US stock futures inch lower after Wall St marks fresh records on tech gains

BBVA Argentina (NYSE:BBAR) presented its second quarter 2025 results on August 21, showing a significant decline in profitability metrics despite continued growth in loans and deposits. The bank’s shares were down 3.62% in premarket trading following the release.

Quarterly Performance Highlights

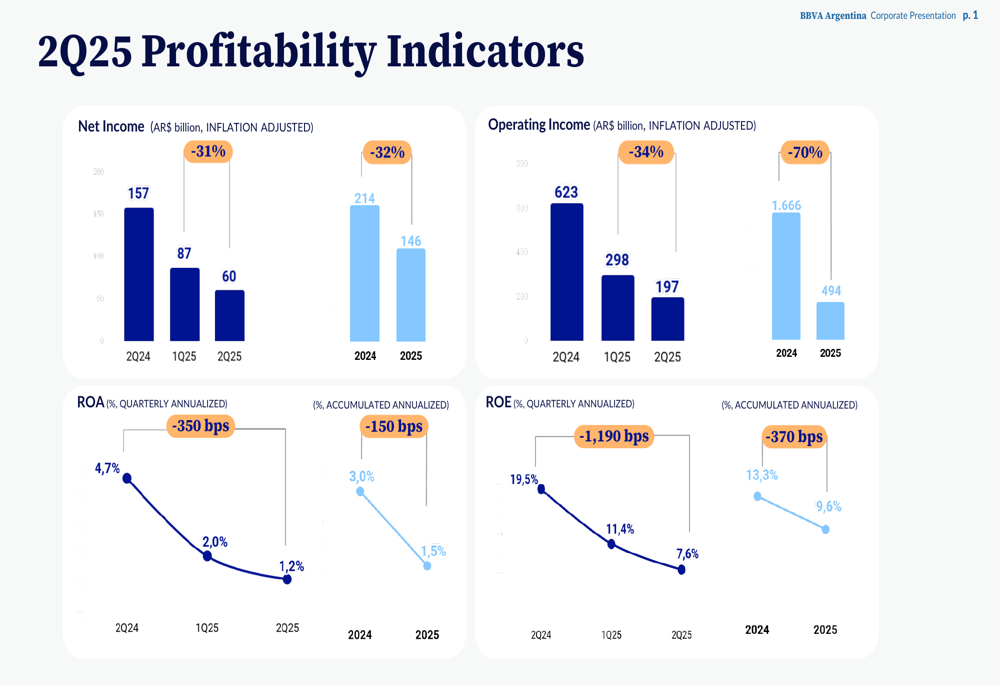

BBVA Argentina reported a sharp decline in key profitability indicators for Q2 2025. Net income decreased by 31% quarter-over-quarter to AR$60 billion, down from AR$87 billion in Q1 2025 and representing a 62% year-over-year decline from AR$157 billion in Q2 2024.

The bank’s operating income also fell by 34% to AR$197 billion compared to Q2 2024. Return on assets (ROA) decreased by 80 basis points quarter-over-quarter to 1.2%, while return on equity (ROE) dropped by 380 basis points to 7.6%.

As shown in the following chart of BBVA Argentina’s key profitability metrics:

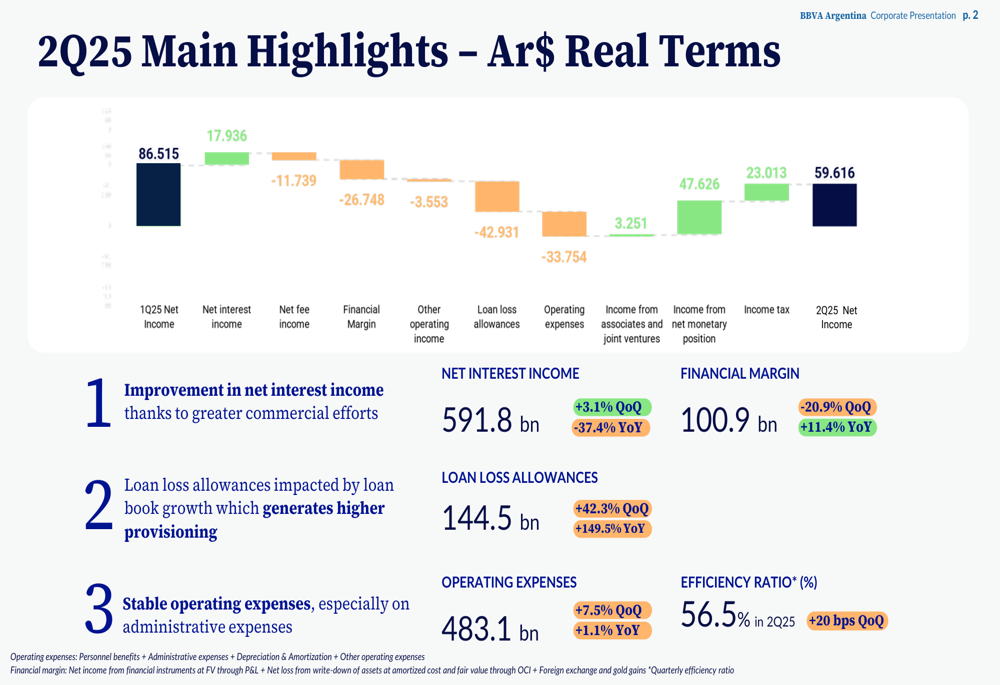

The decline in net income was driven by several factors, including a 20.9% quarter-over-quarter decrease in financial margin to AR$100.9 billion and a significant 42.3% increase in loan loss allowances to AR$144.5 billion. Operating expenses rose by 7.5% quarter-over-quarter to AR$483.1 billion.

This represents a notable reversal from Q1 2025, when the bank reported a 16.2% increase in net income and improved efficiency.

The following waterfall chart illustrates the main factors affecting the sequential change in net income:

Loan Portfolio and Asset Quality

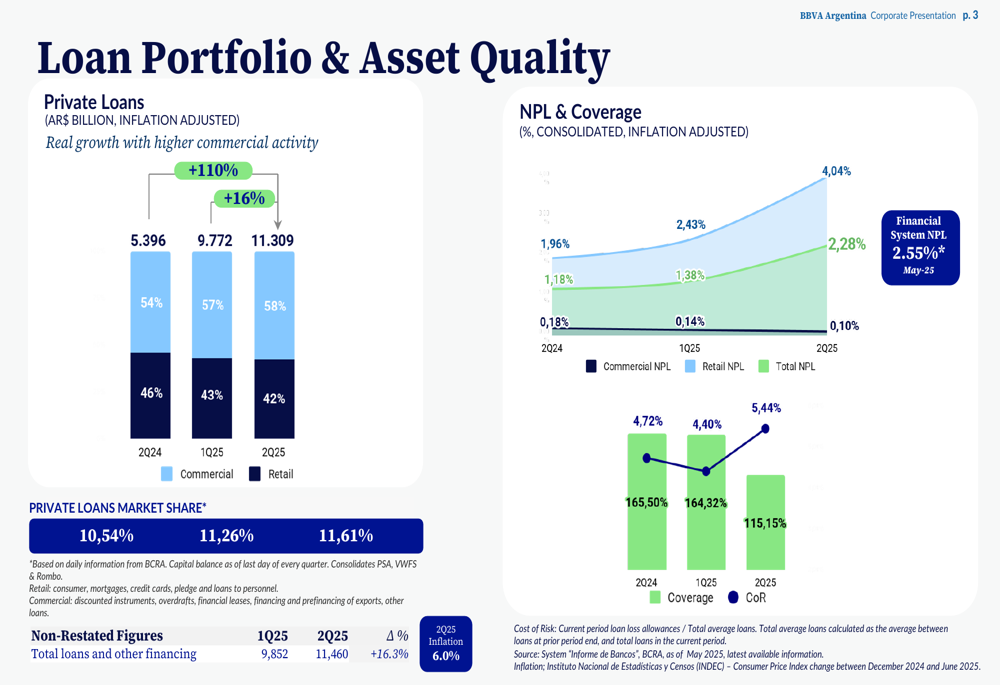

Despite the profitability challenges, BBVA Argentina continued to expand its loan portfolio and market share. Private loans increased to AR$11.31 billion in Q2 2025, up from AR$9.77 billion in Q1 2025, representing real growth of 16.3% when adjusted for the quarter’s 6.0% inflation.

The bank’s market share in private loans also improved to 11.61% in Q2 2025, up from 11.26% in Q1 2025 and 10.54% in Q2 2024. The loan portfolio maintained a balanced mix of 58% commercial and 42% retail loans.

However, asset quality metrics showed signs of deterioration, with rising non-performing loan ratios and decreasing coverage ratios, as illustrated in the following chart:

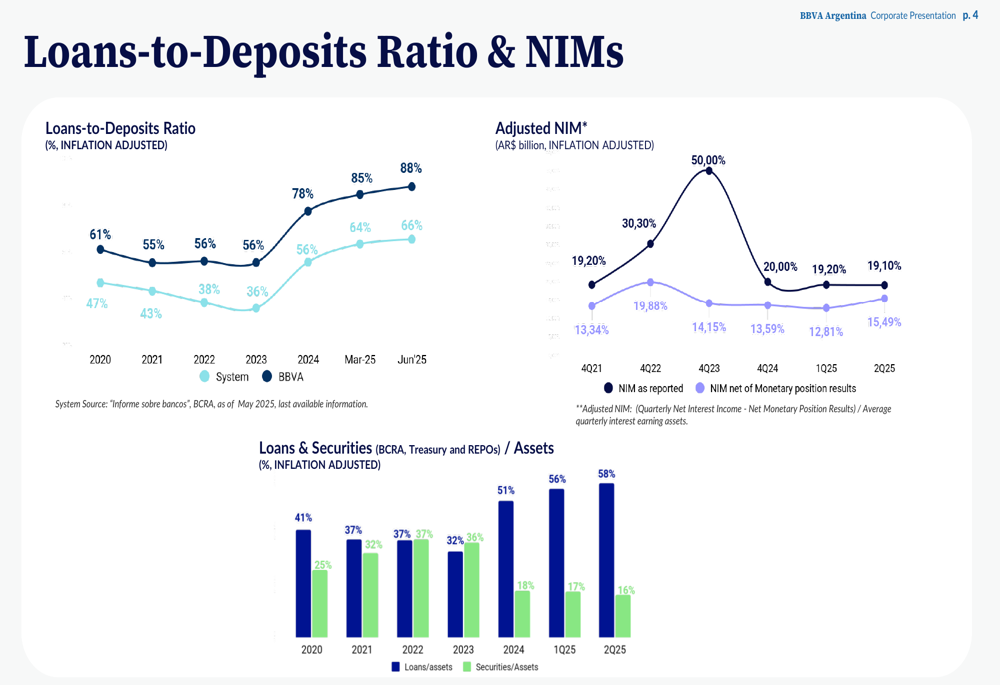

The bank’s loans-to-deposits ratio remained significantly lower than the financial system average, providing BBVA Argentina with additional capacity for loan growth. While the system average approached 88%, BBVA (BME:BBVA)’s ratio remained between 43% and 56%.

The following chart shows the loans-to-deposits ratio and net interest margin trends:

Funding and Capital Position

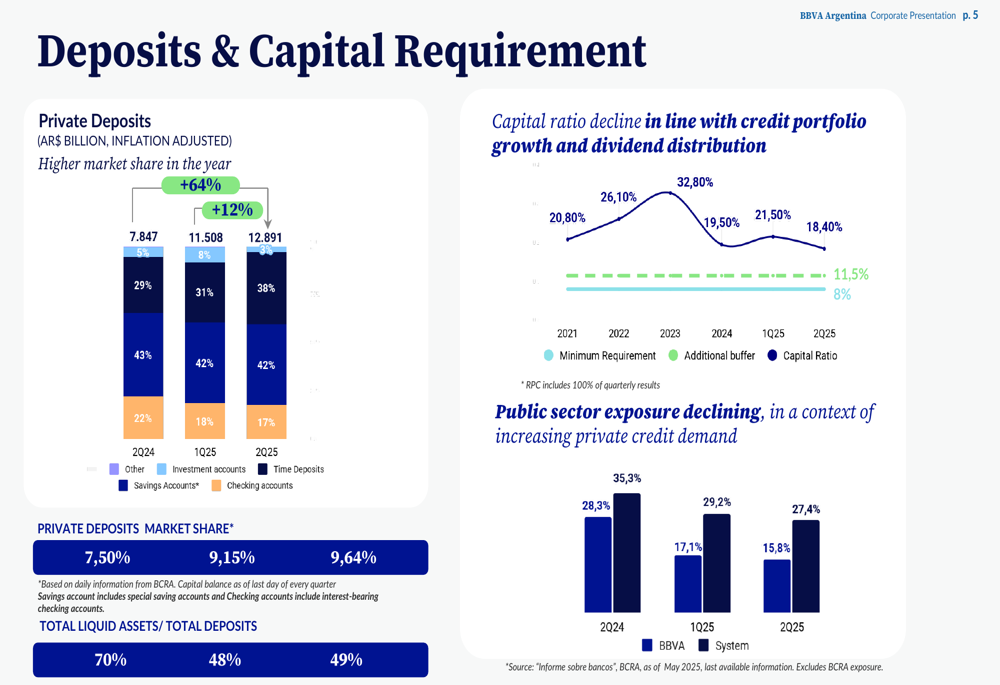

BBVA Argentina’s private deposits grew to AR$12.89 billion in Q2 2025, up from AR$11.51 billion in Q1 2025. The deposit mix remained diversified with 42% in savings accounts, 38% in investment accounts, 17% in checking accounts, and 8% in other deposit types.

However, the bank’s capital ratio declined to 18.40% in Q2 2025, continuing a downward trend that bears monitoring. Public sector exposure decreased to 15.8% of the portfolio, reflecting the bank’s strategic shift toward private credit demand.

The following chart shows the deposit growth and composition:

Digital Transformation Progress

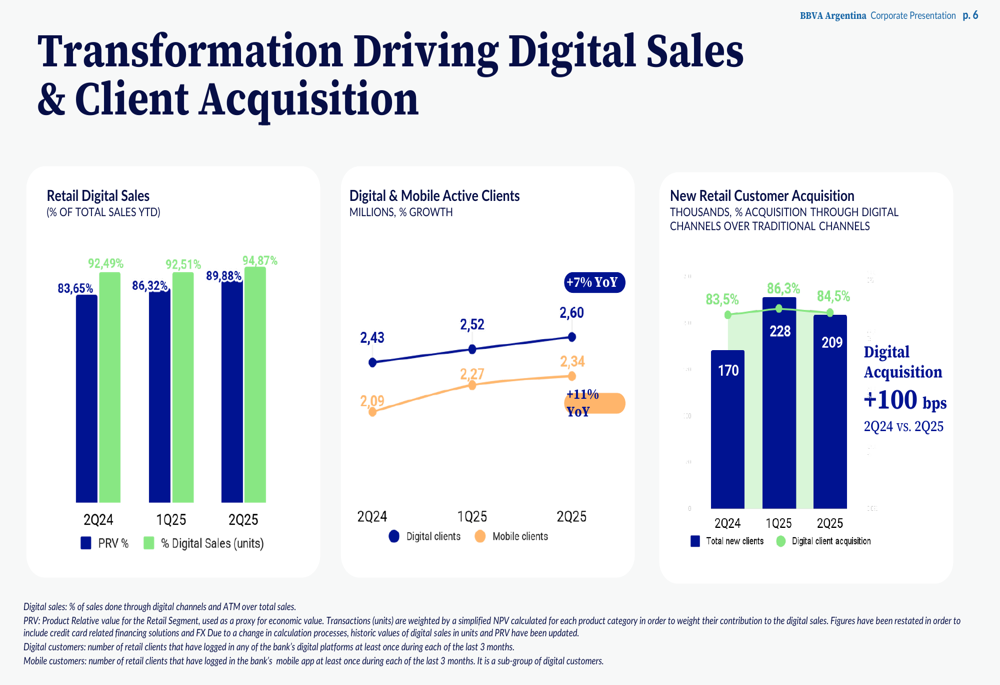

BBVA Argentina continued to make significant progress in its digital transformation initiatives. Retail digital sales increased to 89.88% in Q2 2025, up from 86.32% in Q1 2025 and 83.65% in 2024, demonstrating the bank’s successful execution of its digitalization strategy.

The bank reported 2.60 million digital clients in Q2 2025, with new retail customer acquisition increasing from 170,000 in Q2 2024 to 209,000 in Q2 2025. Digital acquisition also improved by 100 basis points year-over-year.

As illustrated in the following chart of digital sales and client acquisition metrics:

Forward-Looking Statements

While BBVA Argentina continues to grow its loan portfolio and market share, the significant decline in profitability metrics suggests challenges ahead. The substantial increase in loan loss allowances (+42.3% quarter-over-quarter) may indicate concerns about future credit quality, particularly as the loan book expands.

The bank’s efficiency ratio of 56.5% in Q2 2025 represented a slight deterioration from the 56.3% reported in Q1 2025, suggesting that cost control measures may be needed to address rising operating expenses.

BBVA Argentina’s continued focus on digital transformation appears to be yielding positive results in terms of customer acquisition and digital sales, which may help the bank maintain its competitive position despite the current profitability challenges.

Investors will likely be watching closely to see if the bank can reverse the declining profitability trend while maintaining its loan growth and market share gains in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.