US LNG exports surge but will buyers in China turn up?

Bankwell Financial Group (NASDAQ:BWFG) revealed strong second-quarter results in its investor presentation dated July 28, 2025, highlighting significant earnings growth, margin expansion, and progress on strategic initiatives to enhance deposit gathering capabilities.

Quarterly Performance Highlights

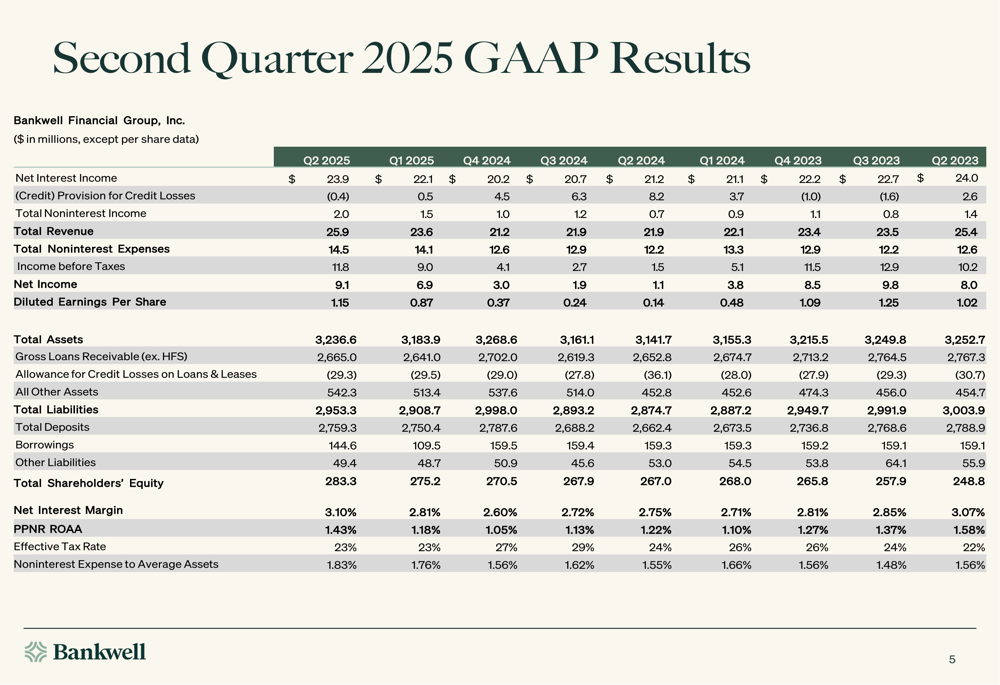

Bankwell reported fully diluted earnings per share of $1.15 for Q2 2025, representing a 32% increase from the previous quarter’s $0.87. This impressive growth was primarily driven by an expanding net interest margin and increased non-interest income.

The company achieved a return on average assets of 1.14%, improving by 28 basis points compared to the first quarter. Net interest margin expanded to 3.10%, up 29 basis points from Q1’s 2.81%, reflecting the company’s improved funding profile and strategic deposit initiatives.

As shown in the following comprehensive financial summary:

Non-interest income grew by $0.5 million or 34% quarter-over-quarter, reaching $2.0 million, largely due to $1.1 million in gains realized from SBA (LON:SBA) loan sales. This diversification of revenue streams represents an important strategic focus for the bank.

Pre-provision net revenue (PPNR) reached $11.4 million, or $1.46 per share, marking a 21% increase from the previous quarter. The bank also reported a provision release of $0.4 million, with zero basis points of net charge-offs, indicating strong credit quality.

Deposit Strategy and Margin Improvement

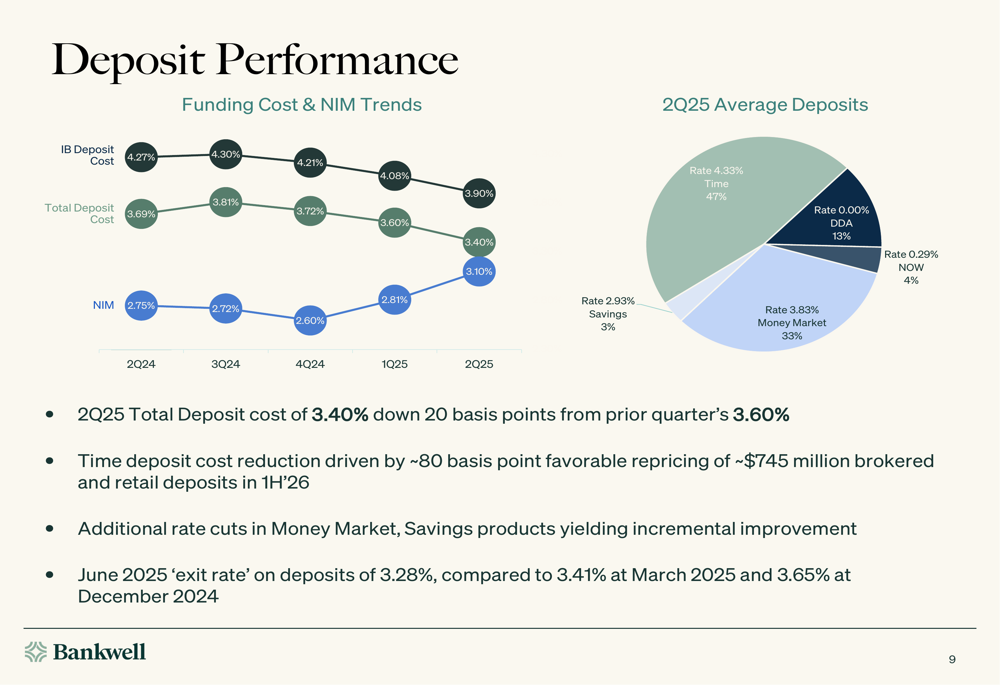

A key driver of Bankwell’s improved performance has been its strategic focus on deposit gathering and cost reduction. The bank added four deposit-focused teams in the NYC metro area during the quarter, with an additional team joining in July 2025.

The following chart illustrates the positive trends in deposit costs and net interest margin:

Total (EPA:TTEF) deposit costs decreased to 3.40% in Q2, down 20 basis points from 3.60% in the previous quarter. The June 2025 "exit rate" on deposits was 3.28%, suggesting further improvement in the third quarter. This reduction was achieved through approximately 80 basis points of favorable repricing on roughly $745 million in brokered and retail deposits during the first half of 2025.

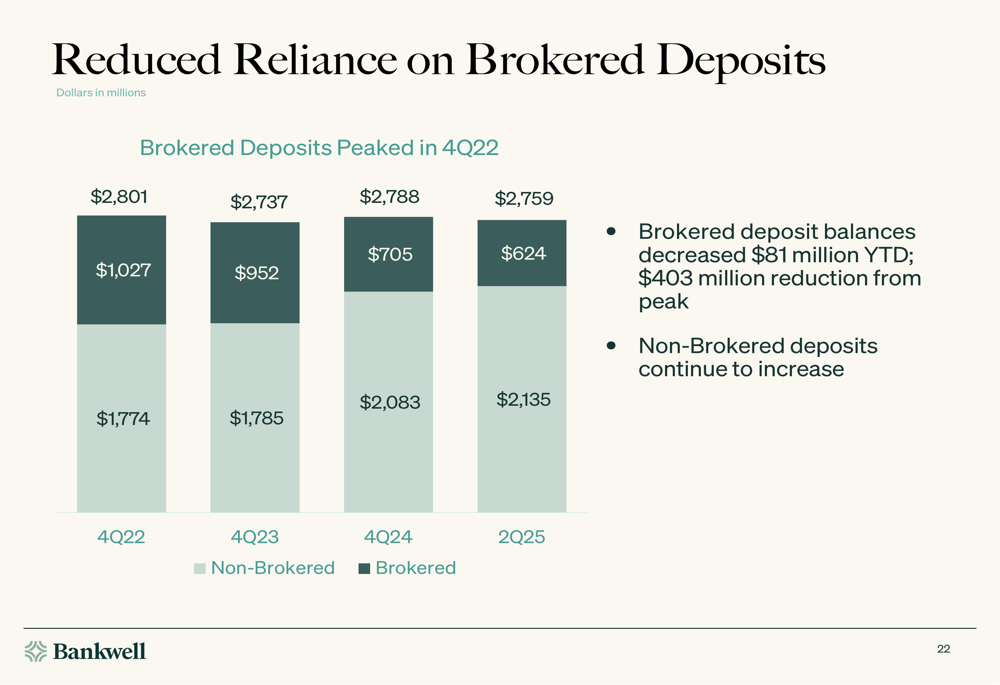

The company has also made significant progress in reducing its reliance on brokered deposits, as shown in the following chart:

Brokered deposit balances decreased by $81 million year-to-date, representing a $403 million reduction from their peak. Meanwhile, non-interest bearing deposits grew by $48 million during the quarter, contributing to a more favorable funding mix.

Balance Sheet Strength and Credit Quality

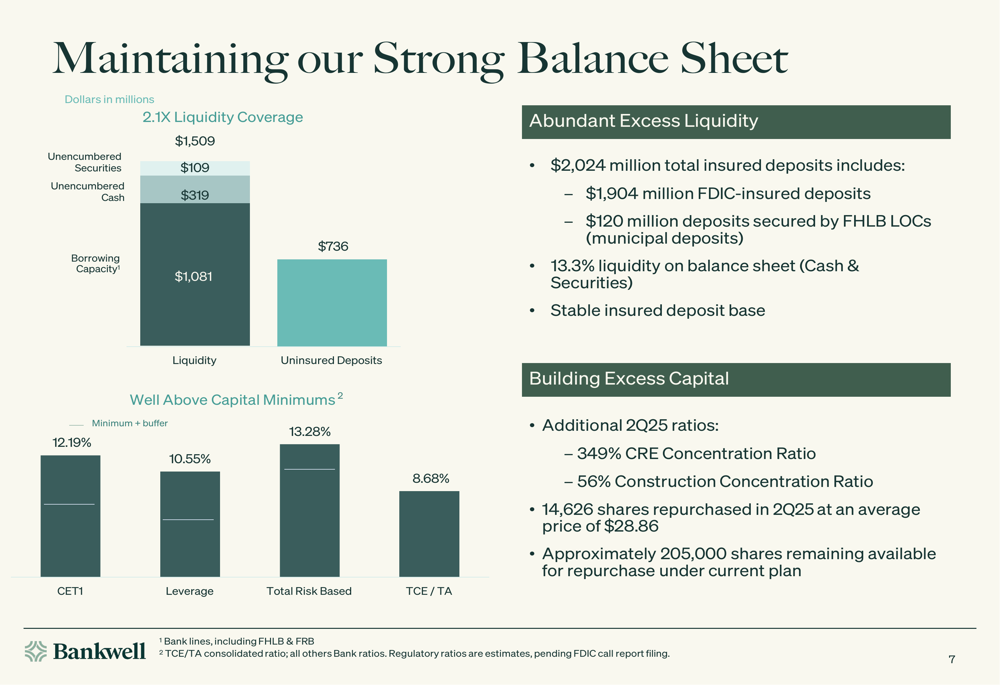

Bankwell maintained a strong balance sheet with ample liquidity and solid capital ratios. The bank reported a liquidity coverage ratio of 2.1x, with $1,509 million in unencumbered securities and $109 million in unencumbered cash.

The following slide details the bank’s strong balance sheet position:

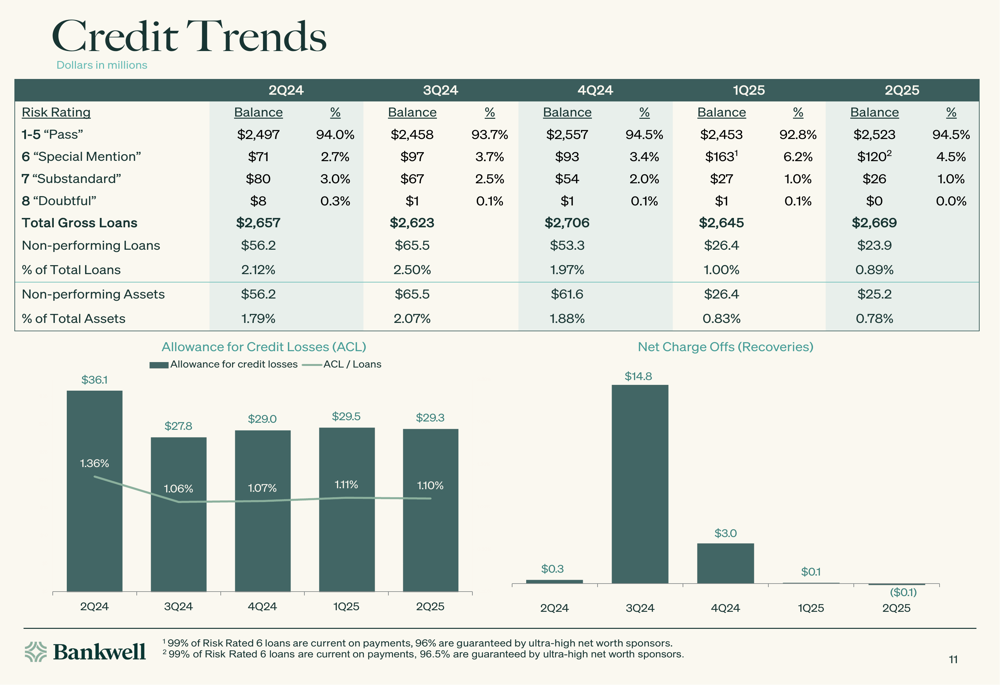

The bank’s loan portfolio showed modest growth, with balances increasing by $24 million during the quarter on $170 million of funded originations. Credit quality improved, with non-performing assets decreasing to 0.78% of total assets.

The composition and trends of the bank’s credit quality are illustrated in the following chart:

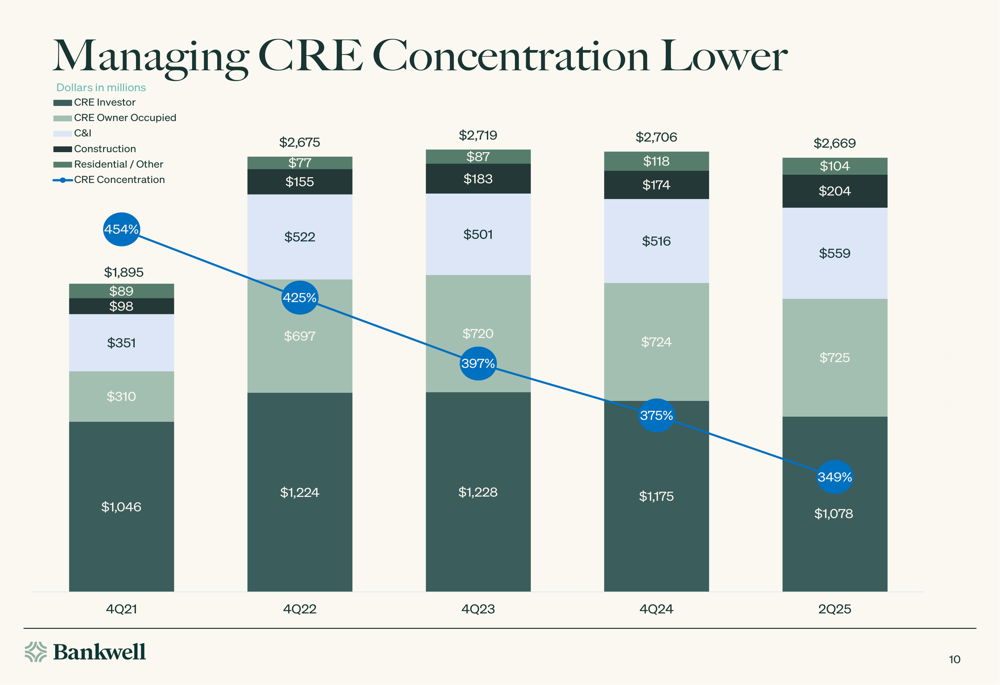

Bankwell has also made progress in managing its commercial real estate (CRE) concentration, reducing it from 454% in Q4 2021 to 349% in Q2 2025:

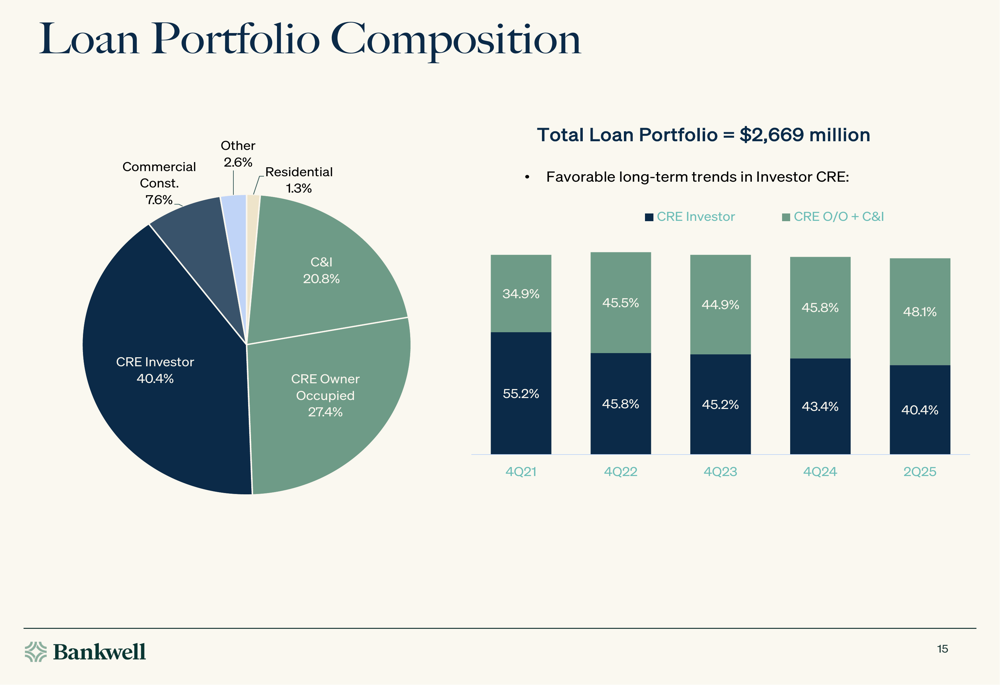

The loan portfolio remains well-diversified, with CRE investor loans representing 40.4%, CRE owner-occupied at 27.4%, and C&I loans at 20.8% of the total portfolio:

Positioning for Lower Interest Rates

Bankwell appears well-positioned for a potential lower interest rate environment. The bank has $665 million in time deposits maturing during the remainder of 2025 at a weighted average rate of 4.41%, creating opportunities for cost savings.

Based on current rates, the company expects approximately $1.2 million in annualized interest expense savings from these maturing deposits, which would translate to approximately $0.12 in EPS benefit and about 4 basis points of incremental net interest margin expansion, assuming stable asset yields.

Forward-Looking Statements

Looking ahead, Bankwell’s management outlined expectations for modest loan growth, continued NIM expansion, stable credit quality, and ongoing capital growth. The bank’s tangible book value reached $35.65 per share, increasing by $1.09 from the previous quarter and $2.04 from the prior year.

The company repurchased 14,626 shares during the quarter at an average price of $28.86, with approximately 205,000 shares remaining available under the current repurchase plan. This reflects management’s confidence in the bank’s financial position and future prospects.

Since reporting Q1 2025 results, Bankwell’s stock has appreciated by approximately 17.7%, closing at $37.39 in the most recent trading session, reflecting investor confidence in the bank’s strategic direction and financial performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.