Bitcoin price today: gains to $120k, near record high on U.S. regulatory cheer

Introduction & Market Context

Banc of California (NYSE:BANC) (NYSE:CALB) released its first quarter 2025 financial results presentation, highlighting significant year-over-year earnings growth, continued net interest margin expansion, and solid loan growth. The bank demonstrated resilience in a challenging interest rate environment, with earnings per share more than doubling compared to the same period last year.

The bank’s strategic focus on growing noninterest-bearing deposits, diversifying its loan portfolio, and maintaining strong capital levels has positioned it well in the competitive California banking landscape. The presentation reveals a bank that has successfully navigated the interest rate cycle while continuing to build shareholder value.

Quarterly Performance Highlights

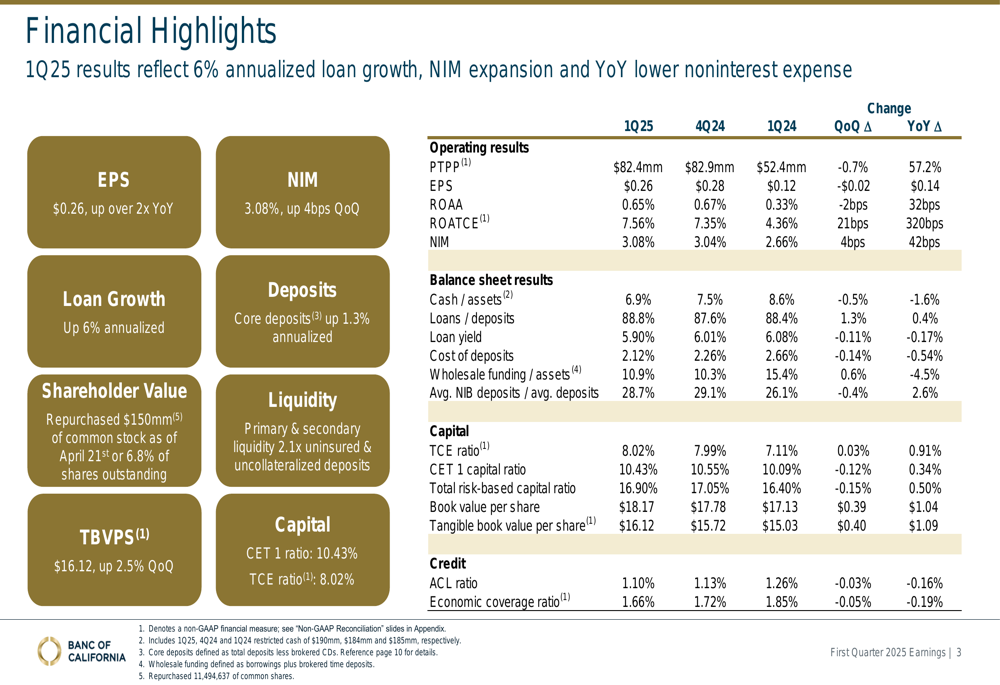

Banc of California reported earnings per share of $0.26 for Q1 2025, representing a more than twofold increase from $0.12 in Q1 2024, though slightly down from $0.28 in the previous quarter. The bank’s net interest margin expanded to 3.08%, up 4 basis points quarter-over-quarter and 42 basis points year-over-year, primarily driven by declining deposit costs.

As shown in the following financial highlights chart, the bank achieved 6% annualized loan growth while maintaining core deposit growth of 1.3% annualized. The bank also repurchased $150 million of common stock during the quarter, representing approximately 6.8% of shares outstanding, demonstrating confidence in its financial position and commitment to returning capital to shareholders.

Pre-tax, pre-provision income reached $82.4 million, representing a slight decrease of 0.7% from the previous quarter but a substantial 57.2% increase year-over-year. Return on average tangible common equity (ROATCE) improved to 7.56%, up 21 basis points quarter-over-quarter and 320 basis points year-over-year, reflecting enhanced profitability.

Net Interest Income and Margin

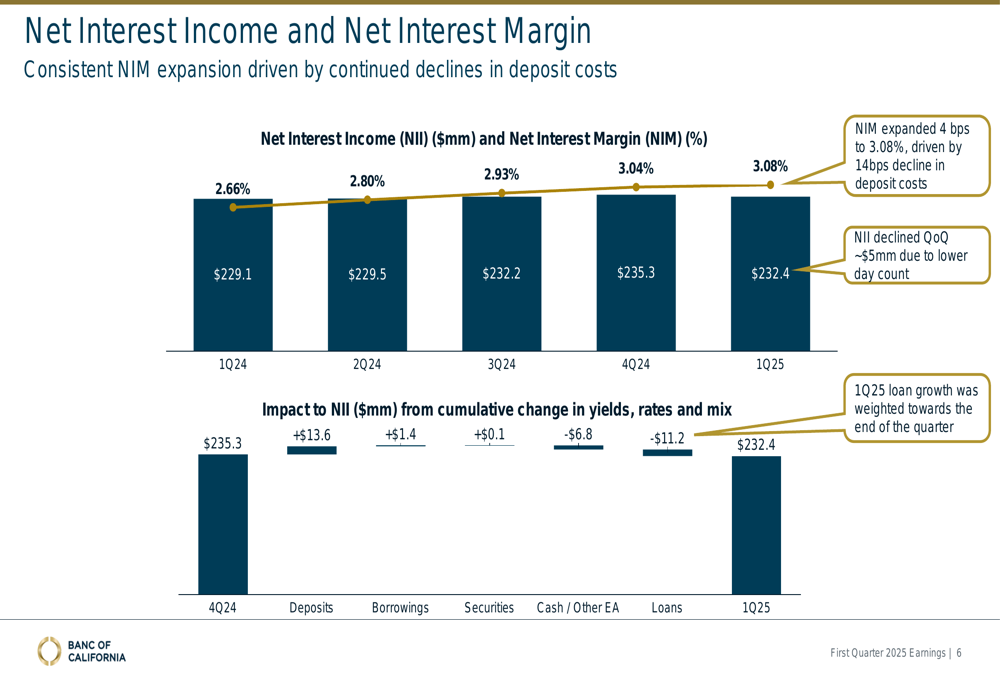

The bank’s net interest income for Q1 2025 was $232.4 million, slightly down from $235.3 million in the previous quarter but up from $229.1 million in Q1 2024. The sequential decline was primarily attributed to fewer days in the quarter, as the bank noted that loan growth was weighted toward the end of the period.

The following chart illustrates how Banc of California’s net interest margin expanded to 3.08% in Q1 2025, continuing a positive trend over the past year. This expansion was primarily driven by a 14 basis point decline in deposit costs, which more than offset the impact of lower loan yields.

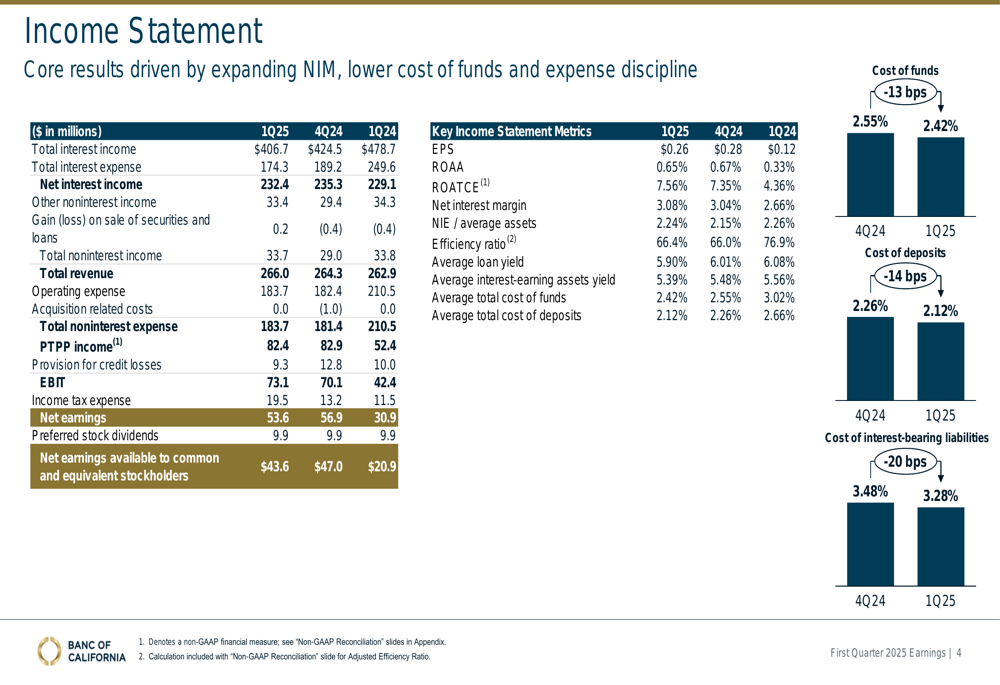

The bank’s income statement reveals total interest income of $406.7 million against interest expense of $174.3 million, resulting in net interest income of $232.4 million. Total (EPA:TTEF) revenue reached $266.0 million, with noninterest income contributing $33.7 million to the total.

Loan and Deposit Growth

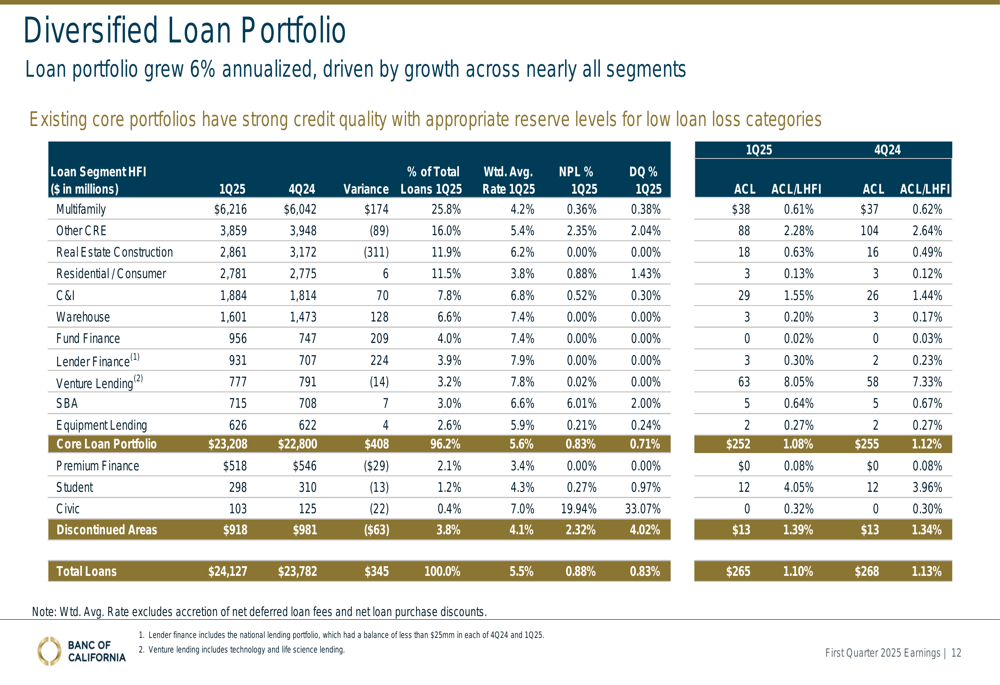

Banc of California’s loan portfolio grew by 6% on an annualized basis in Q1 2025, with the total loan balance reaching $24.1 billion. The growth was broad-based across nearly all segments, demonstrating the bank’s diversified lending approach.

The following chart provides a comprehensive breakdown of the bank’s loan portfolio, highlighting its diversification across multifamily, commercial real estate, construction, residential, and various specialty lending categories. Multifamily loans represent the largest segment at 25.8% of the total portfolio, followed by other commercial real estate at 16.0%.

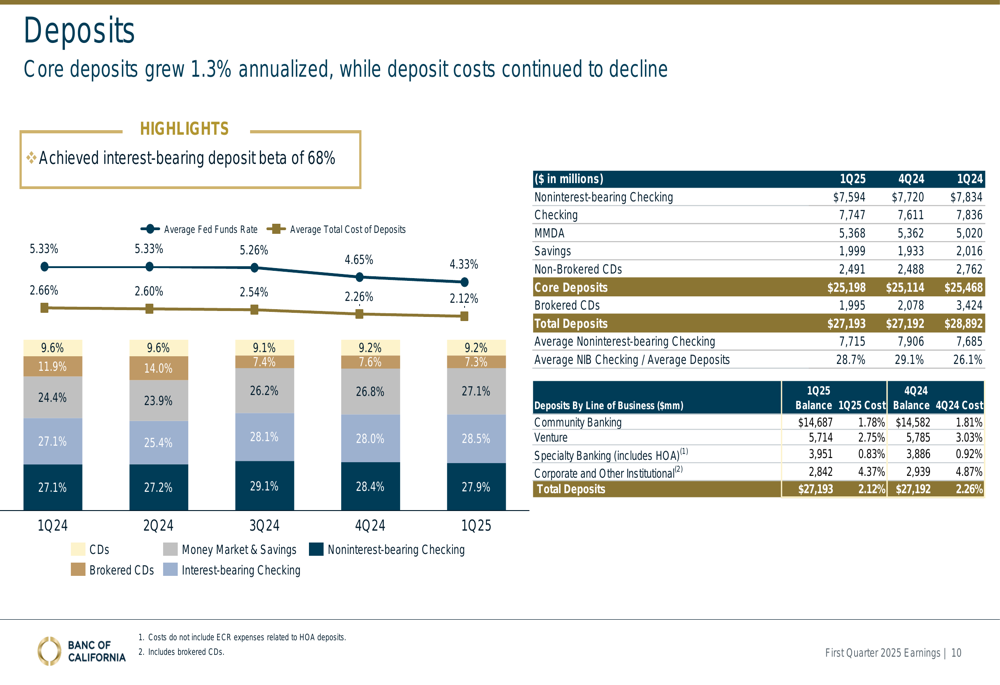

On the deposit front, core deposits grew by 1.3% annualized to $25.2 billion, while total deposits remained stable at $27.2 billion. The bank’s deposit composition shows a healthy mix of noninterest-bearing and interest-bearing accounts, with noninterest-bearing deposits representing 27.9% of total deposits.

The bank continues to prioritize growth in noninterest-bearing deposits, with cumulative new NIB business deposit accounts reaching 2,929 in Q1 2025, representing $537.8 million in balances. This focus on noninterest-bearing deposits is strategic in managing funding costs and improving net interest margin.

Capital and Credit Quality

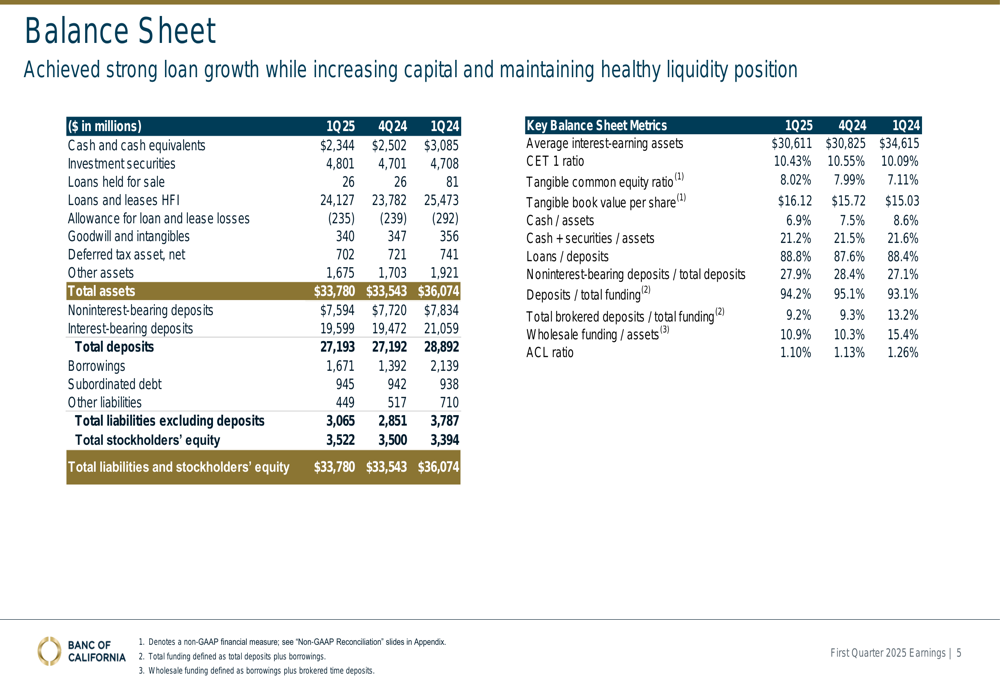

Banc of California maintained strong capital levels in Q1 2025, with a Common Equity Tier 1 (CET1) ratio of 10.43% and a tangible common equity ratio of 8.02%. The bank’s tangible book value per share increased to $16.12, up 2.5% from the previous quarter and 7.3% year-over-year.

The bank’s balance sheet shows total assets of $33.8 billion, with loans and leases held for investment of $24.1 billion and total deposits of $27.2 billion. The loan-to-deposit ratio stood at 88.8%, indicating a well-balanced funding profile.

Credit quality metrics remained stable, with the allowance for credit losses (ACL) ratio at 1.10%, down slightly from 1.13% in the previous quarter and 1.26% a year ago. The bank maintains a conservative outlook on credit quality given the uncertain economic environment, with total economic coverage ratio at 1.66%.

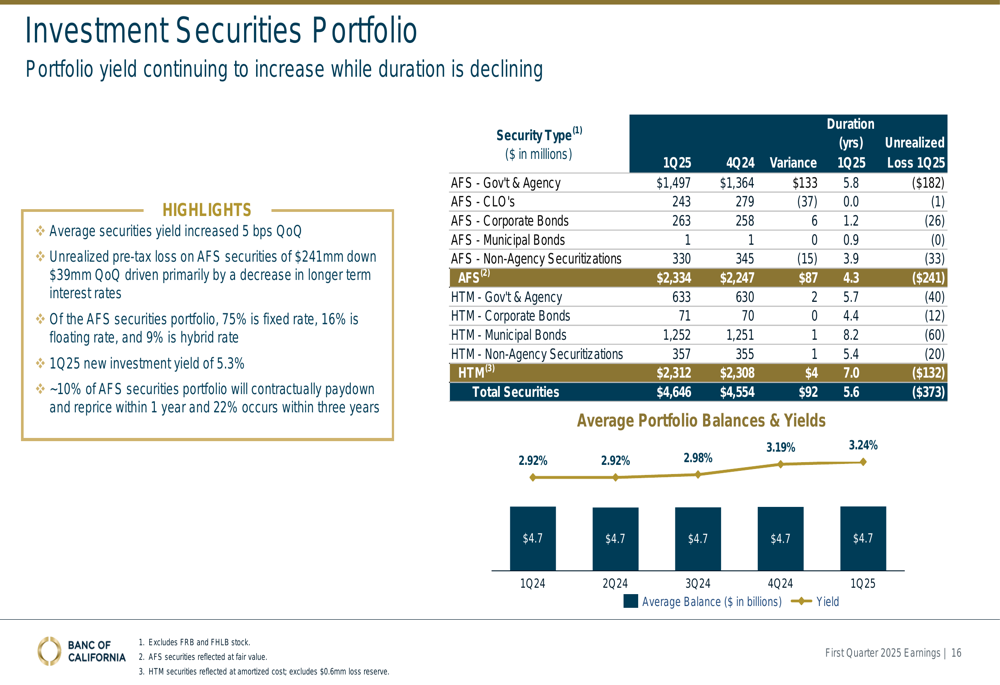

The investment securities portfolio yield continued to increase while duration declined, providing both income and flexibility. The portfolio totaled $4.6 billion with an average duration of 5.6 years and unrealized losses of $373 million.

Forward-Looking Statements

While maintaining a cautious outlook given the uncertain economic environment, Banc of California appears well-positioned for continued growth and profitability. The bank’s focus on expanding noninterest-bearing deposits, diversifying its loan portfolio, and maintaining strong capital levels provides a solid foundation for navigating changing market conditions.

The presentation highlights the bank’s continued emphasis on credit quality monitoring and conservative underwriting standards, particularly important given potential economic headwinds. With a well-diversified loan portfolio, declining deposit costs, and strong capital position, Banc of California demonstrates resilience and strategic focus as it moves through 2025.

The bank’s active capital management, including significant share repurchases, reflects confidence in its financial strength and commitment to enhancing shareholder value. As interest rates potentially decline further, the bank’s expanding net interest margin and growing noninterest-bearing deposit base should continue to support profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.