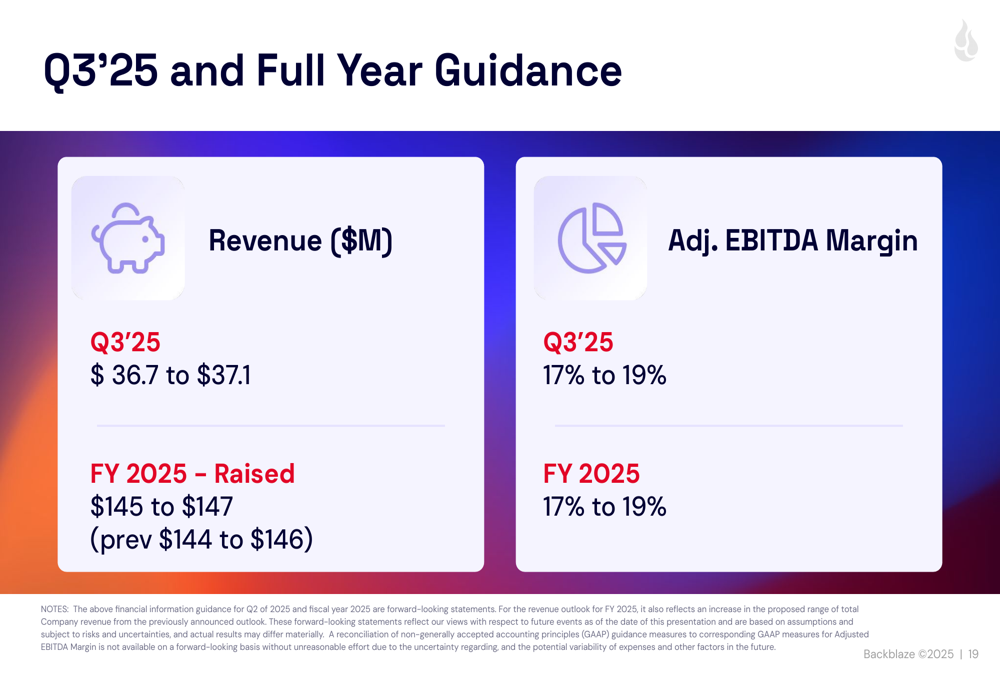

Backblaze raised its full-year 2025 revenue guidance to $145-147 million, up from the previous guidance of $144-146 million. For Q3 2025, the company expects revenue between $36.7-37.1 million and an Adjusted EBITDA margin of 17-19%.

The following slide details the company’s guidance for Q3 and full-year 2025:

On the strategic front, Backblaze launched several new cybersecurity features to enhance its competitive positioning, including:

1. Anomaly Alerts for data exfiltration and ransomware protection

2. Enterprise Web Console with role-based access controls

3. Bucket Access Logs providing granular data usage and access visibility

The company is also transforming its go-to-market approach by upskilling its sales team, deepening partnerships, and executing core sales plays. These initiatives appear to be bearing fruit, with B2 growth accelerating to 29% and a 30% year-over-year increase in customers with $50,000+ annual recurring revenue.

As shown in the company’s go-to-market transformation slide:

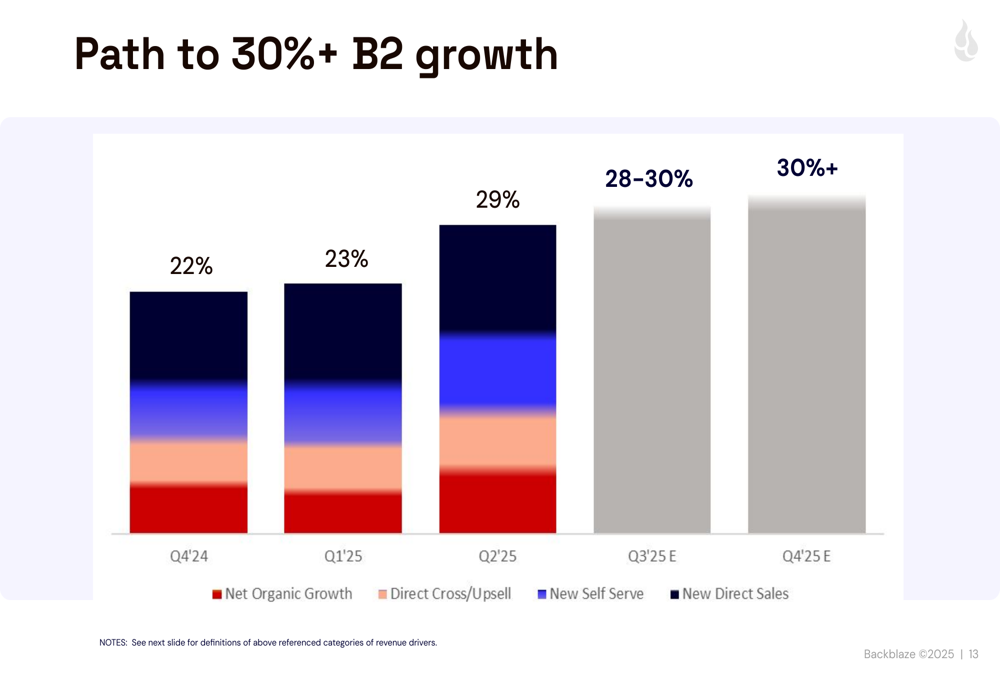

Backblaze’s path to achieving 30%+ B2 growth relies on multiple revenue drivers, including new direct sales, new self-serve customers, direct cross-sell/upsell opportunities, and net organic growth. The company expects to reach this growth target by Q4 2025.

The following chart visualizes Backblaze’s path to 30%+ B2 growth:

With its focus on AI-driven growth, improving profitability metrics, and strategic initiatives in cybersecurity and go-to-market transformation, Backblaze appears well-positioned to continue its growth trajectory through the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.