German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

Bio-Rad Laboratories Inc (NYSE:BIO) presented its second quarter 2025 financial results on July 31, showing modest revenue growth despite ongoing margin challenges and regional market headwinds. The life sciences and clinical diagnostics company reported a 2.1% year-over-year revenue increase to $652 million, slightly exceeding analyst expectations of $615.2 million.

Despite beating earnings forecasts significantly with an EPS of $2.61 (50.87% above expectations), Bio-Rad’s stock fell 3.25% in aftermarket trading to close at $250.08, reflecting investor concerns about declining margins and mixed segment performance.

Quarterly Performance Highlights

Bio-Rad’s Q2 2025 results revealed a company navigating challenging market conditions with some success. Revenue grew 2.1% year-over-year (1.0% on a currency-neutral basis), while cash flow metrics showed improvement despite margin pressure.

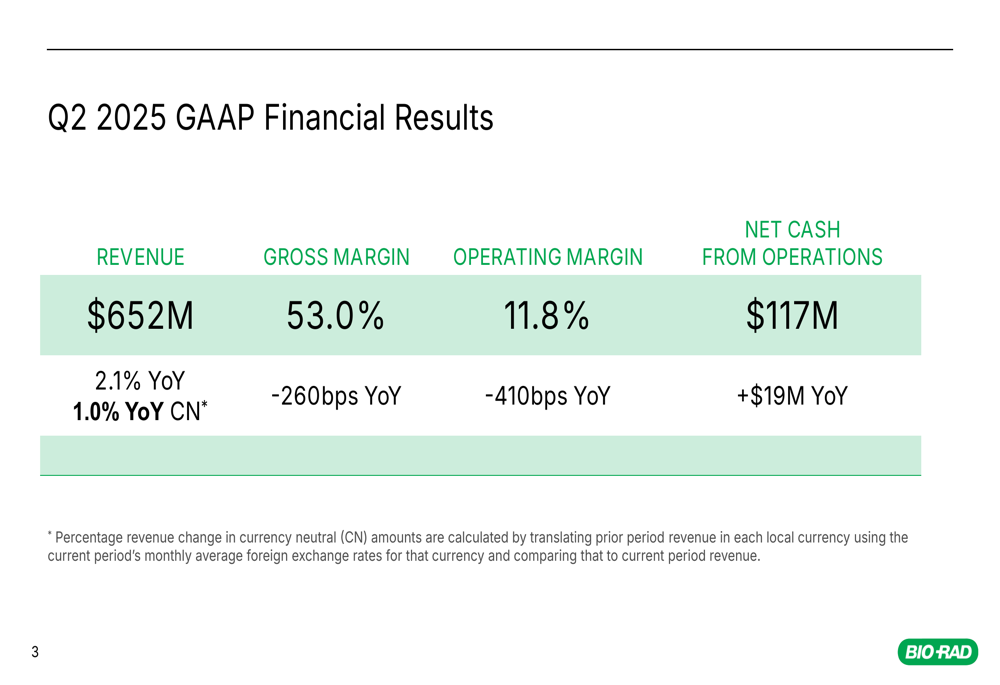

As shown in the following GAAP financial results:

The company’s gross margin declined 260 basis points year-over-year to 53.0%, while operating margin fell more significantly, dropping 410 basis points to 11.8%. Despite these margin challenges, Bio-Rad improved its cash generation, with net cash from operations increasing by $19 million to $117 million compared to the same period last year.

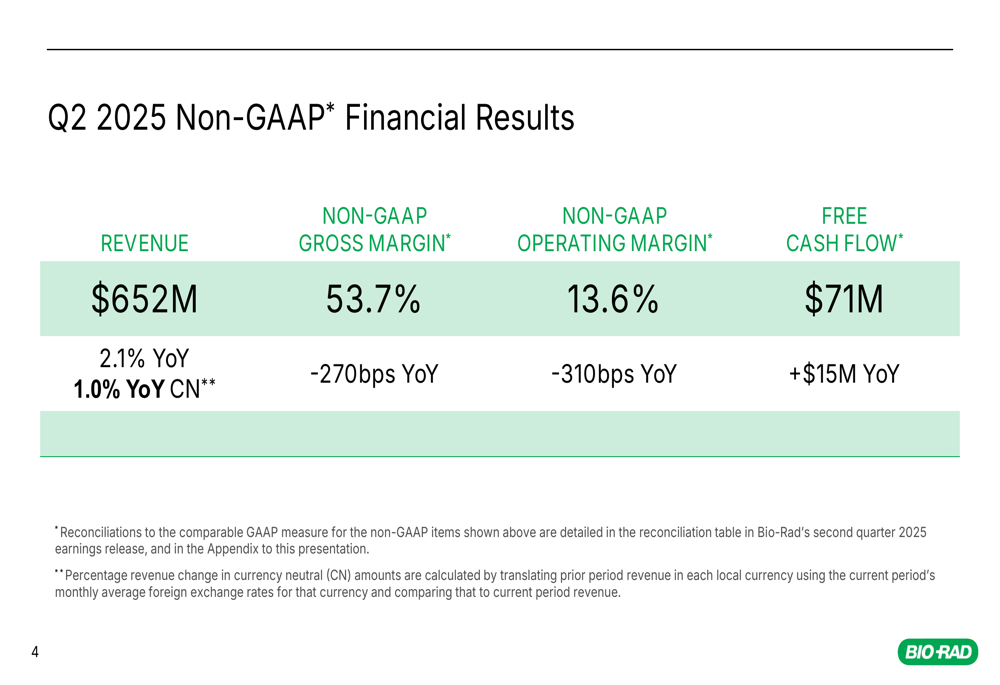

Non-GAAP results painted a similar picture, with slightly better but still declining margins:

Free cash flow showed notable improvement, reaching $71 million for the quarter, up $15 million from Q2 2024. This cash flow improvement comes despite the margin challenges, suggesting effective working capital management.

Segment Analysis

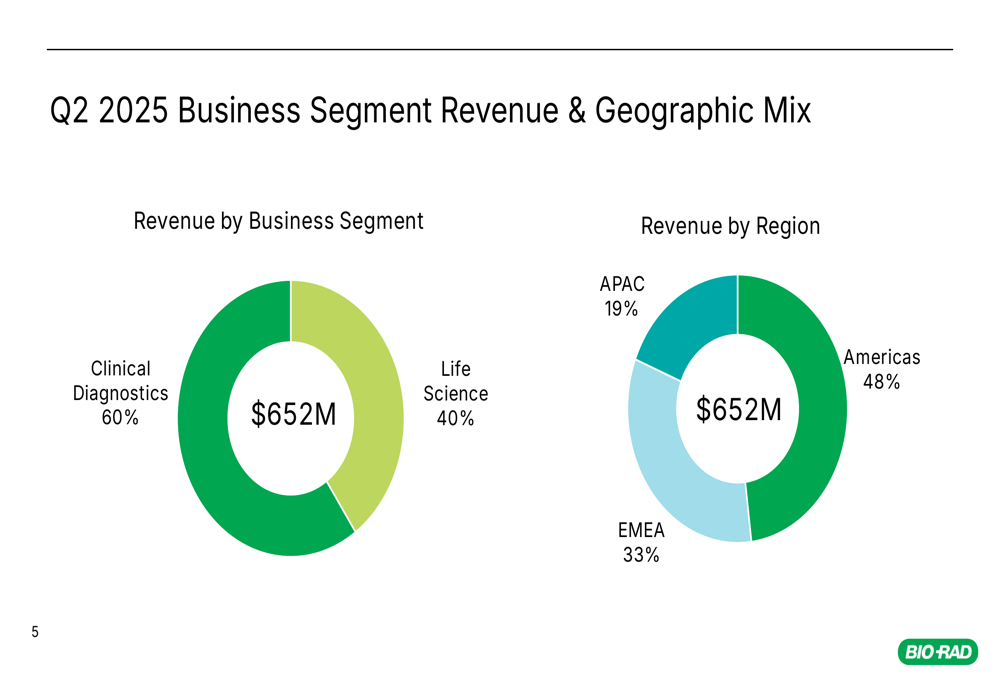

Bio-Rad’s business is divided into two main segments: Clinical Diagnostics (60% of revenue) and Life Science (40% of revenue), with varied performance across geographic regions.

The following chart illustrates this revenue distribution:

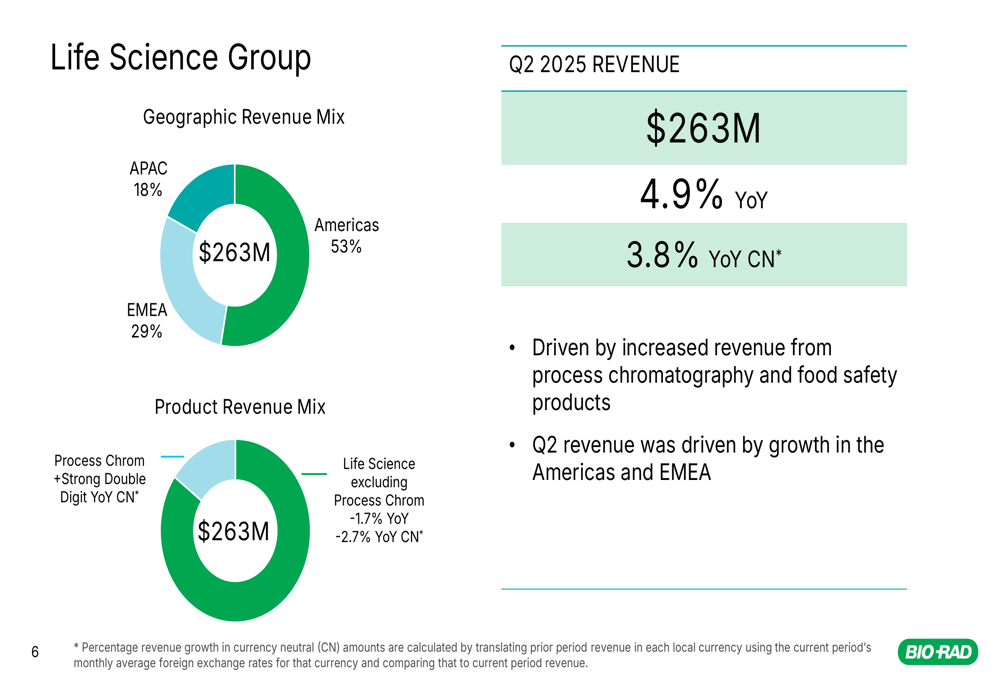

The Life Science segment emerged as the growth driver for the quarter, with revenue increasing 4.9% year-over-year to $263 million (3.8% on a currency-neutral basis). This growth was primarily driven by process chromatography and food safety products, with the Americas and EMEA regions showing the strongest performance.

As detailed in the segment breakdown:

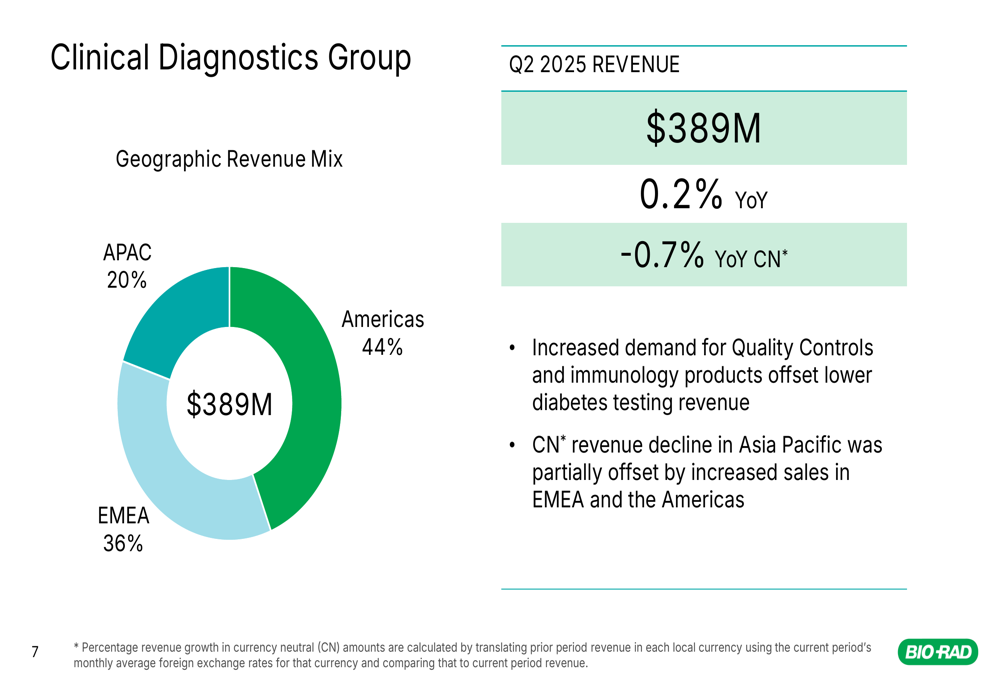

In contrast, the Clinical Diagnostics segment showed minimal growth, with revenue up just 0.2% year-over-year to $389 million, and actually declining 0.7% on a currency-neutral basis. The segment saw increased demand for Quality Controls and immunology products, which helped offset lower diabetes testing revenue.

Geographically, Bio-Rad faced challenges in the Asia Pacific region, particularly in China, where market softness continued to impact results. This aligns with comments from the earnings call, where executives noted ongoing difficulties in the Chinese market and uncertainties in academic research funding.

Balance Sheet and Strategic Investments

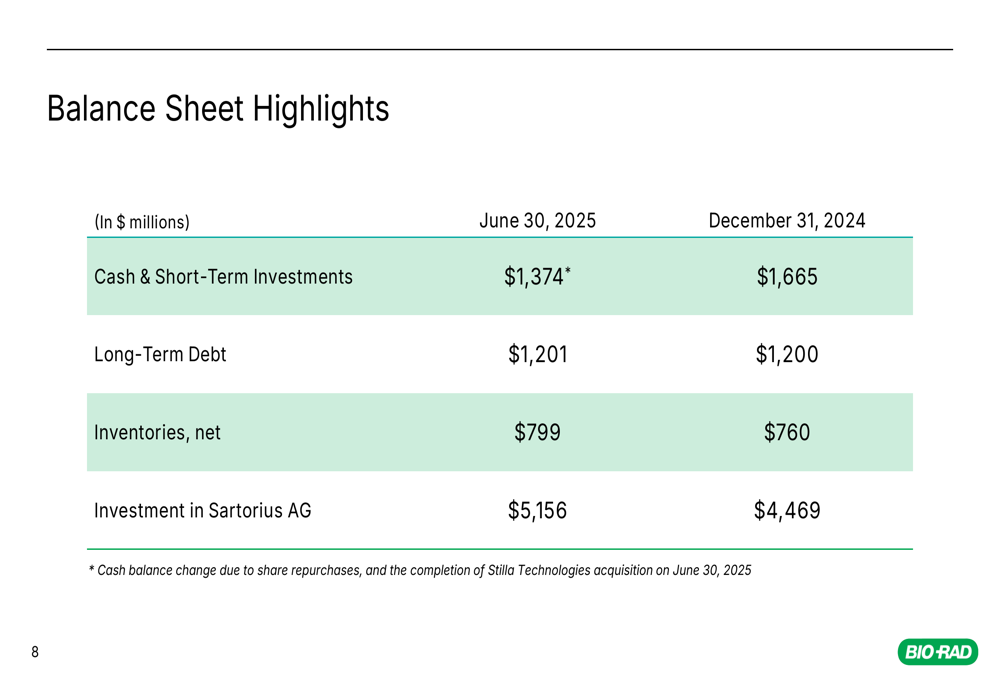

Bio-Rad’s balance sheet showed significant changes in the first half of 2025, most notably a reduction in cash and short-term investments from $1,665 million at the end of 2024 to $1,374 million as of June 30, 2025. This decrease was primarily attributed to share repurchases and the completion of the Stilla Technologies acquisition on June 30, 2025.

The key balance sheet metrics are summarized here:

The company’s investment in Sartorius AG (ETR:SATG) increased substantially to $5,156 million, up from $4,469 million at the end of 2024, representing a significant portion of Bio-Rad’s overall asset value. Long-term debt remained relatively stable at $1,201 million.

The strategic acquisition of Stilla Technologies, completed on the last day of the quarter, signals Bio-Rad’s continued commitment to expanding its digital PCR portfolio, a point emphasized by President and COO John DiVincenzo during the earnings call when he noted, "We’re doing everything possible to drive share and expand overall the market for digital PCR."

Revised Outlook and Guidance

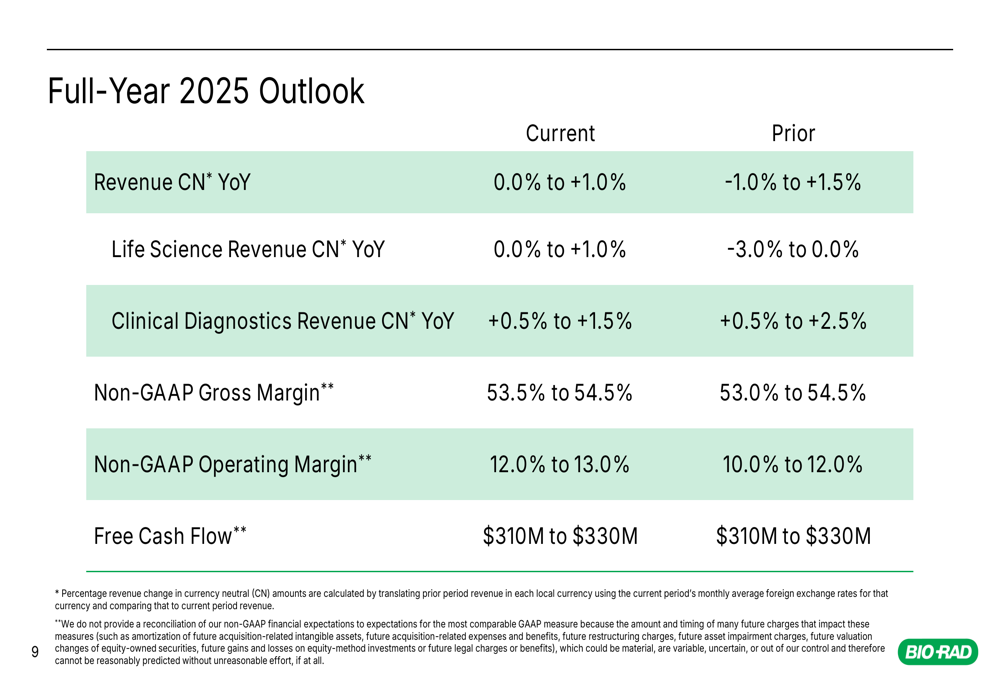

Bio-Rad revised its full-year 2025 outlook, with mixed changes across different metrics. The company narrowed its overall revenue growth forecast to 0.0% to 1.0% on a currency-neutral basis, compared to the previous range of -1.0% to 1.5%.

The detailed outlook revisions are presented here:

Notably, the Life Science segment outlook improved significantly, shifting from an expected decline of up to 3.0% to a new forecast of flat to 1.0% growth. Conversely, the Clinical Diagnostics segment’s upper growth range was trimmed from 2.5% to 1.5%.

The company also raised its non-GAAP operating margin expectations to 12.0% to 13.0%, up from the previous 10.0% to 12.0% range, suggesting improved operational efficiency despite ongoing margin pressures.

Market Reaction and Analyst Perspectives

Despite exceeding both revenue and earnings expectations, Bio-Rad’s stock declined 3.25% in aftermarket trading following the earnings release. The stock has struggled throughout 2025, down 26.35% year-to-date according to available market data.

The negative market reaction likely reflects concerns about several factors: declining gross margins, continued challenges in China, uncertainties in academic research funding, and the modest nature of the company’s growth projections. While Bio-Rad demonstrated resilience in a challenging environment, investors appear focused on the margin pressure and limited growth outlook.

CEO Norman Schwartz emphasized the company’s resilience during the earnings call, stating, "We remain resilient and continue to advance our business on many fronts." However, the market seems to be taking a more cautious view of Bio-Rad’s near-term prospects despite the earnings beat.

With a current stock price well below its 52-week high of $387.99, and trading closer to its 52-week low of $211.43, Bio-Rad faces the challenge of convincing investors that its strategic initiatives and operational improvements will translate into stronger financial performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.