Asia FX moves little with focus on US-China trade, dollar steadies ahead of CPI

Introduction & Market Context

Belden Inc (NYSE:BDC) released its second quarter 2025 earnings presentation on July 31, 2025, revealing strong financial performance that exceeded guidance across key metrics. The company’s stock traded up 1.17% in premarket activity at $129.54, approaching its 52-week high of $132.99, as investors responded positively to the results.

The industrial networking and connectivity solutions provider continues to benefit from secular growth trends including reshoring, Industry 4.0, digital transformation, and AI expansion. These tailwinds have supported Belden’s performance across both of its business segments.

Quarterly Performance Highlights

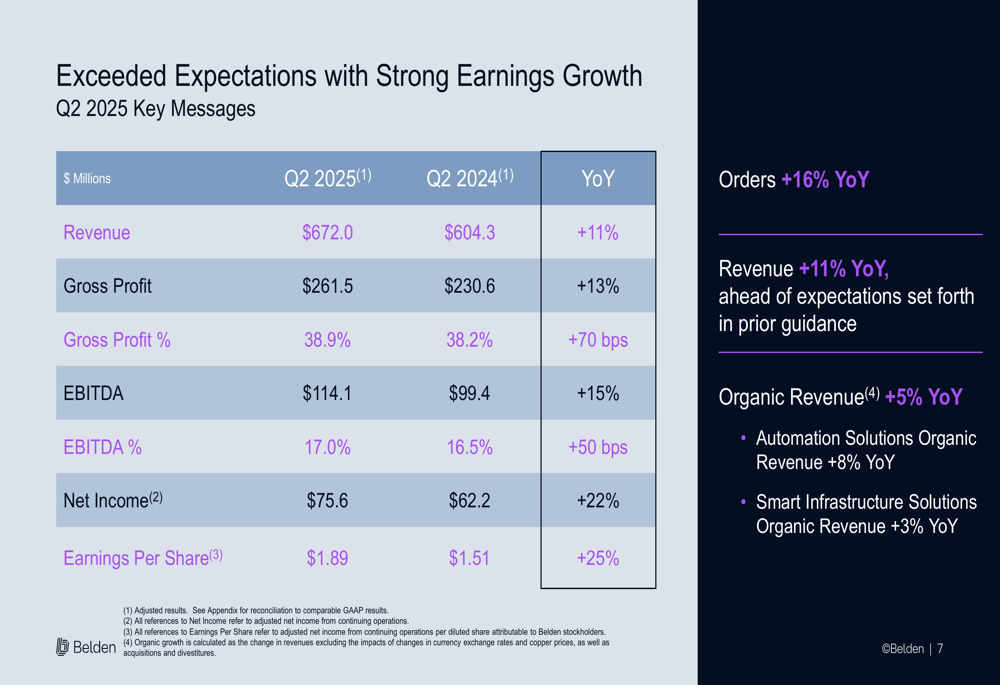

Belden reported Q2 2025 revenue of $672 million, exceeding the high end of its guidance and representing an 11% year-over-year increase. Adjusted earnings per share reached $1.89, growing 25% compared to the same period last year and surpassing analyst expectations.

The company demonstrated solid operational execution with adjusted EBITDA margin expanding to 17.0%, a 50 basis point improvement year-over-year. Adjusted gross margin also improved, reaching 38.9%, up 70 basis points from Q2 2024.

As shown in the following chart of quarterly financial performance:

Order momentum remained strong with a 16% year-over-year increase and a book-to-bill ratio of 1.05, indicating continued demand strength. This follows the 18% order growth reported in Q1 2025, suggesting sustained business momentum through the first half of the year.

Organic revenue growth reached 5% overall, with the Automation Solutions segment leading at 8% organic growth, while Smart Infrastructure Solutions delivered 3% organic growth.

Segment Performance Analysis

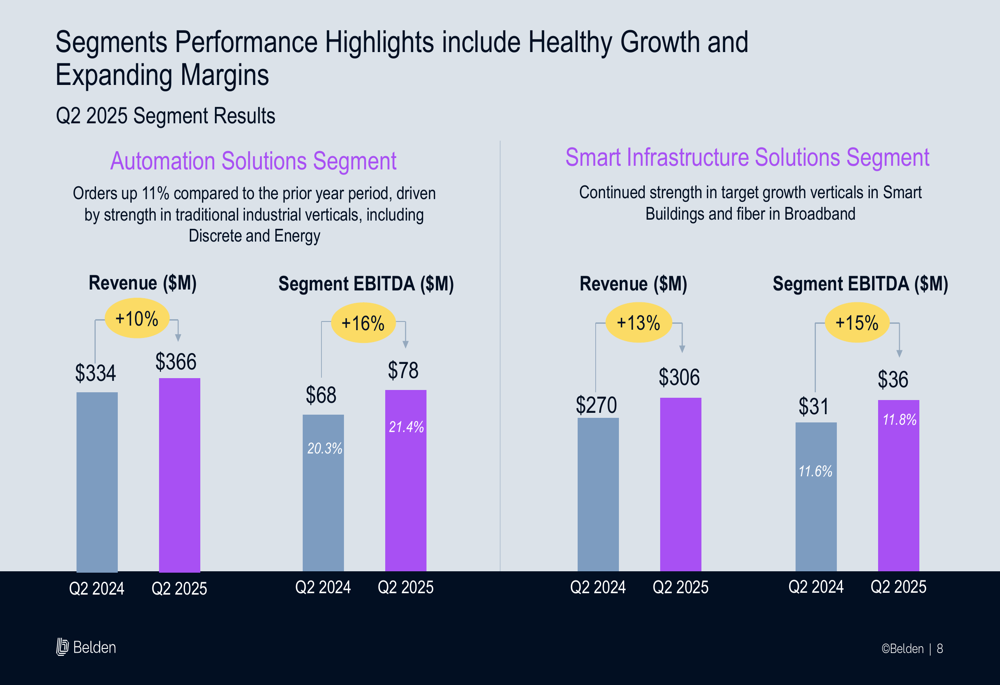

Both of Belden’s business segments delivered strong results in the quarter. The Automation Solutions segment, which focuses on industrial networking and connectivity solutions, posted revenue of $366 million, up 9.6% year-over-year. More impressively, segment EBITDA grew 14.7% to $78 million, with EBITDA margin expanding 110 basis points to 21.4%.

The Smart Infrastructure Solutions segment, which provides network infrastructure and broadband solutions, generated revenue of $306 million, representing a 13.3% increase from Q2 2024. Segment EBITDA rose 16.1% to $36 million, with EBITDA margin improving 20 basis points to 11.8%.

The following chart illustrates the performance of both segments:

Strategic Customer Wins

Belden highlighted two significant customer wins that demonstrate its solutions-based approach is gaining traction in key markets.

The company secured a multi-site solutions award with a Hyperscale Data Center customer for its "Gray Space" solutions. This collaboration involves working with a hyperscaler, OEM, and systems integrator to ensure uptime for advanced data centers by supporting modular cooling systems with a low-latency, high-availability network built on Belden’s industrial switches.

Additionally, Belden announced a major specification position award from a US automotive manufacturer. This global specification award represents approximately $40 million over three years as a single-source supplier, with potential for extension. The deal specifies Belden’s advanced connectivity products for assembly line and related factory equipment, creating expansion opportunities.

Financial Position and Capital Allocation

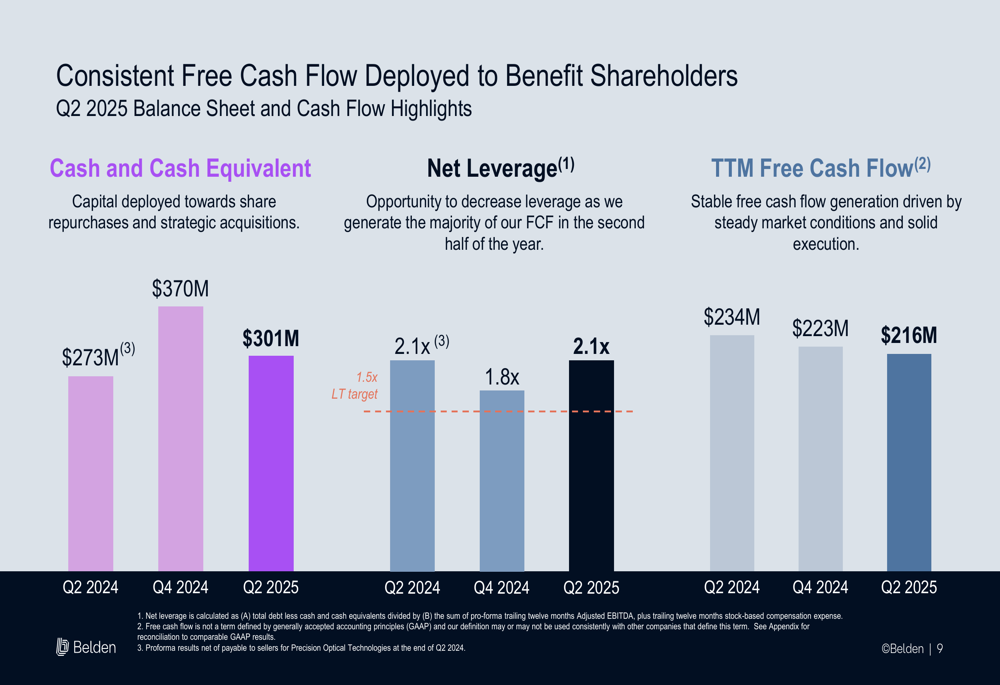

Belden maintained a strong financial position with $301 million in cash and cash equivalents as of Q2 2025, though this represents a decrease from $370 million at the end of 2024. The company’s net leverage ratio stood at 2.1x, above its long-term target of 1.5x.

Free cash flow generation remained robust at $216 million on a trailing twelve-month basis, supporting the company’s capital allocation priorities. Belden repurchased 1.0 million shares for $100 million year-to-date, demonstrating its commitment to returning capital to shareholders.

The following chart shows Belden’s free cash flow and leverage metrics:

Forward Guidance and Long-term Targets

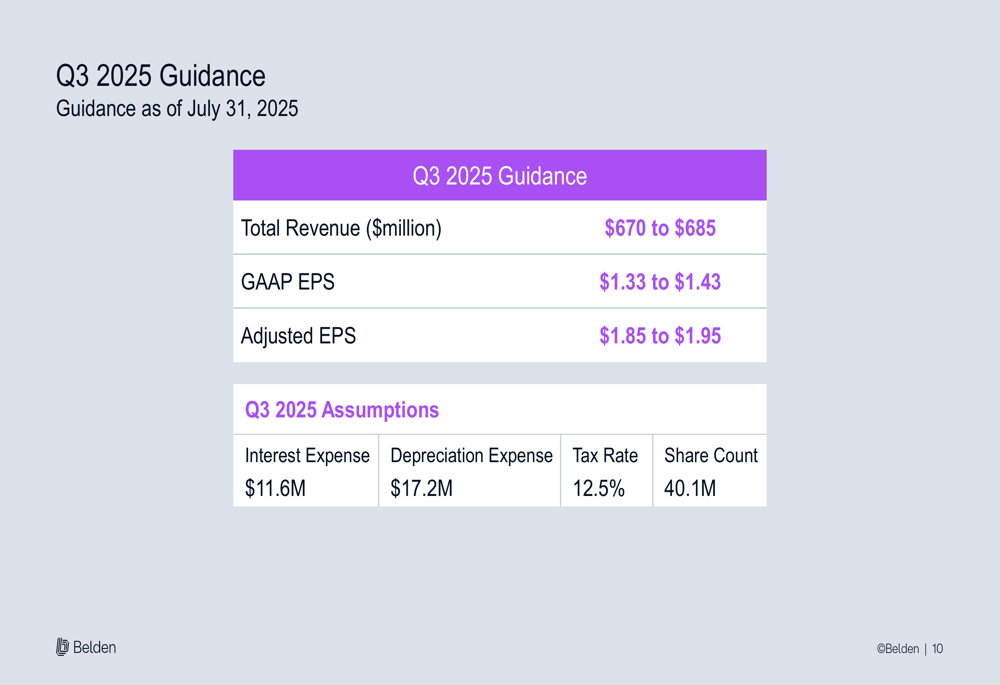

Looking ahead to Q3 2025, Belden provided guidance for:

- Total (EPA:TTEF) revenue of $670 to $685 million

- GAAP EPS of $1.33 to $1.43

- Adjusted EPS of $1.85 to $1.95

This guidance is based on assumptions including interest expense of $11.6 million, depreciation expense of $17.2 million, a tax rate of 12.5%, and a share count of 40.1 million.

As shown in the following guidance table:

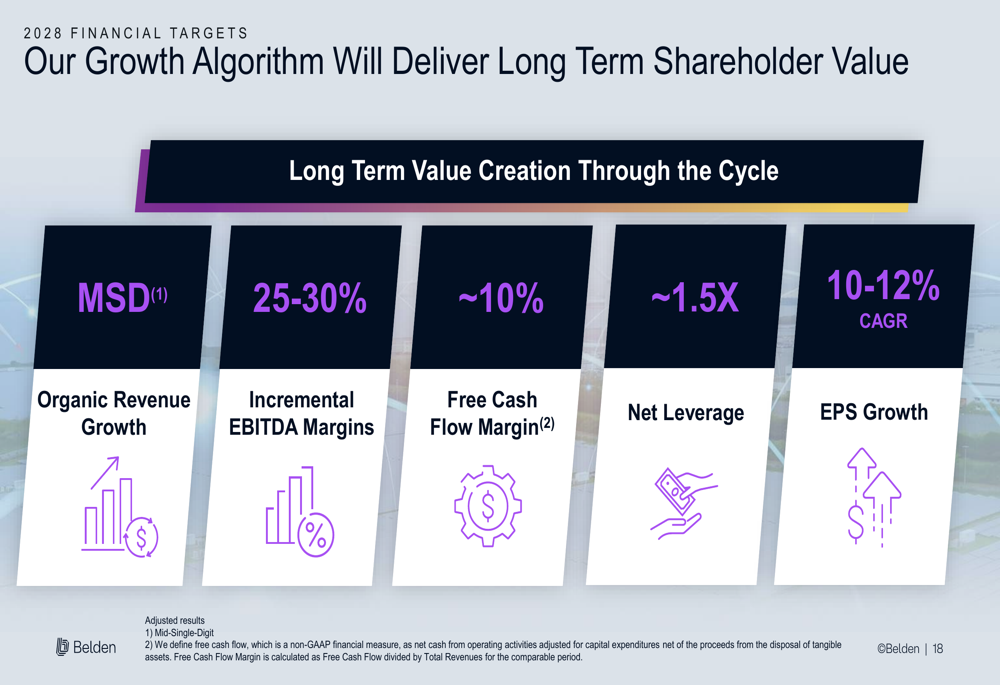

Beyond the near term, Belden reaffirmed its 2028 financial targets, which include mid-single-digit organic revenue growth, 25-30% incremental EBITDA margins, approximately 10% free cash flow margin, net leverage of approximately 1.5x, and 10-12% CAGR EPS growth.

The company’s long-term strategy remains focused on growing its portfolio of networking and data products, advancing solutions capabilities, enhancing growth with selective M&A, and delivering long-term growth in earnings and free cash flow generation.

These targets reflect Belden’s confidence in its strategic direction and ability to capitalize on secular growth trends in its target markets:

Belden’s Q2 2025 results demonstrate continued execution of its strategy, with strong financial performance across both business segments and significant customer wins in key verticals. The company appears well-positioned to benefit from ongoing industrial automation and digital transformation trends, while maintaining its focus on margin expansion and cash flow generation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.