Gold soars to record high over $3,900/oz amid yen slump, US rate cut bets

Introduction & Market Context

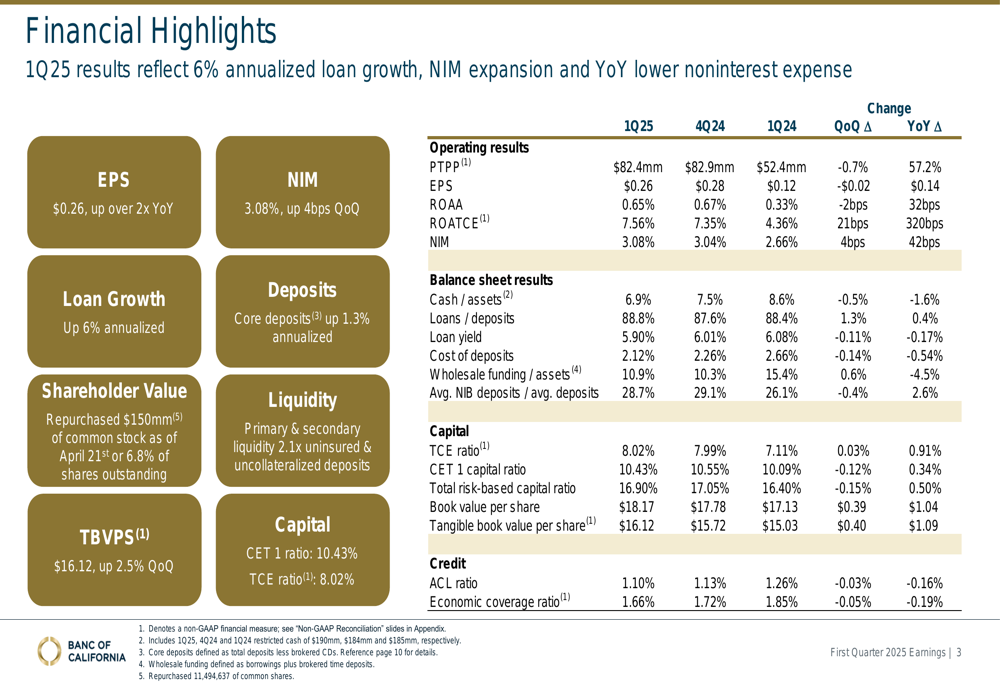

Banc of California (NYSE:BANC) released its first quarter 2025 financial results on April 24, showing continued margin expansion and solid loan growth despite a challenging interest rate environment. The bank reported earnings per share of $0.26, with pre-tax pre-provision income of $82.4 million.

The results follow a strong fourth quarter 2024 performance when the bank exceeded earnings expectations with an EPS of $0.28. Currently trading around $14 per share, BANC stock has shown resilience with a 24% return over the past year according to recent market data.

Quarterly Performance Highlights

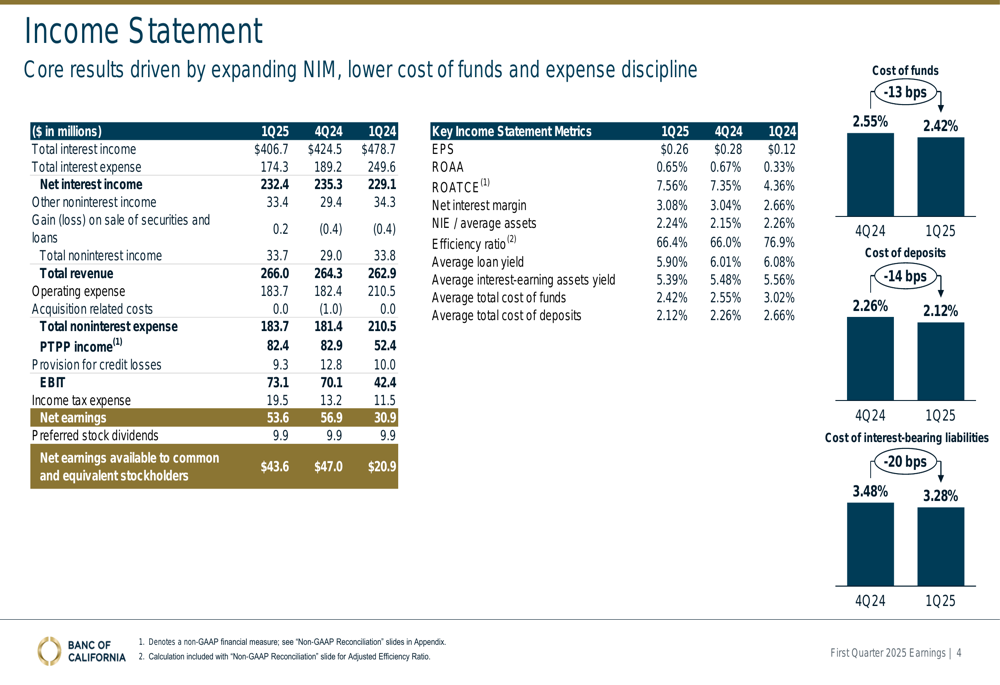

Banc of California reported first quarter EPS of $0.26, with return on average assets (ROAA) of 0.65% and return on average tangible common equity (ROATCE) of 7.56%. Total (EPA:TTEF) revenue reached $266 million, with net interest income of $232.4 million.

As shown in the following comprehensive financial highlights:

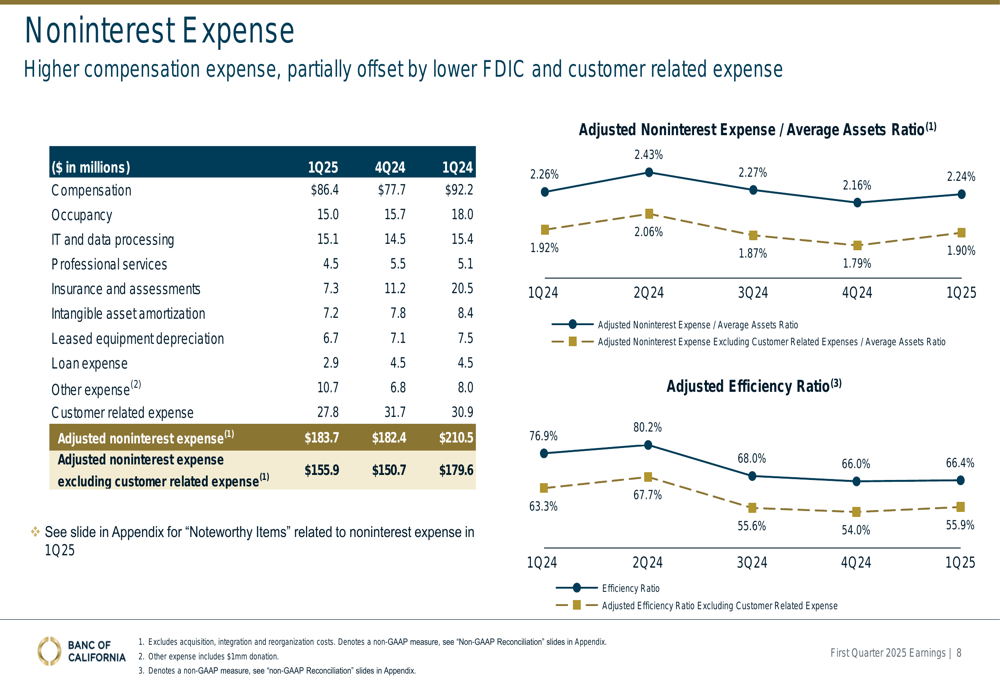

The efficiency ratio stood at 66.4%, showing the bank’s continued focus on operational efficiency. Total assets reached $33.78 billion, with loans representing $24.13 billion and deposits at $27.19 billion, resulting in a loans-to-deposits ratio of 88.8%.

The detailed income statement reveals operating expenses of $183.7 million and a provision for credit losses of $9.3 million:

Net Interest Income and Margin Analysis

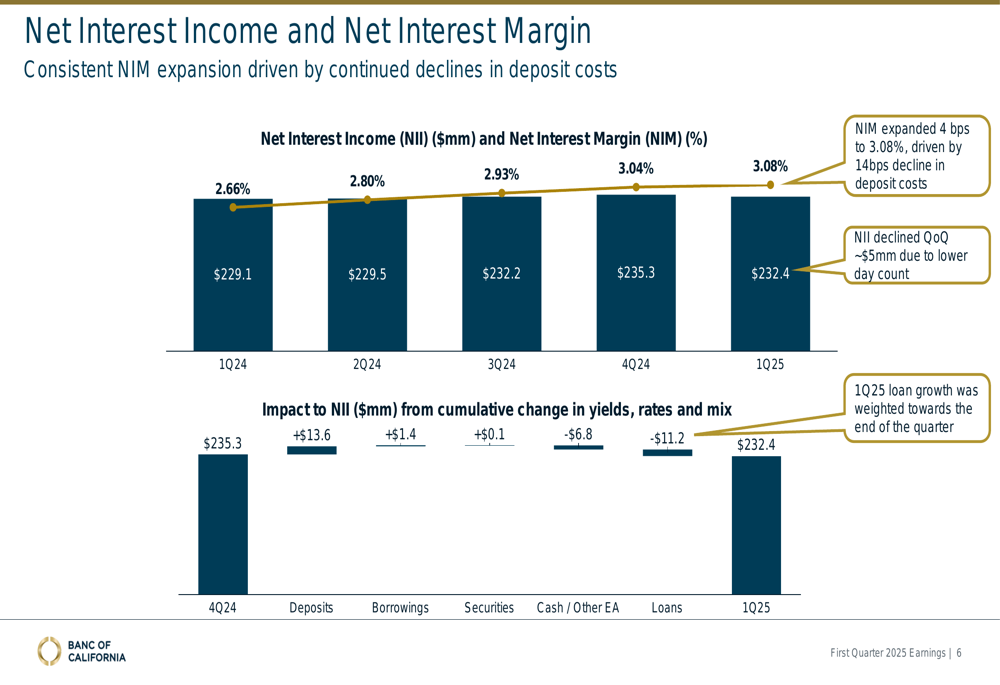

A key highlight of the quarter was the continued expansion of net interest margin (NIM), which increased to 3.08%, up 4 basis points from the previous quarter. This improvement was primarily driven by a 14 basis point decline in deposit costs, which fell to 2.12%.

The following chart illustrates the consistent NIM expansion trend from 2.66% in Q1 2024 to the current 3.08%:

Net interest income (NII) declined slightly quarter-over-quarter by approximately $5 million to $232.4 million, which the bank attributed to fewer days in the quarter. Additionally, loan growth was weighted toward the end of the quarter, limiting its contribution to interest income during the period.

Loan and Deposit Trends

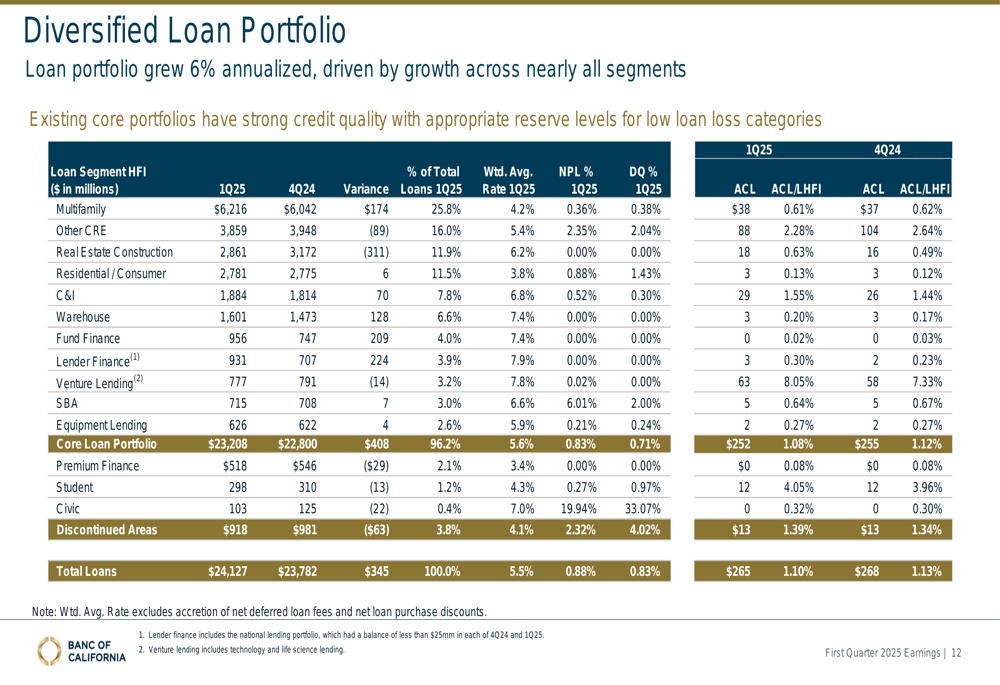

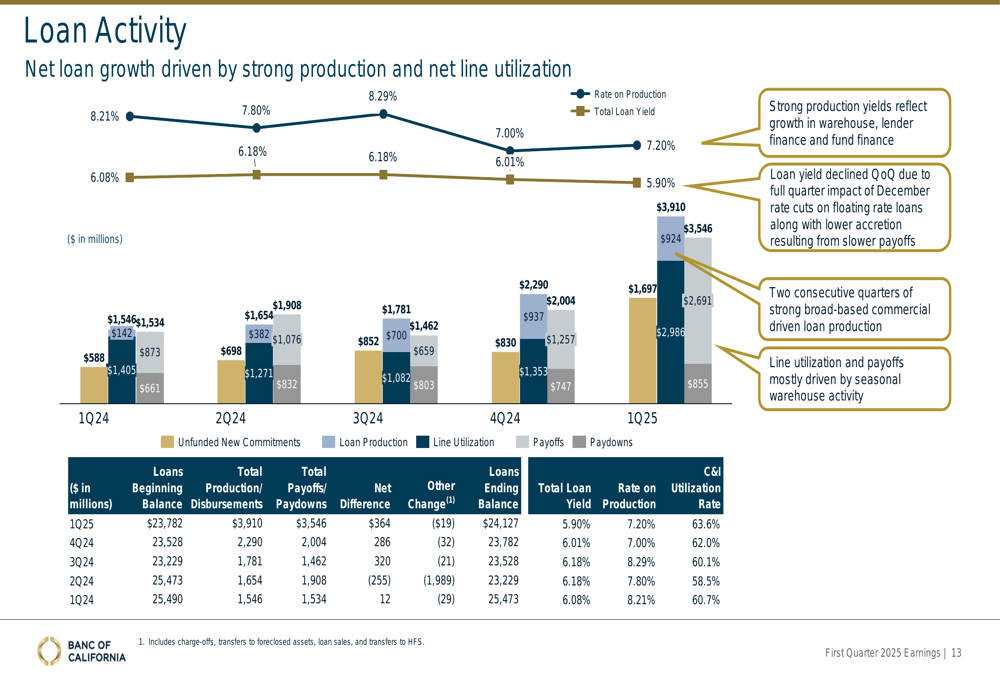

The bank’s loan portfolio grew at an annualized rate of 6%, with growth across nearly all segments. Total loans held for investment reached $24.13 billion, up from $23.78 billion in the previous quarter. The diversified portfolio maintains strong credit quality with an allowance for credit losses (ACL) ratio of 1.10%.

The following breakdown shows the bank’s diversified loan portfolio composition:

Loan production remained robust at $3.91 billion for the quarter, with new originations coming on at an average rate of 7.20%, significantly above the total loan portfolio yield of 5.90%. This positive differential supports future margin expansion as illustrated below:

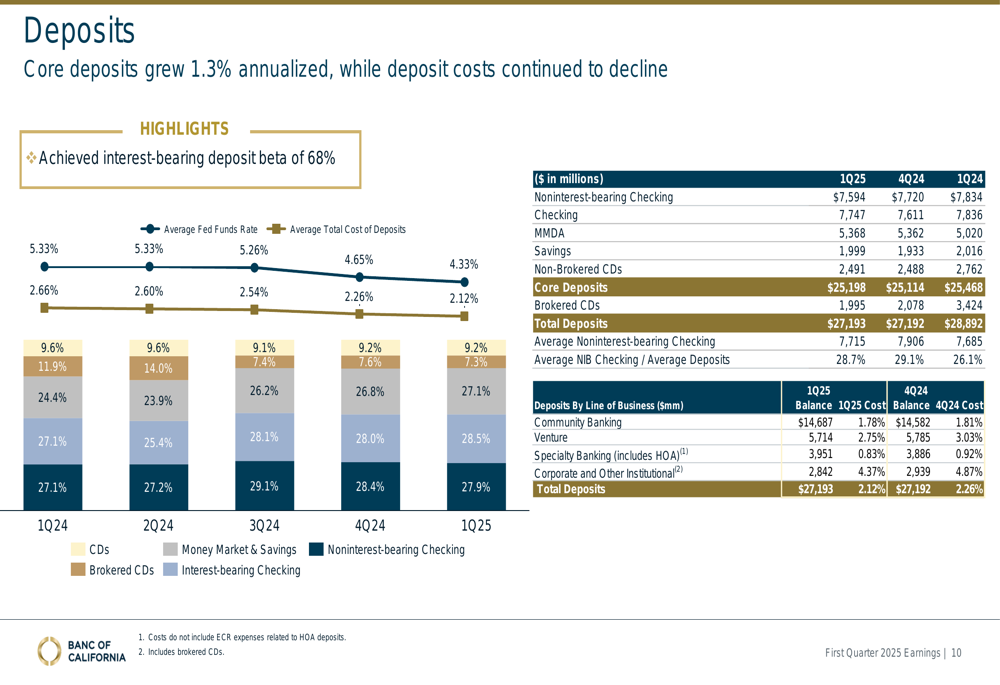

On the funding side, core deposits grew at a 1.3% annualized rate, reaching $25.2 billion. The bank maintained a favorable deposit mix with noninterest-bearing deposits representing 27.9% of total deposits. Importantly, Banc of California achieved an interest-bearing deposit beta of 68%, indicating effective deposit pricing management in a competitive environment.

The deposit composition and trends are detailed in the following slide:

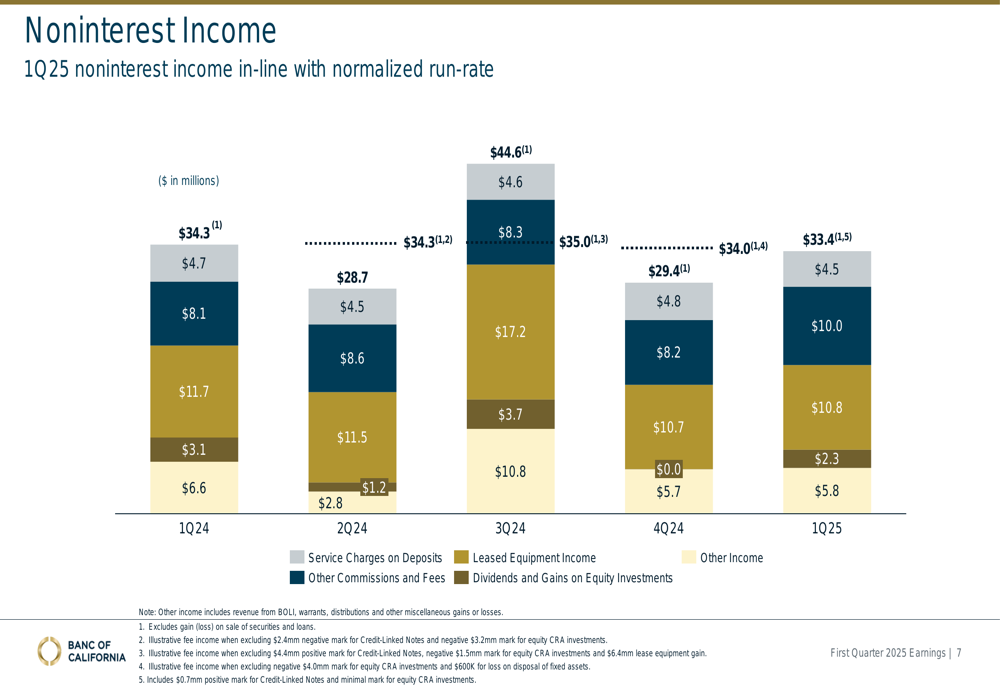

Noninterest income remained stable at $33.4 million, in line with normalized run-rates from previous quarters:

Capital Position and Outlook

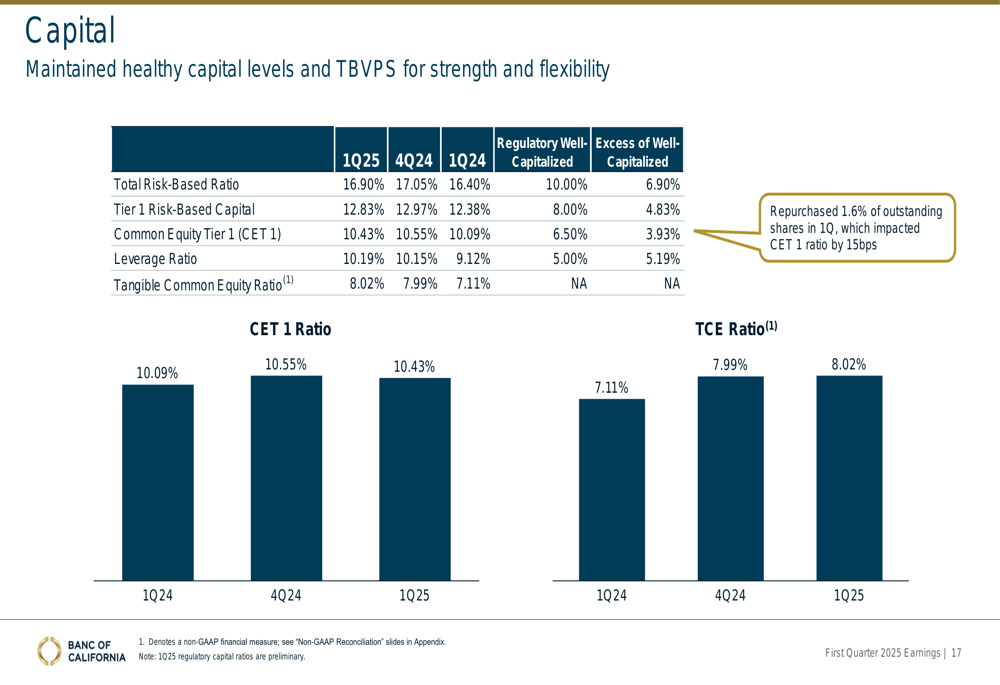

Banc of California maintained healthy capital levels, with a Common Equity Tier 1 (CET1) ratio of 10.43% and a total risk-based capital ratio of 16.90%, both well above regulatory requirements. The tangible common equity ratio stood at 8.02%, providing the bank with financial flexibility.

During the quarter, the bank repurchased 1.6% of its outstanding shares, which impacted the CET1 ratio by approximately 15 basis points, demonstrating its commitment to returning capital to shareholders while maintaining strong capital levels.

Noninterest expenses were well-controlled at $183.7 million, with higher compensation expenses partially offset by lower FDIC and customer-related expenses. The bank noted that customer-related expenses, particularly earnings credit rate (ECR) expenses, declined due to Federal Reserve rate cuts.

Looking ahead, Banc of California appears well-positioned to benefit from any further interest rate cuts, which would reduce deposit costs and potentially expand margins further. The bank’s diversified loan portfolio and strong capital position provide a solid foundation for continued growth in the California market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.