US stock futures inch lower after Wall St marks fresh records on tech gains

Introduction & Market Context

BioFish Holding AS (BFISH) presented its first quarter 2025 results on May 15, showcasing a significant turnaround in financial performance. The Norwegian salmon smolt producer, strategically located in Western Norway’s high-density farming region, has capitalized on growing demand for post-smolt production in the aquaculture industry.

The company’s stock closed at NOK 1.60 on May 14, 2025, near the upper end of its 52-week range of NOK 1.00-1.68, reflecting investor confidence ahead of the quarterly results.

Quarterly Performance Highlights

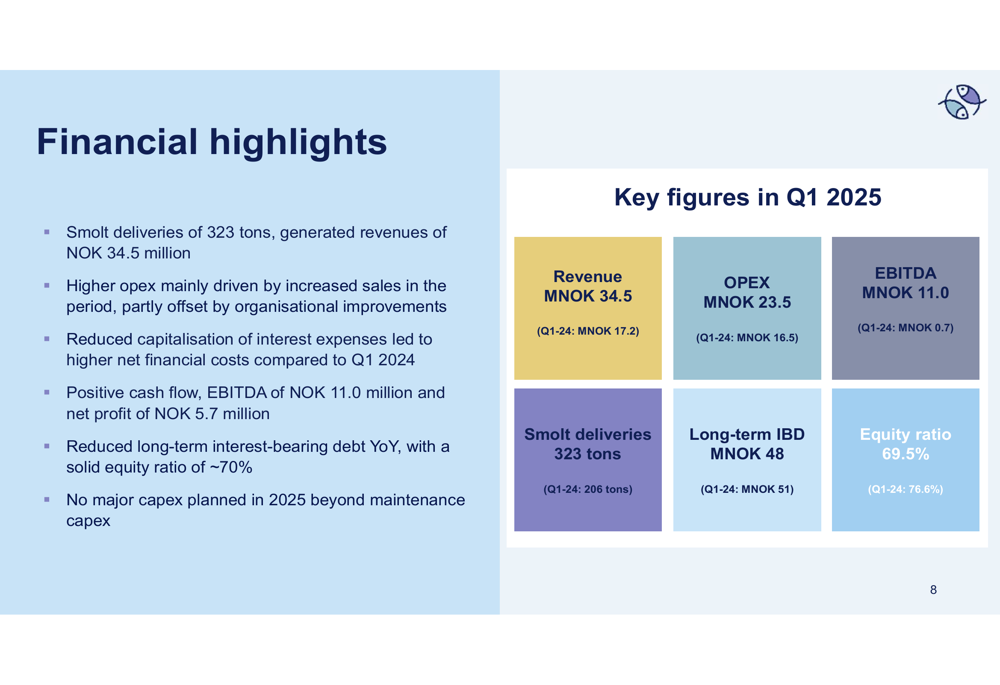

BioFish reported substantial growth in Q1 2025, with revenue more than doubling year-over-year to NOK 34.5 million, compared to NOK 17.2 million in Q1 2024. This growth was primarily driven by a 56.8% increase in smolt deliveries, which reached 323 tons versus 206 tons in the same period last year.

The company also achieved a significant profitability milestone, reporting a net profit of NOK 5.7 million for the quarter, a marked improvement from the NOK 3.8 million loss recorded in Q1 2024.

As shown in the following quarterly highlights:

EBITDA showed remarkable improvement, reaching NOK 11.0 million compared to just NOK 0.7 million in Q1 2024. The company also secured several contracts during the quarter, bringing its total order backlog to 720 tons per year for the 2025-2027 period.

Detailed Financial Analysis

The financial performance demonstrates BioFish’s operational improvements and growing market position. Operating expenses increased to NOK 23.5 million from NOK 16.5 million in Q1 2024, primarily due to higher sales volumes. However, the company maintained strong profitability with an EBITDA margin of approximately 32%.

BioFish has maintained a solid balance sheet with reduced long-term interest-bearing debt of NOK 48 million, down from NOK 51 million a year earlier. The equity ratio remains robust at approximately 70%, providing financial flexibility for future growth.

The company’s detailed financial performance is illustrated in the following slide:

Cash flow turned positive during the quarter, and management noted that no major capital expenditures are planned for 2025 beyond regular maintenance, which should support continued positive cash generation.

Strategic Initiatives & Outlook

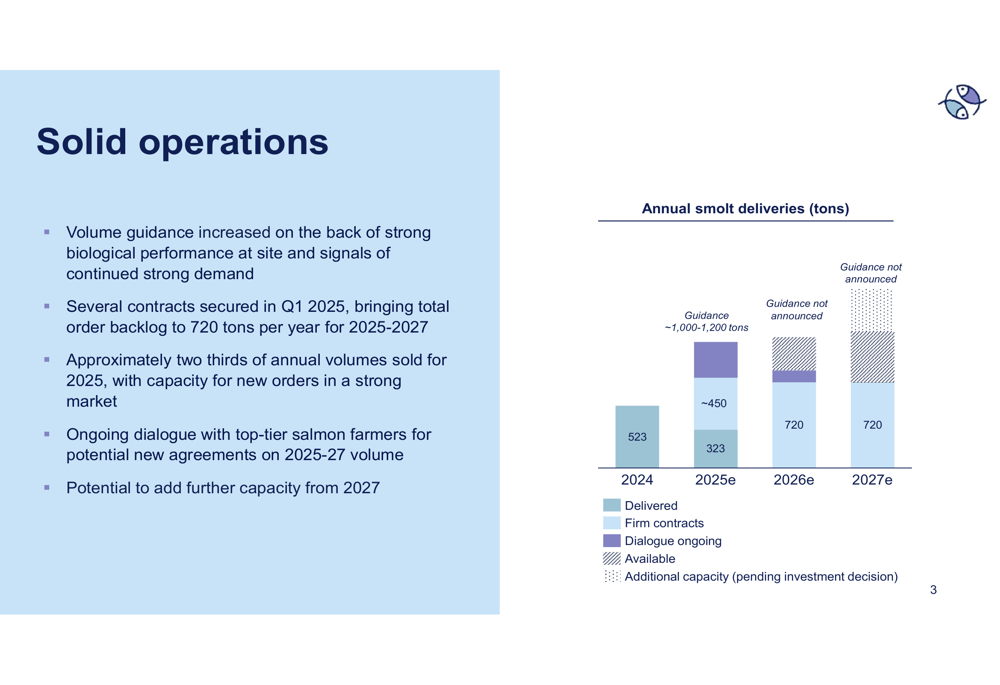

BioFish has increased its volume guidance for 2025 to 1,000-1,200 tons, reflecting strong biological performance and robust market demand. The company disclosed that approximately two-thirds of its annual capacity for 2025 is already committed through firm contracts.

The company’s production facility in Ljones, Western Norway, is strategically positioned in a high farming density region, providing logistical advantages and access to skilled labor. This location allows for shorter transport to sea sites, benefiting fish health and operational efficiency.

The following chart illustrates BioFish’s solid operations and delivery forecast:

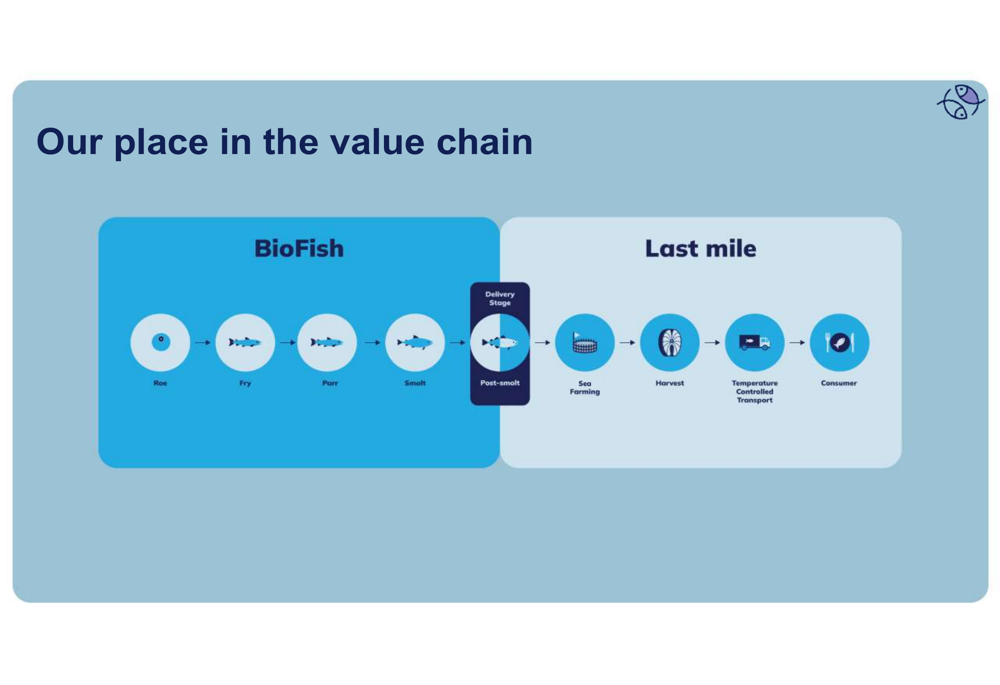

BioFish’s production process spans five stages from hatchery to smolt and post-smolt delivery, positioning the company at a critical juncture in the salmon value chain. The company’s strategic location and specialized focus on high-quality smolt production appear to be yielding positive results in the competitive aquaculture market.

The company’s facility layout and strategic location are highlighted in this image:

Forward-Looking Statements

BioFish announced in January 2025 that it had initiated a strategic review process to explore growth opportunities and increase shareholder value. This process is still ongoing, with updates expected by the end of Q2 2025. Management emphasized that the strategic review will not require capital raising.

The company’s key takeaways and outlook are summarized in the following slide:

Management noted that a recent government white paper was "net positive for producers of high-quality smolt," potentially creating a favorable regulatory environment for BioFish’s operations. The company is also in ongoing dialogue with salmon farmers for potential agreements on 2025-2027 volume, with capacity to add further production from 2027 pending investment decisions.

BioFish’s positioning in the salmon value chain is illustrated in this diagram:

With its improved financial performance, strong order backlog, and strategic initiatives underway, BioFish appears well-positioned to capitalize on the growing demand for high-quality smolt in Norway’s aquaculture industry. Investors will be watching closely for updates on the strategic review process expected later this quarter.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.